Tax Increment Financing and Major League Venues

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Memphis Women's Basketball History

TABLE OF CONTENTS/QUICK FACTS TABLE OF CONTENTS QUICK FACTS 2012-13 SCHEDULE Table of Contents ...................................................................1 2012-13 Quick Facts ..............................................................1 UNIVERSITY OF MEMPHIS INFORMATION November 3 RHODES COLLEGE (Exh.) Location: .......................................... Memphis, Tenn. MEDIA INFORMATION November 11 GRAMBLING STATE % Founded: ............... 1912 as West Tennessee Normal 2012-13 Roster ......................................................................2 November 21 at UT Arlington Media Information & Policies ................................................3 Enrollment: ..................................................... 22,725 Directions to the Elma Roane Fieldhouse ..............................4 Nickname: ........................................................Tigers November 25 PRAIRIE VIEW A&M Fieldhouse Records ...............................................................5 Colors: .................................................Blue and Gray November 30 at East Tennessee State Directions to FedExForum .....................................................6 Conference: ..................................... Conference USA December 7 UALR FedExForum Records .............................................................7 Arena (Capacity): ...................Elma Roane FH (2,565) Women’s Basketball Multimedia ...........................................8 ...........................................FedExForum (18,400) December -

Comprehensive Annual Financial Report Photos Used with Permission of Pacers Sports & Entertainment Used with Permission of Pacers Photos Indiana Basketball

FINANCIAL SECTION COMPREHENSIVE ANNUAL FINANCIAL REPORT Photos used with permission of Pacers Sports & Entertainment used with permission of Pacers Photos Indiana Basketball Professional basketball came to Indianapolis in 1967 when eight businessmen invested a few thousand dollars apiece to create the Indiana Pacers franchise as a charter member of the American Basketball Association (ABA). The nickname “Pacers” was decided on through a collective decision of the original investors. It was a combination of the state’s rich history with the harness racing pacers and the pace car used for the running of the Indianapolis 500. The Pacers became a member of the National Basketball Association (NBA) in 1976 as a result of the ABA-NBA merger. They originally played in the Indiana State Fairgrounds Coliseum, but moved to the Market Square Arena in downtown Indianapolis in 1974 where they stayed for 25 years. They moved to Bakers Life Fieldhouse in 1999 where they currently reside. Over the years the Pacers have been home to a number of top talent including five Hall of Fame members: Reggie Miller, Chris Mullin, Alex English, Mel Daniels and Roger Brown. The team won three championships while in the ABA and eight division titles so far in the NBA. They were also the Eastern Conference champions in 2000. 2 - State of Indiana - Comprehensive Annual Financial Report Comprehensive Annual Financial Report - State of Indiana - 3 4 - State of Indiana - Comprehensive Annual Financial Report Comprehensive Annual Financial Report - State of Indiana - 5 -

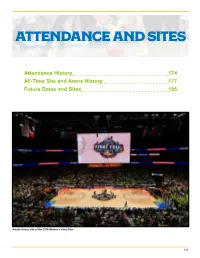

Attendance and Sites

ATTENDANCE AND SITES Attendance History 174 All-Time Site and Arena History 177 Future Dates and Sites 195 Amalie Arena, site of the 2019 Women’s Final Four 173 ATTENDANCE HISTORY 1982-2019 First/Second Round Regionals Finals Totals Year Sessions Total Avg. Sessions Total Avg. Sessions Total Avg. Sessions Total Avg. *Attend. Session *Attend. Session *Attend. Session *Attend. Session 1982 16 32,737 2,046 8 18,656 2,332 2 15,531 7,766 26 66,924 2,574 1983 20 32,876 1,644 8 24,558 3,070 2 16,253 8,127 30 73,687 2,456 1984 15 36,678 2,445 8 36,943 4,618 2 11,537 5,769 25 85,158 3,406 1985 16 44,517 2,782 8 39,042 4,880 2 15,245 7,623 26 98,804 3,800 1986 24 50,780 2,116 8 30,486 3,811 2 15,556 7,778 34 96,822 2,848 1987 24 61,740 2,573 8 28,942 3,618 2 31,230 15,615 34 121,912 3,586 1988 24 82,068 3,420 8 34,507 4,313 2 17,167 8,584 34 133,742 3,934 1989 32 101,848 3,183 8 46,949 5,869 2 18,788 9,394 42 167,585 3,990 1990 32 102,621 3,207 8 49,408 6,176 2 39,490 19,745 42 191,519 4,560 1991 32 109,553 3,424 8 28,590 3,574 2 15,796 7,898 42 153,939 3,665 1992 32 131,097 4,097 8 42,074 5,259 2 24,493 12,247 42 197,664 4,706 1993 32 135,198 4,225 8 63,887 7,986 2 32,282 16,141 42 231,367 5,509 1994 48 212,812 4,434 8 43,750 5,469 2 23,932 11,966 58 280,494 4,836 1995 32 152,968 4,780 8 59,490 7,436 2 36,076 18,038 42 248,534 5,917 1996 32 173,284 5,415 8 54,510 6,814 2 46,582 23,291 42 274,376 6,533 1997 32 158,476 4,952 8 34,019 4,252 2 33,428 16,714 42 225,923 5,379 1998 32 177,423 5,544 8 72,053 9,007 2 35,952 17,976 42 285,428 6,796 1999 -

For Student Success

TRANSFORMING School Environments OUR VISION For Student Success Weaving SKILLS ROPES Relationships 2018 Annual Report Practices to Help All Students Our Vision for Student Success City Year has always been about nurturing and developing young people, from the talented students we serve to our dedicated AmeriCorps members. We put this commitment to work through service in schools across the country. Every day, our AmeriCorps members help students to develop the skills and mindsets needed to thrive in school and in life, while they themselves acquire valuable professional experience that prepares them to be leaders in their careers and communities. We believe that all students can succeed. Supporting the success of our students goes far beyond just making sure they know how to add fractions or write a persuasive essay—students also need to know how to work in teams, how to problem solve and how to work toward a goal. City Year AmeriCorps members model these behaviors and mindsets for students while partnering with teachers and schools to create supportive learning environments where students feel a sense of belonging and agency as they develop the social, emotional and academic skills that will help them succeed in and out of school. When our children succeed, we all benefit. From Our Leadership Table of Contents At City Year, we are committed to partnering Our 2018 Annual Report tells the story of how 2 What We Do 25 Campaign Feature: with teachers, parents, schools and school City Year AmeriCorps members help students 4 How Students Learn Jeannie & Jonathan Lavine districts, and communities to ensure that all build a wide range of academic and social- 26 National Corporate Partners children have access to a quality education that emotional skills to help them succeed in school 6 Alumni Profile: Andrea Encarnacao Martin 28 enables them to reach their potential, develop and beyond. -

Design Considerations for Retractable-Roof Stadia

Design Considerations for Retractable-roof Stadia by Andrew H. Frazer S.B. Civil Engineering Massachusetts Institute of Technology, 2004 Submitted to the Department of Civil and Environmental Engineering In Partial Fulfillment of the Requirements for the Degree of AASSACHUSETTS INSTiTUTE MASTER OF ENGINEERING IN OF TECHNOLOGY CIVIL AND ENVIRONMENTAL ENGINEERING MAY 3 12005 AT THE LIBRARIES MASSACHUSETTS INSTITUTE OF TECHNOLOGY June 2005 © 2005 Massachusetts Institute of Technology All rights reserved Signature of Author:.................. ............... .......... Department of Civil Environmental Engineering May 20, 2005 C ertified by:................... ................................................ Jerome J. Connor Professor, Dep tnt of CZvil and Environment Engineering Thesis Supervisor Accepted by:................................................... Andrew J. Whittle Chairman, Departmental Committee on Graduate Studies BARKER Design Considerations for Retractable-roof Stadia by Andrew H. Frazer Submitted to the Department of Civil and Environmental Engineering on May 20, 2005 in Partial Fulfillment of the Requirements for the Degree of Master of Engineering in Civil and Environmental Engineering ABSTRACT As existing open-air or fully enclosed stadia are reaching their life expectancies, cities are choosing to replace them with structures with moving roofs. This kind of facility provides protection from weather for spectators, a natural grass playing surface for players, and new sources of revenue for owners. The first retractable-roof stadium in North America, the Rogers Centre, has hosted numerous successful events but cost the city of Toronto over CA$500 million. Today, there are five retractable-roof stadia in use in America. Each has very different structural features designed to accommodate the conditions under which they are placed, and their individual costs reflect the sophistication of these features. -

I Spent the Night at the Bass Pro Shops in the Memphis Pyramid and Y'all, It Was Wild

I Spent the Night at the Bass Pro Shops in the Memphis Pyramid and Y'all, It Was Wild April 4, 2019 Bobbie Jean Sawyer This article is part of an ongoing series on Memphis, Tennessee. Growing up in southern Missouri, the Memphis Pyramid always evoked a sense of wonder in me. Who wouldn't love a giant pyramid in the same city as Elvis Presley's delightfully kitschy mansion? It somehow always seemed fitting -- Ancient Egypt had the pharaohs, Memphis has The King. But until recently, the Great American Pyramid mosty meant two things to me: 1) It was one of my very favorite roadside attractions and 2) the place where I saw Disney on Ice in the mid- 90s. I never dreamed I would be spending the night there. And if you told me that the most relaxing and unique hotel stay of my life would be inside that same pyramid, which now houses a giant retail store, I might have been a little skeptical. That all changed earlier this year when I spent two glorious nights at the pyramid, inside a gorgeous, rustic room overlooking a swamp, alligators, a giant fish tank and all the outdoor sporting goods I could ever dream of purchasing. The stunning Big Cypress Lodge is located on the second and third floors of the Memphis Bass Pro Shops and if you're planning a stay in the Bluff City, it should be at the top of your travel list. The Memphis Pyramid re-opened as a Bass Pro Shops in 2015 and the story of how the store wound up inside the pyramid is as wondrous as the 321-foot monument itself. -

Bullock Paper.Pdf (1.7MB)

MAXIMIZING COMMUNITY-BASED DEVELOPMENT OUTCOMES: THE CASE OF RALEIGH’S DOWNTOWN SOUTH PROPOSAL Caylin Bullock A capstone thesis paper submitted to the Faculty Director of the Urban & Regional Planning Program at Georgetown University’s School of Continuing Studies in fulfillment of the requirements for Masters of Professional Studies in Urban & Regional Planning. Project Advisor: Michael Stevens, AICP Academic Advisor: Uwe S. Brandes © Copyright 2019 by Caylin Bullock All Rights Reserved 1 ABSTRACT This paper explores a proposed large mixed-use development project in Raleigh, North Carolina as a case study to identify potential linkages between privately conceived urban development, community benefits, and the corresponding roles played by the private sector, municipalities and community stakeholders. Following a literature review and review of case study precedent practices, research was conducted through unstructured interviews with public and private stakeholders in Raleigh and analysis of project-based scenarios. This paper argues that when receiving proposals, cities must embrace partnerships to maximize positive community-based development outcomes. KEYWORDS Community Benefit Agreement (CBA), Equitable Development, Development Agreement, Public-Private Partnerships, Stadium Development, Raleigh, North Carolina RESEARCH QUESTIONS What are national best practices in the finance and development of large-scale mixed-use urban development projects comparable to the Downtown South proposal? In the case of Raleigh, how might the municipality more aggressively position its actions to ensure long-term equitable development outcomes for historically underserved community stakeholders in close proximity to the project? How might Raleigh institutionalize a project-based agreement as a binding and durable governance structure for future development projects? 2 TABLE OF CONTENTS LIST OF TABLES ......................................................................................................................... -

The Mid-South Coliseum 996 Early Maxwell Boulevard Memphis, Shelby County, Tennessee

The Mid-South Coliseum 996 Early Maxwell Boulevard Memphis, Shelby County, Tennessee Text by Carroll Van West, 2000 Listed in the National Register of Historic Places, the Mid-South Coliseum has extraordinary local significance in the modem history of entertainment/recreation and the music history of Memphis. Developed and constructed between 1960 and 1964, the Mid-South Coliseum was the first public auditorium in Memphis to be planned as an integrated facility, rather than a so-called "separate but equal" segregated building. Performances before integrated audiences occurred there as soon as the building opened in 1964, and its period of significance extends to 1974, when Elvis Presley gave his first Memphis concerts in over a decade at the coliseum and recorded a live album there It is the only extant building In Memphis where such significant musical groups as The Beatles, The Stax-Volt Record Revue, Ike and Tina Turner, The Who, Led Zepellin, The Rolling Stones, James Brown, and Elvis Presley performed during their period of significance in American popular music and as such, the coliseum served as a center for cultural expression among Memphis youth, both white and black. Building a Modern, Integrated Coliseum in an Era of Racial Conflict Planning for a new, modern auditorium for the Mid-Sout Fairgrounds in Memphis began in late 1959. Brown v. Board of Education (1954) had been the law of the land for five years, but Memphis, like most other major Southern cities, had moved only slightly toward anything but token compliance with the end of the legal justification for Jim Crow segregation. -

NHL MEDIA DIRECTORY 2012-13 TABLE of CONTENTS Page Page NHL DIRECTORY NHL MEDIA NHL Offices

NHL MEDIA DIRECTORY 2012-13 TABLE OF CONTENTS PAGE PAGE NHL DIRECTORY NHL MEDIA NHL Offices ...........................................3 NHL.com ...............................................9 NHL Executive .......................................4 NHL Network .......................................10 NHL Communications ............................4 NHL Studios ........................................11 NHL Green ............................................6 NHL MEDIA RESOURCES .................. 12 NHL MEMBER CLUBS Anaheim Ducks ...................................19 HOCKEY ORGANIZATIONS Boston Bruins ......................................25 Hockey Canada .................................248 Buffalo Sabres .....................................32 Hockey Hall of Fame .........................249 Calgary Flames ...................................39 NHL Alumni Association ........................7 Carolina Hurricanes .............................45 NHL Broadcasters’ Association .........252 Chicago Blackhawks ...........................51 NHL Players’ Association ....................16 Colorado Avalanche ............................56 Professional Hockey Writers’ Columbus Blue Jackets .......................64 Association ...................................251 Dallas Stars .........................................70 U.S. Hockey Hall of Fame Museum ..249 Detroit Red Wings ...............................76 USA Hockey Inc. ...............................250 Edmonton Oilers ..................................83 NHL STATISTICAL CONSULTANT Florida -

4X GRAMMY® AWARD WINNING DUO for KING & COUNTRY TO

FOR IMMEDIATE RELEASE July 6th, 2021 4x GRAMMY® AWARD WINNING DUO for KING & COUNTRY TO EMBARK ON FIRST ARENA TOUR IN TWO YEARS WITH RELATE | THE 2021 FALL TOUR Click Here to Download Admat Nashville, TENN. – After setting an industry record with six consecutive No. 1 hits, 4x GRAMMY Award winning, platinum-selling duo and Curb | Word Entertainment recording artist for KING & COUNTRY are announcing RELATE | The 2021 Fall Tour. After wowing crowds in 2020 with their Pollstar recognized drive-in theater performances, this 24-date trek will see Joel and Luke Smallbone return to the road in compelling fashion, arranging their electrifying live spectacle for arenas and amphitheaters. BRAND NEW, never performed songs from an upcoming studio project will be featured on the tour’s setlist, along with selections from the duo’s nine No. 1 hits – including “joy.,” “Fix My Eyes,” and the cross-genre multi-week smash “God Only Knows.” This will be fans’ first chance to hear new music straight from the source. for KING & COUNTRY kick things off in Toledo, Ohio on October 7th before wrapping up in Rochester, Minnesota on November 14th. Ticket pre-sale for RELATE | The 2021 Fall Tour starts tomorrow at 10am local time, to access the pre-sale enter the code “RELATE” at the link HERE. Tickets will go on sale to the public July 9th at 10am local time, click HERE for more information. “The thought of hitting the road and seeing you again is a thrilling one,” Joel and Luke Smallbone share in a statement. “Since we were last together, we’ve been hard at work writing and recording new music, which is going to make ‘RELATE | The 2021 Fall Tour’ a particularly special one. -

214.222.3687 2500 Victory Avenue Dallas,Tx 75219 Oct. 1, 2015 for Immediate Release Melissa K

Oct. 1, 2015 For Immediate Release Melissa Koehler 214.665.4218 [email protected] AMERICAN AIRLINES CENTER, DALLAS STARS AND DALLAS MAVERICKS ANNOUNCE MULTI-YEAR PARTNERSHIP WITH PIZZA HUT DALLAS, Texas - American Airlines Center, Dallas Stars and Dallas Mavericks announced today a multi-year agreement with Pizza Hut, designating the world's largest pizza company as the Official Pizza Partner of all three properties. As part of its partnership, Plano, Texas-based Pizza Hut will have use of team and arena trademarks across various marketing channels, including branded content, advertising and promotional materials. In addition to the marketing rights, Pizza Hut will have six in-arena concession stands within American Airlines Center, with four located on the plaza level and two on the terrace level. The stands will debut a premium 9-inch Hand-Tossed Pizza, available in cheese, pepperoni or sausage, as well as classic breadsticks and an Ultimate Hershey's Chocolate Chip Cookie. "Cultivating strong partnerships with North Texas-based companies has always been a top priority of the Dallas Stars business strategy," Dallas Stars Owner Tom Gaglardi said. "We are excited to bring a locally-based brand like Pizza Hut to American Airlines Center that we know that will provide our fans with a quality product. For almost 60 years, Pizza Hut has been one of the most recognizable and successful restaurant franchises around the world and we look forward to working with them for many seasons to come." "Pizza Hut is one of the most beloved brands in the world and to have them with us as our official pizza partner is very exciting and something we cannot wait to share with our fans," Dallas Mavericks Owner Mark Cuban said. -

Amway Center the Orlando Magic Developed the Amway Center, Which Will Compete to Host Major National Events, Concerts and Family Shows

About Amway Center The Orlando Magic developed the Amway Center, which will compete to host major national events, concerts and family shows. The facility opened in the fall of 2010, and is operated by the City of Orlando and owned by the Central Florida community. The Amway Center was designed to reflect the character of the community, meet the goals of the users and build on the legacy of sports and entertainment in Orlando. The building’s exterior features a modern blend of glass and metal materials, along with ever-changing graphics via a monumental wall along one façade. A 180-foot tall tower serves as a beacon amid the downtown skyline. At 875,000 square feet, the new arena is almost triple the size of the old Amway Arena (367,000 square feet). The building features a sustainable, environmentally-friendly design, unmatched technology, featuring 1,100 digital monitors and the tallest, high-definition videoboard in an NBA venue, and multiple premium amenities available to all patrons in the building. Every level of ticket buyer will have access to: the Budweiser Baseline Bar and food court, Club Restaurant, Nutrilite Magic Fan Experience, Orlando Info. Garden, Gentleman Jack Terrace, STUFF’s Magic Castle presented by Club Wyndham and multiple indoor-outdoor spaces which celebrate Florida's climate. Media Kit Table of Contents Enter Legend Public/Private Partnership Fact Sheet By the Numbers Amenities for All Levels Technology LEED: Environmentally-Friendly Corporate Partnerships Jobs in Tough Times Commitment to Parramore Transportation/Parking Concessions Arts and Culture Construction/Design Arena Maps Media Contacts: Joel Glass Heather Allebaugh Tanya Bowley Orlando Magic City of Orlando Amway Center VP/Communications Press Secretary Marketing Manager 407.916-2631 407.246.3423 407.440.7001 [email protected] [email protected] [email protected] AmwayCenter.com **For media information: amwaycenter.com/press-room Amway Center: Enter Legend AmwayCenter.com From a vision to blueprints to reality.