Submission by Visa Inc. Regarding the Payment System Board of The

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Public Bank Unionpay Lifestyle Debit Card Product Disclosure Sheet

PRODUCT DISCLOSURE SHEET Public Bank Berhad (6463-H) Read this Product Disclosure Sheet before you PB Visa/MasterCard Lifestyle Debit – Generic decide to take up the PB Visa/MasterCard/Union Pay Lifestyle Debit. Be sure to also read the PB Visa/MasterCard Lifestyle Debit – Basic general terms and conditions. Savings Account/Basic Current Account PB UnionPay Lifestyle Debit – PB UnionPay Savings Account Date: 1. What is this product about? PB Visa/MasterCard/UnionPay Lifestyle Debit is a two-in-one card combining Visa/MasterCard/ UnionPay debit card and ATM functions. The card is linked to the Savings Account/Current Account/Basic Savings Account/Basic Current Account/PB UnionPay Savings Account (“Banking Account”) of the individual and any expenditure will be deducted directly from the Banking Account. This is a PB Visa/MasterCard/UnionPay Lifestyle Debit, a payment instrument which allows you to pay via a direct deduction of the cost for goods and services from your Banking Account at participating retail and service outlets. You are required to maintain a Banking Account with us, to be linked to your PB Visa/MasterCard/UnionPay Lifestyle Debit. If you close your Banking Account maintained with us, your PB Visa/MasterCard/UnionPay Lifestyle Debit will be automatically cancelled. 2. What are the fees and charges I have to pay? (i) Annual Fee x Generic/PB UnionPay Savings Account: RM8.00 x Basic Savings Account/Basic Current Account: Waived (subject to eight (8) ATM cash withdrawals and six (6) over-the-counter withdrawals per month*) *Note: Fee for exceeding the threshold will be RM1.00 per transaction. -

New Debit Card Solutions At

New Debit Card Solutions Debit Mastercard and Visa Debit are ready Swiss Banking Services Forum, 22 May 2019 Philippe Eschenmoser, Head Cards & A2A, Swisskey Ltd Maestro/V PAY Have Established Themselves As the “Key to the Account” – Schemes, However, Are Forcing Market Entry For Successor Products Response from the Maestro and V PAY are successful… …but are not future-capable products schemes # cards Maestro V PAY on Lower earnings potential millions8 for issuers as an alternative payment traffic products (e.g. 6 credit cards, TWINT) Issuer 4 V PAY will be 2 decommissioned by VISA Functional limitations: in 20211 – Visa Debit as 0 • No e-commerce the successor 2000 2018 • No preauthorizations Security and stability have End- • No virtualization proven themselves customer High acceptance in CH and Merchants with an online MasterCard is positioning abroad in Europe offer are demanding an DMC in the medium term online-capable debit as the successor to Standard product with an Merchan product Maestro integrated bank card t 2 1: As of 2021 no new V PAY may be issued TWINT (Still) No Substitute For Debit Cards – Credit Cards With Divergent Market Perception TWINT (still) not alternative for debit Credit cards a no alternative for debit Lacking a bank card Debit function Limited target group (age, ~1.1 M 1 ~10 M. creditworthiness...) Issuer ~48.5 k ~170 k1 No direct account debiting DMC/ Visa Debit Potentially high annual fee End-customer Lower customer penetration Banks and merchants DMC/ P2P demand an online- Higher costs Merchant Visa Debit -

TD Generation Union Pay Guide

TD Generation UnionPay Guide For the TD Generation • All-in-One, HSPA, WiFi • Portal with PINpad • Portal 2 with PINpad COPYRIGHT © 2016 by The Toronto-Dominion Bank This publication is confidential and proprietary to The Toronto-Dominion Bank and is intended solely for the use of Merchant customers of TD Merchant Solutions. This publication may not be reproduced or distributed, in whole or in part, for any other purpose without the written permission of an authorized representative of The Toronto-Dominion Bank. NOTICE The Toronto-Dominion Bank reserves the right to make changes to specifications at any time and without notice. The Toronto-Dominion Bank assumes no responsibility for the use by the Merchant customers of the information furnished in this publication, including without limitation for infringements of intellectual property rights or other rights of third parties resulting from its use. Contents Who should use this guide? .....................................................1 What is UnionPay? .................................................................................. 1 How do I identify a UnionPay card? ....................................................... 1 UnionPay card types ............................................................................... 1 Financial Transactions ............................................................2 Transaction requirements ......................................................................2 PIN entry ............................................................................................................2 -

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S

Credit Cards American Express Company 24-Hour Number: (800) 528-2121 (U.S. and Canada) American Express Cards include: Personal Green (pictured), Gold, Platinum, Corporate Green (pic - tured), Corporate Gold, Corporate Platinum, Corpo - rate Optima, Optima, Optima Gold, Purchasing Card, American Express Blue (pictured), Green and Gold Rewards, and more. American Express also issues co-branded cards, including Hilton, Delta SkyMiles (pictured), ITT Sheraton Club Miles, and more. American Express issues multiple styles of prepaid cards. Gift Cards (4 are pictured) can be variable load or pre-denominated ranging from $25 to $3,000. Gift Cards are not reloadable and can be personalized or issued anonymously. Reloadable prepaid cards are also available in various styles and offer different functionality. Serve and Bluebird prepaid cards are multifunction cards with many new features such as bill pay, check writing, and funds transfer. All prepaid cards have the word “PREPAID” printed on either the front or back of the card. Account numbers are 15 digits, begin with 37 or 34, and are sequenced 4-6-5. UV light reveals large “AMEX” and phosphorescence on the face of each card, excluding the Gift Card. The Centurion or the American Express Blue Box appears on most Amer - ican Express cards. To establish the validity of a card, or determine its status, please call (866) 375-3684. 98 Credit Cards Diners Club International ® 2500 Lake Cook Rd. Riverwoods, IL 60015 Security Contacts: Law Enforcement Phone Line: 1-800-347-3083 for law enforcement officers Merchant Code 10 Authorization: 1-800-347-1111 for suspicious transactions Diners Club ® account numbers start with 36 or 55. -

Virtual Debit Cards and Consumer Protection

Virtual debit cards and consumer protection RESEARCH REPORT Produced by Option consommateurs and presented to Industry Canada’s Officer of Consumer Affairs June 2014 Virtual debit cards and consumer protection Option consommateurs received funding for this report under Industry Canada’s Program for Non-Profit Consumer and Voluntary Organizations. The opinions expressed in the report are not necessarily those of Industry Canada or of the Government of Canada. Reproduction of limited excerpts of this report is permitted, provided the source is mentioned. Its reproduction or any reference to its content for advertising purposes or for profit, are strictly prohibited, however. Legal Deposit Bibliothèque nationale du Québec National Library of Canada ISBN: 978-2-89716-017-3 Option consommateurs Head Office 50, rue Ste-Catherine Ouest, Suite 440 Montréal (Québec) H2X 3V4 Tel.: 514 598-7288 Fax: 514 598-8511 Email: [email protected] Website: www.option-consumers.org Option consommateurs, 2014 ii Virtual debit cards and consumer protection Table of Contents Option consommateurs ................................................................................................................... iv Acknowledgements .......................................................................................................................... v Summary .......................................................................................................................................... vi 1. Introduction .................................................................................................................................7 -

Use Your VISA Debit/ATM Card for Purchases and Cash Withdrawa

6. Limitations on dollar amounts and frequencies of DEBIT CARD AGREEMENT & DISCLOSURE STATEMENT transactions: The following limitations apply to the use of the card. VISA DEBIT/ATM CARD In this Agreement and Disclosure Statement, the words “you” and “your” You may make withdrawals up to the amount in your share draft mean each and all of those who agree to be bound by this “agreement”; account, but not to exceed $500 per day at ATMs, $1500 POS daily “card” means the SUNY Geneseo Federal Credit Union debit card and any transactions, and a limit of 11 daily transactions. The card that works like a check- only better! duplicates, renewals, or substitutions the Credit Union issues to you, 7. Charges for transactions from the Credit Union: There are Use your VISA Debit/ATM card for purchases and “account” means the account designated on the application for your debit cash withdrawals anywhere the VISA logo is no annual fees. Monthly, members receive two free ATM withdrawals card; “Credit Union” means the Credit Union whose name appears on the on our surcharge free machines. Any ATM transactions thereafter will agreement or anyone whom the Credit Union transfers the agreement, and displayed! be charged a $1.00 Credit Union fee. All transactions processed On “transaction” means the use of the account number on the card, Personal . ATM machines other than those specified by the Credit Union will be Identification Number (PIN), or signature when required, to perform a subject to a machine charge. The Credit Union reserves the right to transaction with the card. -

EFTPOS and Visa Debit

1 Margaret Street DX 10271 Telephone Sydney NSW 2000 Sydney Stock Exchange 02-8299 9000 GPO Box 4720 Internet Facsimile Sydney NSW 2001 www.cu.net.au 02-8299 9607 29 April 2005 Dr John Veale Head of Payments Policy Reserve Bank of Australia GPO Box 3947 Sydney NSW 2001 By e-mail: [email protected] Dear Dr Veale EFTPOS and Visa Debit This submission by Credit Union Services Corporation (Australia) Ltd (CUSCAL) is made in response to the Reserve Bank of Australia (RBA) February 2005 consultation document Reform of the EFTPOS and Visa Debit Systems in Australia. CUSCAL is the leading industry body for credit unions. CUSCAL represents 144 of Australia’s 167 credit unions, provides credit unions with a range of banking and commercial services, and acts for and on behalf of our customers in accessing the payments systems. Credit unions play an important role in the Australian retail banking sector. As mutual, member-focused institutions, credit unions offer a high quality and affordable range of financial and banking services to more than three million members. The different kind of banking that credit unions offer is demonstrated not just in the very high satisfaction ratings1 that the industry continues to record, but also in tangible value delivered to members. In 2004, analysis conducted by CANNEX showed that credit unions are delivering $110 per year in additional ‘member value’ to their customers through interest rates and fees. This value dividend is in addition to the average $70 per year added to retained earnings that is ultimately returned in the form of better products and services. -

Merchant Transactions Through Debit Cards – Costs and Prices

http://dspace.library.iitb.ac.in/jspui/handle/100/25218 IIT Bombay Technical Report (September 2020) Merchant transactions through debit cards – costs and prices Ashish Das Department of Mathematics Indian Institute of Technology Bombay Mumbai-400076, India Indian Institute of Technology Bombay Powai, Mumbai-400 076, India Merchant transactions through debit cards Merchant transactions through debit cards Merchant transactions through debit cards – costs and prices* Ashish Das Department of Mathematics, Indian Institute of Technology Bombay, Mumbai 400076 September 22, 2020 Executive Summary 1. To promote small ticket debit card merchant transactions up to Rs 2000, the government during the calendar years 2018 and 2019 made merchant discount rate (MDR) zero for the merchants, and provided banks a monetary support, towards MDR, @ 0.4%. In contrast, effective January 1, 2020, the government made MDR zero for every transaction using RuPay debit cards alone. Neither merchants nor the government paid the banks any MDR for such merchant transactions. However, banks were allowed to impose MDR onto the merchants for every transaction using mastercard/VISA debit cards. The cost to merchants 2. For the period January-July 2020, with about Rs 3.3 lakh crore1 worth of debit card merchant transactions, the government has done away with the merchant’s zero MDR regime on ticket sizes up to Rs 2000, for transactions that were done through mastercard/VISA debit cards. A simple projection implies that merchants would be burdened in the calendar year 2020 in the range of Rs 1000 crore to Rs 2300 crore depending upon the MDR ranging between 0.4% and 0.9% for mastercard/VISA’s sub Rs 2000 ticket transactions, as against nil burden in calendar years 2018 and 2019. -

Visa Debit Card Disclosure

VISA DEBIT CARD DISCLOSURE VISA CHECK CARD -point of sale transactions. You may access your share draft accounts to purchase goods (in person or by phone), pay for services (in person or by phone), get cash from any merchant permitting or a participating financial institution, and do anything that you can do with a traditional credit card (that a participating merchant will accept). Point-of-Sale Transactions may include restrictions on frequency and dollar amounts or could include surcharges, as per the individual merchant’s rule. Other limitations enforced by Visa and by our Credit Union state that: You may not exceed $1,500.00 in signature based transactions per day. You may withdraw cash or make PIN based purchases up to $200.00 per day. Point-of-sale or ATM cash withdrawals that will take your account into a negative balance, will be declined unless you have opted to have Courtesy Pay. If you have charges or withdrawals covered by Courtesy Pay, you will be charged $35.00 for each applicable transaction. When a deposit is made at an ATM, certain holds will be placed until the funds have been verified. In any instance, there will be a $30.00 fee for ATM deposits made with empty envelopes, or amounts less than the original transaction amount. TRANSACTION LIMITATIONS – Due to federal regulations, Share Savings accounts may not have more than a total of 6 withdrawals or transfers to a third party by means of a preauthorized, automatic, or computer transfer or similar order, each month. This includes Visa Check Card and electronic transfer transactions. -

The Evolving Landscape of Payments – Technology and Security

The Evolving Landscape of Payments – Technology and Security Scott Broughton, Senior Vice President ICBA Bancard Washington, DC Agenda • EMV After affects – what’s the latest? • Payment Tokenization – Securing Payments • Mobile Payments – Rapidly making a difference • P2P Payments – Faster Payments are here Consumers are changing how they shop… Connecting through more channels and devices. New consumer …but increase interaction points the complexity are growth of managing opportunities… fraud. “Omni-channel” Source: ©2016 MasterCard. Proprietary 3 EMV-Chip Technology What have we seen so far? • Over 62% of US credit cards now have chips. • Over 1.4 million merchant locations are accepting EMV cards • Counterfeit fraud is shifting away from chip merchants as predicted • Card not present fraud is up • Consumers complain about slow transactions EMV – Where are we now? How’s Washington doing? • Over 70% penetrated – one of the highest states in the country • Only 25% - 29% merchant locations accept chip cards (as of July 2016) Source: Visa, Inc. As of July 2016 How Quick Chip for EMV works at the POS Remove card when prompted. Insert the card face up, Follow prompts on screen Processing should take chip end first to finalize transaction 2 seconds or less 1 2 3 Insert Remove Follow card card prompts POS = Point-of-Sale 8 | Quick Chip for EMV and U. S. EMV Adoption Update | July 19, 2016 Visa Confidential How Quick Chip for EMV processing works behind the scenes As with magnetic stripe processing, the cardholder can insert the card at any time during the check-out process Quick Chip processing Cardholder Insert card Store chip data in terminal Remove card Finalize amount Request authorization Receive approval leaves $12.34 Standard chip processing Cardholder Insert card Store chip data in terminal Finalize amount Request authorization Receive approval Remove card leaves $12.34 9 | Quick Chip for EMV and U. -

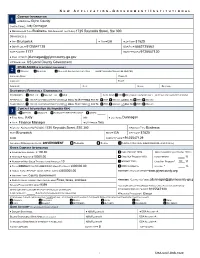

0 New Location

N EW A PPLICATION- G OVERNMENT/INSTITUTIONAL COMPANY INFORMATION 1 ♦DBA NAME: CONTACT NAME: ♦DBA ADDRESS TYPE: ♦ DBA ADDRESS1 (NO PO BOX): DBA ADDRESS 2: ♦CITY: ♦ STATE ♦ZIP CODE: ♦DBA PHONE #: DBA FAX #: DATE FOUNDED: MOBILE PHONE #: ♦EMAIL ADDRESS: CIP EXEMPTION: OTHER ADDRESS (IF DIFFERENT THAN ABOVE ) 2 MAILING SHIPPING SEE ALSO SPECIAL INSTRUCTIONS (MORE THAN ONE OPTION MAY BE SELECTED) LOCATION NAME: PHONE #: CONTACT: FAX #: ADDRESS: CITY: STATE: ZIP CODE: STATEMENTS/ RETRIEVALS /CHARGEBACKS STATEMENTS: DBA OR MAILING OR W-9 AUTO SEND: YES NO (CHAIN COMPANIES ONLY – MUST INCLUDE CHAIN SET UP FORM) RETRIEVALS: ONLINE CASE MANAGEMENT (OCM) OR EMAIL TO: OR FAX TO: DBA MAILING OR MAIL TO: DBA MAILING CHARGEBACKS: ONLINE CASE MANAGEMENT (OCM) OR EMAIL TO: OR FAX TO: DBA MAILING OR MAIL TO: DBA MAILING CONTACT INFORMATION (AUTHORIZED REP) 3 ♦ OFFICER MANAGER AUTHORIZED REPRESENTATIVE OTHER: ♦FIRST NAME: MN: ♦LAST NAME: ♦TITLE: ♦US PERSON: CONTACT ADDRESS (NO PO BOX): ADDRESS TYPE: CITY: STATE: ZIP CODE: DOB: CONTACT PHONE #: INDIVIDUAL ID EXEMPTION CLASS: GOVERNMENT FEDERAL STATE LOCAL (POLITICAL SUBDIVISION OF A US STATE) OTHER COMPANY INFORMATION ♦AVERAGE SALE AMOUNT: $ CARD PRESENT 100% OMNI COMMERCE (MUST TOTAL 100%) ♦HIGH SALE AMOUNT: $ CARD NOT PRESENT 100% CARD PRESENT % ♦NUMBER OF HIGH SALES TRANSACTIONS ANNUALLY: INTERNET 100% CARD NOT PRESENT* % ♦TOTAL MONTHLY VISA/MC/AMEX/DISC/UNIONPAY SALES: $ OMNI COMMERCE INTERNET * % ♦ANNUAL TOTAL REVENUE: (CASH, CHECK, CARD) $ INTERNET : PRODUCT WEBSITE: ♦INDUSTRY TYPE: ♦DESCRIPTION OF PRODUCT/SERVICES OFFERED: INTERNET: “CONTACT US” EMAIL: PECIAL ROGRAM NLY S P MCC O : *CUSTOMER SERVICE PHONE # AND PREVIOUS PROCESSOR REQUIRED BELOW WHEN DOES THE CUSTOMER RECEIVE THE PRODUCT OR SERVICE? CUSTOMER SERVICE PHONE #: IF NOT SAME DAY, # OF DAYS (INCLUDE SHIPPING TIME FRAME) PREVIOUS PROCESSOR: IF SEASONAL, PLEASE CHECK MONTHS CLOSED BELOW. -

Instructions: Using the Bank of America Prepaid Card General

Instructions: Using The Bank of America Prepaid Card How to Make a Purchase at a VISA® Debit Merchant or Maestro® Merchant: Present the Card to the cashier. Swipe the Card through the terminal reader. Push either debit or credit. When selecting credit, no PIN(personal identification number) is necessary. Just sign the receipt when the cashier hands it to you and take a copy of the receipt for your records. If you select debit, you will be asked to enter your PIN. The terminal will then ask you if you want cash back. If you do, enter the amount and the cashier will dispense the cash to you. You will only be able to receive cash back if your sponsor selected this option and you have the available funds on the Card. Always check your balance prior to this type of transaction. How to Get Cash at any ATM Displaying the Cirrus® or VISA® Logos: (ATM functionality varies among financial institutions and countries. To get cash at an ATM, you should first follow any on-screen directions.) Insert the Card into the ATM. Enter your PIN. If asked which account to access, try selecting “Checking” and if that does not work select “Credit.” Press Cash Advance or Withdrawal. Each system is slightly different, but this will make sense once you are at the ATM. Remove and count your money. Remove the Card and receipt. Keep your receipt for your records. Note: For ATM transactions performed at a non Bank of America ATM, the owner or operator of the ATM may charge an additional fee.