Preserving Minority Depository Institutions, May 2019

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

DBE Program 11.07.19

City of Springfield, Ohio Disadvantaged Business Enterprise Program for FTA-assisted Projects MEMORANDUM TO : BRYAN L. HECK, CITY MANAGER FROM: SHANNON L. MEADOWS, COMMUNITY DEVELOPMENT DIRECTOR DATE: NOVEMBER 6, 2019 RE: DISTRIBUTION OF DBE PROGRAM FOR FTA-ASSISTED PROJECTS The City of Springfield, through its Department of Community Development and in partnership with the Department of Finance, has drafted and submitted to the Federal Transit Administration a new Disadvantaged Business Enterprise Program FTA-assisted Projects document. This plan document is to be distributed, along with the City of Springfield’s Policy Statement, to the Springfield City Commission; Senior Staff of each department within the City organization; as well as DBE and non-DBE business communities that perform work for the City of FTA-assisted contracts. Additionally, the City’s Program and it’s associated DBE Policy shall be placed on the city’s website at www.springfieldohio.gov/SCAT . Within the Program and Policy document, you will find the stated objectives for the City’s DBE Program for FTA-assisted Projects: 1. To ensure nondiscrimination in the award and administration of FTA-assisted contracts; 2. To create a level playing field on which DBEs can compete fairly for FTA-assisted contracts; 3. To ensure that the DBE Program is narrowly tailored in accordance with applicable law; 4. To ensure that only firms that fully meet 49 CFR Part 26 eligibility standards are permitted to participate as DBEs; 5. To help remove barriers to the participation of DBEs in FTA-assisted contracts; 6. To assist the development of firms that can compete successfully in the market place outside the DBE Program; 7. -

The Chinese in Hawaii: an Annotated Bibliography

The Chinese in Hawaii AN ANNOTATED BIBLIOGRAPHY by NANCY FOON YOUNG Social Science Research Institute University of Hawaii Hawaii Series No. 4 THE CHINESE IN HAWAII HAWAII SERIES No. 4 Other publications in the HAWAII SERIES No. 1 The Japanese in Hawaii: 1868-1967 A Bibliography of the First Hundred Years by Mitsugu Matsuda [out of print] No. 2 The Koreans in Hawaii An Annotated Bibliography by Arthur L. Gardner No. 3 Culture and Behavior in Hawaii An Annotated Bibliography by Judith Rubano No. 5 The Japanese in Hawaii by Mitsugu Matsuda A Bibliography of Japanese Americans, revised by Dennis M. O g a w a with Jerry Y. Fujioka [forthcoming] T H E CHINESE IN HAWAII An Annotated Bibliography by N A N C Y F O O N Y O U N G supported by the HAWAII CHINESE HISTORY CENTER Social Science Research Institute • University of Hawaii • Honolulu • Hawaii Cover design by Bruce T. Erickson Kuan Yin Temple, 170 N. Vineyard Boulevard, Honolulu Distributed by: The University Press of Hawaii 535 Ward Avenue Honolulu, Hawaii 96814 International Standard Book Number: 0-8248-0265-9 Library of Congress Catalog Card Number: 73-620231 Social Science Research Institute University of Hawaii, Honolulu, Hawaii 96822 Copyright 1973 by the Social Science Research Institute All rights reserved. Published 1973 Printed in the United States of America TABLE OF CONTENTS FOREWORD vii PREFACE ix ACKNOWLEDGMENTS xi ABBREVIATIONS xii ANNOTATED BIBLIOGRAPHY 1 GLOSSARY 135 INDEX 139 v FOREWORD Hawaiians of Chinese ancestry have made and are continuing to make a rich contribution to every aspect of life in the islands. -

Live Oak Banking Company 2605 Iron Gate Dr, Ste 100 2013 7(A) Jpmorgan Chase Bank, National 1111 Polaris Pkwy 2013 7(A) U.S

APPVFY MAJPGM L2Name L2Street 2013 7(A) Wells Fargo Bank, National Ass 101 N Philips Ave 2013 7(A) Live Oak Banking Company 2605 Iron Gate Dr, Ste 100 2013 7(A) JPMorgan Chase Bank, National 1111 Polaris Pkwy 2013 7(A) U.S. Bank National Association 425 Walnut St 2013 7(A) The Huntington National Bank 17 S High St 2013 7(A) Ridgestone Bank 13925 W North Ave 2013 7(A) Seacoast Commerce Bank 11939 Ranho Bernardo Rd 2013 7(A) Wilshire State Bank 3200 Wilshire Blvd, Ste 1400 2013 7(A) Compass Bank 15 S 20th St 2013 7(A) Hanmi Bank 3660 Wilshire Blvd PH-A 2013 7(A) Celtic Bank Corporation 268 S State St, Ste 300 2013 7(A) KeyBank National Association 127 Public Sq 2013 7(A) Noah Bank 7301 Old York Rd 2013 7(A) BBCN Bank 3731 Wilshire Blvd, Ste 1000 2013 7(A) TD Bank, National Association 2035 Limestone Rd 2013 7(A) Manufacturers and Traders Trus One M & T Plaza, 15th Fl 2013 7(A) Newtek Small Business Finance, 212 W. 35th Street 2013 7(A) SunTrust Bank 25 Park Place NE 2013 7(A) Hana Small Business Lending, I 1000 Wilshire Blvd 2013 7(A) First Bank Financial Centre 155 W Wisconsin Ave 2013 7(A) NewBank 146-01 Northern Blvd 2013 7(A) Open Bank 1000 Wilshire Blvd, Ste 100 2013 7(A) Bank of the West 180 Montgomery St 2013 7(A) CornerstoneBank 2060 Mt Paran Rd NW, Ste 100 2013 7(A) Synovus Bank 1148 Broadway 2013 7(A) Comerica Bank 1717 Main St 2013 7(A) Borrego Springs Bank, N.A. -

Annual Report for the As a Result of the National Financial Environment, Throughout 2009, US Congress Calendar Year 2009, Pursuant to Section 43 of the Banking Law

O R K Y S T W A E T E N 2009 B T A ANNUAL N N E K M REPORT I N T G R D E P A WWW.BANKING.STATE.NY.US 1-877-BANK NYS One State Street Plaza New York, NY 10004 (212) 709-3500 80 South Swan Street Albany, NY 12210 (518) 473-6160 333 East Washington Street Syracuse, NY 13202 (315) 428-4049 September 15, 2010 To the Honorable David A. Paterson and Members of the Legislature: I hereby submit the New York State Banking Department Annual Report for the As a result of the national financial environment, throughout 2009, US Congress calendar year 2009, pursuant to Section 43 of the Banking Law. debated financial regulatory reform legislation. While the regulatory debate developed on the national stage, the Banking Department forged ahead with In 2009, the New York State Banking Department regulated more than 2,700 developing and implementing new state legislation and regulations to address financial entities providing services in New York State, including both depository the immediate crisis and avoid a similar crisis in the future. and non-depository institutions. The total assets of the depository institutions supervised exceeded $2.2 trillion. State Regulation: During 2009, what began as a subprime mortgage crisis led to a global downturn As one of the first states to identify the mortgage crisis, New York was fast in economic activity, leading to decreased employment, decreased borrowing to act on developing solutions. Building on efforts from 2008, in December and spending, and a general contraction in the financial industry as a whole. -

2015-2016 Annual Report

Chinese American Service League 2015 - 2016 Annual Report A Message From CASL CASL has always been a fiscally conservative organization, ensuring the best use of the money you entrust to us by making a tremendous impact on our community. However, 2016 was a year of great adversity for Illinois’ not- for-profit community and for CASL. The lack of state budget for much of our fiscal year had a significant impact on our operations. CASL merged our Family and Community Services Department with our Elderly Services Department to create an Elderly and Family Services Department. This move allowed us to further reduce costs while also reevaluating program outcomes and impact. We feel that the services and outcomes will be even stronger under the leadership of our senior program’s evidence-based, data-informed practices. We also moved our Middle School Program under the leadership of our very successful High School Program. This move has provided a greater level of continuity and seamless transition of students from middle to high school. In addition, we reevaluated and shifted our focus of the Middle School Program to a social-emotional model that will better assist our new immigrant teenagers in navigating the stresses and anxieties of a new school, new culture, and new way of life coupled with the already turbulent teenage years. Finally, with the reorganization and strengthening of our Development Program, we were better prepared to adapt to these changes. The sizable increase in revenue from our events, and refocus on individual and major donors and planned gifts, allowed us to better weather the storm. -

Banking Corporation Tax Allocation Percentage Report the NEW YORK CITY DEPARMENT of FINANCE PAGE: 1 2010 BANKING CORPORATION TAX ALLOCATION PERCENTAGE REPORT

2010 Banking Corporation Tax Allocation Percentage Report THE NEW YORK CITY DEPARMENT OF FINANCE PAGE: 1 2010 BANKING CORPORATION TAX ALLOCATION PERCENTAGE REPORT NAME PERCENT AAREAL CAPITAL CORPORATION 100.00 ABACUS FEDERAL SAVINGS BANK & SUBS 88.56 ABN AMRO CLEARING BANK NV 4.64 ABN AMRO HOLDINGS USA LLC 100.00 AGRICULTURAL BANK OF CHINA 100.00 AIG FEDERAL SAVINGS BANK 100.00 ALLIED IRISH BANKS PLC 100.00 ALMA BANK 100.00 ALPINE CAPITAL BANK 100.00 AMALGAMATED BANK 93.82 AMERASIA BANK 100.00 AMERICAN EXPRESS BANK FSB 1.67 AMERICAN EXPRESS BANKING CORPORATION 100.00 AMERIPRISE BANK FSB .21 ANGLO IRISH NEW YORK CORPORATION 100.00 ANTWERPSE DIAMANTBANK NV 100.00 AOZORA BANK LTD 100.00 APPLE FINANCIAL HOLDINGS INC 53.45 ARAB BANK P L C_NEW YORK AGENCY .28 ARAB BANKING CORPORATION 100.00 ARMOR HOLDCO INC 88.51 ASIA BANCSHARES INC & SUBSIDIARIES 100.00 ASTORIA FINANCIAL CORPORATION 18.55 ATLAS SAVINGS & LOAN ASSOCIATION 100.00 AURORA BANK FSB FKA LEHMAN BROTHERS BANK FSB 3.03 AUSTRALIA & NEW ZEALAND BANKING GROUP LTD 1.01 BANCA MONTE DEI PASCHI DI SIENA SPA .11 BANCO BILBAO VIZCAYA ARGENTARIA 1.68 BANCO BRADESCO SA .09 BANCO DE BOGOTA 9.75 BANCO DE LA NACION ARGENTINA .21 BANCO DE LA REPUBLICA ORIENTAL DEL URUGUAY 100.00 BANCO DE SABADELL SA 100.00 BANCO DEL ESTADO DE CHILE 100.00 BANCO DO BRASIL SA 100.00 BANCO DO ESTADO DO RIO GRANDE DO SUL SA ("BANRISUL") 100.00 BANCO ESPIRITO SANTO S.A._AND SUBSIDIARY 1.12 BANCO INDUSTRIAL DE VENEZUELA 66.39 BANCO ITAU SA 100.00 BANCO LATINOAMERICANO DE COMERCIO EXTERIOR EXTERIOR SA .52 BANCO POPULAR -

Community Development Bank City State ABC Bank CHICAGO IL Albina Community Bank PORTLAND OR American Metro Bank CHICAGO IL Aztec

Community Development Bank City State ABC Bank CHICAGO IL Albina Community Bank PORTLAND OR American Metro Bank CHICAGO IL AztecAmerica Bank BERWYN IL Bank 2 OKLAHOMA CITY OK Bank of Cherokee County, Inc. TAHLEQUAH OK Bank of Kilmichael KILMICHAEL MS Bank of Okolona OKOLONA MS BankFirst Financial Services MACON MS BankPlus RIDGELAND MS Broadway Federal Bank LOS ANGELES CA Capitol City Bank & Trust Company ATLANTA GA Carver Federal Savings Bank NEW YORK NY Carver State Bank SAVANNAH GA Central Bank of Kansas City KANSAS CITY MO Citizens Bank of Weir WEIR KS Citizens Savings Bank and Trust Company NASHVILLE TN Citizens Trust Bank ATLANTA GA City First Bank of D.C., N.A. WASHINGTON DC City National Bank of New Jersey NEWARK NJ Commercial Capital Bank DEHLI LA Commonwealth National Bank MOBILE AL Community Bank of the Bay OAKLAND CA Community Capital Bank of Virginia CHRISTIANSBURG VA Community Commerce Bank CLAREMONT CA Edgebrook Bank CHICAGO IL First American International Bank BROOKLYN NY First Choice Bank CERRITOS CA First Eagle Bank CHICAGO IL First Independence Bank DETROIT MI First National Bank of Decatur County BAINBRIDGE GA First Security Bank BATESVILLE MS First Tuskegee Bank MONTGOMERY AL Fort Gibson State Bank FORT GIBSON OK Gateway Bank Federal Savings Bank OAKLAND CA Guaranty Bank & Trust BELZONI MS Harbor Bank of Maryland BALTIMORE MD Illinois Service Federal Savings and Loan Association CHICAGO IL Industrial Bank WASHINGTON DC International Bank of Chicago STONE PARK IL Liberty Bank and Trust Company NEW ORLEANS LA Magnolia State Bank BAY SPRINGS MS Mechanics and Farmers Bank DURHAM NC Merchants & Planters Bank RAYMOND MS Metro Bank LOUISVILLE KY Current as of 12-15-2013 Source: CDFI Fund Community Development Bank City State Mission Valley Bank SUN VALLEY CA Mitchell Bank MILWAUKEE WI Native American Bank, N.A. -

480357300.00

LOS ANGELES DISTRICT OFFICE Lender Ranking Report 7(a) and 504 Loan Programs Fiscal Year 2018 - 1st Quarter (YTD) (10/01/2017 - 12/31/2017) 7(a) Loan Program 1 WELLS FARGO BANK, N.A. 75 $46,434,400 60 Byline Bank 1 $3,400,000 2 JPMORGAN CHASE BANK, N.A. 65 $17,434,700 61 MidFirst Bank 1 $2,596,000 3 BANK OF HOPE 40 $25,544,400 62 Pacific Western Bank 1 $2,421,000 4 East West Bank 29 $9,327,000 63 Cathay Bank 1 $2,210,000 7(a) LOAN TOTALS 5 U.S. Bank, N.A. 28 $5,779,200 64 First-Citizens Bank & Trust Company 1 $1,980,000 591 Loans 6 First Home Bank 18 $3,998,000 65 Community Bank of the Bay 1 $1,866,000 7 Celtic Bank Corporation 18 $3,466,600 66 Partners Bank of California 1 $1,750,000 Valued at: $375,199,300 8 Live Oak Banking Company 14 $22,946,000 67 United Pacific Bank 1 $1,650,000 9 Uniti Bank 14 $15,405,000 68 Meadows Bank 1 $1,601,500 10 Seacoast Commerce Bank 13 $14,323,300 69 Citizens Business Bank 1 $1,600,000 11 Pacific City Bank 13 $13,189,000 70 T Bank, N.A. 1 $1,452,000 504 LOAN TOTALS 12 Bank of the West 13 $13,023,800 71 Community Valley Bank 1 $954,400 81 Loans 13 Commonwealth Business Bank 11 $14,453,000 72 Umpqua Bank 1 $823,000 14 Open Bank 10 $4,784,500 73 Commerce Bank of Temecula Valley 1 $655,000 Valued at: $105,158,000 15 Citibank, N.A. -

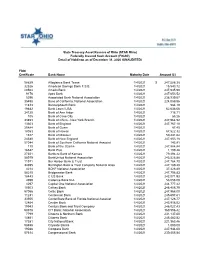

FDIC Certificate Bank Name Maturity Date Amount ($)

State Treasury Asset Reserve of Ohio (STAR Ohio) Federally Insured Cash Account (FICA®) Detail of Holdings as of December 31, 2020 (UNAUDITED) FDIC Certificate Bank Name Maturity Date Amount ($) 58629 Allegiance Bank Texas 1/4/2021 $ 247,586.38 32526 American Savings Bank F.S.B. 1/4/2021 15,543.72 20504 Ameris Bank 1/4/2021 247,935.99 9176 Apex Bank 1/4/2021 247,653.52 5296 Associated Bank National Association 1/4/2021 238,939.67 35498 Banc of California; National Association 1/4/2021 224,059.96 11813 BancorpSouth Bank 1/4/2021 584.19 19842 Bank Leumi USA 1/4/2021 62,638.66 34120 Bank of Ann Arbor 1/4/2021 718.71 105 Bank of Cave City 1/4/2021 55.26 33653 Bank of China - New York Branch 1/4/2021 247,964.52 13303 Bank of England 1/4/2021 247,767.10 20884 Bank of Guam 1/4/2021 87.45 18053 Bank of Hawaii 1/4/2021 67,522.32 1617 Bank of Missouri 1/4/2021 59,441.62 24540 Bank of New England 1/4/2021 247,853.18 57044 Bank of Southern California National Associat 1/4/2021 145.91 110 Bank of the Ozarks 1/4/2021 247,884.84 16547 Bank Plus 1/4/2021 1,199.46 27351 Bankers Bank of Kansas 1/4/2021 79,494.22 58979 BankUnited National Association 1/4/2021 243,528.88 11971 Bar Harbor Bank & Trust 1/4/2021 247,764.70 34395 Barrington Bank & Trust Company National Asso 1/4/2021 247,189.20 4214 BOKF National Association 1/4/2021 37,428.89 58210 Bridgewater Bank 1/4/2021 247,798.83 18443 C US Bank 1/4/2021 242,071.93 4999 Cadence Bank N.A. -

CHINESE AMERICAN MUSEUM CAM Honors History-Making Innovators

CHINESE AMERICAN MUSEUM 425 North Los Angeles Street Los Angeles, CA 90012 Tel 213 485-8484 Fax 213 485-0428 www.camla.org FOR IMMEDIATE RELEASE September 25, 2014 CAM Honors History-making Innovators, Pioneers, Leaders LOS ANGELES.—Innovators, pioneers, corporate and community leaders were recognized Thursday, Sept. 25 as the Chinese American Museum (CAM) raised the curtain on the 18th annual Historymakers Awards Gala and commemorated its 10th anniversary. In line with the gala’s theme, “CAM at 10: New Directions for the Next Decade,” Nissan North America served as title sponsor for the event and announced the launch of Project Future Star, a contest designed to celebrate visionaries and innovators. "We thank Nissan for joining with us as we expand our mission into the next decade," stated Dr. Gay Yuen, Friends of the Chinese American Museum (FCAM) president. Kin Hui, Chairman and CEO of the Singpoli Group, served as honorary dinner chair. The event took place at the Bonaventure Hotel in downtown Los Angeles. Awards were presented to the following individuals and organizations: Ming Hsieh (Judge Ronald S. W. Lew Visionary Award) is at the forefront of engineering medicine for cancer research and biometric identification. As the founder, Chairman, and Chief Executive Officer of 3M Cogent Inc., he has led the development of global identification systems. He has also served as the Chairman and CEO of Fulgent Therapeutics Inc., a cancer drug research and development company. Raised in Shenyang, northern China, he currently a trustee of the University of Southern California. David Fon Lee (Dr. Dan S. Louie, Jr., Lifetime Achievement Award), best known as proprietor of the iconic General Lee’s Man Jen Low Restaurant, led advocacy on behalf of Chinatown and U.S.-China relations as early as the 1970s. -

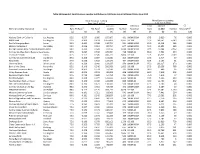

3A Expanded Small Business Lending

Table 3A Expanded. Small Business Lending Institutions in California Using Call Report Data, June 2012 Small Business Lending Micro Business Lending (less than $ million) (less than $ 100k) Total Amount Institution Total Amount CC Name of Lending Institution City Rank TA Ratio1 TBL Ratio1 (1,000) Number Asset Size Rank (1,000) Number Amount/TA1 (1) (2) (3) (4) (5) (6) (7) (8) (9) (10) National Bank of California Los Angeles 95.0 0.537 1.000 187,467 431 100M-500M 67.5 3,020 76 0.000 BBCN Bank Los Angeles 92.5 0.309 0.424 1,557,424 9,537 1B-10B 97.5 168,741 6,149 0.000 Pacific Enterprise Bank Irvine 92.5 0.405 0.549 110,755 591 100M-500M 95.0 11,314 249 0.000 Mission Valley Bank Sun Valley 90.0 0.356 0.564 87,754 647 100M-500M 95.0 12,892 365 0.000 Borrego Springs Bank, National AssociLa Mesa 90.0 0.435 0.628 65,123 3,020 100M-500M 97.5 10,544 2,562 0.000 Community West Bank, National Asso Goleta 87.5 0.227 0.542 129,084 718 500M-1B 85.0 7,591 234 0.000 Tri Counties Bank Chico 87.5 0.173 0.545 436,723 3,804 1B-10B 97.5 43,955 2,289 0.000 Community Commerce Bank Claremont 87.5 0.358 0.687 103,416 365 100M-500M 67.5 2,717 57 0.000 Plaza Bank Irvine 87.5 0.328 0.502 127,075 484 100M-500M 52.5 2,193 61 0.000 Universal Bank West Covina 85.0 0.329 1.000 133,617 170 100M-500M 95.0 133,617 170 0.000 Bank of the Sierra Porterville 85.0 0.148 0.546 206,583 1,602 1B-10B 97.5 20,356 768 0.000 Seacoast Commerce Bank San Diego 82.5 0.363 0.574 57,144 315 100M-500M 30.0 409 16 0.000 Valley Business Bank Visalia 82.5 0.259 0.531 89,428 408 100M-500M 90.0 -

Continental National Bank Charter Number 16325

PUBLIC DISCLOSURE May 20, 2019 COMMUNITY REINVESTMENT ACT PERFORMANCE EVALUATION Continental National Bank Charter Number 16325 1801 SW First Street Miami, FL 33135 Office of the Comptroller of the Currency Miami Field Office 9850 NW 41st Street, Suite 260 Miami, FL 33178 NOTE: This document is an evaluation of this institution's record of meeting the credit needs of its entire community, including low- and moderate-income neighborhoods, consistent with safe and sound operation of the institution. This evaluation is not, and should not be construed as, an assessment of the financial condition of this institution. The rating assigned to this institution does not represent an analysis, conclusion, or opinion of the federal financial supervisory agency concerning the safety and soundness of this financial institution. Charter Number: 16325 Table of Contents Overall CRA Rating……...……………………………………………………………….. 1 Description of Institution………….……………………………………………………… 2 Scope of the Evaluation……………………………………………………………………2 Discriminatory or Other Illegal Credit Practices Review………………………..……….. 3 State Rating…….………………………………………………………………………... 4 State of Florida………………..………………………………………………. 4 Appendix A: Scope of Examination………….…………………………………………A-1 Appendix B: Summary of MMSA and State Ratings…………………………………...B-1 Appendix C: Definitions and Common Abbreviations………………………………….C-1 Appendix D: Tables of Performance Data………………………………………………D-1 i Charter Number: 16325 Overall CRA Rating Institution’s CRA Rating: This institution is rated Outstanding The lending test is rated: Outstanding The community development test is rated: Outstanding The major factors that support this rating include: The Lending Test rating is based on the excellent distribution of loans in low- and moderate-income (LMI) geographies, a reasonable distribution of lending among businesses of different sizes, a substantial majority of loans purchased or originated are in the assessment area (AA), and a reasonable loan-to-deposit (LTD) ratio.