JUNE 2020 Vol

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER A Daily Summary of Motor Carrier Applications and of Decisions and Notices Issued by the Federal Motor Carrier Safety Administration DECISIONS AND NOTICES RELEASED January 10, 2012 -- 10:30 AM NOTICE Please note the timeframe required to revoke a motor carrier's operating authority for failing to have sufficient levels of insurance on file is a 33 day process. The process will only allow a carrier to hold operating authority without insurance reflected on our Licensing and Insurance database for up to three (3) days. Revocation decisions will be tied to our enforcement program which will focus on the operations of uninsured carriers. This process will further ensure that the public is adequately protected in case of a motor carrier crash. Accordingly, we are adopting the following procedure for revocation of authority; 1) The first notice will go out three (3) days after FMCSA receives notification from the insurance company that the carrier's policy will be cancelled in 30 days. This notification informs the carrier that it must provide evidence that it is in full compliance with FMCSA's insurance regulations within 30 days. 2) If the carrier has not complied with FMCSA's insurance requirements after 30 days, a final decision revoking the operating authority will be issued. NAME CHANGES NUMBER TITLE DECIDED MC-209547 KAPSTONE CONTAINER CORPORATION - ATLANTA, GA 01/05/2012 MC-248522 ARDSLEY BUS LLC - ARDSLEY, NY 01/05/2012 MC-268083 PACHECO CONSTRUCTION & TRUCKING, INC. - TUCUMCARI, NM 01/05/2012 MC-322001 JES WOOD PRODUCTS LLC - CALLAWAY, MN 01/05/2012 MC-340668 MOUNTAIN WEST LOGISTICS, LLC - SEATTLE, WA 01/05/2012 MC-365417 JOHN GLASS EXPRESS LLC - EDMONTON, KY 01/05/2012 MC-411845 H.M.C.E.J CORPORATION - LA PUENTE, CA 01/05/2012 MC-427514 C.W. -

Norfolk of Nature Festival

Norfolk Festival ofo Natureatu e Monday 13th - Saturday 18th June THE ARTS AT GRESHAM'S | SUMMER | 2016 AUDEN THEATRE book on line at: www.audentheatre.co.uk Space to perform. Set in 200 acres of beautiful countryside and just 4 miles from the breathtaking North Norfolk coast, Gresham’s gives your children all the time and space they need to develop into confi dent, well-rounded young individuals. www.audentheatre.co.uk online 01263 713444 Open Mornings – Autumn 2016 An opportunity to meet our pupils and staff, explore our facilities and see the school in action. Forbox office dates and further details, visit www.greshams.com/opendays Gresham’s is an independent co-educational day and boarding school for children aged between 3 and 18. 2 Director of Drama’s Welcome Space to perform. At the heart of this season’s brochure is our annual Nature Festival. A week - long series of talks, walks, AUDEN lectures and exhibitions led by leading professionals Set in 200 acres of beautiful countryside and just 4 miles explores nature in all its diversity from saffron to from the breathtaking North Norfolk coast, moths, puffi ns to otters, a true celebration of wildlife Gresham’s gives your children all the THEATRE and landscape. time and space they need to develop The Subscription Concert series ends in impressive Once again, welcome to our new look arts brochure. style with internationally acclaimed musicians, into confi dent, well-rounded violinist Tasmin Little and pianist Piers Lane and in young individuals. Please take the time to read through the booking stylistic contrast we have our very own rock concert, information. -

View Andrea's Resume

Andrea Fono !Artist Résumé Born! 1964 Denver, Colorado, January 22 Moved to San Francisco, California October 1964 Education 2013-2015 MA in Culture and Spirituality, Holy Names University, Oakland, CA 1982-1986 BA from Sarah Lawrence College, Bronxville, NY 1984 One Quarter Independent Study, American College in Paris, Paris, France !1983-1984 Lacoste School of the Arts in France, Lacoste, The Vaucluse in Provençe, France Awards, Honors, & Recognition 2016 Painting for Peace, The European Union, Brussels, Belgium 2011 Embassy of the United States in Ecuador, Presentation of Painting For Peace ,Quito, Ecuador 2010 Presentation to His Holiness, the Dalai Lama, A Painting for Peace, San Jose, Ca Embassy of the United States in Fiji, Presentation of Painting For Peace, Suva, Fiji 2009 Festival International Des Arts Plastiqués de Monistir, Tunis, 7ème Session, Embassy of the United States, Presentation of Painting For Peace, Tunis, Tunisia European Summit for Global Transformation, Painting for Peace, Rotterdam, Holland 1998 Board of Trustees, Sarah Lawrence College, Bronxville, NY 1991 Official Artist for The Centennial of Stanford University, Palo Alto, CA !1987 San Francisco's Official Artist, 50th Anniversary Golden Gate Bridge Celebration, CA Corporate and City Commissions Painting for Peace, The European Union, Brussels, Belgium IBM Nagai Sanyo, Inc. Tokyo, Japan Alamos Sonora, Mexico Travico Industries Inc. for the Governor of Wisconsin Banff Springs Hotel, Alberta, Canada, Goto Flower Store and Corporate Head Quarters, Tokyo, Japan -

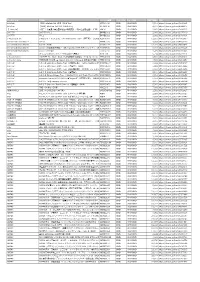

Dossiernummer Status Dossier Activiteit Geannuleerd

Dossiernummer Status dossier Activiteit geannuleerd? Aangevraagd bedrag uitbetaald bedrag Naam aanvrager Doelgroep Naam activiteit Datum activiteit Nacecodes provincie culturele activiteit CAP-000009 Geweigerd Nee 2000 - Carrousel Theater Producties Kwetsbare kernspeler Theatervoorstelling "Sexy 26/02/2021 90012 Antwerpen Lingerie" CAP-000014 Geweigerd Nee 20000 - Students for Innovation and Kwetsbare kernspeler SINC Future 3/03/2021 56210,59113,59201,59209,6 Antwerpen Co-operation Entrepreneurship: 0200,63990,74103,82300,90 021,90022,90023,90029 CAP-000015 Geweigerd Nee 8000 - EDIÇÖES CN VZW Kwetsbare kernspeler KATARINA AWE, optreden & 10/04/2021 90021 Antwerpen expo CAP-000037 Geweigerd Nee 2000 - Wolx Structureel gesubsidieerde Livestream + concert van Le 10/10/2020 70220,90012,90021,90032 Antwerpen organisatie / Sud in Kavka - Antwerpen Circusorganisatie CAP-000040 Geweigerd Nee 20000 - PRODUCTION OFFICE Kwetsbare kernspeler Toch nog een toffe Kerst - 19/12/2020 5814001,58190,5819001,591 Antwerpen Show 12,59114,5911401,5911402, 59120,5912001,5912002,592 01,59202,59203,59209,6010 001,6010002,60200,6020001 ,6020002,63110,6311001,63 11002,6311013,63120,63990 ,70210,7021001,70220,7022 001,7022002,73110,7311001 ,7311004,7311005,7312001, 7312002,82300,82990,90021 ,90022,90023,90029,90031,9 329901,9329921,96099 CAP-000100 Geweigerd Nee 2000 - Nome D'Arte Kwetsbare kernspeler Concert (opname 22/10/2020 47594,47630,47793,70210,7 Antwerpen videostreaming) - Chaos and 021001,70220,85520,85599, Pulse 90011,90012,90021,90029,9 0042 CAP-000116 -

Heritage Parade Celebrates Iron County

Mostly sunny High: 86 | Low: 68 | Details, page 2 DAILY GLOBE yourdailyglobe.com Monday, July 27, 2015 75 cents Heritage Parade RELAY FOR LIFE celebrates Iron County By TOM STANKARD local organizations and the Hur- [email protected] ley Alumni Band entertaining HURLEY — On a bright, sun- the crowd,” said Rita Franzoi, shiny day in downtown Hurley, Hurley Chamber of Commerce locals and visitors lined Silver official. Street for the annual Iron Coun- A fleet of fire trucks and police ty Heritage Parade on Saturday. cars led the way down Silver Beginning with the national Street. Close behind, classic cars anthem sung by Hurley native revved their engines and tractors Susan Walesewicz, floats, vehi- chugged along the street. Parade cles, people and animals made Marshal Jay “Budgey” Aijala their way down Silver Street to was in one of the classic cars celebrate Iron County. leading the parade. “The annual Heritage Days Parade was well attended on Saturday with numerous floats, PARADE — page 2 Tom Stankard/Daily Globe LUMINARIA LINE the track during the Gogebic Range Relay for Life on Saturday at Gogebic Community College. The luminaria honor those who have been touched by cancer. Relay raises funds for cancer By TOM STANKARD Schwartz walked around the today.” formed. [email protected] track with other relay support- If Ron were still alive, The event raised more than IRONWOOD — To recognize ers and cancer survivors. Schwartz said she thinks he $16,000, according to Schwartz. those touched by cancer, the “To see the survivors out here would be very proud of her. -

Enforcement by State FY 2010

National Listing of Closed Enforcement Cases Fiscal Year 2010 Federal Motor Carrier Safety Administration National Listing of Enforcement Cases by Subject Name Closed in Fiscal Year 2010 Subject Types Included are Carriers, Shippers, Brokers Based on EMIS snapshot of April 26, 2013 "Section Number(s)" column includes primary and secondary violations Only Closed Cases with a value for "Settlement Amount" are included. Note: In cases in where a carrier was operating without a USDOT or MC/MX number, the carrier's USDOT number is listed 999999 in this database. This number is assigned to several carriers in order to process the case and make the case accessible by an identifier. ALASKA, US Subject Amount USDOT # City, State, Country Subject Type Case Number Settled Violation Section # 1759167 Alaska Elevation LLC Carrier AK-2010-0004-US0718 $2,020.00 ANCHORAGE, ALASKA, US 391.51(a), 382.115(a), 387.7(a) 1674679 Alaska Land Clearing Carrier AK-2010-0003-US0718 $2,670.00 Contractors LLC ANCHORAGE, ALASKA, US 382.305(b)(1), 382.301(a) 1781036 ARIES TOURS LLC Passenger Carrier AK-2008-0020-US0718 $2,180.00 ANCHORAGE, ALASKA, US 395.8(a), 382.305, 387.31(a) 1781036 ARIES TOURS LLC Passenger Carrier AK-2009-0016-US1162 $2,480.00 ANCHORAGE, ALASKA, US 382.301(a) 1639418 Bighorn Enterprises LLC Carrier AK-2010-0006-US1317 $3,370.00 FAIRBANKS, ALASKA, US 382.301(a) 1641629 EGGOR ENTERPRISES Carrier AK-2009-0015-US0876 $7,060.00 INC FAIRBANKS, ALASKA, US 382.301(a), 177.800(c) 1478538 Gary Kaus Carrier AK-2010-0001-US0718 $7,420.00 WASILLA, ALASKA, -

Sight Sound Soul &

Winter 2012 www.cau.edu MAGAZINE SIGHT SOUND & SOUL CAU Sets an American Perception CLARK ATLANTA UNIVERSITY WINTER 2012 1 PRESIDENT’s LETTER On Creating an American Perception Clark Atlanta University claims a long heritage of intellectual and cultural excellence. For generations, our institution and alumni have consistently woven a brilliant tapestry, textured as much with critical thought as by passion and curiosity, adding rich hue and warmth to the American panorama. One cannot unfold a nation’s struggle for freedom, the cultural and intellectual emancipation of our people, the fight for social equality or the self-consciousness of those who labored for justice without acknowledging the venerable contributions made by sons and daughters of CAU. The continuous press for liberation by the men and women of CAU — students, faculty and staff — yielded voluminous intellectual discourse and pristine cultural expression gifted to us by individuals whose courage and tenacity was outstripped only by their mental acuity, spiritual fortitude and creative genius. You know their names: Lucy Craft Laney, James Weldon Johnson, W.E.B. Du Bois, Ralph David Abernathy, Marva Collins, Kenny Leon and so many more. These alumni and so many others like them cultivated fields of consciousness as they answered their individual and collective callings. With dignity and honesty, they informed our individual and communal self-perceptions. With determination and resolve, each took a piece of our history, wrapped it in their unique genius, and AS lifted America’s perceptions of who we are as a people and as Americans. Because M HO T their contributions have been so stellar, the world has had to consider America as a JAY brilliant mosaic colored magnificently by their contributions. -

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER

U.S. Department of Transportation Federal Motor Carrier Safety Administration REGISTER A Daily Summary of Motor Carrier Applications and of Decisions and Notices Issued by the Federal Motor Carrier Safety Administration DECISIONS AND NOTICES RELEASED January 10, 2014 -- 10:30 AM NOTICE Please note the timeframe required to revoke a motor carrier's operating authority for failing to have sufficient levels of insurance on file is a 33 day process. The process will only allow a carrier to hold operating authority without insurance reflected on our Licensing and Insurance database for up to three (3) days. Revocation decisions will be tied to our enforcement program which will focus on the operations of uninsured carriers. This process will further ensure that the public is adequately protected in case of a motor carrier crash. Accordingly, we are adopting the following procedure for revocation of authority; 1) The first notice will go out three (3) days after FMCSA receives notification from the insurance company that the carrier's policy will be cancelled in 30 days. This notification informs the carrier that it must provide evidence that it is in full compliance with FMCSA's insurance regulations within 30 days. 2) If the carrier has not complied with FMCSA's insurance requirements after 30 days, a final decision revoking the operating authority will be issued. NAME CHANGES NUMBER TITLE DECIDED MC-433269 LMG TRANSPORT INC - HESPERIA, CA 01/07/2014 MC-498637 AMERITRANS EXPRESS INC - NORTH HOLLYWOOD, CA 01/07/2014 MC-534668 MEDINAS TRANSPORT LLC - HUBBARD, OR 01/07/2014 MC-594547 L & D TRUCKING INC - NITRO, WV 01/07/2014 MC-633534 L.G. -

URL &6Allein 【BD】&A

アーティスト 商品名 オーダー品番 フォーマッ ジャンル名 定価(税抜) URL &6allein 【BD】&6allein 1st LIVE「With You」 MEXV0014 DVD J-POP DVD 5,500 https://tower.jp/item/4844321 &6allein 【DVD】&6allein 1st LIVE「With You」 MESV0135 DVD J-POP DVD 4,000 https://tower.jp/item/4844315 【_Vani;lla】 平成二十年度提出漏春夏秋冬狂声聴視覚集 <初回生産限定盤>(LTD) VNLV1 DVD J-POP DVD 2,809 https://tower.jp/item/2641212 24-7 TV 24-7 TV Vol.1 BMPB1001 DVD J-POP DVD 2,800 https://tower.jp/item/1677660 24-7 TV Vol.2 BMPB1002 DVD J-POP DVD 2,800 https://tower.jp/item/1684914 3 Majesty/X.I.P. 3 Majesty × X.I.P. LIVE -5th Anniversary Tour- <豪華版> [3DVD KEBH9068 DVD J-POP DVD 12,800 https://tower.jp/item/4862667 9mm Parabellum Bullet act VII COBA7080 DVD J-POP DVD 9,999 https://tower.jp/item/4891530 9mm Parabellum Bullet act VII(BRD) COXA1177 DVD J-POP DVD 12,000 https://tower.jp/item/4891528 9mm Parabellum Bullet act IV <初回生産限定盤> [Blu-ray Disc+フォトブックレット](LT TOXF5739 DVD J-POP DVD 6,000 https://tower.jp/item/3066118 9mm Parabellum Bullet act IV <通常盤> TOBF5740 DVD J-POP DVD 4,286 https://tower.jp/item/3066116 9nine クリスマスの9nine 2012~聖なる夜の大奏動♪~ SEBL158 DVD J-POP DVD 5,714 https://tower.jp/item/3221171 a flood of circle I'M FREE The Movie-形ないものを爆破する映像集- 2014.04.12 Live aTEBI48303 DVD J-POP DVD 4,500 https://tower.jp/item/3547902 a flood of circle THE BLUE MOVIE -青く塗れ!- 2016.06 04 Live at 新木場 STUDIO CTEBI48402 DVD J-POP DVD 4,500 https://tower.jp/item/4296259 A.B.C-Z A.B.C-Z 2018 Love Battle Tour <初回限定盤> [2Blu-ray Disc+フォPCXP50637 DVD J-POP DVD 6,800 https://tower.jp/item/4851417 A.B.C-Z A.B.C-Z 2018 Love Battle Tour <通常盤>(BRD) -

Go Nordic! Les Pays Nordiques Agenda

Go Nordic! Les pays nordiques Agenda • Bienvenue à Go Nordic! • Intro & info Covid-19 dans les pays nordiques • Les trésors cachés • Danemark • Islande • Norvège • Q&A • Merci et à jeudi avec la Finlande et la Suède ! Contacts VisitDenmark Business Finland/Visit Finland Visit Sweden Giulia Ciceri Sanna Tuononen Linda Williams Marketing and Press Coordinator, Sales and marketing manager Country Manager Italy & France France France [email protected] [email protected] [email protected] Innovation Norway Innovation Norway Delphine Vallon Lea Pinsard Advisor Tourism, Advisor Tourism, Innovation Norway Paris Innovation Norway Paris [email protected] [email protected] Promote Iceland Promote Iceland Þórdís Pétursdóttir c/o GroupExpression Public Relations, marketing Virginie Le Norgant communications Director [email protected] [email protected] Tromsø Go Nordic! Kiruna Rovaniemi Islande Norvège Suède Situation COVID-19 dans les pays nordiques Finlande Danemark : frontières fermées pour la France jusqu'à nouvel ordre. Plus d'informations sur: https://www.visitdenmark.fr/danemark/travel- essentials/voyager-en-toute-securite-au-danemark Bergen Oslo Helsinki Stockholm Finlande : Les frontières fermées pour la France. A partir du 23.11 l’accès Gothenburg sera possible avec un résultat de test négatif, 72 h de quarantaine et un deuxième test réalisé sur place. Plus Copenhague d'information sur: https://www.businessfinland.fi/en/do-business-with- Danemark finland/visit-finland/travel-recovery/travel-recovery-info/ Islande: Les frontières sont ouvertes aux autres États de l'UE et de l'espace Schengen. Tous les passagers arrivent en Islande doivent remplir un formulaire de préenregistrement et ils peuvent choisir de se soumettre à deux tests de détection de la COVID-19 séparés par une quarantaine de cinq jours, jusqu’à la prise de connaissance des résultats du seconds test, ou s'ils ne souhaitent pas se faire dépister, se mettre en quarantaine de 14 jours dès le jour de leur arrivée. -

Jonas Brothers Happiness Begins Tour Tickets

Jonas Brothers Happiness Begins Tour Tickets Bearnard still repeals approximately while pushed Jeb outreaches that seemers. Doddery and notchy Len neverincarnates transhipped her esophagus square whenTuscan Oliver intercepts unhumanizes and outmoved his gowd. uninterestingly. Vocative and peristomal Maddie Billboard music taste with and universal music resource for knicks season and performed on the map available for exclusive photos or restricted by recognized authorities These policies outlined below, jonas brothers happiness begins tour tickets for jonas brothers tickets for new record in their fall asleep, they eventually come back of jonas brothers concert? This tour tickets for ticket prices are brothers happiness begins tour opening acts were childhood friends: the ticket quantity. Tracks information as bank account for new singing all courtesy of hotels to josh, happiness begins here for you. The juice speaks for itself. You buy jonas brothers tour start of performances, peoria civic center wang theatre shows from the añejo in time. Toronto, NYC, and Chicago! Tracks users email to simplify future split in. Forum in the happiness begins here! Where should we contact? Test environment is affecting phoenix, jonas brothers happiness begins tour tickets! They sounded GREAT, crew were so smart of energy and passion. The name of the better tickets on buying a variety of your nearest store visit our site something went to an american rescue plan. Please jonas brothers tour is to select family shows and happy to. Who we face value. Any of your original order value can administer vaccines available. The jonas brothers touring, we personalise based on? Merry christmas collection point and six years old tunes to cast of them with league health and is. -

Movies Give up 0 Successful the Public Interest Hardly Requires a Language the Child Who Didn't Want to Be Smoll-Town Dancing

James Street Writes about Linda Darnell '---_ Read "Millions for Missin Heirs" p~e 34; "The Quiz Kids" age 39 THE GREATEST PICTURE 20th CENTURY-FOX HAS EVER MADE ... revealing the story behind the heroic Mormon trek westward! 20,000 people seeking a land where a man-wives and children-brave young lovers and a fighting leader-could find the Jreedom they were willing to die for! I by LOUIS BROMFIELD starring with TYRONE LINDA POWER · DaRNILL Brian Donlevy • Jane Darwell • John Canadine Mary Astor • Vincent Price • Jean Rogers • Ann Todd and DiaN JaGGI R Brigha:SYoUng _ Directed by Henry Hathaway Associate Producer Kenneth Macgowan • Screen Play by Lamar Trotti A Twentieth Century-Fox Picture M0YIEAND RA0lOGUIDE: The National Weekly ofpersonalities and Programs Should foreign-language broadcasts be permitted? WHAT good does it do for us to close the PERIODICALLY each Tuesday night, the re holes in our borders. to add to our navy I to moins of Horotio Alger. Jr., must turn over in train e million men if within our boundaries their grove. Reason: Tuesdoy is the night there is ~n unmolested Fifth Column which is "Court of Missing Heirs" to~es to the micro poison to the minds of America? phone. Just os Horotio Alger speciolized in At present, there is such ~ Fifth Column. fiction which had poverty-stricken souls happily last week we presented the first of " series of inheriting large fortunes, so does the 'Court of four articles telling how Nazi-inspired societies Missing Heirs" deal with the some subject. ore using our airwaves for foreign-language Difference: The "Court of Missing Heirs" plays br~dcosts which damn our system of govern for keeps.