LIFE at KKR We Are Investors

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Combining Banking with Private Equity Investing*

Unstable Equity? * Combining Banking with Private Equity Investing First draft: April 14, 2010 This draft: July 30, 2010 Lily Fang INSEAD Victoria Ivashina Harvard University and NBER Josh Lerner Harvard University and NBER Theoretical work suggests that banks can be driven by market mispricing to undertake activity in a highly cyclical manner, accelerating activity during periods when securities can be readily sold to other parties. While financial economists have largely focused on bank lending, banks are active in a variety of arenas, with proprietary trading and investing being particularly controversial. We focus on the role of banks in the private equity market. We show that bank- affiliated private equity groups accounted for a significant share of the private equity activity and the bank’s own capital. We find that banks’ share of activity increases sharply during peaks of the private equity cycles. Deals done by bank-affiliated groups are financed at significantly better terms than other deals when the parent bank is part of the lending syndicate, especially during market peaks. While bank-affiliated investments generally involve targets with better ex-ante characteristics, bank-affiliated investments have slightly worse outcomes than non-affiliated investments. Also consistent with theory, the cyclicality of banks’ engagement in private equity and favorable financing terms are negatively correlated with the amount of capital that banks commit to funding of any particular transaction. * An earlier version of this manuscript was circulated under the title “An Unfair Advantage? Combining Banking with Private Equity Investing.” We thank Anna Kovner, Anthony Saunders, Antoinette Schoar, Morten Sorensen, Per Strömberg, Greg Udell and seminar audiences at Boston University, INSEAD, Maastricht University, Tilburg University, University of Mannheim and Wharton for helpful comments. -

Private Equity;

MICHAEL MORTELL Senior Managing Director Digital Media; Mergers & Acquisitions; Private Equity; Restructuring; Strategy 485 Lexington Avenue, 10th Michael Mortell is a Senior Managing Director at Ankura Capital Advisors, Floor New York, NY 10017 based in New York. Mike has extensive experience advising entrepreneurs +1.212.818.1555 Main and companies on mergers, acquisitions, strategic and business planning, +1.646.291.8597 Direct restructuring, and capital raising alternatives. Over a career in investment banking and consulting, he has cultivated expertise in the digital media and [email protected] private equity industries and developed strong relationships within them. Mike has a proven record of identifying young, high-potential companies, and providing the strategical and tactical counsel that supports growth EDUCATION objectives and positions them for future success. He also has advised MBA, University or Chicago owners/shareholders of established companies on strategic growth and Booth School of Business liquidity options. In addition to his work in digital media, he has significant BS, Finance Fairfield University experience in the e-commerce, software, retail, specialty manufacturing, and business services sectors. Prior to joining Ankura, Mike was a senior advisor at GP Bullhound, a CERTIFICATIONS boutique investment bank that acquired AdMedia Partners, the M&A FINRA Series 24, 7, 79 and 63 advisory firm where he served as a managing director. He previously ran the Private Equity Financing Group of Prudential Securities and worked for Zolfo, Cooper and Company where he was a consultant to troubled companies and their creditors. Mike also co-founded and managed Grandwood Capital LLC, an investment bank and advisory firm focused on middle-market companies. -

August Investor Presentation

APOLLO GLOBAL MANAGEMENT, LLC (NYSE: APO) Apollo Global Management Investor Presentation August 2018 Forward Looking Statements & Other Important Disclosures This presentation may contain forward-looking statements that are within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements include, but are not limited to, discussions related to Apollo Global Management, LLC’s (together with its subsidiaries, “Apollo”,”we”,”us”,”our” and the “Company”) expectations regarding the performance of its business, liquidity and capital resources and the other non-historical statements. These forward looking statements are based on management’s beliefs, as well as assumptions made by, and information currently available to, management. When used in this presentation, the words “believe,” “anticipate,” “estimate,” “expect,” “intend” or future or conditional verbs, such as “will,” “should,” “could,” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. Although management believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will prove to be correct. These statements are subject to certain risks, uncertainties and assumptions, including risks relating to our dependence on certain key personnel, our ability to raise new private equity, credit or real asset funds, market conditions generally, our ability to manage our growth, fund performance, changes in our regulatory environment and tax status, the variability of our revenues, net income and cash flow, our use of leverage to finance our businesses and investments by funds we manage (“Apollo Funds”) and litigation risks, among others. -

Preqin Special Report: Subscription Credit Facilities

PREQIN June 2019 SPECIAL REPORT: SUBSCRIPTION CREDIT FACILITIES PREQIN SPECIAL REPORT; SUBSCRIPTION CREDIT FACILITIES Contents 3 CEO’s Foreword 4 Subscription Credit Facility Usage in Private Capital 7 Subscription Lines of Credit and LP-GP Alignment: ILPA’s Recommendations - ILPA 8 Are Subscription Facilities Oversubscribed? - Fitch Ratings 10 Subscription Finance Market - McGuireWoods LLP Download the Data Pack All of the data presented in this report is available to download in Excel format: www.preqin.com/SCF19 As with all our reports, we welcome any feedback you may have. To get in touch, please email us at: [email protected] 2 CEO's Foreword Subscription credit facilities: angels or demons? A legitimate and valuable tool for managing liquidity and streamlining transactions in a competitive market, or a cynical ploy for massaging IRRs? The debate continues in private equity and wider private capital circles. As is often the case, historical perspective is helpful. Private capital operates in a dynamic and competitive environment, as GPs and LPs strive to achieve superior net returns, through good times and bad. Completing deals and generating the positive returns that LPs Mark O’Hare expect has never been more challenging than it is CEO, Preqin today, given the availability of capital and the appetite for attractive assets in the market. Innovation and answers: transparent data, combined with thoughtful dynamism have long been an integral aspect of the communication and debate. private capital industry’s arsenal of tools, comprised of alignment of interest; close attention to operational Preqin’s raison d’être is to support and serve the excellence and value add; over-allocation in order to alternative assets industry with the best available data. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

Mercer Capital's Value Focus

MERCER CAPITAL’S VALUE FOCUS » THIRD QUARTER 2009 Mercer Capital provides asset managers, trust companies, and investment consultants Asset Management with corporate valuation, fi nancial reporting valuation, transaction advisory, portfolio valuation, and related services. Call Matt Industry Crow or Brooks Hamner at 901.685.2120 to discuss your needs in confi dence. Segment Focus: Alternative Asset Managers It is no surprise that companies employing massive amounts of leverage to make risky bets 20.00% on perceived mispricings and underperforming businesses have seen their own share prices 10.00% fl uctuate wildly over the last 12 months. Most 0.00% notably, Fortress Investment Group lost nearly 90% of its market cap in the fourth quarter of -10.00% 2008, which preceded a seven-fold increase in the months to follow. Most other publicly -20.00% traded hedge funds and private equity managers have experienced similar volatility, as our index -30.00% of alternative asset managers dropped roughly -40.00% half its value in the fourth quarter last year and is up almost 60% year-to-date. Investor anxiety, -50.00% credit disruptions, market deterioration and BX BAM FIG GLG OZM subsequent recovery, coupled with a gradual Alternative Asset Managers S&P 500 thawing of the credit markets and a few quarters of earnings surprises, are largely to blame for these variations. Political events may have also contributed to the volatility of these insider trading scheme could revitalize investor scrutiny and induce investments. Many analysts have suggested that compensation limits at even tighter regulation of alternative asset managers, whose reputation Wall Street fi rms that owe money to the government will unintentionally and AUM are still badly bruised from the catastrophic second half of benefi t hedge funds and other alternative asset managers, who may be last year. -

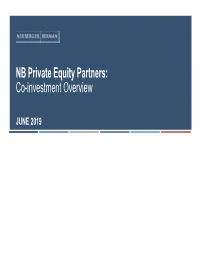

Co-Investment Overview

NB Private Equity Partners: Co-investment Overview JUNE 2019 NB Private Equity Partners (“NBPE”) Key Highlights Investment Type by Fair Value1 Equity Listing Date: 2007 Co-investments 84% Market Capitalisation (3/6/19): £510.7m Net Asset Value (NAV)1: $878.2 NAV per Share1: $18.57 Funds Income 4% Investments 12% 1 Based on 30 April 2019 re-stated Net Asset Value. NB PRIVATE EQUITY PARTNERS CO-INVESTMENT OVERVIEW 2 NBPE’s Manager: Neuberger Berman Neuberger Berman manages over $70 billion in Private Equity commitments Equity Key Highlights Co-investments Credit 30 years as a private equity investor LP in over 530 active private equity funds Expertise across fund investments, direct investments and income investments Over 200 dedicated private equity investment Funds Specialty professionals with extensive networks Strategies Leading, Global Private Equity Platform Note: Represents aggregate committed capital since inception as of April 2019, including commitments in the process of documentation. NB PRIVATE EQUITY PARTNERS CO-INVESTMENT OVERVIEW 3 Private Equity & Co-investments Overview Private Equity Co-investments Co-investments provide direct private equity exposure at the company level and often possess the advantage of no associated fees or carry. Such investments require extensive due diligence and industry expertise for proper evaluation Equity Syndication (can be pre or post investment closing) Financial Sponsor Investor Direct Investment Co-investment Portfolio Company Source: Neuberger Berman. NB PRIVATE EQUITY PARTNERS CO-INVESTMENT OVERVIEW 5 The Need for Co-Investment Capital Co-investors are used in a variety of situations and offer clear advantages GENERAL PARTNERS SEEK CO-INVESTORS FOR A VARIETY OF PURPOSES: Provide equity to complete transactions Manage portfolio exposure Extend LP relationships Familiarise investors with GP investment process Provide independent valuation for mid-life situations Source: Neuberger Berman. -

Walker Report

WALKER REPORT NOVEMBER 2018 Our Support of the Walker Report Over the past several years, Kohlberg Kravis Roberts & Co. L.P. Overview of KKR and our private equity business (together with its affiliates, “KKR,” “we” or “us”) has been KKR is a leading global investment firm that manages multiple working to increase the transparency of our investment activities alternative asset classes, including private equity, energy, and processes, both through formal compliance with guidelines infrastructure, real estate and credit, with strategic partners recommending increased levels of disclosure as well as through that manage hedge funds. KKR aims to generate attractive voluntary initiatives with our clients, partners, portfolio investment returns for its fund investors by following a patient companies and the public at large. and disciplined investment approach, employing world-class In November 2007, a working group formed by The British people, and driving growth and value creation with KKR portfolio Private Equity and Venture Capital Association (“BVCA”) and companies. KKR invests its own capital alongside the capital it led by Sir David Walker issued the Guidelines for Disclosure manages for fund investors and provides financing solutions and Transparency in Private Equity. That publication, which is and investment opportunities through its capital markets also known as the “Walker Report,” makes specific business. References to KKR’s investments may include the recommendations for improving the level of public disclosure activities of its sponsored funds. For additional information by private equity firms operating in the United Kingdom. about KKR & Co. Inc. (NYSE: KKR), please visit KKR’s website at www.kkr.com and on Twitter @KKR_Co. -

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum and Rosemary Batt Working Paper No

Private Equity Buyouts in Healthcare: Who Wins, Who Loses? Eileen Appelbaum* and Rosemary Batt† Working Paper No. 118 March 15, 2020 ABSTRACT Private equity firms have become major players in the healthcare industry. How has this happened and what are the results? What is private equity’s ‘value proposition’ to the industry and to the American people -- at a time when healthcare is under constant pressure to cut costs and prices? How can PE firms use their classic leveraged buyout model to ‘save healthcare’ while delivering ‘outsized returns’ to investors? In this paper, we bring together a wide range of sources and empirical evidence to answer these questions. Given the complexity of the sector, we focus on four segments where private equity firms have been particularly active: hospitals, outpatient care (urgent care and ambulatory surgery centers), physician staffing and emergency * Co-Director and Senior Economist, Center for Economic and Policy Research. [email protected] † Alice H. Cook Professor of Women and Work, HR Studies and Intl. & Comparative Labor ILR School, Cornell University. [email protected]. We thank Andrea Beaty, Aimee La France, and Kellie Franzblau for able research assistance. room services (surprise medical billing), and revenue cycle management (medical debt collecting). In each of these segments, private equity has taken the lead in consolidating small providers, loading them with debt, and rolling them up into large powerhouses with substantial market power before exiting with handsome returns. https://doi.org/10.36687/inetwp118 JEL Codes: I11 G23 G34 Keywords: Private Equity, Leveraged Buyouts, health care industry, financial engineering, surprise medical billing revenue cycle management, urgent care, ambulatory care. -

Private Equity in the 2000S 1 Private Equity in the 2000S

Private equity in the 2000s 1 Private equity in the 2000s Private equity in the 2000s relates to one of the major periods in the history of private equity and venture capital. Within the broader private equity industry, two distinct sub-industries, leveraged buyouts and venture capital experienced growth along parallel although interrelated tracks. The development of the private equity and venture capital asset classes has occurred through a series of boom and bust cycles since the middle of the 20th century. As the 20th century ended, so, too, did the dot-com bubble and the tremendous growth in venture capital that had marked the previous five years. In the wake of the collapse of the dot-com bubble, a new "Golden Age" of private equity ensued, as leveraged buyouts reach unparalleled size and the private equity firms achieved new levels of scale and institutionalization, exemplified by the initial public offering of the Blackstone Group in 2007. Bursting the Internet Bubble and the private equity crash (2000–2003) The Nasdaq crash and technology slump that started in March 2000 shook virtually the entire venture capital industry as valuations for startup technology companies collapsed. Over the next two years, many venture firms had been forced to write-off large proportions of their investments and many funds were significantly "under water" (the values of the fund's investments were below the amount of capital invested). Venture capital investors sought to reduce size of commitments they had made to venture capital funds and in numerous instances, investors sought to unload existing commitments for cents on the dollar in the secondary market. -

Unpacking Private Equity Characteristics and Implications by Asset Class

Unpacking Private Equity Characteristics and Implications by Asset Class www.mccombiegroup.com | +1 (786) 664-8340 Unpacking Private Equity: Characteristics & implications by asset class The term private equity is often treated as a catchall, used interchangeably to describe a broad variety of investments. Such loose use of the phrase fails to capture the range of nuanced business ownership strategies it refers to and risks branding an entire asset class with characteristics and implications that are typically relevant to only a particular sub-category. Recently, this has especially been the case given the outsized global attention placed on the leveraged buyout deals of Bain Capital, a private equity firm founded by Republican U.S. presidential candidate Mitt Romney. In this context, popular discourse has inappropriately attached the label of private equity to a general practice of debt-fueled corporate takeovers that disproportionately focus on cost cutting. In reality, however, private equity refers to an array of investment strategies each with a unique risk-return profile and differing core skillsets for success. This article is intended to help family office executives better understand the nuances of the various sub-categories of private equity. It seeks to draw high-level distinctions, serving as a practical guide for investors entering the private equity arena, be it directly or through a more curated fund structure. Ultimately by understanding the characteristics and implications of each asset class, the reader should be equipped to make an educated choice regarding the most relevant and appropriate strategy for their unique profile. From a technical perspective, private equity is nothing more than making investments into illiquid non-publicly traded companies— i.e.