Private Equity in the 2000S 1 Private Equity in the 2000S

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Financial Services & Technology

Leadership Newsleter Financial Services & Technology Fall 2015 GTCR Firm Update Since the firm’s inception in 1980, GTCR has partnered with management teams to build and transform growth businesses, investing over $12 billion in more than 200 companies. In January 2014, we closed GTCR Fund XI, the firm’s largest fund to date, with $3.85 billion of limited partner equity capital commitments. To date, we have made five investments in Fund XI. Financial Services & Technology Group Update GTCR's Financial Services & Technology group has stayed very busy in 2015: with the sale of three porfolio companies, Premium Credit Limited, Fundtech and AssuredPartners; the pending sales of Ironshore and The Townsend Group; and the acquisition by Opus Global of Alacra, a provider of KYC compliance workflow sotware to financial institutions. Industry Viewpoints During the extended bull market since the Great Recession, “fintech” has become one of the hotest segments of the economy in terms of media and investor focus. The space has received intense media atention and an influx of capital from venture capitalists and traditional strategic buyers looking to avoid falling behind the curve. Unlike many industries where wholesale technology changes can quickly upend a traditional landscape, financial services requires a more nuanced evolution of technological progress given heightened regulatory requirements, dependence on human capital and the need for trust in financial markets. Many new entrants in the fintech space (both companies and investors) have focused heavily on the “tech” and less on the “fin.” Unlike many new investors in the space, GTCR sees technology not as a separate subsector but as an integral part of financial services, and we have been investing behind the adoption of technology throughout the industry for over two decades. -

Form 3 FORM 3 UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

SEC Form 3 FORM 3 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 OMB APPROVAL INITIAL STATEMENT OF BENEFICIAL OWNERSHIP OF OMB Number: 3235-0104 Estimated average burden SECURITIES hours per response: 0.5 Filed pursuant to Section 16(a) of the Securities Exchange Act of 1934 or Section 30(h) of the Investment Company Act of 1940 1. Name and Address of Reporting Person* 2. Date of Event 3. Issuer Name and Ticker or Trading Symbol Requiring Statement EASTMAN KODAK CO [ EK ] Chen Herald Y (Month/Day/Year) 09/29/2009 (Last) (First) (Middle) 4. Relationship of Reporting Person(s) to Issuer 5. If Amendment, Date of Original Filed C/O KOHLBERG KRAVIS ROBERTS & (Check all applicable) (Month/Day/Year) CO. L.P. X Director 10% Owner Officer (give title Other (specify 2800 SAND HILL ROAD, SUITE 200 below) below) 6. Individual or Joint/Group Filing (Check Applicable Line) X Form filed by One Reporting Person (Street) MENLO Form filed by More than One CA 94025 Reporting Person PARK (City) (State) (Zip) Table I - Non-Derivative Securities Beneficially Owned 1. Title of Security (Instr. 4) 2. Amount of Securities 3. Ownership 4. Nature of Indirect Beneficial Ownership Beneficially Owned (Instr. 4) Form: Direct (D) (Instr. 5) or Indirect (I) (Instr. 5) Table II - Derivative Securities Beneficially Owned (e.g., puts, calls, warrants, options, convertible securities) 1. Title of Derivative Security (Instr. 4) 2. Date Exercisable and 3. Title and Amount of Securities 4. 5. 6. Nature of Indirect Expiration Date Underlying Derivative Security (Instr. 4) Conversion Ownership Beneficial Ownership (Month/Day/Year) or Exercise Form: (Instr. -

Private Equity Investment in Health Care in 2018: a Year in Review Page 1 of 9

Private Equity Investment in Health Care in 2018: A Year in Review Page 1 of 9 Private Equity Investment in Health Care in 2018: A Year in Review PG Bulletin March 14, 2019 Alé Dalton (Bradley Arant Boult Cummings LLP, Nashville, TN) Cody G. Robertson (InnovAge, Denver, CO) Jed Roebuck (Chambliss Bahner & Stophel PC, Chattanooga, TN) This Bulletin is brought to you by AHLA’s Transactions Affinity Group of the Business Law and Governance Practice Group. 2018 saw a remarkable volume and breadth of private equity and venture capital investment in health care, with transactions spanning the spectrum of primary care, to specialty care, to whole hospital systems, and reaching beyond the direct provision of care to ancillary services involving data management and electronic health records. The industry saw similar breadth in transaction size, ranging from single practice acquisitions to multi-billion dollar take-private transactions. This Bulletin summarizes five notable transactions or clusters of transactions that were indicative of private equity investment in health care in 2018. Primary Care Enters the Conversation After years of private equity focus on specialty providers, 2018 saw significant investor interest in primary care. Two notable https://www.healthlawyers.org/Members/PracticeGroups/blg/alerts/Pages/Private_Equity_In... 4/6/2019 Private Equity Investment in Health Care in 2018: A Year in Review Page 2 of 9 transactions highlight the growing investment in the primary care space: the $350 million investment in One Medical by The Carlyle Group and a $100 million Series E investment in Iora Health. One Medical is the largest independently held primary care practice in the United States. -

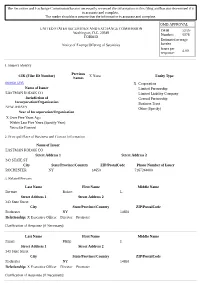

The Securities and Exchange Commission Has Not Necessarily Reviewed the Information in This Filing and Has Not Determined If It Is Accurate and Complete

The Securities and Exchange Commission has not necessarily reviewed the information in this filing and has not determined if it is accurate and complete. The reader should not assume that the information is accurate and complete. OMB APPROVAL UNITED STATES SECURITIES AND EXCHANGE COMMISSION OMB 3235- Washington, D.C. 20549 Number: 0076 FORM D Estimated average Notice of Exempt Offering of Securities burden hours per 4.00 response: 1. Issuer's Identity Previous CIK (Filer ID Number) X None Entity Type Names 0000031235 X Corporation Name of Issuer Limited Partnership EASTMAN KODAK CO Limited Liability Company Jurisdiction of General Partnership Incorporation/Organization Business Trust NEW JERSEY Other (Specify) Year of Incorporation/Organization X Over Five Years Ago Within Last Five Years (Specify Year) Yet to Be Formed 2. Principal Place of Business and Contact Information Name of Issuer EASTMAN KODAK CO Street Address 1 Street Address 2 343 STATE ST City State/Province/Country ZIP/PostalCode Phone Number of Issuer ROCHESTER NY 14650 7167244000 3. Related Persons Last Name First Name Middle Name Berman Robert L. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Faraci Philip J. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Haag Joyce P. Street Address 1 Street Address 2 343 State Street City State/Province/Country ZIP/PostalCode Rochester NY 14650 Relationship: X Executive Officer Director Promoter Clarification of Response (if Necessary): Last Name First Name Middle Name Kruchten Brad W. -

2018 Online Trust Audit & Honor Roll Report

Internet Society’s Online Trust Alliance (OTA) 2 TABLE OF CONTENTS Overview & Background .......................................................................................................................... 3 Executive Summary & Highlights ............................................................................................................. 4 Best Practices Highlights ......................................................................................................................... 9 Consumer Protection .......................................................................................................................... 9 Site Security ........................................................................................................................................ 9 Privacy Trends ................................................................................................................................... 10 Domain, Brand & Consumer Protection ................................................................................................. 12 Email Authentication ......................................................................................................................... 12 Domain-based Message Authentication, Reporting & Conformance (DMARC) ................................... 14 Opportunistic Transport Layer Security (TLS) for Email ...................................................................... 15 Domain Locking ................................................................................................................................ -

HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA Case No

UNITED STATES BANKRUPTCY COURT SOUTHERN DISTRICT OF NEW YORK In re: Chapter 15 HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA Case No. 12-10631 (MG) Debtor in a Foreign Proceeding. ANDREW LAWRENCE HOSKING and BRUCE MACKAY, in Adv. Pro. No. 14-01848 (MG) their capacity as joint compulsory liquidators and duly authorized foreign representatives of HELLAS TELECOMMUNICATIONS (LUXEMBOURG) II SCA, Plaintiffs, -against- TPG CAPITAL MANAGEMENT, L.P., f/k/a TPG CAPITAL, L.P., and APAX PARTNERS, L.P., on behalf of themselves, -and- DAVID BONDERMAN, JAMES COULTER, WILLIAM S. PRICE III, TPG ADVISORS IV, INC., TPG GENPAR IV, L.P., TPG PARTNERS IV, L.P., T3 ADVISORS II, INC., T3 GENPAR II, L.P., T3 PARTNERS II, L.P., T3 PARALLEL II, L.P., TPG FOF IV, L.P., TPG FOF IV-QP, L.P., TPG EQUITY IV-A, L.P., f/k/a FIRST AMENDED COMPLAINT TPG EQUITY IV, L.P., TPG MANAGEMENT IV-B, L.P., TPG COINVESTMENT IV, L.P., TPG ASSOCIATES IV, L.P., TPG MANAGEMENT IV, L.P., TPG MANAGEMENT III, L.P., BONDERMAN FAMILY LIMITED PARTNERSHIP, BONDO-TPG PARTNERS III, L.P., DICK W. BOYCE, KEVIN R. BURNS, JUSTIN CHANG, JONATHAN COSLET, KELVIN DAVIS, ANDREW J. DECHET, JAMIE GATES, MARSHALL HAINES, JOHN MARREN, MICHAEL MACDOUGALL, THOMAS E. REINHART, RICHARD SCHIFTER, TODD B. SISITSKY, BRYAN M. TAYLOR, CARRIE A. WHEELER, JAMES B. WILLIAMS, JOHN VIOLA, TCW/CRESCENT MEZZANINE PARTNERS III NETHERLANDS, L.P., a/k/a TCW/CRESCENT MEZZANINE PARTNERS NETHERLANDS III, L.P., TCW/CRESCENT MEZZANINE PARTNERS III, L.P., a/k/a TCW/CRESCENT MEZZANINE FUND III, L.P., TCW/CRESCENT MEZZANINE TRUST III, TCW/CRESCENT MEZZANINE III, LLC, TCW CAPITAL INVESTMENT CORPORATION, DEUTSCHE BANK AG, and DOES 1-25, on behalf of themselves and a class of similarly situated persons and legal entities, Defendants. -

Private Equity 05.23.12

This document is being provided for the exclusive use of SABRINA WILLMER at BLOOMBERG/ NEWSROOM: NEW YORK 05.23.12 Private Equity www.bloombergbriefs.com BRIEF NEWS, ANALYSIS AND COMMENTARY CVC Joins Firms Seeking Boom-Era Size Funds QUOTE OF THE WEEK BY SABRINA WILLMER CVC Capital Partners Ltd. hopes its next European buyout fund will nearly match its predecessor, a 10.75 billion euro ($13.6 billion) fund that closed in 2009, according to two “I think it would be helpful people familiar with the situation. That will make it one of the largest private equity funds if Putin stopped wandering currently seeking capital. One person said that CVC European Equity Partners VI LP will likely aim to raise 10 around bare-chested.” billion euros. The firm hasn’t yet sent out marketing materials. Two people said they expect it to do so — Janusz Heath, managing director of in the second half. Mary Zimmerman, an outside spokeswoman for CVC Capital, declined Capital Dynamics, speaking at the EMPEA to comment. conference on how Russia might help its reputation and attract more private equity The London-based firm would join only a few other firms that have closed or are try- investment. See page 4 ing to raise new funds of similar size to the mega funds raised during the buyout boom. Leonard Green & Partners’s sixth fund is expected to close shortly on more than $6 billion, more than the $5.3 billion its last fund closed on in 2007. Advent International MEETING TO WATCH Corp. is targeting 7 billion euros for its seventh fund, larger than its last fund, and War- burg Pincus LLC has a $12 billion target on Warburg Pincus Private Equity XI LP, the NEW JERSEY STATE INVESTMENT same goal as its predecessor. -

The Sallie Mae Saga: a Government-Created, Student Debt Fueled Profit Machine

_Why The Sallie Mae Saga: A Government-Created, Student Debt Fueled Profit Machine January 2014 Deanne Loonin National Consumer Law Center® © Copyright 2014, National Consumer Law Center, Inc. All rights reserved. ABOUT THE AUTHOR Deanne Loonin is an attorney with the National Consumer Law Center (NCLC) and the Director of NCLC’s Student Loan Borrower Assistance Project. Deanne assists attorneys representing low-income consumers, and teaches consumer law to legal services, private consumer attorneys, and other advocates. Deanne is the co-author of NCLC’s publications Student Loan Law and Guide to Surviving Debt as well as numerous reports on the student loan industry and borrower issues. Prior to joining NCLC in 1997, Deanne worked as a legal aid attorney in Los Angeles. She is a member of the California and Massachusetts bars. ACKNOWLEDGEMENTS This report is a release of the National Consumer Law Center’s Student Loan Borrower Assistance Project. NCLC research assistant Marina Levy provided extensive research and editorial content. The author thanks NCLC colleagues Carolyn Carter, Jan Kruse, Robyn Smith and Persis Yu for valuable comments and assistance. We also thank NCLC colleague Beverlie Sopiep for layout assistance. The findings and conclusions presented in this report are those of the authors alone. NCLC’s Student Loan Borrower Assistance Project provides information about student loan rights and responsibilities for borrowers and advocates. We also seek to increase public understanding of student lending issues and to identify policy solutions to promote access to education, lessen student debt burdens, and make loan repayment more manageable. www.studentloanborrowerassistance.org ABOUT THE NATIONAL CONSUMER LAW CENTER Since 1969, the nonprofit National Consumer Law Center® (NCLC®) has used its expertise in consumer law and energy policy to work for consumer justice and economic security for low- income and other disadvantaged people, including older adults, in the United States. -

Stepstone Atlantic Fund, L.P

StepStone Atlantic Fund, L.P. Private Equity and Infrastructure Quarterly Monitoring Report For the period ending December 31, 2020 Report Prepared For: Important Information This document is meant only to provide a broad overview for discussion purposes. All information provided here is subject to change. This document is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation for any security, or as an offer to provide advisory or other services by StepStone Group LP, StepStone Group Real Assets LP, StepStone Group Real Estate LP, StepStone Conversus LLC, Swiss Capital Alternative Investments AG and StepStone Group Europe Alternative Investments Limited or their subsidiaries or affiliates (collectively, “StepStone”) in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this document should not be construed as financial or investment advice on any subject matter. StepStone expressly disclaims all liability in respect to actions taken based on any or all of the information in this document. This document is confidential and solely for the use of StepStone and the existing and potential clients of StepStone to whom it has been delivered, where permitted. By accepting delivery of this presentation, each recipient undertakes not to reproduce or distribute this presentation in whole or in part, nor to disclose any of its contents (except to its professional advisors), without the prior written consent of StepStone. While some information used in the presentation has been obtained from various published and unpublished sources considered to be reliable, StepStone does not guarantee its accuracy or completeness and accepts no liability for any direct or consequential losses arising from its use. -

Preqin Industry News: 2012 Round-Up

View the full edition of Spotlight at: https://www.preqin.com/docs/newsletters/PE/Preqin_Private_Equity_Spotlight_January_2013.pdf News Preqin Industry News Download Data Preqin Industry News: 2012 Round-Up Olivia Harmsworth looks at the notable private equity fund closures, investor commitments, deals and exits in 2012. 2012 remained challenging for fund managers attempting to raise Chart of the Month: Breakdown of Private Equity Funds Closed in 2012 capital for their funds. However, as the chart of the month shows, by Proportion of Target Size Achieved a signifi cant proportion of fund managers met or exceeded their 30% target size for their funds in 2012. Sixty percent of all private equity 26% funds to close in 2012 met or exceeded their target, a marginal 25% increase from the 58% of funds closed in 2011 which had a 20% successful fundraising period. Funds which achieved between 20% 101% and 124% of their target were most common, accounting for 16% 26% of the funds closed. The number of funds which closed exactly 15% 14% on target has decreased slightly from 2011 by two percentage 10% points to 20% in 2012. 10% Proportion of Funds Closed 6% The diffi cult fundraising conditions in Europe were highlighted at 5% 4% the start of 2012, when the experienced mid-market European 3% fund manager, Duke Street, abandoned its latest fundraising 0% 0-24% 25-49% 50-74% 75-99% 100% 101-124% 125-149% 150% or more efforts for the buyout vehicle Duke Street Capital VII, which was Proportion of Target Size Achieved targeting €850mn. However, despite the continuing prevalence Source: Preqin Funds in Market of a challenging fundraising climate, 2012 witnessed a number of high-value fund closures and deals. -

Government-Sponsored Enterprises and Their Implicit Federal Subsidy

GovernmentSponsored Enterpriks and Their Implicit Federal Subsi*: The Case of Sallie Mae GOVERNMENT-SPONSORED ENTERPRISES AND THEIR IMPLICIT FEDERAL SUBSIDY: THE CASE OF SALLIE MAE The Congress of the United States Congressional Budget Office PREFACE This report on the Student Loan Marketing Association (Sallie Mae) is part of an ongoing study of government-sponsored enterprises (GSEs). The Con- gressional Budget Office undertook the study at the request of the Senate Budget Committee and the Subcommittee on Federal Credit Programs of the Senate Banking Committee. Government-sponsored enterprises include, in addition to the Student Loan Marketing Association, the Federal National Mortgage Association, the Farm Credit Banks, the Federal Home Loan Mortgage Corporation, and the Federal Home Loan Banks. Although the emphasis in this report is on Sallie Mae, the analysis is applicable to the other sponsored enterprises. In keeping with CBO's mandate to provide ob- jective analysis, the paper offers no recommendations. This paper was prepared by Marvin Phaup of.the Budget Process Unit under the supervision of Richard P. Emery, Jr. A significant contribution to the study was made by Robert W. Hartman, Senior Analyst for Budget Pro- cess. Useful comments and suggestions were also made by Ron Boster, Jim Carr, Samuel Chase, Barry L. Cooper, Alfred B. Fitt, Ray Garea, Janet Hansen, Carol Hartwell, Timothy Howard, Ronald F. Hunt, Jan Lilja, Fred- erick C. Meltzer, Carl Mintz, William Schmidt, Robin Seiler, Kevin E. Villani, and Dan A. Woods. CBO analysts Deborah Kalcevic, Maureen McLaughlin, Roy Meyers, Mitchell Mutnick, Pearl Richardson, and Mark Weatherly also contributed to the paper. -

LIFE at KKR We Are Investors

LIFE AT KKR We are investors. But we're more than that. IT'S IN OUR DNA We're collaborative team players who are curious communities. We often measure success over about the world around us. We're passionate about years, not quarters. We value integrity in all that we always learning more and pushing to be better. do, whether it's presenting numbers accurately or Here, we're never finished growing or discovering being open and honest with a portfolio company new ideas. executive. People want to do business with those they like and trust. It's a mantra instilled in all of us People want to do business from the top down. with those they like and trust As a firm we manage investments across multiple asset classes and as individuals we are encouraged to think creatively to solve problems, explore opportunities, take on new responsibilities and challenges, put our clients first and contribute to our LIFE AT KKR | 2 We are investors. But we're more than that. Culture & Work Environment For over 40 years, our At KKR, you'll find a team of curious, driven, dedicated and intelligent professionals who enjoy working together. We all work collaborative approach hard to create a friendly environment that encourages asking continues to drive our culture questions and reaching out to others. Teamwork Entrepreneurial Spirit Integrity No matter where you sit in the Some of our best ideas come from It's at the heart of everything we do organization, you have the full giving people the time to explore, from our internal interactions to resources, network, skills and research and have conversations.