South London Freight Consolidation Centre Feasibility Study

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Lewisham Town Centre Local Plan Submission Version

Lewisham local plan Lewisham town centre local plan Submission version September 2012 PLEASE NOTE: The maps and figures within this document will be professionally altered for the final publication version. Contents 1 The plan and context 3 1.1 Lewisham town centre and the Local Plan 4 1.2 Key characteristics of Lewisham town centre 6 1.3 Summary of issues and challenges for the town centre 11 1.4 How does the LTC Local Plan relate to other policy? 12 1.5 Sustainability Appraisal and Equalities Analysis Assessment 15 2 Vision and objectives 16 2.1 The vision 17 2.2 The objectives 18 2.3 From issues to objectives 20 3 Presumption in favour of sustainable development 22 4 The spatial strategy 24 4.1 The plan boundaries 25 4.2 Introducing policy areas and sites 27 4.3 Creating a cohesive and complete town centre experience 32 5 Policy Areas and sites 37 5.1 Lewisham Gateway Policy Area 37 5.2 Loampit Vale Policy Area 41 5.3 Conington Road Policy Area 46 5.4 Lee High Road Policy Area 51 5.5 Ladywell Policy Area 55 5.6 Central Policy Area 60 6 Area-wide policies 66 6.1 Growing the local economy 67 6.1.1 Employment 69 6.1.2 Housing 73 6.1.3 Shopping 76 6.2 Building a sustainable community 84 6.2.1 Urban design 85 Lewisham TCLP Adoption Version Contents 6.2.2 Sustainable movement 89 6.2.3 Community 95 6.3 Environmental management 100 7 Implementation, monitoring and risk 106 7.1 Implementation 107 7.2 Monitoring 111 7.3 Risk 113 8 Appendix 1 - Policy, guidance and evidence base linkages 115 9 Appendix 2 - Heritage assets 122 10 Appendix 3 - Delivery strategy and monitoring framework 125 11 Appendix 4 - Lewisham town centre infrastructure schedule 134 12 Appendix 5 - UDP proposals replaced by the LTCLP 143 13 Glossary 144 Lewisham TCLP Adoption Version The plan and context 1 Section 1 of the Lewisham Town Centre Local Plan (LTCLP) firstly introduces Lewisham town centre, its strengths, weaknesses and the opportunities for it to develop and improve in the next five to ten years. -

1. Entering Into a Competition Or Promotion Hosted by Us

PRIVACY & COOKIES POLICY This Privacy Notice may vary from time to time so please check it regularly. This Notice describes the types of information collected, how that information is used and disclosed, and how you can access, modify, or delete your information. Land Securities Properties Limited (company number 961477) whose registered office is at 100 Victoria Street London SW1E 5JL (“we”, “us” or “our”) is the ‘data controller’ for the personal data we collect. We are registered with the Information Commissioner’s Office with registration number Z5806812. 1. WIFI IN OUR CENTRES Please see (wifi Link) 2. MARKETING AND GUEST SERVICES HOW DO WE COLLECT INFORMATION ABOUT YOU? 1. Entering into a competition or promotion hosted by us or our third parties: You may provide us with personal data when you subscribe to these services either online or through a physical form. 2. Enrolling for a loyalty card or a club run at our centres: you will typically provide us with your name and contact details when you enrol for a loyalty card either online or through a physical form. 3. Feedback: providing feedback to us through our online surveys where you may provide your contact details and subscribe to receiving marketing information. Our main supplier for this service is Privacy Shield accredited and based in the United States so your data will be transferred securely and legally outside of the UK. You can also provide us feedback through writing to or emailing the centre with any comments, complaints or suggestions. 4. Website usage: We may also collect information from you automatically when you access and use our Online Services, including the time and duration of your visit, the referring URL, your Internet Protocol (IP) or MAC address, the type of device you use and its operating system. -

Tall Buildings Study Draft

LEWISHAM TALL BUILDINGS STUDY DRAFT LONDON BOROUGH OF LEWISHAM Allies and Morrison Urban Practitioners February 2021 D R A F T D R A F T CONTENTS 1 INTRODUCTION AND CONTEXT 5 4 SENSITIVITY ASSESSMENT 53 1.1 Introduction, Purpose and Structure of the Study 5 4.1 Introduction 53 1.2 Introduction to The Borough 6 4.2 Assessment of Sensitivity 54 1.3 Tall Building Policy Context 7 4.3 World Heritage Sites 56 1.4 Other Relevant Guidance 10 4.4 Conservation Areas and Special Local Character 58 4.5 Listed Buildings 60 2 DEFINING WHAT IS TALL 15 4.6 Strategic and Local Views And Landmarks 62 2.1 Lewisham Borough Definition for Tall Buildings 15 4.7 Areas Characterised by Consistent Building Heights 64 2.2 Lewisham Borough Definition for Taller Buildings 15 4.8 Topography 66 2.3 Building Heights 16 4.9 Tall Building Sensitivity Map 68 2.4 Existing and Proposed Tall Buildings 18 4.10 Site Allocations 70 2.5 Average Building Heights by Area 20 2.6 Average Building Heights by Neighbourhood 22 2.7 Average Building Heights Area Analysis 24 2.8 Building Height Variance 25 2.9 Prevailing Heights 26 2.10 What is Tall 26 3 SUITABILITY ASSESSMENT 29 3.1 Introduction 29 3.2 Assessment of Suitability 30 3.3 High PTAL 32 3.4 Bakerloo Line Extension 34 3.5 Town Centres 36 3.6 Opportunity Areas 38 3.7 Growth Areas 40 3.8 Building Heights and Tall Building Clusters 42 3.9 Tall Building Suitability Map 44 3.10 Green, Open Space and Rivers 46 3.11 Cycling Transport Accessibility Level (CTAL) 48 3.12 Site Allocations 50 D R A F T D R A F T DRAFT LB LEWISHAM TALL -

96 Lewisham High Street, Lewisham London SE13 5JH

www.acuitus.co.uk lot 2 96 Lewisham High Street, Lewisham London SE13 5JH Rent Freehold Retail Investment • Entirely let to RAL Limited (t/a Quicksilver) • Nearby occupiers include Vodafone, £44,500 until 2028 Barclays Bank, Subway and Greggs per annum • Recently re-geared lease • 40 metres from Lewisham Shopping Centre exclusive • Prominent town centre position • Six Week Completion Available Ref: 4407/GT/WH PA: AS Location Description Miles: 1.4 miles south of Greenwich The property comprises a ground floor retail unit with office/storage 2 miles west of Blackheath Village accommodation on the first and second floors and a third floor attic 6 miles south-east of the City of London area which is currently unuseable. N Roads: A20, A21 Rail: Lewisham Rail (direct to Charing Cross & Cannon Street), Tenure Lewisham DLR (19 minutes to Canary Wharf) Freehold. Air: London City Airport VAT Situation VAT is not applicable to this lot. The property is situated in a prominent position on the western side of the pedestrianised High Street, close to its junction with Lee High Road. The property is situated 40 metres from an entrance to Lewisham Shopping Centre which houses retailers including Marks & Spencer, TK Maxx, BHS, H & M, Next, New Look and Boots Chemist. Other nearby occupiers include Vodafone, Barclays Bank, Subway and Greggs. Tenancy and accommodation Floor Use Floor Areas (Approx) Tenant Term Rent p.a.x. Reviews Ground Retail 118.64 sq m (1,277 sq ft) RAL LIMITED (1) 16 years and 17 days from £44,500 29/05/2017 First Office/Storage 48.62 sq m (523 sq ft) (t/a Quicksilver) 29/05/2012 until 14/06/2028 on a and LEWISHAM SHOPPING CENTRE Second Office 21.34 sq m (230 sq ft) full repairing and insuring lease 29/05/2022 Third Not Measured Totals 188.60 sq m (2,030 sq ft) £44,500 (1) As of 19th January 2012, RAL Ltd have a Dun & Bradstreet Rating of 4A1, showing minimum risk. -

Lewisham Local Plan Site Allocations – Central Area

Draft Lewisham Local Plan Site Allocations – Central area Regulation 18 stage ‘Preferred Approach’ Document Lewisham Gateway Site address: Lewisham Gateway Site, Lewisham High Street, London, SE13 Site details: Site size (ha): 5.52, Setting: Central, PTAL: In 2015: 6b, In 2021: 6b, In 2031: 6b, Ownership: Mixed public and private, Current use: Transport interchange How site was Lewisham Core Strategy (2011) and London SHLAA (2017) identified: Planning Opportunity Area, adjacent to Conservation Area, Critical Drainage Area, designations Flood Zones 1 and 2 and site constraints: Planning Full application DC/06/062375 granted in May 2009. Various reserved matters and Status: s73 minor material amendment granted April 2013 – February 2019. Started construction and development is partially complete. Timeframe for 2020/21 – 2024/25 2025/26 – 2029/30 2030/31 – 2034/35 2035/36 – 3039/40 delivery: Yes Indicative Net residential units: Non-residential floorspace: development 607 Town centre: 2,550 capacity: 1 Employment: 17,500 Existing planning consent DC/06/062375 - The comprehensive mixed use redevelopment of the Lewisham Gateway Site, SE13 (land between Rennell Street and Lewisham Railway Station) for 100000m² comprising retail (A1, A2, A3, A4 and A5), offices (B1), hotel (C1), residential (C3), education/health (D1) and leisure (D2) with parking and associated infrastructure, as well as open space and water features as follows: up to 57,000 m² residential (C3) up to 12,000 m² shops, financial & professional services (A1 & A2) up to 17,500 m² offices (B1) / education (D1) up to 5,000 m² leisure (D2) up to 4,000 m² restaurants & cafés and drinking establishments (A3 & A4) up to 3,000 m² hotel (C1) up to 1,000 m² hot food takeaways (A5) 500m² health (D1) provision of up to 500 car parking spaces revised road alignment of (part of) Lewisham High Street, Rennell Street, Molesworth Street and Loampit Vale and works to Lewisham Road. -

Vebraalto.Com

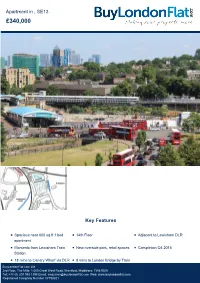

Apartment in , SE13 £340,000 Key Features ■ Spacious near 600 sq ft 1 bed ■ 14th Floor ■ Adjacent to Lewisham DLR apartment ■ Moments from Lewisham Train ■ New riverside park, retail spaces ■ Completion Q4 2016 Station ■ 18 mins to Canary Wharf via DLR ■ 8 mins to London Bridge by Train BuyLondonFlat.com Ltd 2nd Floor, The Mille, 1,000 Great West Road, Brentford, Middlesex, TW8 9DW Tel: +44 (0) 207 993 1398 Email: [email protected] Web: www.buylondonflat.com Registered Company Number 07798821 Description BuyLondonFlat is proud to present a desirable 1-bed apartment in a brand new exciting development right next to Lewisham DLR and 1min from the train station. This spacious one bedroom apartment in the 14th floor is nearly 600 sq feet. Ideal for the buy-to-let investor with projected rental yield of approx 5% or for young professionals who would appreciate the quick commute via Rail or DLR to the City and Canary Wharf. Lewisham Gateway is a brand new 24-storey tower that comprises a wide variety of studios, one, two and three apartments, numerous offering panoramic views of London's horizon, Blackheath or Greenwich. The first phase of a major regeneration project, the final development will boast a new riverside park, Confluence Place, new retail and commercial facilities, and a new pedestrianised road layout. For an extraordinary shopping day you can pick between Lewisham Shopping Centre that is a couple of minutes stroll from the property, Canary Wharf with its designer stores or Stratford where Westfield City features 334 brand stores, numerous restaurants and bistros. -

Lewisham Town Centre Local Plan Adoption Version

Lewisham local plan Lewisham town centre local plan Adoption version February 2014 &RQWHQWV 7KH SODQ DQG FRQWH[W /HZLVKDP WRZQ FHQWUH DQG WKH /RFDO 3ODQ .H\ FKDUDFWHULVWLFV RI /HZLVKDP WRZQ FHQWUH 6XPPDU\ RI LVVXHV DQG FKDOOHQJHV IRU WKH WRZQ FHQWUH +RZ GRHV WKH /7& /RFDO 3ODQ UHODWH WR RWKHU SROLF\" 6XVWDLQDELOLW\ $SSUDLVDO DQG (TXDOLWLHV $QDO\VLV $VVHVVPHQW 9LVLRQ DQG REMHFWLYHV 7KH YLVLRQ 7KH REMHFWLYHV )URP LVVXHV WR REMHFWLYHV 3UHVXPSWLRQ LQ IDYRXU RI VXVWDLQDEOH GHYHORSPHQW 7KH VSDWLDO VWUDWHJ\ 7KH SODQ ERXQGDULHV ,QWURGXFLQJ SROLF\ DUHDV DQG VLWHV &UHDWLQJ D FRKHVLYH DQG FRPSOHWH WRZQ FHQWUH H[SHULHQFH 3ROLF\ $UHDV DQG VLWHV /HZLVKDP *DWHZD\ 3ROLF\ $UHD /RDPSLW 9DOH 3ROLF\ $UHD &RQLQJWRQ 5RDG 3ROLF\ $UHD /HH +LJK 5RDG 3ROLF\ $UHD /DG\ZHOO 3ROLF\ $UHD &HQWUDO 3ROLF\ $UHD $UHDZLGH SROLFLHV *URZLQJ WKH ORFDO HFRQRP\ (PSOR\PHQW +RXVLQJ 6KRSSLQJ %XLOGLQJ D VXVWDLQDEOH FRPPXQLW\ 8UEDQ GHVLJQ /HZLVKDP 7RZQ &HQWUH /RFDO 3ODQ &RQWHQWV 6XVWDLQDEOH PRYHPHQW &RPPXQLW\ (QYLURQPHQWDO PDQDJHPHQW ,PSOHPHQWDWLRQ PRQLWRULQJ DQG ULVN ,PSOHPHQWDWLRQ 0RQLWRULQJ 5LVN $SSHQGL[ 3ROLF\ JXLGDQFH DQG HYLGHQFH EDVH OLQNDJHV $SSHQGL[ +HULWDJH DVVHWV $SSHQGL[ 'HOLYHU\ VWUDWHJ\ DQG PRQLWRULQJ IUDPHZRUN $SSHQGL[ /HZLVKDP WRZQ FHQWUH LQIUDVWUXFWXUH VFKHGXOH $SSHQGL[ 8'3 SURSRVDOV UHSODFHG E\ WKH /7&/3 *ORVVDU\ /HZLVKDP 7RZQ &HQWUH /RFDO 3ODQ 7KH SODQ DQG FRQWH[W 6HFWLRQ RI WKH /HZLVKDP 7RZQ &HQWUH /RFDO 3ODQ /7&/3 ILUVWO\ LQWURGXFHV /HZLVKDP WRZQ FHQWUH LWV VWUHQJWKV -

Portraittwo.Co.Uk

PORTRAITTWO.CO.UK WELCOME This striking 22-storey tower brings the best of contemporary living to South-East London. The Portrait Buildings are the centrepiece of one of London’s most vibrant regeneration projects, with exceptional transport links to Canary Wharf, O2 Arena and London’s prestigious universities. Comprising one, two and three bedroom apartments, the development offers current panoramic views of the London skyline, the open spaces of Blackheath and Greenwich and is situated next to one of London’s most interconnecting transport hubs. Welcome to the next generation of urban living. WELCOME TO PORTRAIT TWO. Computer Generated Image for illustrative purposes only Computer Generated Image for illustrative purposes only Final as-built product may vary from the image above LEWISHAM CONFLUENCE REGENERATION PLACE An attractive riverside park open to residents Lewisham and visitors to Lewisham, Confluence Place will is changing provide green space and an area of tranquility within the heart of the borough. It will open up the previously-hidden rivers Quaggy and Significant investment from the public and Progressive regeneration is already uniting Ravensbourne, making a natural gateway in to private sectors has introduced new opportunity elements of Lewisham Town Centre including Lewisham Town Centre. and enlivenment into Lewisham Town Centre. Lewisham Shopping Centre, the High Street and The rejuvenation of the area has created a truly Glass Mill Leisure Centre, to form a streamlined Pedestrian-only walkways create a safer, vibrant modern living destination; unmistakably hub which is easy to navigate for pedestrians cleaner environment for the residents of today, young, fresh and cosmopolitan. and cyclists as well as motorists. -

SDSC Business Development Review

_____________________________________ Overview and Scrutiny High Streets Review Sustainable Development Select Committee January 2016 _____________________________________ Membership of the Sustainable Development Select Committee in 2015- 16: Councillor Liam Curran (Chair) Councillor James-J Walsh (Vice-Chair) Councillor Bill Brown Councillor Suzannah Clarke Councillor Amanda De Ryk Councillor Carl Handley Councillor Mark Ingleby Councillor Olurotimi Ogunbadewa Councillor Eva Stamirowski Councillor Paul Upex 2 Contents Vice-Chair’s introduction 4 1. Executive summary 5 2. Recommendations 7 3. Purpose and structure of review 9 Findings 4. Background and policy review – Scoping Paper 11 5. Witnesses: a. John Miller - Planning Service 15 b. Andrew Rawlings – Land Securities 21 c. Ed Holloway – SEE3 24 6. Monitoring and ongoing scrutiny 26 3 Introduction I'm proud to present to Mayor and Cabinet this report carried out by the Sustainable Development Committee, which has undertaken a High Streets Review, which is dealing with a very contemporary issue that affects both residents and businesses alike. Ensuring that our high streets meet the current and future needs of those who use them, and those who want to grow and develop businesses in our Borough, has to be a significant priority of the council. At a time of changing local economies and markets; technological advances; and both evolving and emerging needs of communities from their public realm; it is important that Lewisham Council does not remain a passive participant, but instead uses its significant role as a Council, a landlord, and planning authority to not only facilitate these developments but craft and sculpt them, failure to do so, will mean urban decay, a proliferation of low quality or boarded up shops, and a loss of amenity from our communities. -

Annual Results 2020

Introduction Mark Allan Chief Executive Landsec 3 Introduction Reflections on Landsec Strength and resilience — Our people’s quick response to the pandemic — Working proactively and collaboratively together and for our customers — Quality of our portfolio and financial resources Leadership in sustainability — Commitment to tackling climate change — Our responsible actions on Covid-19 Opportunities for change in challenging times Cardinal Place, SW1 Financial results Martin Greenslade Chief Financial Officer Landsec 5 Our year in context Continuation of the trends in H1…. until March Office Specialist Retail April 19 to Healthy market conditions Leisure and hotels virtually full Nuanced markets mid-March 2020 Portfolio virtually full Good demand from consumers Outlets and London steady and operators despite headwinds Myo and Fitted going well in F&B market Regional retail and retail parks impacted by declining values Demonstrable progress on Cinema attendance up and poor investor sentiment development plan Hotel revenues flat Piccadilly Lights ahead of expectations Mid to Our office assets are open Leisure and hotel assets Shopping centres still open but only end-March 2020 with 10% usage closed essential shops trading Development programme Rental income down Significant reduction in rental income delayed Landsec providing support to help sustain customers and the industry Landsec 6 Financial summary 31 March 2019 31 March 2020 % change £442m Revenue profit(1) £414m -6.3 £(557)m Valuation deficit(1) £(1,179)m -8.8(2) £(123)m Loss before -

Note: Photographic Content Has Been Commissioned Post-Impact of Covid-19

Note: Photographic content has been commissioned post-impact of Covid-19 Positioning Landsec for growth Landsec – Strategy review 2020 4 Overview Mark Allan Our strategic priorities Mark Allan Marcus Geddes Colette O’Shea David Heaford Culture, capability and organisation Mark Allan Financial implications Martin Greenslade Summary Mark Allan Landsec – Strategy review 2020 5 Six key findings that inform our strategy Our strategic review identified six conclusions which shaped the development of our strategy London portfolio Talent Balance sheet Very high-quality Significant capability We have a strong London portfolio and expertise balance sheet in the business Resilient and liquid With an uncertain Clear opportunity outlook due to Covid-19 Strong foundation to leverage this, through and Brexit we cannot for new growth developing the right afford to be complacent opportunities culture Landsec – Strategy review 2020 6 Six key findings that inform our strategy Our strategic review identified six conclusions which shaped the development of our strategy Retail Portfolio mix Covid-19 Not all retail is the same Some elements of the Long-term implications of portfolio are subscale with Covid-19 are unclear and Structural challenges are little or no competitive our strategy will adapt as the significant, but limited primarily advantage picture becomes clearer to our regional shopping centres (only 13% of our portfolio) Structural growth areas We are managing near-term under-represented challenges proactively and We need to be realistic in our focused -

Renaissance Building Loampit Vale, Lewisham Se13 7Dj

RENAISSANCE BUILDING LOAMPIT VALE, LEWISHAM SE13 7DJ VIRTUAL FREEHOLD CONVENIENCE STORE IN AN AFFLUENT RESIDENTIAL LOCATION WITH 10.5 YEARS UNEXPIRED INVESTMENT CONSIDERATIONS ■ Rare opportunity to purchase ground floor convenience retail unit that services a 788 ■ Rent to increase to approximately £97,850 per annum in June 2020, based unit residential scheme within a densely populated residential suburb of London on RPI forecast of 3% for 2019/2020 ■ Prominent position on the busy Loampit Vale (A20) ■ 5 yearly reviews on RPI basis per annum compounded with a collar and cap ■ In close proximity to Lewisham DLR Station and Lewisham Railway Station of 1% - 4% ■ ■ Let to the strong covenant of Sainsbury’s Supermarkets Ltd with a further Virtual Freehold 10.5 years to expiry ■ We are instructed to seek offers in excess of £1,750,000 (One Million Seven ■ No Breaks Hundred and Fifty Thousand Pounds) reflecting a net initial yield of 5.11% assuming purchaser’s costs of 6.19% and an estimated reversionary yield ■ Effective rent passing of £95,000 per annum (£19.42psft) of 5.26% in June 2020 based on an increase to £97,850 pa G o l l i d e H a r o s d R R w m n d Po o a ts R h n u H r s o a L i M re e St. John’s & ie w w Bill l e e is t e h L Ro a a p m Elverson d t RENAISSANCE BUILDING, LOAMPIT VALE, LEWISHAM SE13 7DJ Virtual freehold Convenience Store in an affluent residential location with 10.5 years unexpired Wa Road n y o ill BLACKHEATH H M ot e Eli d T ra ra a n P q l u a i y l V a o le R A 2 l il 2 H Lo 1 1 m a a m L h p is e A it w 2