January 2000

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

![Contents [Edit] Africa](https://docslib.b-cdn.net/cover/9562/contents-edit-africa-79562.webp)

Contents [Edit] Africa

Low cost carriers The following is a list of low cost carriers organized by home country. A low-cost carrier or low-cost airline (also known as a no-frills, discount or budget carrier or airline) is an airline that offers generally low fares in exchange for eliminating many traditional passenger services. See the low cost carrier article for more information. Regional airlines, which may compete with low-cost airlines on some routes are listed at the article 'List of regional airlines.' Contents [hide] y 1 Africa y 2 Americas y 3 Asia y 4 Europe y 5 Middle East y 6 Oceania y 7 Defunct low-cost carriers y 8 See also y 9 References [edit] Africa Egypt South Africa y Air Arabia Egypt y Kulula.com y 1Time Kenya y Mango y Velvet Sky y Fly540 Tunisia Nigeria y Karthago Airlines y Aero Contractors Morocco y Jet4you y Air Arabia Maroc [edit] Americas Mexico y Aviacsa y Interjet y VivaAerobus y Volaris Barbados Peru y REDjet (planned) y Peruvian Airlines Brazil United States y Azul Brazilian Airlines y AirTran Airways Domestic y Gol Airlines Routes, Caribbean Routes and y WebJet Linhas Aéreas Mexico Routes (in process of being acquired by Southwest) Canada y Allegiant Air Domestic Routes and International Charter y CanJet (chartered flights y Frontier Airlines Domestic, only) Mexico, and Central America y WestJet Domestic, United Routes [1] States and Caribbean y JetBlue Airways Domestic, Routes Caribbean, and South America Routes Colombia y Southwest Airlines Domestic Routes y Aires y Spirit Airlines Domestic, y EasyFly Caribbean, Central and -

My Personal Callsign List This List Was Not Designed for Publication However Due to Several Requests I Have Decided to Make It Downloadable

- www.egxwinfogroup.co.uk - The EGXWinfo Group of Twitter Accounts - @EGXWinfoGroup on Twitter - My Personal Callsign List This list was not designed for publication however due to several requests I have decided to make it downloadable. It is a mixture of listed callsigns and logged callsigns so some have numbers after the callsign as they were heard. Use CTL+F in Adobe Reader to search for your callsign Callsign ICAO/PRI IATA Unit Type Based Country Type ABG AAB W9 Abelag Aviation Belgium Civil ARMYAIR AAC Army Air Corps United Kingdom Civil AgustaWestland Lynx AH.9A/AW159 Wildcat ARMYAIR 200# AAC 2Regt | AAC AH.1 AAC Middle Wallop United Kingdom Military ARMYAIR 300# AAC 3Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 400# AAC 4Regt | AAC AgustaWestland AH-64 Apache AH.1 RAF Wattisham United Kingdom Military ARMYAIR 500# AAC 5Regt AAC/RAF Britten-Norman Islander/Defender JHCFS Aldergrove United Kingdom Military ARMYAIR 600# AAC 657Sqn | JSFAW | AAC Various RAF Odiham United Kingdom Military Ambassador AAD Mann Air Ltd United Kingdom Civil AIGLE AZUR AAF ZI Aigle Azur France Civil ATLANTIC AAG KI Air Atlantique United Kingdom Civil ATLANTIC AAG Atlantic Flight Training United Kingdom Civil ALOHA AAH KH Aloha Air Cargo United States Civil BOREALIS AAI Air Aurora United States Civil ALFA SUDAN AAJ Alfa Airlines Sudan Civil ALASKA ISLAND AAK Alaska Island Air United States Civil AMERICAN AAL AA American Airlines United States Civil AM CORP AAM Aviation Management Corporation United States Civil -

Peculiarities of Development of the Low-Cost Airlines in Russian and Norwegian Context

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Brage Nord Open Research Archive Logistics and transport BE303E 003 Peculiarities of development of the low-cost airlines in Russian and Norwegian context by Elena Toramanyan Spring, 2007 Abstract E. Toramanyan, Master thesis ABSTRACT Low-cost flights per se become more and more popular in the world airline industry, while in Russia the first low-cost carrier has recently appeared. The purpose of this paper is to investigate the phenomenon of low-cost carriers, peculiarities of the development of the low-cost airlines in the context of Russian Federation and Norway. In order to cover the topic, deep literature review and qualitative research were carried out. In the paper, I attempted to follow history, analyze reasons for low-cost flights, advantages and disadvantages of low-cost carriers, scrutinize perspectives and peculiarities of the low-cost airline market in Russia and Norway, and analyze future opportunities. Under these circumstances, case study method and interviews as primary information sources and reports and articles written by airline experts as secondary sources were used. Two companies were under the research: Sky Express – a Russian low-cost airline company launched the market this year, and a Norwegian low-cost airline company, a member of European Low Fares Airline Association, Norwegian Air Shuttle. Deep literature review concerning low-cost airlines and empirical findings showed that the phenomenon of low fares has its peculiarities on a particular market. In order to understand the role of context regarding the research question, I tried to find similarities and to reveal differences in the activities of two companies with the help of PESTE analysis. -

Air Transport in Russia and Its Impact on the Economy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Tomsk State University Repository Вестник Томского государственного университета. Экономика. 2019. № 48 МИРОВАЯ ЭКОНОМИКА UDC 330.5, 338.4 DOI: 10.17223/19988648/48/20 V.S. Chsherbakov, O.A. Gerasimov AIR TRANSPORT IN RUSSIA AND ITS IMPACT ON THE ECONOMY The study aims to collect and analyse statistics of Russian air transport, show the in- fluence of air transport on the national economy over the period from 2007 to 2016, compare the sector’s role in Russia with the one in other countries. The study reveals the significance of air transport for Russian economy by comparing airlines’ and air- ports’ monetary output to the gross domestic product. On the basis of the research, the policies in the aviation sector can be adjusted by government authorities. Ключевые слова: Russia, aviation, GDP, economic impact, air transport, statistics. Introduction According to Air Transport Action Group, the air transport industry supports 62.7 million jobs globally and aviation’s total global economic impact is $2.7 trillion (approximately 3.5% of the Gross World Product) [1]. Aviation transported 4 billion passengers in 2017, which is more than a half of world population, according to the International Civil Aviation Organization [2]. It makes the industry one of the most important ones in the world. It has a consid- erable effect on national economies by providing a huge number of employment opportunities both directly and indirectly in such spheres as tourism, retail, manufacturing, agriculture, and so on. Air transport is a driving force behind economic connection between different regions because it may entail economic, political, and social effects. -

Skyteam Global Airline Alliance

Annual Report 2005 2005 Aeroflot made rapid progress towards membership of the SkyTeam global airline alliance Aeroflot became the first Russian airline to pass the IATA (IOSA) operational safety audit Aeroflot annual report 2005 Contents KEY FIGURES > 3 CEO’S ADDRESS TO SHAREHOLDERS> 4 MAIN EVENTS IN 2005 > 6 IMPLEMENTING COMPANY STRATEGY: RESULTS IN 2005 AND PRIORITY TASKS FOR 2006 Strengthening market positions > 10 Creating conditions for long-term growth > 10 Guaranteeing a competitive product > 11 Raising operating efficiency > 11 Developing the personnel management system > 11 Tasks for 2006 > 11 AIR TRAFFIC MARKET Global air traffic market > 14 The passenger traffic market in Russia > 14 Russian airlines: main events in 2005 > 15 Market position of Aeroflot Group > 15 CORPORATE GOVERNANCE Governing bodies > 18 Financial and business control > 23 Information disclosure > 25 BUSINESS IN 2005 Safety > 28 Passenger traffic > 30 Cargo traffic > 35 Cooperation with other air companies > 38 Joining the SkyTeam alliance > 38 Construction of the new terminal complex, Sheremetyevo-3 > 40 Business of Aeroflot subsidiaries > 41 Aircraft fleet > 43 IT development > 44 Quality management > 45 RISK MANAGEMENT Sector risks > 48 Financial risks > 49 Insurance programs > 49 Flight safety risk management > 49 PERSONNEL AND SOCIAL RESPONSIBILITY Personnel > 52 Charity activities > 54 Environment > 55 SHAREHOLDERS AND INVESTORS Share capital > 58 Securities > 59 Dividend history > 61 Important events since December 31, 2005 > 61 FINANCIAL REPORT Statement -

Hva Er Rovatferd?

Hovedoppgave for mastergradsstudiet i samfunnsøkonomi Hva er rovatferd? Eksempler fra norsk luftfart Harald Evensen Mai 2006 Økonomisk institutt Universitetet i Oslo i Forord Det er de store endringene i flymarkedet, og den spesielle konkurransesituasjonen, som gjorde at jeg ønsket å skrive om dette temaet. De fleste av oss har merket at det er billigere å fly til Bergen i dag, enn hva tilfellet var for kun noen få år siden. Jeg håper denne oppgaven kan være med på å belyse hva som har skjedd i det norske flymarkedet, og hvilke former konkurransen har tatt de siste åtte årene, etter åpningen av Oslo Lufthavn Gardermoen. Min veileder, Professor Tore Nilssen ved Økonomisk institutt ved Universitetet i Oslo, har vært til stor hjelp både når det gjelder å konsentrere oppgaven rundt ett tema – rovatferd – og å komme med konkrete tilbakemeldinger som har gjort innhold og språk bedre. Jeg vil også benytte anledningen til å takke min kjæreste, Kari, som har lest korrektur og passet på at jeg ikke har sittet og furtet for lenge de gangen det har gått trått med oppgaven. Oslo, 2. mai 2006 Harald Evensen ii Innhold Forord………………………………………………………………………………......... i 1. Innledning………………………………………………………………………... 1 2. Luftfartsmarkedet i Norge……………………………………………………… 3 2.1 Beskrivelse av markedet………………………………………………….. 3 2.2 Kampen mot Color Air…………………………………………………… 7 2.3 Braathens gir opp…………………………………………………………. 9 2.4 Bonusavtaler og storkundeavtaler………………………………………… 11 2.4.1 Bonusavtaler………………………………………………………. 11 2.4.2 Storkundeavtaler………………………………………………….. 12 2.5 Konkurranse på nytt………………………………………………………. 13 2.6 Rovatferd mot en liten konkurrent?............................................................. 15 2.7 Sunn konkurranse?....................................................................................... 17 3. Rovatferd………………………………………………………………………… 19 3.1 Hva er rovatferd? Definisjoner og utdypning…………………………..... -

January 2001

A VERY HAPPY AND PROSPEROUS 2001 TO ALL OUR READERS Aviation Strategy Issue No: 39 January 2001 GAO: no seasonal cheer for UAL/US CONTENTS Analysis s the Justice Department's antitrust review of the proposed UAL/US AAirways merger looked like entering the home stretch, on December 20 Competition report on US General Accounting Office (GAO) released a mostly negative report on United/US Airways merger 1-2 the competitive merits of the deal. What are GAO's views on the matter and how is the DoJ likely to rule? Indian privatisation: will The GAO report, titled "Issues related to the proposed United Airlines- US Airways merger", was requested by two members of Congress, James its potential be fulfilled? 3-5 Oberstar and Louise Slaughter, and carries political weight. However, its focus was naturally much narrower than that of the DoJ investigation, which BA in 2001 6 is currently anticipated to be concluded in January. The report did not examine in detail the impact of the proposed merger Review: The airline business on airline concentration at particular cities or effects on new market entry - subjects that the DoJ is interested in. Nor did it evaluate US Airways' long in the 21st century 6 term financial viability - something that United and US Airways hope that the DoJ will give some weight to. Briefings The GAO report, first, looked at how the merger would alter the US domestic industry using common measures of market strength. Second, it Russian airlines: assessed effects on consumers by analysing data in specific markets. the first alliance and Third, it compared DC Air's plans with the service scheduled by competi- other developments 7-10 tors by analysing frequencies and types of aircraft operated. -

Valuation of Norwegian Air Shuttle Asa As of 31.12.2010

Valuation of Norwegian Air Shuttle ASA as of 31.12.2010 Copenhagen Business School, January 2012 Program: Accounting Strategy and Control Number of pages: 80 Supervisor: Number of characters: 191 423 Jeppe Schoenfeld, external Executive summary The aim of the thesis was to estimate the share price of Norwegian Air Shuttle ASA as of 31.12.10 from an investor’s point of view. Strategic and financial analyses were conducted in order to forecast future financial statements and required rate of return to apply in a discounted cash flow model. The Nordic market for air travel was analyzed under the concept of a perfect market. This analysis concluded that the market, and especially the leisure segment, was highly competitive because of limited differentiation opportunities, low switching costs and brand loyalty, and few entrance barriers on new routes for existing airlines. Airlines’ cost structure were characterized by a high degree of fixed and batch costs, which implied significant economic of scale benefits. This has contributed to high capacity in the market after the low cost carriers (LCCs) entrance and been a driver of the heavy unit price decrease seen the last ten years. The strategic analysis also evaluated Norwegian’s future revenue growth potential in the Nordic market, partly based on historical development. Norwegian is positioned as the dominant actor in the Nordic leisure segment and challenges SAS in the business segment. The major finding of the financial analyses was that Norwegian has generated an unstable EBITDAR-margin, which has been the major underlying factor to the volatile return on invested capital. -

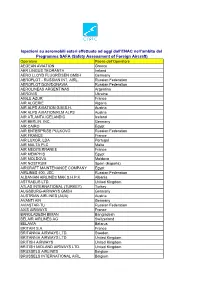

Compagnie Aeree Ispezionate

Ispezioni su aeromobili esteri effettuate ad oggi dall’ENAC nell’ambito del Programma SAFA (Safety Assessment of Foreign Aircraft) Operatore Paese dell'Operatore AEGEAN AVIATION Greece AER LINGUS TEORANTA Ireland AERO LLOYD FLUGREISEN GMBH Germany AEROFLOT - RUSSIAN INT. AIRL. Russian Federation AEROFLOT DON/DONAVIA Russian Federation AEROLINEAS ARGENTINAS Argentina AEROVIS Ukraine AIGLE AZUR France AIR ALGERIE Algeria AIR ALPS AVIATION G.M.B.H. Austria AIR ALPS AVIATION/KLM ALPS Austria AIR ATLANTA ICELANDIC Iceland AIR BERLIN, INC. Germany AIR CAIRO Egypt AIR ENTERPRISE PULKOVO Russian Federation AIR FRANCE France AIR LUXOR, LDA Portugal AIR MALTA PLC Malta AIR MEDITERRANEE France AIR MEMPHIS Egypt AIR MOLDOVA Moldova AIR NOSTRUM Spain (España) AIRCRAFT MAINTENANCE COMPANY Egypt AIRLINES 400, JSC Russian Federation ALBANIAN AIRLINES MAK S.H.P.K. Albania ASTRAEUS LTD. United Kingdom ATLAS INTERNATIONAL (TURKEY) Turkey AUGSBURG-AIRWAYS GMBH Germany AUSTRIAN AIRLINES (AUA) Austria AVANTI AIR Germany AVIASTAR-TU Russian Federation AXIS AIRWAYS France BANGLADESH BIMAN Bangladesh BELAIR AIRLINES AG Switzerland BELAVIA Belarus BRITAIR S.A. France BRITANNIA AIRWAYS LTD. Sweden BRITANNIA AIRWAYS LTD. United Kingdom BRITISH AIRWAYS United Kingdom BRITISH MIDLAND AIRWAYS LTD. United Kingdom BRUSSELS AIRLINES Belgium BRUSSELS INTERNATIONAL AIRL. Belgium CAIRO AIR TRANSPORT COMPANY Egypt CARPATAIR S.A. Romania CATHAY PACIFIC AIRWAYS LTD. Hong Kong CHINA AIRLINES Taiwan (Republic of China) CIMBER AIR A/S Denmark CIRRUS LUFTFAHRTGESELL. MBH Germany CONDOR FLUGDIENST GMBH Germany CORSE AIR INTERNATIONAL France CYPRUS AIRWAYS LTD. Cyprus CZECH AIRLINES J.S.C. Czech Republic DANISH AIR TRANSPORT Denmark DENIM AIR Netherlands EAST LINE AIRLINES Russian Federation EASYJET AIRLINES CO. LTD United Kingdom EDELWEISS AIR AG Switzerland EGYPT AIR Egypt EL AL - ISRAEL AIRLINES LTD. -

PROCEEDINGS of the 40Th ANNUAL MEETING

PROCEEDINGS OF THE40 Th ANNUAL MEETING OF ME TRANSPORTATION RESEARCH FORUM Philadelphia, Pennsylvania October 29-31, 1998 Volume 1 AsS 2,1 Welcome to the Transportation Research Forum's 1998 Annual Meeting These proceedings contain those papers presented at the 40th Annual Meeting of the Transportation Research Forum, held in Philadelphia from October 29-31, 1998, that were received by the deadline publishing date. All papers were reviewed by the Program Vice President to assess their suitability for inclusion in these volumes. Additional papers may be made available by some of the presenters at the time of the Conference. The Transportation Research Forum (TRF) is an independent organization of transportation professionals providing pertinent and timely information to those who conduct research and those who use and benefit from research. It functions as an impartial meeting ground for carriers, shippers, government officials, consultants, university researchers, suppliers, and others seeking an exchange of information and ideas related to both passenger and freight transportation. The Transportation Research Forum started with a small group of transportation researchers in New York in 1958 and the first national meeting was held in St. Louis in 1960. National meetings have been held annually since 1960 at various cities throughout the U.S. and Canada. Numerous TRF members and supporters aided in the development of this year's Forum, but it is authors of the papers, the organizers and contributors to the various panels, and the session chairs who make TRF annual meetings so worthwhile and enjoyable. The conference program simply reflects the interests, enthusiasm and commitment of those members of the transportation community. -

Change 3, FAA Order 7340.2A Contractions

U.S. DEPARTMENT OF TRANSPORTATION CHANGE FEDERAL AVIATION ADMINISTRATION 7340.2A CHG 3 SUBJ: CONTRACTIONS 1. PURPOSE. This change transmits revised pages to Order JO 7340.2A, Contractions. 2. DISTRIBUTION. This change is distributed to select offices in Washington and regional headquarters, the William J. Hughes Technical Center, and the Mike Monroney Aeronautical Center; to all air traffic field offices and field facilities; to all airway facilities field offices; to all international aviation field offices, airport district offices, and flight standards district offices; and to the interested aviation public. 3. EFFECTIVE DATE. July 29, 2010. 4. EXPLANATION OF CHANGES. Changes, additions, and modifications (CAM) are listed in the CAM section of this change. Changes within sections are indicated by a vertical bar. 5. DISPOSITION OF TRANSMITTAL. Retain this transmittal until superseded by a new basic order. 6. PAGE CONTROL CHART. See the page control chart attachment. Y[fa\.Uj-Koef p^/2, Nancy B. Kalinowski Vice President, System Operations Services Air Traffic Organization Date: k/^///V/<+///0 Distribution: ZAT-734, ZAT-464 Initiated by: AJR-0 Vice President, System Operations Services 7/29/10 JO 7340.2A CHG 3 PAGE CONTROL CHART REMOVE PAGES DATED INSERT PAGES DATED CAM−1−1 through CAM−1−2 . 4/8/10 CAM−1−1 through CAM−1−2 . 7/29/10 1−1−1 . 8/27/09 1−1−1 . 7/29/10 2−1−23 through 2−1−27 . 4/8/10 2−1−23 through 2−1−27 . 7/29/10 2−2−28 . 4/8/10 2−2−28 . 4/8/10 2−2−23 . -

Airlines Codes

Airlines codes Sorted by Airlines Sorted by Code Airline Code Airline Code Aces VX Deutsche Bahn AG 2A Action Airlines XQ Aerocondor Trans Aereos 2B Acvilla Air WZ Denim Air 2D ADA Air ZY Ireland Airways 2E Adria Airways JP Frontier Flying Service 2F Aea International Pte 7X Debonair Airways 2G AER Lingus Limited EI European Airlines 2H Aero Asia International E4 Air Burkina 2J Aero California JR Kitty Hawk Airlines Inc 2K Aero Continente N6 Karlog Air 2L Aero Costa Rica Acori ML Moldavian Airlines 2M Aero Lineas Sosa P4 Haiti Aviation 2N Aero Lloyd Flugreisen YP Air Philippines Corp 2P Aero Service 5R Millenium Air Corp 2Q Aero Services Executive W4 Island Express 2S Aero Zambia Z9 Canada Three Thousand 2T Aerocaribe QA Western Pacific Air 2U Aerocondor Trans Aereos 2B Amtrak 2V Aeroejecutivo SA de CV SX Pacific Midland Airlines 2W Aeroflot Russian SU Helenair Corporation Ltd 2Y Aeroleasing SA FP Changan Airlines 2Z Aeroline Gmbh 7E Mafira Air 3A Aerolineas Argentinas AR Avior 3B Aerolineas Dominicanas YU Corporate Express Airline 3C Aerolineas Internacional N2 Palair Macedonian Air 3D Aerolineas Paraguayas A8 Northwestern Air Lease 3E Aerolineas Santo Domingo EX Air Inuit Ltd 3H Aeromar Airlines VW Air Alliance 3J Aeromexico AM Tatonduk Flying Service 3K Aeromexpress QO Gulfstream International 3M Aeronautica de Cancun RE Air Urga 3N Aeroperlas WL Georgian Airlines 3P Aeroperu PL China Yunnan Airlines 3Q Aeropostal Alas VH Avia Air Nv 3R Aerorepublica P5 Shuswap Air 3S Aerosanta Airlines UJ Turan Air Airline Company 3T Aeroservicios