Biotech Investor Since 1993

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Market Notice Date: 14 November 2019 Market Notice Number: 112/2019

Market Notice Date: 14 November 2019 Market Notice Number: 112/2019 Equiduct Universe Change Please see today's changes below effective 18 November 2019: Trading Reporting MIC Settlement Trading Settlement Tick Size Change/ Security Name ISIN Home Market Symbol Country Currency Currency table Action ABB LTD ABBNz CH0012221716 XSWX EQTB CH CHF CHF ESMA_E Deletion ABB ABBs CH0012221716 XSTO EQTB SE SEK SEK ESMA_E Deletion ADECCO SA ADENz CH0012138605 XSWX EQTC CH CHF CHF ESMA_E Deletion AMS AG AMSz AT0000A18XM4 XSWX EQTC CH CHF CHF ESMA_E Deletion ARYZTA AG ARYNz CH0043238366 XSWX EQTB CH CHF CHF ESMA_E Deletion JULIUS BAER GRUPPE AG BAERz CH0102484968 XSWX EQTC CH CHF CHF ESMA_E Deletion BALOISE-HLDGS BALNz CH0012410517 XSWX EQTC CH CHF CHF ESMA_D Deletion BARRY CALLEBAUT AG BARNz CH0009002962 XSWX EQTC CH CHF CHF ESMA_D Deletion BB BIOTECH BBZAd CH0038389992 XETR EQTB DE EUR EUR ESMA_D Deletion BB BIOTECH BIONz CH0038389992 XSWX EQTB CH CHF CHF ESMA_D Deletion BASILEA PHARMACEUTICA AG BSLNz CH0011432447 XSWX EQTC CH CHF CHF ESMA_D Deletion BUCHER INDUSTRIES BUCNz CH0002432174 XSWX EQTC CH CHF CHF ESMA_D Deletion COMPAGNIE FINANCIERE RICHEMONT CFRz CH0210483332 XSWX EQTC CH CHF CHF ESMA_E Deletion CLARIANT CLNz CH0012142631 XSWX EQTC CH CHF CHF ESMA_E Deletion CEMBRA MONEY BANK AG CMBNz CH0225173167 XSWX EQTC CH CHF CHF ESMA_D Deletion CREDIT SUISSE GROUP AG CSGNz CH0012138530 XSWX EQTC CH CHF CHF ESMA_E Deletion DKSH HOLDING DKSHz CH0126673539 XSWX EQTC CH CHF CHF ESMA_D Deletion DORMA+KABA HOLDING AG DOKAz CH0011795959 XSWX EQTC CH CHF -

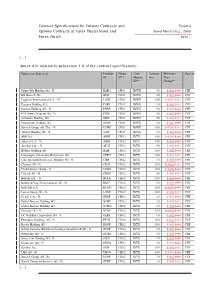

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1

Contract Specifications for Futures Contracts and Eurex14 Options Contracts at Eurex Deutschland and Stand March 2831, 2008 Eurex Zürich Seite 1 [....] Annex A in relation to subsection 1.6 of the contract specifications: Futures on Shares of Produkt- Group Cash Contract Minimum Currency ID ID** Market- Size Price ID** Change* Julius Bär Holding AG - N. BAEG CH01 XSWX 50 0.0010.01 CHF BB Biotech AG BIOF CH01 XSWX 50 0.0010.01 CHF Logitech International S.A. - N. LOGF CH01 XSWX 100 0.00010.01 CHF Pargesa Holding S.A. PARF CH01 XSWX 10 0.0010.01 CHF Sonova Holding AG - N. PHBF CH01 XSWX 50 0.0010.01 CHF PSP Swiss Property AG - N. PSPF CH01 XSWX 50 0.0010.01 CHF Schindler Holding AG SINF CH01 XSWX 50 0.0010.01 CHF Straumann Holding AG STMF CH01 XSWX 10 0.0010.01 CHF Swatch Group AG, The - N. UHRF CH01 XSWX 100 0.00010.01 CHF Valiant Holding AG - N. VATF CH01 XSWX 10 0.0010.01 CHF ABB Ltd. ABBF CH02 XVTX 100 0.00010.01 CHF Adecco S.A. - N. ADEF CH02 XVTX 100 0.0010.01 CHF Actelion Ltd. - N. ATLG CH02 XVTX 50 0.0010.01 CHF Bâloise Holding AG BALF CH02 XVTX 100 0.0010.01 CHF Compagnie Financière Richemont AG CFRH CH02 XVTX 100 0.0010.01 CHF Ciba Spezialitätenchemie Holding AG - N. CIBF CH02 XVTX 10 0.0010.01 CHF Clariant AG - N. CLNF CH02 XVTX 100 0.00010.01 CHF Credit Suisse Group - N. CSGG CH02 XVTX 100 0.00010.01 CHF Geberit AG - N. -

2019 Switzerland Spencer Stuart Board Index

2019 Switzerland Spencer Stuart Board Index About Spencer StuArt Spencer Stuart has had an uninterrupted presence in Switzerland since 1959, when it opened its Zurich office. Spencer Stuart is one of the world’s leading executive search consulting firms. We are trusted by organisations around the world to help them make the senior-level leadership decisions that have a lasting impact on their enterprises. Through our executive search, board and leadership advisory services, we help build and enhance high-performing teams for select clients ranging from major multinationals to emerging companies to nonprofit institutions. Privately held since 1956, we focus on delivering knowledge, insight and results though the collaborative efforts of a team of experts — now spanning more than 60 offices, over 30 countries and more than 50 practice specialties. Boards and leaders consistently turn to Spencer Stuart to help address their evolving leadership needs in areas such as senior-level executive search, board recruitment, board effectiveness, succession planning, in-depth senior management assessment and many other facets of organisational effectiveness. For more information on Spencer Stuart, please visit www.spencerstuart.com. Social Media @ Spencer Stuart Stay up to date on the trends and topics that are relevant to your business and career. @Spencer Stuart © 2020 Spencer Stuart. All rights reserved. For information about copying, distributing and displaying this work, contact: [email protected]. 1 spencer stuart Contents 3 Foreword -

SIX Swiss Exchange Message No. 42/2018

SIX Swiss Exchange message no. 42/2018 Subject Change of trading segments due to the ordinary index review Category Index Adjustments Authorized by Adrian Isler, Head Market Operations Björn Schaub, Head Exchange Operations Pages 2 Date 24.08.2018 Information Content of this message: - New trading segment for ams AG, Temenos AG, Bâloise Holding AG and ARYZTA AG as of 24 September 2018 - New stop trading range for VAT Group AG, BB Biotech AG, DKSH Holding AG and Galenica AG as of 24 September 2018 On 6 July 2018, SIX Swiss Exchange published SIX Swiss Exchange message No. 30/2018 to announce the impending index adjustments decided by the Index Commission on the occasion of the regular index review. This message provides the most important information on the impact of these index adjustments. Changes to the trading segments With the index adjustment, ams AG and Temenos AG will be included in the SLI® Index and Bâloise Holding AG and ARYZTA AG will be excluded from the SLI® Index. Therefore, these securities will also move to different trading segments effective from 24 September 2018. ams AG and Temenos AG will move from the Mid-/Small-Cap Shares segment (market code XSWX) to the Blue Chips Shares segment (market code XVTX). At the same time, Bâloise Holding AG and ARYZTA AG will move from the Blue Chip Shares segment (market code XVTX) to the Mid-/Small-Cap Shares segment (market code XSWX). Due to change of trading segment, all outstanding orders for these securities will be deleted from the order books: On 21 September 2018 (the last trading day before the segment change), after close of trading at 17:30 CEST, all “good-till-date” orders for these securities will be deleted from the order books by SIX Swiss Exchange. -

The FCO Cockpit Global Bubble Status Report

The FCO Cockpit Global Bubble Status Report Didier Sornette & Ke Wu Chair of Entrepreneurial Risks Department of Management, Technology and Economics ETH Zurich Scheuchzerstrasse 7 8092 Zurich, Switzerland October 1st, 2017 The FCO Cockpit - Global Bubble Status Report 1 October 2017 Announcement Dear supporters and followers of FCO, We are sorry about the delay of the report this month. We are experiencing a few technical issues and personnel changes. Therefore, we only publish the part on single stocks this month. At the same time, we are working on a new improved version of our methodology and reports, which will be published next month. Thank you very much for your long-term understanding and supports. Should you have any questions, please do not hesitate to contact us. Best regards, Chair of Entrepreneurial Risks The FCO Cockpit - Global Bubble Status Report 1 October 2017 Contents About Methodology Single Stocks Sectors Final Remarks The FCO Cockpit - Global Bubble Status Report 1 October 2017 About The Financial Crisis Observatory (FCO) monthly report discusses the historical evolution of bubbles in and between different asset classes and geographies. It is the result of an extensive analysis done on the historical time series of 431 systemic assets and 847 single stocks. The systemic assets are bond, equity and commodity indices and a selection of currency pairs. The single stocks are mainly US and European equities. The data is from Thomson Reuters. In the first part of this report, we present the state of the world, based on the analysis of the systemic assets. In the second part, we zoom in on the bubble behavior of single stocks and discuss some specific cases. -

Equiduct Market Notice

Equiduct Market Notice Date: 28/06/2019 Market Notice Number: 061/2019 Suspension of Swiss instruments On Thursday 27th June 2019 the Swiss Federal Department of Finance (FDF) announced that they will be activating protective measures prohibiting trading venues in the EU from trading Swiss registered shares from 1st July 2019. On Tuesday 25th June 2019, Market Notice 058/2019 announced that Equiduct would suspend trading in all Swiss equities if the Swiss Federal Department of Finance implemented its protective measures. As such, Equiduct will suspend all Swiss instruments from the start of trading on 1st July 2019. The full list of affected instruments are listed below. Please contact the Equiduct Market Operations Team ([email protected]) if you have any questions. Full list of affected instruments ISIN Instrument ID Instrument Name Currency Trading Market CH0012221716 ABBNz ABB LTD CHF XSWX CH0012221716 ABBs ABB SEK XSTO CH0012138605 ADENz ADECCO SA CHF XSWX CH0043238366 ARYNz ARYZTA AG CHF XSWX CH0102484968 BAERz JULIUS BAER GRUPPE AG CHF XSWX CH0012410517 BALNz BALOISE-HLDGS CHF XSWX CH0009002962 BARNz BARRY CALLEBAUT AG CHF XSWX CH0038389992 BBZAd BB BIOTECH EUR XETR CH0038389992 BIONz BB BIOTECH CHF XSWX CH0011432447 BSLNz BASILEA PHARMACEUTICA AG CHF XSWX CH0002432174 BUCNz BUCHER INDUSTRIES CHF XSWX CH0210483332 CFRz COMPAGNIE FINANCIERE RICHEMONT CHF XSWX CH0012142631 CLNz CLARIANT CHF XSWX CH0225173167 CMBNz CEMBRA MONEY BANK AG CHF XSWX CH0012138530 CSGNz CREDIT SUISSE GROUP AG CHF XSWX CH0126673539 DKSHz DKSH HOLDING CHF XSWX Equiduct is the electronic trading segment of the Regulated Market Börse Berlin. Equiduct Systems provides Market Notices covering operational information including data, functional and procedural changes to the trading system. -

Notice N19 2019

UBS MTF Market Notice Swiss Market Removal 28 June 2019 Dear Member, Following the announcement of the Swiss Federal Department of Finance on June 24 (FDF prepared to activate measure to protect Swiss stock exchange infrastructure), and further to our notice of the same date, UBS MTF will remove all instruments issued by companies with registered offices in Switzerland which are listed on Swiss trading venues. This update will take effect from 1 July. Our daily Stock Universe file, published on our website at https://www.ubs.com/global/en/investment- bank/ib/multilateral-trading-facility/reference-data.html and by SFTP, will reflect the removal of these instruments as of this date. Instruments not subject to the Swiss measure are unaffected; a list of affected instruments is attached to this notice. If you have any queries regarding this notice please contact the UBS MTF Supervisors at +44 207 568 2052 or [email protected]. UBS MTF Management Notice N19 2019 UBS MTF Notices and documentation are available at https://www.ubs.com/mtf. If you have any queries regarding this notice, or comments on the above, please contact the UBS MTF Supervisors at +44 20 7568 2052 or [email protected]. UBS MTF is operated by UBS AGLB which is authorised by the Prudential Regulation Authority and regulated by the UK Financial Conduct Authority and Prudential Regulation Authority. UBS AG is a public company incorporated with limited liability in Switzerland domiciled in the Canton of Basel-City and the Canton of Zurich respectively registered at the Commercial Registry offices in those Cantons with Identification No: CHE-101.329.561 as from 18 December 2013 (and prior to 18 December 2013 with Identification No: CH-270.3.004.646-4) and having respective head offices at Aeschenvorstadt 1, 4051 Basel and Bahnhofstrasse 45, 8001 Zurich, Switzerland and is authorised and regulated by the Financial Market Supervisory Authority in Switzerland. -

Unterschleißheim, 27

Program BAADER HELVEA SWISS EQUITIES CONFERENCE 10 – 11 January 2019 Grand Resort Bad Ragaz, Switzerland CONTACTS @ BAADER HELVEA Lukas Burkart, Head of Equity Sales T +49 89 5150 1858, [email protected] Andreas von Arx, Head of Equity Research Switzerland T +41 43 388 9257, [email protected] Reto Amstalden, Equity Research T +41 43 388 9261, [email protected] www.baaderbank.com Enable Change in Banking. Baader Helvea Swiss Equities Conference 10 – 11 January 2019 PRESENTING COMPANIES 67 companies have agreed to participate in the Swiss Equities Conference 2019: Bloomberg Reuters Company name ticker ticker Sector Addex Therapeutics ADXN SE ADXN.S Pharma & Healthcare Adecco Group ADEN SE ADEN.S Business Services & Logistics ARBONIA ARBN SE ARBNO.S Construction Ascom ASCN SE ASCN.S Technology Baloise BALN SE BALN.S Banks & Insurance Basilea (one-on-one only) BSLN SE BSLN.S Pharma & Healthcare BB Biotech (one-on-one only) BION SW BION.S Pharma & Healthcare BKW AG BKW SE BKWB.S Utilities Bossard BOSN SE BOS.S Industrials Bucher Industries BUCN SE BUCN.S Industrials Cembra Money Bank CMBN SE CMBN.S Banks & Insurance Clariant CLN SE CLN.S Chemicals COLTENE CLTN SE CLTN.S Pharma & Healthcare Compagnie Financière Tradition (one-on-one only) CFT SE CFT.S Banks & Insurance Conzzeta CON SE CONC.S Industrials Dätwyler Holding Inc. DAE SE DAE.S Technology dormakaba DOKA SE DOKA.S Industrials Dufry DUFN SE DUFN.S Consumer & Retail EFG International EFGN SE EFGN.S Banks & Insurance Evolva (one-on-one only) EVE SE EVE.S Chemicals Galenica -

Stoxx® Europe Christian Index

STOXX® EUROPE CHRISTIAN INDEX Components1 Company Supersector Country Weight (%) NESTLE Food & Beverage CH 2.99 HSBC Banks GB 2.39 TOTAL Oil & Gas FR 1.77 ROYAL DUTCH SHELL A Oil & Gas GB 1.69 BP Oil & Gas GB 1.56 SIEMENS Industrial Goods & Services DE 1.34 BCO SANTANDER Banks ES 1.29 SAP Technology DE 1.28 ALLIANZ Insurance DE 1.24 BASF Chemicals DE 1.14 BNP PARIBAS Banks FR 1.06 DIAGEO Food & Beverage GB 1.01 DAIMLER Automobiles & Parts DE 1.01 ANHEUSER-BUSCH INBEV Food & Beverage BE 1.00 UNILEVER NV Personal & Household Goods NL 1.00 ASML HLDG Technology NL 0.99 LVMH MOET HENNESSY Personal & Household Goods FR 0.98 VODAFONE GRP Telecommunications GB 0.90 UBS GROUP Banks CH 0.85 PRUDENTIAL Insurance GB 0.82 ING GRP Banks NL 0.82 LLOYDS BANKING GRP Banks GB 0.81 UNILEVER PLC Personal & Household Goods GB 0.78 GLENCORE PLC Basic Resources GB 0.78 RIO TINTO Basic Resources GB 0.73 AXA Insurance FR 0.70 VINCI Construction & Materials FR 0.68 INTESA SANPAOLO Banks IT 0.66 BCO BILBAO VIZCAYA ARGENTARIA Banks ES 0.65 L'OREAL Personal & Household Goods FR 0.65 AIR LIQUIDE Chemicals FR 0.64 DEUTSCHE TELEKOM Telecommunications DE 0.64 DANONE Food & Beverage FR 0.63 ZURICH INSURANCE GROUP Insurance CH 0.60 ABB Industrial Goods & Services CH 0.59 SCHNEIDER ELECTRIC Industrial Goods & Services FR 0.59 ENEL Utilities IT 0.56 BARCLAYS Banks GB 0.56 CIE FINANCIERE RICHEMONT Personal & Household Goods CH 0.56 TELEFONICA Telecommunications ES 0.55 GRP SOCIETE GENERALE Banks FR 0.54 UNICREDIT Banks IT 0.53 CREDIT SUISSE GRP Banks CH 0.53 ENI Oil & Gas -

Instrument Change

Market Notice 28 June 2019 Instrument Change Referential Update 2019-2096 - Instrument changes effective 01 July 2019 Please be aware of the instrument changes below effective 01 July 2019: Name MIC ISIN Symbol CCY Segment Tick Table Action Region ABB LTD-REG XSTO CH0012221716 ABBs SEK SE 2000_9000 DELETE ALL ARYZTA AG XDUB CH0043238366 YZAi EUR IE 600_2000 DELETE ALL AUTONEUM XSWX CH0127480363 AUTNz CHF CH 600_2000 DELETE ALL HOLDING AG BARRY CALLEBAUT AG- XSWX CH0009002962 BARNz CHF CH 600_2000 DELETE ALL REG BASILEA PHARMACEUTICA- XSWX CH0011432447 BSLNz CHF CH 600_2000 DELETE ALL REG SWISS PRIME SITE- XSWX CH0008038389 SPSNz CHF CH 600_2000 DELETE ALL REG EFG INTERNATIONAL XSWX CH0022268228 EFGNz CHF CH 80_600 DELETE ALL AG EMS-CHEMIE XSWX CH0016440353 EMSNz CHF CH 600_2000 DELETE ALL HOLDING AG-REG GAM HOLDING AG XSWX CH0102659627 GAMz CHF CH 600_2000 DELETE ALL HIGHLIGHT COMMUNICATIONS XETR CH0006539198 HLGd EUR DE _10 DELETE ALL -BR KUDELSKI SA-BR XSWX CH0012268360 KUDz CHF CH 80_600 DELETE ALL GB00BYSRJ69 LONMIN PLC XLON LMIl GBX GB 80_600 DELETE ALL 8 PERROT DUVAL XSWX CH0252620700 PEDUz CHF CH _10 DELETE ALL HOLDING-BR NEW OC OERLIKON XSWX CH0000816824 OERLz CHF CH 600_2000 DELETE ALL CORP AG-REG PANALPINA WELTTRANSPORT - XSWX CH0002168083 PWTNz CHF CH 600_2000 DELETE ALL REG UNILEVER NV-CVA XAMS NL0000009355 UNAa EUR NL 9000_ DELETE ALL BB BIOTECH AG- XETR CH0038389992 BBZAd EUR DE 80_600 DELETE ALL REG FISCHER (GEORG)- XSWX CH0001752309 FINz CHF CH 600_2000 DELETE ALL REG HELVETIA XSWX CH0466642201 HELNz CHF CH 600_2000 DELETE -

Subpart 2.6 Contract Specifications for Options Contracts and Low Exercise Price Options on Stocks

Contract Specifications for Futures Contracts and Eurex14e Options Contracts at Eurex Deutschland As of 11.02.2019 Page 1 ********************************************************************************** AMENDMENTS ARE MARKED AS FOLLOWS: INSERTIONS ARE UNDERLINED DELETIONS ARE CROSSED OUT ********************************************************************************** Subpart 2.6 Contract Specifications for Options Contracts and Low Exercise Price Options on Stocks […] 2.6.11 Price Gradations The price of a stock option or LEPO will generally be quoted with three or four decimal place. The smallest price change (Tick) shall be EUR 0.0005, EUR 0.001, EUR 0.01 or CHF 0.01 or GBX* 0.5, GBX 0.25 or USD 0.01. For stock options with group ID NL11, FR11, BE11, DE11, CH11, NL12, FR12, BE12, DE12, CH12, AT12 and NL13, FR13, BE13, DE13, CH13 the tick size will increase to EUR 0.05 for contracts with a premium above a predefined threshold stipulated in Annex B (Premium Threshold). The Management Boards of the Eurex Exchanges shall determine the relevant decimal place and the smallest price change (Tick) and shall notify all Exchange participation of any such decision. […] Annex B in relation to Subsection 2.6 of the Contract Specifications: […] The table referenced below stipulates further information for products with a premium threshold. The information regarding the below mentioned products is supplementary to the information stipulated in the table above. Options on shares of Product-ID Group ID Minimum price Premium Minimum price change -

Instrument ID ISIN Code Description Market ID Yzai CH0043238366 ARYZTA AG XDUB Notd CH0012005267 NOVARTIS AG-REG XETR O5hd CH002

Instrument ID ISIN Code Description Market ID YZAi CH0043238366 ARYZTA AG XDUB NOTd CH0012005267 NOVARTIS AG-REG XETR O5Hd CH0022237009 OPENLIMIT HOLDING AG XETR HLGd CH0006539198 HIGHLIGHT COMMUNICATIONS-BR XETR NESRd CH0038863350 NESTLE SA-REG XETR BBZAd CH0038389992 BB BIOTECH AG-REG XETR CCHl CH0198251305 COCA-COLA HBC AG-DI XLON TVRBp CH0008175645 TELEVERBIER XPAR AGTAp CH0008853209 AGTA RECORD LTD XPAR GNROp CH0308403085 GENEURO SA XPAR LHNp CH0012214059 LAFARGEHOLCIM LTD-REG XPAR CCCs CH0136071542 CAVOTEC SA XSTO ORIs CH0256424794 ORIFLAME HOLDING AG XSTO FOIBs CH0242214887 FENIX OUTDOOR INTERNATIONAL XSTO ABBs CH0012221716 ABB LTD-REG XSTO MIKNz CH0003390066 MIKRON HOLDING AG-REG NEW XSWX PSPNz CH0018294154 PSP SWISS PROPERTY AG-REG XSWX SFZNz CH0014284498 SIEGFRIED HOLDING AG-REG XSWX SWTQz CH0010754924 SCHWEITER TECHNOLOGIES AG-BR XSWX GRKPz CH0001340204 GRAUBUENDNER KANTONALBANK-PC XSWX GMIz CH0012949464 GROUPE MINOTERIES SA-REG XSWX BPDGz CH0473243506 BANQUE PROFIL DE GESTION-BR XSWX UHRNz CH0012255144 SWATCH GROUP AG/THE-REG XSWX TIBNz CH0214706357 BERGBAHNEN ENGELB. TRUEB-REG XSWX TAMNz CH0011178255 TAMEDIA AG-REG XSWX ZWMz CH0002661731 ZWAHLEN & MAYR SA-BR XSWX ZUGNz CH0148052126 ZUG ESTATES HOLDING AG-B SHR XSWX ZUBNz CH0312309682 ZUEBLIN IMMOBILIEN HOLDI-REG XSWX ALPHz CH0034389707 ALPIQ HOLDING AG-REG XSWX AEVSz CH0478634105 AEVIS VICTORIA SA XSWX HRENz CH0025607331 ROMANDE ENERGIE HOLDING-REG XSWX HLEEz CH0003583256 HIGHLIGHT EVENT AND ENTERTAI XSWX HBMNz CH0012627250 HBM HEALTHCARE IVST-A XSWX ZGz CH0001308904 ZUGER