Full Year Results 2008-09

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

IATA CLEARING HOUSE PAGE 1 of 21 2021-09-08 14:22 EST Member List Report

IATA CLEARING HOUSE PAGE 1 OF 21 2021-09-08 14:22 EST Member List Report AGREEMENT : Standard PERIOD: P01 September 2021 MEMBER CODE MEMBER NAME ZONE STATUS CATEGORY XB-B72 "INTERAVIA" LIMITED LIABILITY COMPANY B Live Associate Member FV-195 "ROSSIYA AIRLINES" JSC D Live IATA Airline 2I-681 21 AIR LLC C Live ACH XD-A39 617436 BC LTD DBA FREIGHTLINK EXPRESS C Live ACH 4O-837 ABC AEROLINEAS S.A. DE C.V. B Suspended Non-IATA Airline M3-549 ABSA - AEROLINHAS BRASILEIRAS S.A. C Live ACH XB-B11 ACCELYA AMERICA B Live Associate Member XB-B81 ACCELYA FRANCE S.A.S D Live Associate Member XB-B05 ACCELYA MIDDLE EAST FZE B Live Associate Member XB-B40 ACCELYA SOLUTIONS AMERICAS INC B Live Associate Member XB-B52 ACCELYA SOLUTIONS INDIA LTD. D Live Associate Member XB-B28 ACCELYA SOLUTIONS UK LIMITED A Live Associate Member XB-B70 ACCELYA UK LIMITED A Live Associate Member XB-B86 ACCELYA WORLD, S.L.U D Live Associate Member 9B-450 ACCESRAIL AND PARTNER RAILWAYS D Live Associate Member XB-280 ACCOUNTING CENTRE OF CHINA AVIATION B Live Associate Member XB-M30 ACNA D Live Associate Member XB-B31 ADB SAFEGATE AIRPORT SYSTEMS UK LTD. A Live Associate Member JP-165 ADRIA AIRWAYS D.O.O. D Suspended Non-IATA Airline A3-390 AEGEAN AIRLINES S.A. D Live IATA Airline KH-687 AEKO KULA LLC C Live ACH EI-053 AER LINGUS LIMITED B Live IATA Airline XB-B74 AERCAP HOLDINGS NV B Live Associate Member 7T-144 AERO EXPRESS DEL ECUADOR - TRANS AM B Live Non-IATA Airline XB-B13 AERO INDUSTRIAL SALES COMPANY B Live Associate Member P5-845 AERO REPUBLICA S.A. -

Appeal Brought on 25 November 2019 by Confédération

23.3.2020 EN Official Journal of the European Union C 95/13 Request for a preliminary ruling from the Rechtbank Amsterdam (Netherlands) lodged on 6 November 2019 — Stichting Cartel Compensation, Equilib Netherlands BV v Koninklijke Luchtvaart Maatschappij NV and Others (Case C-819/19) (2020/C 95/12) Language of the case: Dutch Referring court Rechtbank Amsterdam Parties to the main proceedings Applicants: Stichting Cartel Compensation, Equilib Netherlands BV Defendants: Koninklijke Luchtvaart Maatschappij NV, Martinair Holland NV, Deutsche Lufthansa AG, Lufthansa Cargo AG, British Airways plc, Société Air France SA, Singapore Airlines Ltd, Singapore Airlines Cargo Pte Ltd, Koninklijke Luchtvaart Maatschappij NV, Martinair Holland NV, Société Air France SA, Singapore Airlines Cargo Pte Ltd, Singapore Airlines Ltd, Lufthansa Cargo AG, Deutsche Lufthansa AG, Swiss International Air Lines AG, British Airways plc, Air Canada, Cathay Pacific Airways Ltd, SAS AB, Scandinavian Airlines System Denmark-Norway-Sweden, SAS Cargo Group A/S, Koninklijke Luchtvaart Maatschappij NV, Martinair Holland NV, Société Air France SA, Lufthansa Cargo AG, Deutsche Lufthansa AG, British Airways plc Question referred In a dispute between injured parties (in the present case shippers, recipients of air cargo services) and air carriers, do the national courts have the power — either because of the direct effect of Article 101 TFEU, or at least of Article 53 EEA, or on the basis of (the direct effect of) Article 6 of Regulation 1/2003 (1) — to fully apply Article 101 -

Air France KLM Martinair Cargo and Bolloré Logistics Team up to Launch the First Low-Carbon Airfreight Route Between France and the United States

Press release Puteaux, 21 January 2021 Air France KLM Martinair Cargo and Bolloré Logistics team up to launch the first low-carbon airfreight route between France and the United States Bolloré Logistics has joined the Sustainable Aviation Fuel (SAF) programme of Air France KLM Martinair Cargo (AFKLMP Cargo) for its 2021 shipments between Paris Charles de Gaulle and New York John F. Kennedy airports. This first of its kind collaboration illustrates the ambition of these two historical partners to tackle the environmental challenge of airfreight transportation. Christophe Boucher, EVP Air France Cargo says: “The Cargo SAF Programme enables shippers and forwarders to power a percentage of their flights with SAF. Customers determine their own level of engagement and we ensure that their entire investment is used for sourcing SAF. I’m delighted to see the speed at which Air France KLM Martinair Cargo and Bolloré Logistics have come to an agreement on the use of our SAF programme, launched a few weeks ago. I’m proud that together we are trendsetters in a field that will grow in our companies and in society.” This innovative aviation fuel will cut CO₂ emissions by at least 50% on airfreight shipped by Bolloré Logistics on this symbolic trade lane. Investing in this strategic route represents a new step towards achieving greater sustainability in the future for both Bolloré Logistics and AFKLMP Cargo. “Reducing carbon emissions is a major challenge in the airfreight transportation industry and Bolloré Logistics is committed to addressing this with innovative solutions. In 2021, the company has committed itself to reducing scope 3 CO₂ emissions linked to the performance of its transport services by 30% by 2030. -

New Expanded Joint Venture

Press Release The Power of Choice for Cargo Customers as Air France-KLM, Delta and Virgin Atlantic launch trans-Atlantic Joint Venture AMSTERDAM/PARIS, ATLANTA and LONDON: February 3rd, 2020 – Air France-KLM Cargo, Delta Air Lines Cargo and Virgin Atlantic Cargo are promising cargo customers more connections, greater shipment routing flexibility, improved trucking options, aligned services and innovative digital solutions with the launch of their expanded trans-Atlantic Joint Venture (JV). The new partnership, which represents 23% of total trans-Atlantic cargo capacity or more than 600,000 tonnes annually, will enable the airlines to offer the best-ever customer experience, and a combined network of up to 341 peak daily trans-Atlantic services – a choice of 110 nonstop routes with onward connections to 238 cities in North America, 98 in Continental Europe and 16 in the U.K. More choice and convenience for customers Customers will be able to leverage an enhanced network built around the airlines’ hubs in Amsterdam, Atlanta, Boston, Detroit, London Heathrow, Los Angeles, Minneapolis, New York-JFK, Paris, Seattle and Salt Lake City. It creates convenient nonstop or one-stop connections to every corner of North America, Europe and the U.K., giving customers the added confidence of delivery schedules being met by a wide choice of options. The expanded JV enables greater co-operation between the airlines, focused on delivering world class customer service and reliability on both sides of the Atlantic achieved through co-located facilities, joint trucking options as well as seamless bookings and connected service recovery. The airlines already co-locate at warehouses in key U.S., U.K. -

Prof. Paul Stephen Dempsey

AIRLINE ALLIANCES by Paul Stephen Dempsey Director, Institute of Air & Space Law McGill University Copyright © 2008 by Paul Stephen Dempsey Before Alliances, there was Pan American World Airways . and Trans World Airlines. Before the mega- Alliances, there was interlining, facilitated by IATA Like dogs marking territory, airlines around the world are sniffing each other's tail fins looking for partners." Daniel Riordan “The hardest thing in working on an alliance is to coordinate the activities of people who have different instincts and a different language, and maybe worship slightly different travel gods, to get them to work together in a culture that allows them to respect each other’s habits and convictions, and yet work productively together in an environment in which you can’t specify everything in advance.” Michael E. Levine “Beware a pact with the devil.” Martin Shugrue Airline Motivations For Alliances • the desire to achieve greater economies of scale, scope, and density; • the desire to reduce costs by consolidating redundant operations; • the need to improve revenue by reducing the level of competition wherever possible as markets are liberalized; and • the desire to skirt around the nationality rules which prohibit multinational ownership and cabotage. Intercarrier Agreements · Ticketing-and-Baggage Agreements · Joint-Fare Agreements · Reciprocal Airport Agreements · Blocked Space Relationships · Computer Reservations Systems Joint Ventures · Joint Sales Offices and Telephone Centers · E-Commerce Joint Ventures · Frequent Flyer Program Alliances · Pooling Traffic & Revenue · Code-Sharing Code Sharing The term "code" refers to the identifier used in flight schedule, generally the 2-character IATA carrier designator code and flight number. Thus, XX123, flight 123 operated by the airline XX, might also be sold by airline YY as YY456 and by ZZ as ZZ9876. -

2017-05 Ag En.Pdf

COMBINED ORDINARY AND EXTRAORDINARY SHAREHOLDERS’ MEETING 2017 LEGAL OPENING A I R F R A NPARIS C E - KLM RESULTS* OF THE PRE-SHAREHOLDERS’ MEETING SURVEY OF INDIVIDUAL SHAREHOLDERS Ranking of the expected themes Market outlook and growth relays 69% Results targets 51% Dividend distribution policy 44% The new Trust Together strategic project 38% Financial strategy (investment, operational efficiency, etc.) 30% Changes in the shareholder structure and shareholder loyalty policy 29% Human resources policy and relations with the unions 28% * Survey of Air France-KLM individual shareholders realized electronically during April 2017 COMBINED ORDINARY AND EXTRAORDINARY 3 A I R F R A N C E - KLM SHAREHOLDERS’ MEETING 2017 SHAREHOLDERS’ MEETING AGENDA Legal Opening Corporate Governance 2016 Financial Review Strategy and Outlook Presentation of the Resolutions Statutory Auditors’ Reports Dialogue with Shareholders Vote on the Resolutions Conclusion COMBINED ORDINARY AND EXTRAORDINARY 4 A I R F R A N C E - KLM SHAREHOLDERS’ MEETING 2017 CORPORATE GOVERNANCE NICE A I R F R A N C E - KLM SHAREHOLDER STRUCTURE OF THE GROUP AT MARCH 31, 2017 French individual shareholders* Institutional 9.9% investors Employees (FCPE) 6.2% France: 13.8% United Kingdom: 6.8% 65.9% United States: 24.7% Germany: 1.5% 17.6% French State Netherlands: 1.1% Switzerland: 0.3% 0.4% Treasury stock * In registered form and/or holding more than 1,000 shares in bearer form. COMBINED ORDINARY AND EXTRAORDINARY 6 A I R F R A N C E - KLM SHAREHOLDERS’ MEETING 2017 COMPOSITION OF THE CURRENT BOARD OF DIRECTORS Jean-Marc Peter Maryse Isabelle Jean-Dominique Anne-Marie Jaap JANAILLAC HARTMAN AULAGNON* BOUILLOT* COMOLLI COUDERC* DE HOOP SCHEFFER* Louis Solenne Hans Isabelle Alexander François Antoine Patrick JOBARD LEPAGE N.J. -

Case No COMP/JV.19 - */*** KLM / ALITALIA

EN Case No COMP/JV.19 - */*** KLM / ALITALIA Only the English text is available and authentic. REGULATION (EEC) No 4064/89 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 11/08/1999 Also available in the CELEX database Document No 399J0019 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 11.08.1999 PUBLIC VERSION MERGER PROCEDURE ARTICLE 6(1)(b) DECISION In the published version of this decision, some information has been omitted pursuant to Article 17(2) of Council Regulation (EEC) No 4064/89 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a general description. to the notifying parties Dear Sirs, Subject: Case M/JV-19 KLM-Alitalia Notification of 29 June 1999 pursuant to Article 4 of Regulation N°4064/89 1. On 29 June 1999, the Commission received a notification of a proposed concentration pursuant to Article 4 of Council Regulation (EEC) No. 4064/891 as last amended by Regulation (EC) No. 1310/972 (the Merger Regulation) by which the undertakings Koninklijke Luchtvaart Maatschappij N.V. (KLM) and Alitalia Linee Aeree Italiane S.p.A. (Alitalia) will constitute a Joint Venture under the meaning of Article 3 (2) of the Merger Regulation. 2. In the course of the proceedings, the parties submitted undertakings designed to eliminate competition concerns identified by the Commission, in accordance with Article 6(2) of the Merger Regulation. After examination of the notification and in the light of these modifications, the Commission has concluded that the operation 1 OJ L 395, 30.12.1989, p.1; corrigendum OJ L 257, 21.9.1990, p.13 2 OJ L 180, 9.7.1997, p.1; corrigendum OJ L 40, 13.2.1998, p.17 Rue de la Loi 200, B-1049 Bruxelles/Wetstraat 200, B-1049 Brussel - Belgium Telephone: exchange 299.11.11. -

Airline Alliances

AIRLINE ALLIANCES by Paul Stephen Dempsey Director, Institute of Air & Space Law McGill University Copyright © 2011 by Paul Stephen Dempsey Open Skies • 1992 - the United States concluded the first second generation “open skies” agreement with the Netherlands. It allowed KLM and any other Dutch carrier to fly to any point in the United States, and allowed U.S. carriers to fly to any point in the Netherlands, a country about the size of West Virginia. The U.S. was ideologically wedded to open markets, so the imbalance in traffic rights was of no concern. Moreover, opening up the Netherlands would allow KLM to drain traffic from surrounding airline networks, which would eventually encourage the surrounding airlines to ask their governments to sign “open skies” bilateral with the United States. • 1993 - the U.S. conferred antitrust immunity on the Wings Alliance between Northwest Airlines and KLM. The encirclement policy began to corrode resistance to liberalization as the sixth freedom traffic drain began to grow; soon Lufthansa, then Air France, were asking their governments to sign liberal bilaterals. • 1996 - Germany fell, followed by the Czech Republic, Italy, Portugal, the Slovak Republic, Malta, Poland. • 2001- the United States had concluded bilateral open skies agreements with 52 nations and concluded its first multilateral open skies agreement with Brunei, Chile, New Zealand and Singapore. • 2002 – France fell. • 2007 - The U.S. and E.U. concluded a multilateral “open skies” traffic agreement that liberalized everything but foreign ownership and cabotage. • 2011 – cumulatively, the U.S. had signed “open skies” bilaterals with more than100 States. Multilateral and Bilateral Air Transport Agreements • Section 5 of the Transit Agreement, and Section 6 of the Transport Agreement, provide: “Each contracting State reserves the right to withhold or revoke a certificate or permit to an air transport enterprise of another State in any case where it is not satisfied that substantial ownership and effective control are vested in nationals of a contracting State . -

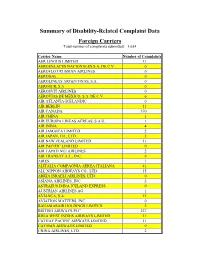

Summary of Disability-Related Complaint Data Foreign Carriers

Summary of Disability-Related Complaint Data Foreign Carriers Total number of complaints submitted: 1,654 Carrier Name Number of Complaints AER LINGUS LIMITED 11 AEROENLACES NACIONALES S.A. DE C.V. 0 AEROFLOT RUSSIAN AIRLINES 0 AEROGAL 0 AEROLINEAS ARGENTINAS, S.A. 0 AEROSUR, S.A. 0 AEROSVIT AIRLINES 0 AEROVIAS DE MEXICO, S.A. DE C.V. 6 AIR ATLANTA-ICELANDIC 0 AIR BERLIN 11 AIR CANADA 370 AIR CHINA 1 AIR EUROPA LINEAS AEREAS, S.A.U. 1 AIR INDIA 4 AIR JAMAICA LIMITED 2 AIR JAPAN, CO., LTD. 5 AIR NEW ZEALAND LIMITED 11 AIR PACIFIC LIMITED 0 AIR TAHITI NUI AIRLINES 2 AIR TRANSAT A.T., INC. 6 AIRES 1 ALITALIA COMPAGNIA AEREA ITALIANA 41 ALL NIPPON AIRWAYS CO., LTD. 15 ARKIA ISRAELI AIRLINES, LTD. 0 ASIANA AIRLINES, INC. 2 ASTRAEUS D/B/A ICELAND EXPRESS 0 AUSTRIAN AIRLINES AG 1 AVIANCA, S.A. 15 AVIATION MATTERS, INC. 0 BAHAMASAIR HOLDINGS LIMITED 2 BRITISH AIRWAYS PLC 237 BWIA WEST INDIES AIRWAYS LIMITED 11 CATHAY PACIFIC AIRWAYS LIMITED 11 CAYMAN AIRWAYS LIMITED 0 CHINA AIRLINES, LTD. 2 CHINA EASTERN AIRLINES CORPORATION 0 COMLUX AVIATION AG 0 COMLUX MALTA LTD. 0 COMPANIA MEXICANA DE AVIACION, S.A. 1 COMPANIA PANAMENA DE AVIACION, S.A. 10 CONDOR FLUGDIENST GMBH 2 CORSAIR 0 CZECH AIRLINES 1 DC AVIATION GMBH 0 DEUTSCHE LUFTHANSA AG 151 EGYPTAIR 1 EL AL ISRAEL AIRLINES LTD. 23 EMIRATES 24 ETHIOPIAN AIRLINES ENTERPRISE 0 ETIHAD AIRWAYS P.J.S.C. 6 EUROATLANTIC AIRWAYS TRANSPORTES AE 0 EVA AIRWAYS CORPORATION 6 FINNAIR OY D/B/A FINNAIR OYJ 1 FIRST AIR 0 GLOBAL JET LUXEMBOURG S.A. -

General. Note: in Addition to the Comments Which Were Received on the Specific Proposals, Some Commentors Made Comments Or Suggestions of a General Nature

General. Note: In addition to the comments which were received on the specific proposals, some commentors made comments or suggestions of a general nature. The responses to these are shown below. Item Comment Commentor Summary of Operations Reason for the Resulting change to Number Comment Committee Response NPA text Response 094 Transport Canada 108 CAA Hungary 114 CAA Iceland Commentors expressed 1 231 Air 2000 general agreement with the Noted -- -- 273 LFV Norway proposals 293 LFV Sweden 310 Brit. Aerospace A generalized complaint that Noted -- No change intended at the 2 the JAR uses 3 numbering moment systems 137 CAA UK Editorial comment Noted -- -- 136 CAA UK Changes to Subpart N should Noted FCL/OPS co-ordination group to -- take full account of JAR-FCL deal with this. 3 027 CAA Czech Several comments concerning Attended to -- -- Subpart K under ‘K’ 239 Martinair Maintenance Postholder to be Attended to -- -- a separate person under ‘C’ NPA-OPS-15 Comment/Response Document Page 1 Subpart A. Refer to NPA-OPS-12 JAR-OPS 1/3.001(a)(2) Item Comment Commentor Summary of Operations Reason for the Resulting change to Number Comment Committee Response NPA text Response 34 CAA Finland Parachuting should be an Agree It is intended to regulate for Additional para. (a)(2) to 1 19 Finnish Aeronautic exempted category parachuting under Parts 2 and 4 exempt parachutists 2 25 Heli Air Zagel Should be no limit on number Disagree Wide agreement that 6 is a 26 Agrarflug Helilift of pax reasonable limit provided that -- parachutists and firefighters are exempted 3 32 Skyjet AG Authority could approve more Disagree Ditto above -- than 6 pax 4 36 Transport Canada Exclude firefighters and all Agree Aerial Work to be regulated under Firefighters exempted crew of Aerial Work Parts 2 and 4 under new para. -

Air France-KLM Group for the Year Ended Activity AFR 33 December 31, 2012

Selected fi nancial information 2 Highlights of the 2012 fi nancial year AFR 4 4.6 Note on the methodology for the reporting Corporate governance AFR 5 of the environmental indicators 129 1.1 The Board of Directors 6 4.7 Environmental indicators 132 1.2 The CEO Committee 30 4.8 Statutory Auditor’s Attestation report on the social, environmental and corporate 1 1.3 The Group Executive Committee 30 citizenship information disclosed in the 2012 management report 136 4.9 Statutory Auditor’s Assurance report on a selection of environmental and social indicators of Air France-KLM group for the year ended Activity AFR 33 December 31, 2012. 137 2.1 Market and environment 34 2.2 Strategy 42 2 Activities Financial r eport 139 2.3 Passenger business 45 2.4 Cargo business 53 5.1 Investments and fi nancing 140 2.5 Maintenance business 57 5.2 Property, plant and equipment 143 2.6 Other businesses 62 5 5.3 Comments on the fi nancial statements 146 2.7 Fleet 64 5.4 Key fi nancial indicators 150 2.8 Highlights of the beginning Financial statements AFR of the 2013 fi nancial year 71 5.5 Consolidated fi nancial statements 156 5.6 Notes to the consolidated fi nancial statements 163 5.7 Statutory auditors’ report on the consolidated fi nancial statements 245 Risks and risk 5.8 Statutory fi nancial statements 247 5.9 Five-year results summary 259 management AFR 73 5.10 Statutory Auditor’s report 3.1 Risk management process 74 on the fi nancial statements 260 3 3.2 Risk factors and their management 75 5.11 Statutory Auditors’ special report on regulated agreements and commitments 261 3.3 Market risks and their management 83 3.4 Report of the Chairman of the Board of Directors on corporate governance, internal control and risk management for the 2012 fi nancial year 87 3.5 Statutory auditors’ report prepared in accordance Other information 265 with article L.225-235 of the French Commercial Code (Code de commerce) on the report prepared 6.1 History 266 by the Chairman of the Board of Directors of Air France-KLM S.A. -

Airline Codes.Indd

AIRLINE CODES AND AWB PREFIX PREFIX IATA code AIRLINE PREFIX IATA code AIRLINE 044 AR Aerolineas Argentinas 173 HA Hawaiian Air Cargo 139 AM Aero Mexico 096 IR Iran Air 439 ZI Aigle Azur 131 JL Japan Airlines 657 BT Air Baltic 745 TB JetairFly 745 AB Air Berlin 589 9W Jet Airways 580 RU Air Bridge Cargo 074 KL KLM 159 CW Air Cargo Global 180 KE Korean Airlines 014 AC Air Canada 229 KU Kuwait Airways 427 TX Air Caraibes 045 LA Lan Chili 999 CA Air China International 148 LN Libyan Airlines 745 UX Air Europe 020 LH Lufthansa Cargo 057 AF Air France 232 MH Malaysian Airline 167 QM Air Malawi 129 MO Martinair 643 KM Air Malta 429 VL Med View Airlines 239 MK Air Mauritius 805 4X Mercury Air Cargo 086 NZ Air New Zealand 716 MG MNG Airlines Cargo 115 JU Air Serbia 519 NAB Niger Air Cargo 135 VT Air Tahiti 933 KZ Nippon Cargo Airlines 649 TS Air Transat 329 DY Norwegian Cargo 574 4W Allied Air 910 WY Oman Air 001 AA American Airlines 214 PR Pakistan International 810 M6 Amerijet International 624 PC Pegasus Airlines 988 OZ Asiana Airlines 079 PR Philippine Airlines 369 5Y Atlas Global 157 QR Qatar Airways 134 AV Avianca - Aerovias 672 BI Royal Runei Airlines 417 E6 Bringer Air Cargo 512 RJ Royal Jordanian 125 BA British Airways 117 SK Scandinavian Airlines 489 W8 Cargojet Airways 774 FM Shanghai Airlines 172 CV Cargolux Airlines 728 U3 Sky Gates 700 5C CAL 501 7L Silk Way West Airlines 160 CX Cathay Pacific Airways 618 SQ Singapore Airline Cargo 297 CI China Airlines 603 LX Srilankan Airlines 112 CK China Cargo Airlines 242 4E Stabo Air 781 MU