Noble Media Newsletter Q3 2018

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

VAB Member Stations

2018 VAB Member Stations Call Letters Company City WABN-AM Appalachian Radio Group Bristol WACL-FM IHeart Media Inc. Harrisonburg WAEZ-FM Bristol Broadcasting Company Inc. Bristol WAFX-FM Saga Communications Chesapeake WAHU-TV Charlottesville Newsplex (Gray Television) Charlottesville WAKG-FM Piedmont Broadcasting Corporation Danville WAVA-FM Salem Communications Arlington WAVY-TV LIN Television Portsmouth WAXM-FM Valley Broadcasting & Communications Inc. Norton WAZR-FM IHeart Media Inc. Harrisonburg WBBC-FM Denbar Communications Inc. Blackstone WBNN-FM WKGM, Inc. Dillwyn WBOP-FM VOX Communications Group LLC Harrisonburg WBRA-TV Blue Ridge PBS Roanoke WBRG-AM/FM Tri-County Broadcasting Inc. Lynchburg WBRW-FM Cumulus Media Inc. Radford WBTJ-FM iHeart Media Richmond WBTK-AM Mount Rich Media, LLC Henrico WBTM-AM Piedmont Broadcasting Corporation Danville WCAV-TV Charlottesville Newsplex (Gray Television) Charlottesville WCDX-FM Urban 1 Inc. Richmond WCHV-AM Monticello Media Charlottesville WCNR-FM Charlottesville Radio Group (Saga Comm.) Charlottesville WCVA-AM Piedmont Communications Orange WCVE-FM Commonwealth Public Broadcasting Corp. Richmond WCVE-TV Commonwealth Public Broadcasting Corp. Richmond WCVW-TV Commonwealth Public Broadcasting Corp. Richmond WCYB-TV / CW4 Appalachian Broadcasting Corporation Bristol WCYK-FM Monticello Media Charlottesville WDBJ-TV WDBJ Television Inc. Roanoke WDIC-AM/FM Dickenson Country Broadcasting Corp. Clintwood WEHC-FM Emory & Henry College Emory WEMC-FM WMRA-FM Harrisonburg WEMT-TV Appalachian Broadcasting Corporation Bristol WEQP-FM Equip FM Lynchburg WESR-AM/FM Eastern Shore Radio Inc. Onley 1 WFAX-AM Newcomb Broadcasting Corporation Falls Church WFIR-AM Wheeler Broadcasting Roanoke WFLO-AM/FM Colonial Broadcasting Company Inc. Farmville WFLS-FM Alpha Media Fredericksburg WFNR-AM/FM Cumulus Media Inc. -

Voter Groups Differ on Tv, Sports Favs

www.spotsndots.com PDF/TXT newsletter Subscription: $325 per year Call toll free: 888-884-2630 This publication cannot be distributed beyond the office of its named subscriber. Send sales-related job listing The Daily News of TV Sales Friday, August 12, 2016 to: [email protected] Copyright 2016. VOTER GROUPS DIFFER ON TV, SPORTS FAVS CLINTON CAMP BETS ON RIO OLYMPICS ADVERTISER NEWS Political ideology aside, Republicans and Democrats Macy’s will close another 100 stores, about 15% share a lot of common ground in their entertainment of its roster, on top of the 40 closings it had announced choices, and they also have some very distinct differences, previously and CEO Terry Lundgren said “We operate in a according to new data from The NPD Group. According fast-changing world…this involves doing things differently to NPD’s BrandLink, the most popular movie genres, and making tough decisions.” Second quarter same-store music types and video games are favored equally by sales were down 2% which was actually an improvement both Republicans and Democrats. In addition, men over the first quarter’s 5.6% decline but was still Macy’s of both parties favor celebrity athletes, showing that sixth straight quarter of negative comps. The closed stores sports heroes transcend politics within the male gender. account for about $1 billion in annual sales……Kohl’s However, entertainment preferences same-store sales were also negative, of conservative vs. liberal-leaning down 1.8%, although margin improved women are notably different, with strong due to inventory-management initiatives opinions held by women who identify as and profit was up slightly. -

11.15.13 WQCW Press Release

NEWS RELEASE GRAY REACHES AGREEMENT TO PROVIDE SERVICES TO WQCW (CW) IN CHARLESTON/HUNTINGTON, W.V. Charleston/Huntington, WV – November 15, 2013. Gray Television, Inc. (“Gray”) (NYSE: GTN and GTN.A) announced today that it has agreed to enter into a shared services agreement with Excalibur Broadcasting, LLC (“Excalibur”) for WQCW(TV), Portsmouth, Ohio and WOCW-LP, Charleston, West Virginia (collectively, “WQCW-TV”). WQCW-TV serves as the CW affiliate for the Charleston/Huntington, West Virginia television market, where Gray owns and operates WSAZ-TV, the market’s NBC affiliate. Under this agreement, Gray has agreed to provide back-office services and limited programming to WQCW-TV. Earlier today, Excalibur reached an agreement with Lockwood Broadcast Group (“Lockwood”) to purchase all of the assets of WQCW-TV for $5.5 million. Gray and Excalibur will begin the shared services agreement upon Excalibur’s purchase of WQCW-TV. Excalibur’s President and owner, Don Ray, is a resident of Huntington, West Virginia, and the former long-time General Manager of WSAZ-TV. He said, “Acquiring the Tri-State’s CW while simultaneously leveraging the resources of WSAZ for WQCW’s benefit presents an incredible opportunity to provide better service for area viewers and local businesses.” Kevin Latek, Gray’s Senior Vice President for Business Affairs, observed, “Gray is excited to work with Lockwood and Excalibur in this important market. We look forward to building upon the talent and resources of both WSAZ and WQCW to better serve the greater Charleston and Huntington region.” The parties expect the transactions to close following receipt of Federal Communications Commission consent and satisfaction of other closing conditions in the first quarter of 2014. -

Case 20-11719-CSS Doc 103 Filed 10/19/20 Page 1 of 126 Case 20-11719-CSS Doc 103 Filed 10/19/20 Page 2 of 126

Case 20-11719-CSS Doc 103 Filed 10/19/20 Page 1 of 126 Case 20-11719-CSS Doc 103 Filed 10/19/20 Page 2 of 126 EXHIBIT A Case 20-11719-CSS Doc 103 Filed 10/19/20 Page 3 of 126 Exhibit A Core Parties Service List Served as set forth below Description Name Address Email Method of Service Counsel to the Wilmington Trust, NA Arnold & Porter Kaye Scholer LLP 250 West 55th Street [email protected] Email New York, NY 10019 [email protected] First Class Mail [email protected] Notice of Appearance and Request for Notices ‐ Counsel to Ad Hoc Ashby & Geddes, P.A. Attn: William P. Bowden [email protected] Email Committee of First Lien Lenders 500 Delaware Ave, 8th Fl P.O. Box 1150 Wilmington, DE 19899‐1150 Notice of Appearance and Request for Notices Ballard Spahr LLP Attn: Matthew G. Summers [email protected] Email Counsel to Universal City Development Partners Ltd. and Universal Studios 919 N Market St, 11th Fl Licensing LLC Wilmington, DE 19801 Counsel to the Financial Advisors BCF Business Law Attn: Claude Paquet, Gary Rivard [email protected] Email 1100 René‐Lévesque Blvd W, 25th Fl, Ste 2500 [email protected] First Class Mail Montréal, QC H3B 5C9 Canada Governmental Authority Bernard, Roy & Associés Attn: Pierre‐Luc Beauchesne pierre‐[email protected] Email Bureau 8.00 [email protected] First Class Mail 1, rue Notre‐Dame Est Montréal, QC H2Y 1B6 Canada Notice of Appearance and Request for Notices Buchalter, PC Attn: Shawn M. -

Download Competitive Impact Statement

Case 1:18-cv-02951 Document 3 Filed 12/14/18 Page 1 of 27 UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA UNITED STATES OF AMERICA 450 Fifth Street NW Washington, DC 20530 Plaintiff, v. GRAY TELEVISION, INC. Case No. ___________________ 4370 Peachtree Road NE Atlanta, Georgia 30319; and RAYCOM MEDIA, INC. RSA Tower 20th Floor 201 Monroe Street Montgomery, Alabama 36104 Defendants. COMPETITIVE IMPACT STATEMENT Plaintiff United States of America (“United States”), pursuant to Section 2(b) of the Antitrust Procedures and Penalties Act (“APPA” or “Tunney Act”), 15 U.S.C. § 16(b)-(h), files this Competitive Impact Statement relating to the proposed Final Judgment submitted for entry in this civil antitrust proceeding. I. NATURE AND PURPOSE OF THE PROCEEDING On June 23, 2018, Defendant Gray Television, Inc. (“Gray”) and Raycom Media, Inc. (“Raycom,” and together with Gray, “Defendants”) entered into an Agreement and Plan of Merger (the “Merger Agreement”) pursuant to which Gray proposes to acquire Raycom for approximately $3.6 billion. The United States filed a civil antitrust Complaint on December 14, 2018, seeking to enjoin the proposed merger. The Complaint alleges that the proposed merger Case 1:18-cv-02951 Document 3 Filed 12/14/18 Page 2 of 27 likely would substantially lessen competition in violation of Section 7 of the Clayton Act, 15 U.S.C. § 18, in nine local geographic markets, in (1) the licensing of the television programming of NBC, CBS, ABC, and FOX (“Big 4”) affiliate stations to cable, satellite, and fiber optic television providers (referred to collectively as multichannel video programming distributors, or “MVPDs”) for retransmission to their subscribers (known as “retransmission consent”), and (2) the sale of broadcast television spot advertising. -

Case 16-52371 Doc 181 Filed 10/07/19 Entered 10/07/19 20:29:41 Desc Main Document Page 1 of 18

Case 16-52371 Doc 181 Filed 10/07/19 Entered 10/07/19 20:29:41 Desc Main Document Page 1 of 18 IN THE UNITED STATES BANKRUPTCY COURT MIDDLE DISTRICT OF GEORGIA MACON DIVISION In Re: : : RADIO PERRY, INC., : Case No. 16-52371-AEC : Chapter 11 Debtor. : : : MOTION FOR AN ORDER: (A) APPROVING SALE OF SUBSTANTIALLY ALL OF THE DEBTOR’S ASSETS, FREE AND CLEAR OF ALL LIENS, CLAIMS, INTERESTS, AND ENCUMBRANCES; (B) AUTHORIZING THE SALE, ASSUMPTION, AND ASSIGNMENT OF CERTAIN EXECUTORY CONTRACTS AND UNEXPIRED LEASES IN CONNECTION WITH SUCH SALE; (C) MAKING A DETERMINATION OF CURE AMOUNTS WITH RESPECT TO EXECUTORY CONTRACTS AND UNEXPIRED LEASES IN CONNECTION WITH SUCH SALE; AND (D) GRANTING RELATED RELIEF The above-captioned debtor and debtor-in-possession (the “Debtor ”, the “Company ” or the “Seller ”), by and through its undersigned counsel, hereby moves this Court for entry of an order, pursuant to Sections 105(a), 363, and 365 of title the Bankruptcy Code, and Rules 2002, 6004, and 6006 of the Federal Rules of Bankruptcy Procedure (the “Bankruptcy Rules ”): (a) approving the sale (the “Sale ”) of substantially all of the Debtor’s assets, free and clear of all liens, claims, interests, and encumbrances to Marquee Broadcasting Georgia, Inc. (the “Buyer ” or “Marquee ”); (b) approving the sale, and the assumption and assignment of certain executory contracts and unexpired leases (each an “Assumed Executory Contract ” and, collectively, the “Assumed Executory Contracts ”) in connection with such sale; (c) making a determination of cure amounts with respect to each of the Debtor’s Assumed Executory Contracts; and (d) granting related relief (the “Motion ”). -

Media Sector Review July 2017

MEDIA SECTOR REVIEW Dog Days Of Summer Already? INSIDE THIS ISSUE It seems that investors in media stocks are already affected by the “dog days of Outlook: Traditional Media 2 summer.” Media stocks have drifted after a strong first quarter performance. (See TV 3 details later in the report). We believe that the performance relates to concern over the Radio 4 general macro-economic environment, including slowing auto sales. In addition, there has been a fairly lackluster M&A environment, aside from some announced, high profile Publishing 5 mergers including Entercom and CBS Radio and Sinclair and Tribune Media. We believe Industry M&A Activity 6 that there is a heightened M&A environment emerging and will build in the second half 2017. In our view, the prospect of the FCC lifting in-market rules, which will allow a Outlook: Internet and Digital Media 7 TV broadcaster to own two of the big four Networks, and a lift in the ownership caps, Digital Media 9 both will be a catalyst for heightened M&A activity. Furthermore, in radio, there will be Advertising Tech. 10 activity related to the stations that Entercom plans to sell to complete the CBS Radio merger. We believe that this emerging M&A environment will create winners and losers Marketing Tech. 11 and, as such, it will become a stock pickers market. Social Media 12 Industry M&A Activity 13 NOBLE Overview 15 STOCK MARKET PERFORMANCE: TRADITIONAL MEDIA 35% 25% 15% 5% Noble TV S&P 500 Index Noble Radio -5% Noble Publishing -15% Jul-31-2016 Apr-30-2017 Jan-31-2017 Feb-28-2017 Jun-30-2016 Jun-30-2017 Mar-31-2017 Oct-31-2016 Sep-30-2016 Aug-31-2016 Dec-31-2016 Nov-30-2016 May-31-2017 NOBLE International Investments, Inc., dba NOBLE Capital Markets is a FINRA registered broker/dealer. -

Marquee WSWG Petition

Before the FEDERAL COMMUNICATIONS COMMISSION Washington, D.C. 20554 In the Matter of ) ) MB Docket No.______ Amendment of Section 73.622, ) RM-_________ Digital Television Table of Allotments, ) (Valdosta, Georgia and Moultrie, Georgia) ) ) To: Office of the Secretary, Federal Communications Commission Attn: Chief, Media Bureau PETITION FOR RULEMAKING Marquee Broadcasting Georgia, Inc (“Marquee”), licensee of television station WSWG(TV) Valdosta, Georgia (Facility ID Number 28155, Channel 31) (“WSWG” or the “Station”), hereby submits this Petition for Rulemaking to modify the DTV Table of Allotments (the “DTV Table”)1 contained in Section 73.622(i) of the Commission’s rules.2 Specifically, Marquee requests that the Commission: amend the DTV Table to delete Channel 43 at Valdosta, Georgia, and add Channel 31 at Moultrie, Georgia; and (3) modify WSWG’s license to specify Moultrie as its community of license.3 1 It should be noted that Gray Television Licensee, LLC (“Gray”), the former licensee of WSWG(TV), submitted a similar Petition in 2012, as amended in 2013, but no action was taken on that filing. To the extent necessary, Marquee requests dismissal of that earlier Petition. 2 See 47 C.F.R. §§ 1.401, 73.622(i). 3 WSWG(TV)’s license was modified as part of the post-auction repack to specify operation on Channel 31 (LMS File No. 0000063722), although the DTV Table has not yet been updated to reflect this change. See Expanding the Economic and Innovation Opportunities of Spectrum Through Incentive Auctions, Report and Order, 29 FCC Rcd 6567, 6789 (2014), aff’d Nat’l Assn. -

NEWS RELEASE GRAY ANNOUNCES NEW ACQUISITIONS and DIVESTITURES Atlanta, GA – October 1, 2015. . . Gray Television, Inc. (“Gra

NEWS RELEASE GRAY ANNOUNCES NEW ACQUISITIONS AND DIVESTITURES Atlanta, GA – October 1, 2015. Gray Television, Inc. (“Gray” or “we” or “our”) (NYSE: GTN and GTN.A) announced today that it has reached agreements to sell television stations in three markets to facilitate regulatory approvals for its recently announced acquisition of the television and radio stations owned by Schurz Communications, Inc. (“Schurz”). Gray also announced the acquisition of three additional television stations that will result in Gray operating in one additional market. Upon the closing of all previously announced transactions, Gray will own and/or operate network affiliated television stations serving 50 markets across the country. In the Wichita, Kansas, market (DMA 65), Schurz owns CBS affiliate KWCH-TV and Gray owns ABC affiliate KAKE-TV. Gray previously announced its intention to acquire KWCH- TV and divest KAKE-TV. Gray has now reached an agreement with Lockwood Broadcast Group, Inc. (“Lockwood”) to sell all of KAKE-TV’s assets in exchange for the assets of Lockwood’s WBXX-TV and $11.2 million in cash. WBXX-TV is the CW affiliate for the Knoxville, Tennessee, market (DMA 62), where Gray owns CBS affiliate WVLT-TV. This swap will provide Gray with a second owned television station in our company’s largest market, and the cash component will slightly lower our effective purchase price for the Schurz acquisition. Gray and Lockwood will not enter into any form of shared services agreement, such that KAKE-TV will be owned and operated completely independently from Gray following the closing of this transaction. The implied pro forma broadcast cash flows of KAKE-TV and WBXX-TV (after including the cash component) are approximately equivalent. -

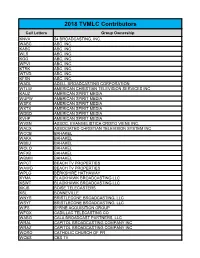

2018 TVMLC Contributors

2018 TVMLC Contributors Call Letters Group Ownership KNVA 54 BROADCASTING, INC. WABC ABC, INC. KABC ABC, INC. WLS ABC, INC. KGO ABC, INC. WPVI ABC, INC. KTRK ABC, INC. WTVD ABC, INC. KFSN ABC, INC. WADL ADELL BROADCASTING CORPORATION WTLW AMERICAN CHRISTIAN TELEVISION SERVICES INC KAUZ AMERICAN SPIRIT MEDIA WUPW AMERICAN SPIRIT MEDIA WSFX AMERICAN SPIRIT MEDIA WXTX AMERICAN SPIRIT MEDIA WDBD AMERICAN SPIRIT MEDIA KVHP AMERICAN SPIRIT MEDIA WVSN ASSOC. EVANGELISTICA CRISTO VIENE INC. WACX ASSOCIATED CHRISTIAN TELEVISION SYSTEM INC WCCB BAHAKEL WAKA BAHAKEL WBBJ BAHAKEL WOLO BAHAKEL WFXB BAHAKEL WBMM BAHAKEL WPCT BEACH TV PROPERTIES WAWD BEACH TV PROPERTIES WPLG BERKSHIRE HATHAWAY KYMA BLACKHAWK BROADCASTING LLC KSWT BLACKHAWK BROADCASTING LLC KKJB BOISE TELECASTERS KSL BONNEVILLE WNYS BRISTLECONE BROADCASTING, LLC WSYT BRISTLECONE BROADCASTING, LLC WIFS BYRNE ACQUISITION GROUP WFQX CADILLAC TELECASTING CO WABG CALA BROADCAST PARTNERS, LLC WRAL CAPITOL BROADCASTING COMPANY INC WRAZ CAPITOL BROADCASTING COMPANY INC WORO CATHOLIC CHURCH OF PR WCBS CBS TV KCBS CBS TV WBBM CBS TV KPIX CBS TV WBZ CBS TV KYW CBS TV KCAL CBS TV KCNC CBS TV WCCO CBS TV WJZ CBS TV KTVT CBS TV KOVR CBS TV KDKA CBS TV WFOR CBS TV KBCW CBS TV WSBK CBS TV WPSG CBS TV KSTW CBS TV KTXA CBS TV WKBD CBS TV WWJ CBS TV WUPA CBS TV WBFS CBS TV WTOG CBS TV KMAX CBS TV WLNY CBS TV WPCW CBS TV WGGN CHRISTIAN FAITH BROADCASTING WLLA CHRISTIAN FAITH BROADCASTING WISH CIRCLE CITY BROADCASTING INC WLNE CITADEL COMMUNICATIONS KLKN CITADEL COMMUNICATIONS WLOV COASTAL TELEVISION KTBY -

GRAY TELEVISION, INC. (Exact Name of Registrant As Specified in Its Charter) Georgia 58-0285030 (State Or Other Jurisdiction of Incorporation Or Organization) (I.R.S

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 10-K ☒ Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the fiscal year ended December 31, 2016 or ☐ Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 for the transition period from __________ to __________. Commission File Number 1-13796 ________________________________________ GRAY TELEVISION, INC. (Exact Name of Registrant as Specified in its Charter) Georgia 58-0285030 (State or Other Jurisdiction of Incorporation or Organization) (I.R.S. Employer Identification No.) 4370 Peachtree Road, NE Atlanta, GA 30319 (Address of Principal Executive Offices) (Zip Code) Registrant’s telephone number, including area code: (404) 504-9828 Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered Class A Common Stock (no par value) New York Stock Exchange Common Stock (no par value) New York Stock Exchange Securities registered pursuant to Section 12(g) of the Act: NONE ________________________________________ Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒ Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒ Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. -

DA-18-1286A1.Pdf

Federal Communications Commission DA 18-1286 Before the Federal Communications Commission Washington, D.C. 20554 In the Matter of Applications for ) ) Consent to Transfer Control of Certain License ) MB Docket No. 18-230 Subsidiaries of Raycom Media, Inc. to Gray ) Television, Inc. ) File Nos. BALCDT-20180709ACV, et al. ) Consent to Assignment of Certain Licenses from ) Subsidiaries of Raycom Media, Inc. to a Subsidiary ) of Gray Television, Inc. ) ) Consent to Assignment of Certain Licenses from ) Subsidiaries of Raycom Media, Inc. to ) Subsidiaries of Lockwood Broadcasting, Inc. ) File Nos. BALCDT-20180828AAE, et al ) Consent to Assignment of Certain Licenses from ) Subsidiaries of Raycom Media, Inc. to ) Subsidiaries of the E.W. Scripps Company ) File Nos. BALCDT-20180828AAK, et al. ) Consent to Assignment of Certain Licenses from ) Subsidiaries of Raycom Media, Inc. to ) Subsidiaries of TEGNA, Inc. ) File Nos. BALCDT-20180829AAY, et al. ) Consent to Assignment of WSWG(DT), Valdosta, ) Georgia from a Subsidiary of Gray Television ) Licensee, LLC to Marquee Broadcasting Georgia, ) File No. BALCDT-20180823AAT Inc. ) MEMORANDUM OPINION AND ORDER Adopted: December 20, 2018 Released: December 20, 2018 By the Chief, Media Bureau: I. INTRODUCTION 1. The Media Bureau (Bureau) has before it applications in the attached appendices that: (1) seek consent to the assignment of certain television broadcast licenses held by subsidiaries of Raycom Media, Inc. (Raycom) to a subsidiary of Gray Television, Inc. (Gray) (jointly, the Applicants), and to the transfer of control of subsidiaries of Raycom holding television broadcast licenses to Gray (the Applications);1 and (2) seek consent to divest certain stations necessary to bring the post-transaction Gray into compliance with the Local Television Ownership Rule.2 DISH Network L.L.C.