Dr. Daniel Yergin Vice Chairman, IHS Markit ______

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Deception, Disinformation, and Strategic Communications: How One Interagency Group Made a Major Difference by Fletcher Schoen and Christopher J

STRATEGIC PERSPECTIVES 11 Deception, Disinformation, and Strategic Communications: How One Interagency Group Made a Major Difference by Fletcher Schoen and Christopher J. Lamb Center for Strategic Research Institute for National Strategic Studies National Defense University Institute for National Strategic Studies National Defense University The Institute for National Strategic Studies (INSS) is National Defense University’s (NDU’s) dedicated research arm. INSS includes the Center for Strategic Research, Center for Complex Operations, Center for the Study of Chinese Military Affairs, Center for Technology and National Security Policy, Center for Transatlantic Security Studies, and Conflict Records Research Center. The military and civilian analysts and staff who comprise INSS and its subcomponents execute their mission by conducting research and analysis, publishing, and participating in conferences, policy support, and outreach. The mission of INSS is to conduct strategic studies for the Secretary of Defense, Chairman of the Joint Chiefs of Staff, and the Unified Combatant Commands in support of the academic programs at NDU and to perform outreach to other U.S. Government agencies and the broader national security community. Cover: Kathleen Bailey presents evidence of forgeries to the press corps. Credit: The Washington Times Deception, Disinformation, and Strategic Communications: How One Interagency Group Made a Major Difference Deception, Disinformation, and Strategic Communications: How One Interagency Group Made a Major Difference By Fletcher Schoen and Christopher J. Lamb Institute for National Strategic Studies Strategic Perspectives, No. 11 Series Editor: Nicholas Rostow National Defense University Press Washington, D.C. June 2012 Opinions, conclusions, and recommendations expressed or implied within are solely those of the contributors and do not necessarily represent the views of the Defense Department or any other agency of the Federal Government. -

Britain, British Petroleum, Shell and the Remaking of the International Oil Industry, 1957-1979

Empires of Energy: Britain, British Petroleum, Shell and the Remaking of the International Oil Industry, 1957-1979 Author: Jonathan Robert Kuiken Persistent link: http://hdl.handle.net/2345/bc-ir:104079 This work is posted on eScholarship@BC, Boston College University Libraries. Boston College Electronic Thesis or Dissertation, 2013 Copyright is held by the author, with all rights reserved, unless otherwise noted. Boston College The Graduate School of Arts and Sciences Department of History EMPIRES OF ENERGY: BRITAIN, BRITISH PETROLEUM, SHELL AND THE REMAKING OF THE INTERNATIONAL OIL INDUSTRY, 1957-1979 [A dissertation by] JONATHAN R. KUIKEN submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy August, 2013 © copyright by JONATHAN ROBERT KUIKEN 2013 Empires of Energy: Britain, British Petroleum, Shell and the remaking of the international oil industry, 1957-1979 Jonathan R. Kuiken Dissertation Advisor - James E. Cronin Dissertation Abstract This dissertation examines British oil policy from the aftermath of the Suez Crisis in 1956-1957 until the Iranian Revolution and the electoral victory of Margaret Thatcher’s Conservative Party in 1979. It was a period marked by major transitions within Britain’s oil policy as well as broader changes within the international oil market. It argues that the story of Britain, and Britain’s two domestically-based oil companies, BP and Shell, offers a valuable case study in the development of competing ideas about the reorganization of the international oil industry in the wake of the rise of the Organization of Petroleum Exporting countries and the companies’ losing control over the production of oil. -

Energy Transitions Present and Future

IHS ENERGY Energy Transitions Present and future October 2015 ihs.com STRATEGIC REPORT Daniel Yergin Vice Chairman, IHS, and author of The Quest: Energy, Security, and the Remaking of the Modern World IHS Energy | Energy Transitions: Present and future Contents The beginning of energy transitions 5 The “rule of energy inertia” 6 Capturing the sun 7 Wind gears up 8 Lithium-ion batteries—Back to 1976 8 Energy efficiency—Different tempo 8 IHS™ ENERGY © 2015 IHS. This report is subject to IHS copyright but you are free to redistribute the entire report in the form as made available by IHS and provided that it is attributed to Daniel Yergin and IHS (www.ihs.com) and all IHS legal notices and markings are displayed and you do not redistribute the report for revenue or other commercial purposes or in any way that suggests that IHS endorses you or your business. This report is provided AS IS without warranty and IHS shall not be liable for any errors or omissions in this report or any loss, damage, or expense incurred by reliance on information or any statement, forecast or assumption contained herein. This report is not to be construed as legal or financial advice. IHS and the IHS logo are trademarks of IHS. © 2015 IHS 2 October 2015 IHS Energy | Energy Transitions: Present and future Energy Transitions Present and future Key implications In this essay, which originally appeared in The Wall Street Journal, Daniel Yergin, Vice Chairman, IHS, and author of The Quest: Energy, Security, and the Remaking of the Modern World, examines the patterns of energy transitions and the state of energy innovation. -

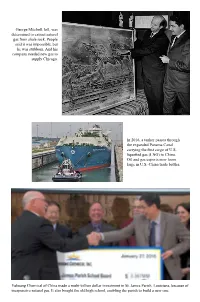

George Mitchell, Left, Was Determined to Extract Natural Gas from Shale Rock

George Mitchell, left, was determined to extract natural gas from shale rock. People said it was impossible, but he was stubborn. And his company needed new gas to supply Chicago. In 2016, a tanker passes through the expanded Panama Canal carrying the first cargo of U.S. liquefied gas (LNG) to China. Oil and gas exports now loom large in U.S.-China trade battles. Yuhuang Chemical of China made a multi-billion dollar investment in St. James Parish, Louisiana, because of inexpensive natural gas. It also bought the old high school, enabling the parish to build a new one. In 2010, Mark Papa predicted that shale oil would be a North American “game changer”. It turned out to be a global game changer. The Permian basin in West Texas and New Mexico is now world’s second largest producing area, propelling the United States to becoming the world’s largest oil producer in 2018, ahead of Saudi Arabia and Russia. Horizontal drilling taps multiple zones containing shale oil. President Donald Trump told India’s Prime Minister Narendra Modi that he looked forward to India’s buying more U.S. LNG. But, he added, he was “trying to get the price up a little.” With gasoline prices high in 2012, Barack Obama flew to pipeline junction at Cushing, Oklahoma, to declare that his administration would “cut through” red tape to “get done” the building of southern segment of Keystone pipeline, which starts in Canada. In 2016 and 2017, protestors tried to block last 1320 feet of 1172-mile Dakota Access pipeline, which was built to move new Bakken oil out of North Dakota, replacing 740 rail cars a day. -

Pestilence and Other Calamities in Civilizational Theory: Sorokin, Mcneill, Diamond, and Beyond

Comparative Civilizations Review Volume 83 Number 83 Fall Article 13 9-2020 Pestilence and Other Calamities in Civilizational Theory: Sorokin, McNeill, Diamond, and Beyond Vlad Alalykin-Izvekov [email protected] Follow this and additional works at: https://scholarsarchive.byu.edu/ccr Part of the Comparative Literature Commons, History Commons, International and Area Studies Commons, Political Science Commons, and the Sociology Commons Recommended Citation Alalykin-Izvekov, Vlad (2020) "Pestilence and Other Calamities in Civilizational Theory: Sorokin, McNeill, Diamond, and Beyond," Comparative Civilizations Review: Vol. 83 : No. 83 , Article 13. Available at: https://scholarsarchive.byu.edu/ccr/vol83/iss83/13 This Essay is brought to you for free and open access by the Journals at BYU ScholarsArchive. It has been accepted for inclusion in Comparative Civilizations Review by an authorized editor of BYU ScholarsArchive. For more information, please contact [email protected], [email protected]. Alalykin-Izvekov: Pestilence and Other Calamities in Civilizational Theory: Sorokin 20 Number 83, Fall 2020 Pestilence and Other Calamities in Civilizational Theory: Sorokin, McNeill, Diamond, and Beyond Vlad Alalykin-Izvekov [email protected] Everybody knows that pestilences have a way of recurring in the world; yet somehow we find it hard to believe in ones that crash down on our heads from a blue sky. — Albert Camus Truth unfolds in time through a communal process. — Carroll Quigley Those who make peaceful revolution impossible will make violent revolution inevitable. — John F. Kennedy Abstract This paper analyses the phenomenon of pestilence through paradigmatic and methodological lenses of several outstanding social scholars, including Pitirim A. Sorokin, William H. McNeill, and Jared M. -

60 Years BP Statistical Review of World Energy Bp.Com/60Yearsstatisticalreview 1 9 5 1 – 2 0 1 1 What’S Inside

60 Years BP Statistical Review of World Energy bp.com/60yearsstatisticalreview 1 9 5 1 – 2 0 1 1 What’s inside The BP Statistical Review of World Energy is now 60 1 Celebrating 60 years years old. It is the longest running compilation of global energy statistics available. Collected down the years, it 2 How it all began has become widely recognized as a key source of data on energy markets, useful to business, policy, academia, journalists and the public alike. It seems fair to say that it 4 The first map of a global trade has become a crucial resource, underpinning with facts discussions about energy or the environment. 6 Branching out Over the past 60 years, the Review has expanded from six typewritten pages plus one page for graphical 8 The impact of 1973 illustrations to an internet database that can be used for very detailed analysis. Behind the published data are 9 A lesson in numbers about 300,000 single data entries – at the last count, and growing every day, of course. Yet, in a world ever more concerned with the commercial value of data, it is 10 Fuel diversity freely available to all who wish to use it. Above all, there is no wishful thinking, no politics and no spin. It is simply 11 The editor explains the numbers a portrait in numbers of global energy production, consumption, trade, reserves and prices. 12 Sustaining objectivity These numbers contain the story of energy in the last half of the 20th century and the beginning of 13 Pro bono Christof Rühl this one. -

THE QUEST: ENERGY, SECURITY, and the REMAKING of the MODERN WORLD by Daniel Yergin, Penguin Press 2011

THE QUEST: ENERGY, SECURITY, AND THE REMAKING OF THE MODERN WORLD By Daniel Yergin, Penguin Press 2011 Reviewed by Jonathan D. Schneider* Daniel Yergin has done much for the reputation of oil as a central figure on the world stage over the course of the 20th Century. While others have chronicled the careers of those who developed and profited from the resource, Yergin gave the substance itself the starring role it deserves in his 1992 work, The Prize.1 Yergin won a Pulitzer for the book, and he deserved it for so well telling the story of oil’s career as it rose from coal’s less prominent cousin at the outset of 20th Century to its starring role as the world’s predominant energy resource. Yergin’s tale of oil’s influence on world events includes the riveting back story leading to World War II, as Japanese naval strategists pressed for the attack on Pearl Harbor as a means of securing oil supplies in the Pacific. The Prize concluded with the rise of OPEC, and the profound resulting shift in the axis of world power, as developed nations adjusted to a new and relatively less self-sufficient reality. In The Quest,2 Yergin picks up the thread of the story in the latter part of the 20th Century, a time in which fossil fuels have shared the stage with other forms of energy more favored by certain policy makers, while the world reeled from the break-up of the Soviet Union and the emergence of newly independent oil-producing nations in the former Soviet Republics. -

Why the United States Must End the Second Cold War As It Begins Adam Fernandez

Florida State University Libraries Electronic Theses, Treatises and Dissertations The Graduate School 2008 Why the United States Must End the Second Cold War as It Begins Adam Fernandez Follow this and additional works at the FSU Digital Library. For more information, please contact [email protected] FLORIDA STATE UNIVERSITY COLLEGE OF SOCIAL SCIENCES WHY THE UNITED STATES MUST END THE SECOND COLD WAR AS IT BEGINS By ADAM FERNANDEZ A Thesis submitted to the Department of International Affairs in partial fulfillment of the requirements for the degree of Master of Science Degree Awarded: Fall Semester, 2008 The members of the Committee approve the Thesis of Adam Fernandez defended on September 23, 2008. Jonathan Grant Professor Directing Thesis Michael Creswell Committee Member Charles Upchurch Committee Member Approved: Lee Metcalf, Chair, International Affairs Program The Office of Graduate Studies has verified and approved the above named committee members. ii TO MY WIFE JANELLE. iii TABLE OF CONTENTS Abstract ...................................................................................................... vi Introduction ................................................................................................ 1 1. One Hundred Years of Peace between Russia and America................ 4 Early Relations between the United States and Russia ...................... 4 The War to End All Wars Leads to Revolution in Russia .................. 5 The Washington Conference ................................................................. -

Non-Fiction Inside Biosphere 2: Earth Science Under Glass by Mary Kay Carson; with Photographs 304.2 CAR by Tom Uhlman

To borrow the titles mentioned below, please contact Circulation desk: 022-26724024 or write to us at [email protected] Call. No Particulars Non-Fiction Inside Biosphere 2: Earth Science Under Glass By Mary Kay Carson; with photographs 304.2 CAR by Tom Uhlman. 2016 “A Problem From Hell": America And The Age of Genocide by Samantha Power. 304.663 POW 2013 305.42 SLA Unfinished Business: Women, Men, Work, Family by Anne-Marie Slaughter. 2015 305.55 STA Social Transformation of American Medicine by Paul Starr. 1982 323.1196073 BAU March Against Fear by Ann Bausum. 2016 International Public Relations And Public Diplomacy: Communication And 327.11 INT Engagement by Guy J. Golan. 2015 330.019 THA Misbehaving: The Making Of Behavioral Economics by Richard H. Thaler. 2016 House of Morgan: An American Banking Dynasty And The Rise of Modern Finance 332.12 MOR by Ron Chernow. 2001 338.2728 YER The Prize: The Epic Quest For Oil, Money, & Power By Daniel Yergin. 2009 Making Curriculum Pop: Developing Literacies In All Content Areas By Pam Goble, 371.334 GOB Ed.D. And Ryan R. Goble. 2016 378.73 PET Peterson's Two-Year Colleges 2014 by Bernadette Webster, managing editor. 2013 We Are Market Basket: The Story Of The Unlikely Grassroots Movement That Saved 381.45 KOR A Beloved Business by Daniel Korschun & Grant Welker. 2015 381.457 WIT How Music Got Free: A Story of Obsession and Invention by Stephen Witt. 2016 Word Power Made Easy: The Complete Handbook For Building A Superior 428.1 LEW vocabulary by Norman Lewis. -

New World of Rivalries: Reshaping the Energy Future

11-15 March 2019 38th Executive Conference and Related Events New World of Rivalries: Reshaping the Energy Future Dialogue: Bob Dudley, BP plc Group Chief Executive 12 March, Tuesday Daniel Yergin, vice chairman, IHS Markit Bob Dudley, group chief executive, BP plc Summary In prepared remarks and a Q&A to close out the 2nd day of CERAWeek 2019, Bob Dudley, group chief executive, BP plc, shared with attendees his optimistic and expansive vision of the global energy industry and its future. But at the same time, he warned that the challenge of climate change is immense, and the industry must make a deep and lasting commitment to be part of the solution. “We in the energy industry and at BP have a deep sense of purpose, and I’m proud of that,” Dudley said. “But it does not give us a blank check.” Fortunately, Dudley believes the industry is well-positioned to maintain its positive influence. “The industry is in better shape than it has been in a long time,” he said, listing achievements such as rising and less costly oil and gas production, new investments in methane capture and “disciplined cost of capital that I think is here to stay.” All of those efforts must remain intact if the industry is to meet the twin goals of reducing carbon emissions and continuing to raise living standards around the world. Dudley said that 80% of the world’s population lives in nations where “increased energy demand goes hand in hand with higher living standards,” so any forecasts of falling world demand for energy are simply unrealistic. -

Still the American Century

Copyright © British International Studies Association 1999 Still the American Century BRUCE CUMINGS At the inception of the twenty-first century—not to mention the next millennium— books on ‘the American Century’ proliferate monthly, if not daily.1 We now have The American Century Dictionary, The American Century Thesaurus, and even The American Century Cookbook; perhaps the American Century baseball cap or cologne is not far behind. With one or two exceptions, the authors celebrate the unipolar pre-eminence and comprehensive economic advantage that the United States now enjoys. Surveys of public opinion show that most people agree: the American wave appears to be surging just as the year 2000 beckons. Unemployment and inflation are both at twenty-year lows, sending economists (who say you can’t get lows for both at the same time) back to the drawing board. The stock market roars past the magic 10,000 mark, and the monster federal budget deficit of a decade ago miraculously metamorphoses into a surplus that may soon reach upwards of $1 trillion. Meanwhile President William Jefferson Clinton, not long after a humiliating impeachment, is rated in 1999 as the best of all postwar presidents in conducting foreign policy (a dizzying ascent from eighth place in 1994), according to a nationwide poll by the Chicago Council on Foreign Relations. This surprising result might also, of course, bespeak inattention: when asked to name the two or three most important foreign policy issues facing the US, fully 21 per cent of the public couldn’t think of one (they answered ‘don’t know’), and a mere seven per cent thought foreign policy issues were important to the nation.2 But who cares, when all is for the best in the best of all possible worlds? If this intoxicating optimism is commonplace today, it would have seemed demented just a few short years ago: back then, the scholars and popular pundits who are supposed to know the occult science of international affairs were full of dread about American decline and Japanese and German advance. -

The Fates of American Presidents Who Challenged the Deep State (1963-1980) アメリカの深層国家に抗した大統領の運 命(1963-1980)

Volume 12 | Issue 43 | Number 4 | Article ID 4206 | Oct 20, 2014 The Asia-Pacific Journal | Japan Focus The Fates of American Presidents Who Challenged the Deep State (1963-1980) アメリカの深層国家に抗した大統領の運 命(1963-1980) Peter Dale Scott In the last decade it has become more and subsurface part of the iceberg I more obvious that we have in America today shall call the Deep State, which what the journalists Dana Priest and William operates according to its own Arkin have called compass heading regardless of who is formally in power.3 two governments: the one its citizens were familiar with, I believe that a significant shift in the operated more or less in the open: relationship between public and deep state the other a parallel top secret power occurred in the 1960s and 1970s, government whose parts had culminating in the Reagan Revolution of 1980. mushroomed in less than a decade In this period five presidents sought to curtail into a gigantic, sprawling universe the powers of the deep state. And as we shall of its own, visible to only a see, the political careers of all five—Kennedy, carefully vetted cadre—and its Johnson, Nixon, Ford and Carter—were cut off entirety . visible only to God.1 in ways that were unusual. One president, Kennedy, was assassinated. Another, Nixon, was forced to resign. And in 2013, particularly after the military return to power in Egypt, more and more To some extent the interplay of these two forms authors referred to this second level asof power and political organization is found in 2 America’s “deep state.” Here for example is all societies.