Presentation Title

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

1983 Ketron Inc

DOT-TSC-U MT A -83-2 Wheelchair Lifts on U.S.Department of Transportation Transit Buses Urban Mass Transportation Administration Prepared by: January 1983 Ketron Inc. H: 3 1 ~ 190 i EQUIPM ENT ENGlNEERING DEPARTMENT NOTICE This document is disseminated under the sponsorship of the Department of Trans portation in the interest of information exchange. The United States Government assumes no liability for its contents or use thereof. The United States Government does not endorse products or manufacturers. Trade or manufacturers' names appear herein solely because they are considered essential to th e object of this report. DOT-TSC-U tv'IT A-83-2 S.C.R. T.D. LIBRARY Wheelchair Lifts on U.S. Department of Transportation Urban Mass Transit Buses Transportation Administration Summary of U. S. Experience Prepared by: Ketron Inc. One Broadway Cambridge MA 02142 Office of Technical Assistance Office of Bus and Paratransit Systems Washington DC 20590 0-7548 ~ .. PREFACE This project was conducted for the USDOT Transportati on Systems Center (TSC) and the Urban Mass Transportation Administration (UMTA) by KETRON, Inc . - Cambridge Facility. The contract \vas initiated in September, 1980 betv1een TSC and Applied Resour ce Integration, Ltd. (ARI) of Boston - Contract r~o . DTRS57-80-C-00150 . In 1981 KETRON acquired ARI and t he project was continued and completed by the same project teom . The successful completion of t he project is attr ibutabl e to the cooperation of a large number of organizations and personnel representing t r ansit properties, bus manuf ac t ur Prs, lift su pp liers , and others concerned v1ith the problem of acccssi bil ity on public transit systems. -

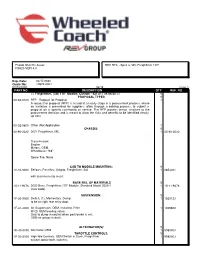

Flroida Sheriff's Assoc REV RTC - Spec 3- WC Freightliner 170" FSA20-VEF14.0

Flroida Sheriff's Assoc REV RTC - Spec 3- WC Freightliner 170" FSA20-VEF14.0 Exp. Date: 03/15/2020 Quote No: 10572-0001 02/20/2020 WO#: Page 1 PART NO DESCRIPTION QTY REF. NO == Freightliner, (SO) 170" Module, Custom - 621.017 01/06/20 == 1 PROPOSAL TYPES 1 00-02-0100 RFP - Request for Proposal 1 A request for proposal (RFP) is issued at an early stage in a procurement process, where an invitation is presented for suppliers, often through a bidding process, to submit a proposal on a specific commodity or service. The RFP process brings structure to the procurement decision and is meant to allow the risks and benefits to be identified clearly up front 00-02-0800 Other (Not Applicable) 1 CHASSIS: 1 00-90-2032 2021 Freightliner, M2, 1 00-90-2030 Transmission: Engine: Mirrors, OEM. Wheelbase: 168" Spare Tire, None CAB TO MODULE MOUNTING: 1 10-10-8000 Bellows, Passthru, Unigrip, Freightliner, Std 1 0653021 with aluminum cab insert. BASE BILL OF MATERIALS 1 15-11-9376 2020 Base, Freightliner,170" Module, Standard Model 2020-1 1 15-11-9376 (new code) SUSPENSION: 1 1F-30-9000 Switch, (1), Momentary, Dump 1 1530123 to be on right rear entry door. 1F-31-3000 Air Suspension, OEM, Installed, Frtlnr 1 1009608 W/(2) OEM leveling valves. Only to dump in neutral when park brake is set. OEM air gauge in dash. ALTERNATOR(S): 1 1K-40-5000 Alternator,OEM 1 9980003 THROTTLE CONTROLS: 1 1P-50-5000 High Idle Controls, OEM Switch in Dash, Freightliner 1 9980003 w/label above both switches. -

INVESTOR PRESENTATION August 2019

INVESTOR PRESENTATION August 2019 NFI:TSX Who is NFI? Bus Design & Manufacture Part Fabrication Parts and Service North America’s largest bus and North America’s largest heavy-duty Captive fiberglass reinforced plastic motor coach parts distributor public transit bus manufacturer fabricator for MCI, New Flyer and ADL and the leader in Zero-Emission Bus (ZEB) transit Captive parts fabricator for New Flyer, UK’s leading bus parts distributor North American market leader in ARBOC and NFI Parts. Plans to and aftermarket service support motor coaches for both Public and KMG fabricate for MCI and ADL beyond network Private operators 2020 U.K.’s largest bus and motor coach Supports eMobility projects from manufacturer with leading share in start to finish Hong Kong and New Zealand and a growing global presence. North America’s first innovation North America’s disruptive low-floor lab dedicated to the exploration cutaway and medium-duty transit and advancement of bus and bus leader coach technology 2 Why Invest In NFI? Track Record Our Differentiators • Trusted business partner with over 300 years of combined bus • Market leading positions in US, Canada, UK, Hong Kong and and motor coach design and manufacturing experience New Zealand with strong portfolios in Singapore, Malaysia and Mexico • 5 year Q2 2019 LTM Revenue CAGR of 13.1% and Adj. EBITDA CAGR of 21.5% • Growing presence in Switzerland and Germany (gateway into continental Europe) • Peer Leading(1) 11.6% Q2 2019 LTM Adj. EBITDA margin • ~80% of revenue driven by public (i.e. government -

Global Equity Fund Description Plan 3S DCP & JRA MICROSOFT CORP

Global Equity Fund June 30, 2020 Note: Numbers may not always add up due to rounding. % Invested For Each Plan Description Plan 3s DCP & JRA MICROSOFT CORP 2.5289% 2.5289% APPLE INC 2.4756% 2.4756% AMAZON COM INC 1.9411% 1.9411% FACEBOOK CLASS A INC 0.9048% 0.9048% ALPHABET INC CLASS A 0.7033% 0.7033% ALPHABET INC CLASS C 0.6978% 0.6978% ALIBABA GROUP HOLDING ADR REPRESEN 0.6724% 0.6724% JOHNSON & JOHNSON 0.6151% 0.6151% TENCENT HOLDINGS LTD 0.6124% 0.6124% BERKSHIRE HATHAWAY INC CLASS B 0.5765% 0.5765% NESTLE SA 0.5428% 0.5428% VISA INC CLASS A 0.5408% 0.5408% PROCTER & GAMBLE 0.4838% 0.4838% JPMORGAN CHASE & CO 0.4730% 0.4730% UNITEDHEALTH GROUP INC 0.4619% 0.4619% ISHARES RUSSELL 3000 ETF 0.4525% 0.4525% HOME DEPOT INC 0.4463% 0.4463% TAIWAN SEMICONDUCTOR MANUFACTURING 0.4337% 0.4337% MASTERCARD INC CLASS A 0.4325% 0.4325% INTEL CORPORATION CORP 0.4207% 0.4207% SHORT-TERM INVESTMENT FUND 0.4158% 0.4158% ROCHE HOLDING PAR AG 0.4017% 0.4017% VERIZON COMMUNICATIONS INC 0.3792% 0.3792% NVIDIA CORP 0.3721% 0.3721% AT&T INC 0.3583% 0.3583% SAMSUNG ELECTRONICS LTD 0.3483% 0.3483% ADOBE INC 0.3473% 0.3473% PAYPAL HOLDINGS INC 0.3395% 0.3395% WALT DISNEY 0.3342% 0.3342% CISCO SYSTEMS INC 0.3283% 0.3283% MERCK & CO INC 0.3242% 0.3242% NETFLIX INC 0.3213% 0.3213% EXXON MOBIL CORP 0.3138% 0.3138% NOVARTIS AG 0.3084% 0.3084% BANK OF AMERICA CORP 0.3046% 0.3046% PEPSICO INC 0.3036% 0.3036% PFIZER INC 0.3020% 0.3020% COMCAST CORP CLASS A 0.2929% 0.2929% COCA-COLA 0.2872% 0.2872% ABBVIE INC 0.2870% 0.2870% CHEVRON CORP 0.2767% 0.2767% WALMART INC 0.2767% -

Alphabetical Index

Alphabetical Index 1st Source Corporation 3 Aerojet-General Corporation 12 Allied/Egry Business Systems, Inc 25 20th Century Industries 3 Aeronautical Electric Co 13 Allied Materials Corporation 26 3COM Corporation 3 Aeronca Inc 13 Allied Paper Inc 26 3M 3 Aeroquip Corporation 13 Allied Products Company 26 A A Brunell Electroplating Aerospace Corporation 13 Allied Products Corporation 26 Corporation 4 Aetna Life & Casualty Company 13 Allied Security Inc 26 A B Dick Company 4 Aetna Life Insurance & Annuity Co 13 Allied Stores Corporation 26 A C Nielsen Co 4 Aetna Life Insurance Co 14 Allied Van Lines, Inc 27 A E Staley Mfg Co 4 Affiliated Bank Corporation of Allied-Lyons North America A G Edwards Inc 4 Wyoming 14 Corporation 27 A H Belo Corporation 4 Affiliated Bankshares of Colorado 14 Allied-Signal Aerospace Company 27 A H Robins Company, Inc 4 Affiliated Food Stores, Inc 14 Allied-Signal, Inc 27 A Johnson & Company, Inc 4 Affiliated Hospital Products, Inc 14 Allis-Chalmers Corporation 28 A L Williams Corporation (The) 4 Affiliated Publications, Inc 15 Allstate Insurance Group 28 A M Castle & Co 4 AFG Industries, Inc 15 Alltel Corporation 28 A 0 Smith Corporation 4 Ag Processing Inc 15 Alma Plastics Companies 28 A P Green Refractories Co 4 Agency-Rent-A-Car Inc 15 Aloha Inc 28 A Schulman Inc 4 AGRI Industries 16 Alpha Corporation of Tennessee 28 AT Cross Co 4 AGRIPAC Inc 16 Alpha Industries Inc 28 A Y McDonald Industries, Inc 4 Ags Computers Inc 16 Alpha Metals, Inc 29 A&E Products Group, Inc 4 AGWAY Inc 16 Alpha Microsystems 29 A&M Food -

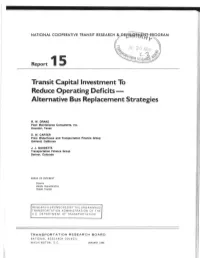

L.1 ~~1 - ~~ !! DN Rfseahc~ ~// Report 1 5 ~--~

NATIONAL COOPERATIVE TRANSIT RESEARCH rEt'.-E\19™- c/IJ/ 2 0 /"Qc ~ ~~ u ~ J'..oOt?r, · L.1 ~~1 - ~~ !!_DN RfSEAHC~ ~// Report 1 5 ~--~ Transit Capital Investment To Reduce Operating Deficits - Alternative Bus Replacement Strategies R. W. DRAKE Fleet Maintenance Consultants, Inc. Houston, Texas D. W. CARTER Price Waterhouse and Transportation Finance Group Oakland, California J. J. GAUDETTE Transportation Finance Group Denver, Colorado AREAS OF INTEREST Finance Vehicle Characteristics (Public Transit) RESEAR CH SPONSORED BY THE URBAN MASS TRANSPORTATION ADMINISTRATION OF THE US DEPARTMENT OF TRANSP ORTA T ION TRANSPORTATION RESEARCH BOARD NATIONAL RESEARCH COUNCIL WASHINGTON , D.C . JANUARY 1988 NATIONAL COOPERATIVE TRANSIT RESEARCH & DEVELOPMENT PROGRAM Administrators, engineers, and many others in the transit in NCTRP REPORT 15 dustry are faced with a multitude of complex problems that range between local, regional, and national in their prevalence. Project 31-2 FY '84 How they might be solved is open to a variety of approaches; ISSN 0732-4839 however, it is an established fact that a highly effective approach ISBN 0-309-04571-1 to problems of widespread commonality is one is which oper Library of Congress Catalog Card No. 88-50067 ating agencies join cooperatively to support, both in financial Price: $10.40 and other participatory respects, systematic research that is well designed, practically oriented, and carried out by highly com petent researchers. As problems grow rapidly in number and NOTICE escalate in complexity, the value of an orderly, high-quality The project that is the subject of this report was 11 part of the National Cooperative cooperative endeavor likewise escalates. -

Propane Autogas School Bus Manufacturers

PROPANE AUTOGAS SCHOOL BUS MANUFACTURERS When schools adopt propane autogas school buses, everyone — students, parents, and educators — wins. Schools can reduce fuel and maintenance costs with propane autogas buses compared with diesel, giving them the opportunity to invest those savings where it matters most — back in the classroom. Here’s a list of propane-powered school bus manufacturers. Blue Bird Corporation www.blue-bird.com Blue Bird offers a complete line of Type A, C and D school buses in a variety of options and configurations. Since 1927, Blue Bird Corporation has continued to set industry standards with its innovative design and manufacturing capabilities. Additionally, Blue Bird provides comprehensive financial solutions through Blue Bird Capital Services. Today, Blue Bird has more than 1,500 employees, Georgia-based manufacturing facilities and an extensive network of Dealers and Parts & Service facilities throughout North America. Its global presence can be seen in more than 60 countries through sales into Africa, Asia, the Caribbean, Latin America, Europe and the Middle East. Collins Bus Corporation www.collinsbuscorp.com Headquartered in Hutchinson, Kansas, Collins Industries specializes in manufacturing Type A school buses, and also manufactures ambulances and other special-purpose vehicles. The company’s Nexbus Propane model is available only on a GM chassis. It was built in conjunction with CleanFUEL USA, which was the first company to develop liquid propane fuel injection engine systems in the United States. IC Bus www.icbus.com Each vehicle built by IC Bus is backed by the power of Navistarr, a global leader in the transportation industry with more than 175 years of experience building trucks, buses, RVs, and defense vehicle. -

Usef-I Q2 2021

Units Cost Market Value U.S. EQUITY FUND-I U.S. Equities 88.35% Domestic Common Stocks 10X GENOMICS INC 5,585 868,056 1,093,655 1ST SOURCE CORP 249 9,322 11,569 2U INC 301 10,632 12,543 3D SYSTEMS CORP 128 1,079 5,116 3M CO 11,516 2,040,779 2,287,423 A O SMITH CORP 6,897 407,294 496,998 AARON'S CO INC/THE 472 8,022 15,099 ABBOTT LABORATORIES 24,799 2,007,619 2,874,948 ABBVIE INC 17,604 1,588,697 1,982,915 ABERCROMBIE & FITCH CO 1,021 19,690 47,405 ABIOMED INC 9,158 2,800,138 2,858,303 ABM INDUSTRIES INC 1,126 40,076 49,938 ACACIA RESEARCH CORP 1,223 7,498 8,267 ACADEMY SPORTS & OUTDOORS INC 1,036 35,982 42,725 ACADIA HEALTHCARE CO INC 2,181 67,154 136,858 ACADIA REALTY TRUST 1,390 24,572 30,524 ACCO BRANDS CORP 1,709 11,329 14,749 ACI WORLDWIDE INC 6,138 169,838 227,965 ACTIVISION BLIZZARD INC 13,175 839,968 1,257,422 ACUITY BRANDS INC 1,404 132,535 262,590 ACUSHNET HOLDINGS CORP 466 15,677 23,020 ADAPTHEALTH CORP 1,320 39,475 36,181 ADAPTIVE BIOTECHNOLOGIES CORP 18,687 644,897 763,551 ADDUS HOMECARE CORP 148 13,034 12,912 ADOBE INC 5,047 1,447,216 2,955,725 ADT INC 3,049 22,268 32,899 ADTALEM GLOBAL EDUCATION INC 846 31,161 30,151 ADTRAN INC 892 10,257 18,420 ADVANCE AUTO PARTS INC 216 34,544 44,310 ADVANCED DRAINAGE SYSTEMS INC 12,295 298,154 1,433,228 ADVANCED MICRO DEVICES INC 14,280 895,664 1,341,320 ADVANSIX INC 674 15,459 20,126 ADVANTAGE SOLUTIONS INC 1,279 14,497 13,800 ADVERUM BIOTECHNOLOGIES INC 1,840 7,030 6,440 AECOM 5,145 227,453 325,781 AEGLEA BIOTHERAPEUTICS INC 287 1,770 1,998 AEMETIS INC 498 6,023 5,563 AERSALE CORP -

2020 Milwaukee Business Journal Insert

COMMUNITY PARTNER RECOGNITION 2020 COMMUNITY CAMPAIGN Every year, thousands of organizations support United Way’s Publication Sponsor: Community Campaign through workplace campaigns, corporate gifts, sponsorships, and more. We thank everyone who helped create lasting change in our community. You are the example of what it means to Live United. THANK YOU 2020 COMMUNITY CAMPAIGN ALL-STARS TOTAL COMBINED GIVING $4.8 MILLION $3.6 MILLION $3.4 MILLION $3.2 MILLION $2.5 MILLION $2.3 MILLION $1.8 MILLION $1.7 MILLION $1.6 MILLION $1 MILLION $1 MILLION UnitedWayGMWC.org Thank you to all the organizations who ran a workplace campaign and/or supported 2020 TOTAL COMBINED GIVING United Way with a sponsorship, in-kind donation, corporate gift, foundation gift, or treasury gift. SUPER STARS Meijer GUARDIAN raSmith Michael Best & Friedrich LLP Regal Beloit Corporation - Grafton $500,000 - $999,999 Milwaukee County $10,000 - $24,999 Rite Hite Corporation Foundation Milwaukee Journal Sentinel Rogers Behavioral Health Foundation Children’s Wisconsin Advicent Pieper Electric, Inc./Ideal Mechanical RSM US LLP Foley & Lardner LLP AHEAD R&R Insurance Services, Inc. Ruekert & Mielke, Inc. GE Healthcare Alight Solutions State of Wisconsin S & C Electric Company Harley-Davidson Motor Company American Red Cross STRATTEC Security Corporation salesforce.com Johnson Financial Group in Southeastern Wisconsin Target Schlossmann’s Automotive Group ManpowerGroup Anderson Packaging, LLC University of Wisconsin - Milwaukee School District of Waukesha MGIC Investment Corporation Avaya, Inc. UW Credit Union Sentry Equipment Corp. Quarles & Brady LLP Briohn Building Corporation von Briesen & Roper, s.c. ServiceNow, Inc. U.S. Bank Carroll University Wells Fargo Shorewest Realtors Check Point Sikich LLP CIBC Cleary Gull SoftwareONE, Inc. -

Top 10 School Bus Companies Blog

TOP 10 SCHOOL BUS COMPANIES Throughout the years, the task of making the best buses for school transportation has been handled by various companies. This article features 10 school bus companies which made a name for themselves, when it came to redefining the way we look at a school bus. #1 WAYNE CORPORATION Topping our list of companies is Wayne Corporation. Though the company declared itself bankrupt and discontinued operation in 1992, the Wayne Corporation had played a vital role in the development of safe buses for school children. They were the first and foremost to introduce the concept of school buses for schools. Their innovation predates the famous yellow coloured buses which are widely used these days. www.trackschoolbus.com They introduced the horse drawn carts, including kid hacks, which later evolved into automobiles which used full metal body chassis. Wayne Corporation introduced guard rails on the sides of all school buses, inboard wheelchair lifts, and even high-headroom doors. They were the first with a school bus based upon a cutaway van chassis, the Wayne Busette. This chassis design is still one of the most popular in North American markets even after more than 35 years. #2 BLUE BIRD An all time giant, the Blue Bird Corporation (formerly called Blue Bird Body Company) is clearly one of the top school bus manufacturing companies even today. Blue Bird's corporate headquarters and main manufacturing facilities are in Georgia. www.trackschoolbus.com It was in 1937 that the company began production of full-steel bus bodies. This innovation would soon replace the wooden bodies which were commonly used in the United States. -

Standardized Parent Company Names for TRI Reporting

Standardized Parent Company Names for TRI Reporting This alphabetized list of TRI Reporting Year (RY) 2010 Parent Company names is provided here as a reference for facilities filing their RY 2011 reports using paper forms. For RY2011, the Agency is emphasizing the importance of accurate names for Parent Companies. Your facility may or may not have a Parent Company. Also, if you do have a Parent Company, please note that it is not necessarily listed here. Instructions Search for your standardized company name by pressing the CTRL+F keys. If your Parent Company is on this list, please write the name exactly as spelled and abbreviated here in Section 5.1 of the appropriate TRI Reporting Form. If your Parent Company is not on this list, please clearly write out the name of your parent company. In either case, please use ALL CAPITAL letters and DO NOT use periods. Please consult the most recent TRI Reporting Forms and Instructions (http://www.epa.gov/tri/report/index.htm) if you need additional information on reporting for reporting Parent Company names. Find your standardized company name on the alphabetical list below, or search for a name by pressing the CTRL+F keys Standardized Parent Company Names 3A COMPOSITES USA INC 3M CO 4-D CORROSION CONTROL SPECIALISTS INC 50% DAIRY FARMERS OF AMERICA 50% PRAIRIE FARM 88TH REGIONAL SUPPORT COMMAND A & A MANUFACTURING CO INC A & A READY MIX INC A & E INC A G SIMPSON AUTOMOTIVE INC A KEY 3 CASTING CO A MATRIX METALS CO LLC A O SMITH CORP A RAYMOND TINNERMAN MANUFACTURING INC A SCHULMAN INC A TEICHERT -

NTSB Executive Summary

NATIONAL TRANSPORTATION SAFETY BOARD Public Meeting of May 22, 2018 (Information subject to editing) Special Investigation Report School Bus Transportation Safety, Baltimore, Maryland, November 1, 2016, and Chattanooga, Tennessee, November 21, 2016 NTSB/SIR-18/02 This is a synopsis from the NTSB’s report and does not include the Board’s rationale for the conclusions, probable cause, and safety recommendations. NTSB staff is currently making final revisions to the report from which the attached conclusions and safety recommendations have been extracted. The final report and pertinent safety recommendation letters will be distributed to recommendation recipients as soon as possible. The attached information is subject to further review and editing to reflect changes adopted during the Board meeting. Executive Summary School bus travel is one of the safest forms of transportation in the United States. Every day, nearly 600,000 buses carry more than 25 million students to and from school and activities. Children are safer traveling in school buses than in any other vehicle. Although school buses are extremely safe, the National Transportation Safety Board (NTSB) continues to investigate school bus crashes in which fatalities and injuries occur. Improved oversight of school bus drivers and enhancements to school bus design—such as installation of passenger lap/shoulder belts, electronic stability control, and automatic emergency braking—could prevent or mitigate such crash outcomes. In November 2016, the NTSB began the investigation of two multifatality crashes involving school buses. Each crash was initiated when the driver lost control of the school bus. In the November 1 crash in Baltimore, Maryland, the driver was epileptic and suffered a seizure.