Independent Auditor's Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Notes to Financial Statements

Digital for all Notes to financial statements 46. Auditors’ Remuneration (` Millions) For the year ended For the year ended Particulars March 31, 2015 March 31, 2014 - Audit Fee* 68 68 - Reimbursement of Expenses* 5 5 - As advisor for taxation matters* - - - Other Services* 8 11 Total 81 84 * Excluding Service Tax 47. Details of dues to micro and small enterprises as defined under the MSMED Act, 2006 Amounts due to micro and small enterprises under Micro, Small and Medium Enterprises Development (MSMED) Act, 2006 aggregate to ` 10 Mn (March 31, 2014 – ` 38 Mn) based on the information available with the Company and the confirmation obtained from the creditors. (` Millions) Sr No Particulars March 31, 2015 March 31, 2014 1 The principal amount and the interest due thereon [` Nil (March 31, 10 38 2014 – ` Nil)] remaining unpaid to any supplier as at the end of each accounting year 2 The amount of interest paid by the buyer in terms of section 16 of - - the MSMED Act, 2006, along with the amounts of the payment made to the supplier beyond the appointed day during each accounting year 3 The amount of interest due and payable for the period of delay in - - making payment (which have been paid but beyond the appointed day during the year) but without adding the interest specified under MSMED Act, 2006. 4 The amount of interest accrued and remaining unpaid at the end of - - each accounting year; 5 The amount of further interest remaining due and payable even - - in the succeeding years, until such date when the interest dues as above are actually paid to the small enterprise for the purpose of disallowance as a deductible expenditure under section 23 of the MSMED Act, 2006. -

Notes to Consolidated Financial Statements 40. Companies

Digital for all Notes to consolidated financial statements 40. Companies in the Group, Joint Ventures and Associates The Group conducts its business through Bharti Airtel and its directly and indirectly held subsidiaries, joint ventures and associates. Information about the composition of the Group is as follows:- S. No. Principal Activity Principal place of operation / Number of wholly-owned country of incorporation subsidiaries As of As of March 31, 2015 March 31, 2014 1 Telecommunication services Africa 10 10 2 Telecommunication services India 4 3 3 Telecommunication services South Asia 2 2 4 Telecommunication services Other 7 7 5 Mobile commerce services Africa 17 17 6 Mobile commerce services India 1 1 7 Infrastructure services Africa 9 10 8 Infrastructure services South Asia 2 2 9 Investment company Africa 3 3 10 Investment company Netherlands 25 27 11 Investment company Mauritius 6 6 12 Investment company Other 2 2 13 Direct to Home services Africa 3 5 14 Submarine cable system Mauritius 1 1 15 Holding, finance services and Netherlands 1 1 management services 16 Other India 1 1 94 98 S. No. Principal Activity Principal place of operation / Number of Non-wholly-owned country of incorporation subsidiaries As of As of March 31, 2015 March 31, 2014 1 Telecommunication services Africa 9 9 2 Telecommunication services India 1 1 3 Infrastructure services India 2 2 4 Infrastructure services Africa 7 7 5 Direct to Home services India 1 1 20 20 266 Annual Report 2014-15 Corporate OverviewStatutory Reports FINANCIAL Financial Statements STATEMENTS Bharti Airtel Limited Notes to consolidated financial statements Additionally the Group also controls the trusts as mentioned in Note 40(b) below. -

Telecoms Renewable Energy Vendors/Escos Landscape in Bangladesh Bangladesh Vendor Directory GSMA Mobile for Development Green Power for Mobile

In partnership with the Netherlands Telecoms Renewable Energy Vendors/ESCOs Landscape in Bangladesh Bangladesh Vendor Directory GSMA Mobile for Development Green Power for Mobile Contents Company Page Introduction Applied Solar Technologies (AST) 1 Ballard Power Systems 2 BGMP 3 EBI 4 Electro Solar Power Limited 5 Eltek 6 Engreen Ltd 7 Ericsson 8 Heliocentris Industry GmbH 9 Huawei Hybrid Power – PowerCube 10 InGen 11 NextGen 12 NorthStar Battery 13 Rahimafrooz Renewable Energy 14 Southwest Windpower 15 Bangladesh Vendor Directory GSMA Mobile for Development Green Power for Mobile Introduction The Green Power for Mobile (GPM) At the same time government of Bangladesh has driven financial programme to promote green technology in telecom by offering a 15% Programme was launched in 2008 by Value Added Tax exemption for all renewable energy equipment and GSMA to promote the use of renewable related raw material as well. Since mid-2012, the GPM team has led Bangladesh-specific activities energy technology and solutions by and conducted one country-focused working group in Dhaka in October telecom Industry. The programme is 2012. Bangladesh, with an electrification rate of below 50%, has limited 1 supported by the International Finance the telecom industry’s delivery of power to their base station . This document presents a summary of the power situation in Corporation (IFC) and partners with the Bangladesh, listing the main vendors/service providers that operate Government of the Netherlands. or have interests in the Bangladeshi telecom market. 1 Power Division – www.powerdivision.gov.bd Bangladesh Vendor Directory GSMA Mobile for Development Green Power for Mobile Figure 1: Subscriber Growth in Bangladesh Telecom Market Figure 1. -

Robi-Airtel Merger

A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger i A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger Internship Report A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger Submitted to: Mr. Fairuz Chowdhury Lecturer BRAC Business School BRAC University Submitted by: Jainul Abedin ID: 13204034 BUS 400 BRAC Business School BRAC University Date of Submission ii A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger Letter of Transmittal , 2016 Fairuz Chowdhury Lecturer, BRAC Business School, BRAC University Mohakhali, Dhaka Subject: Submission of Internship Report Dear Sir, I am here by submitting my Internship Report on “A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger” which is a part of the BBA program curriculum. Besides, I also include about my experience on the project regarding “cheque collection and monitoring “in Robi Axiatra Limited in FAMR unit under Finance Division for 3 months, under the supervision of Enamul Haque, General Manager, Finance division. I, therefore hope and pray that you are kind enough to receive this report and provide your valuable judgment. And also it would be pleasure for me if you find this report helpful. Sincerely, Jainul Abedin ID: 13204034 iii A study on the recent challenges of the telecommunication sector in Bangladesh: Robi-Airtel merger ACKNOWLEDGEMENT Firstly, I am thankful to Almighty ALLAH for giving me the opportunity to work with a MNC as an Intern and also Robi Axiata ltd for selecting me. -

CORE View Metadata, Citation and Similar Papers at Core.Ac.Uk

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by BRAC University Institutional Repository INTERNSHIP REPORT On “Critical Evaluation of Sales & Distribution Department of Airtel Bangladesh Limited” COURSE: Internship [BUS 400] SUBMITTED TO: Mr. ARIF GHANI LECTURER - II BRAC BUSINESS SCHOOL BRAC UNIVERSITY PREPARED BY: TAMIM AHMED CHOWDHURY ID: 10204131 BRAC BUSINESS SCHOOL BRAC UNIVERSITY Date of Submission: 28th June, 2015 ii Letter of Transmittal 28th June, 2015 Arif Ghani Lecturer-II BRAC Business School BRAC University Subject: Submission of Internship Report Dear Sir, Enclosed is a copy of my internship report of the four month period I have been working as an intern at Airtel Bangladesh Limited. The title of the report is ‘Critical Evaluation of Sales and Distribution Department of Airtel Bangladesh Limited’ and has been prepared since submission of an Internship Report is a mandatory partial requirement for the successful completion of my Bachelor of Business Administration Degree. In this report, I have tried my best to bring up all the necessary details that were assigned to me. I have tried to apply my learning from courses as well as my experience as an intern to make this report more enriched. I express my gratitude to you for letting me work on this topic and I hope that this report will meet your expectations. Moreover, I will be pleased to clarify and answer doubts regarding discrepancies or inconsistencies that may have presented itself in the report. Thank you. Sincerely yours, Tamim Ahmed Chowdhury ID# 10204131 BRAC Business School BRAC University iii Acknowledgement This report would not be accomplished without the generous contributions of any individuals and organizations. -

Salient Features of the Financial Statement of Subsidiaries

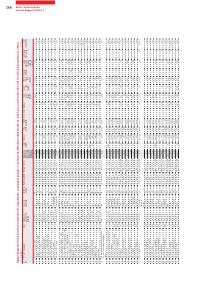

Bharti Airtel Limited Annual Report 2016–17 268 Salient features of the financial statement of subsidiaries, associates and joint ventures for the year ended March 31, 2017, pursuant to Section 129 (3) of the Companies Act 2013. Part A - Subsidiaries (` Millions) S. Name of the Subsidiary Note Date on which Country of Reporting Reporting Period Financial Year End Exchange Share Reserves Total Total Investments* Turnover Profit/ Provision Profit/ Proposed Capital Community % of No. subsidiary was Registration Currency Rate as of Capital Assets Liabilities (Loss) for (Loss) Dividend Expenditure Contribution shareholding acquired March 31, Before Taxation After during the ^ 2017 Taxation Taxation reporting period # 1 Airtel Payments Bank Limited a, i April 1, 2010 India INR Apr '16 to Mar '17 March 31, 2017 1.000 9,944 (5,018) 8,811 3,885 - 264 (2,443) - (2,443) - 19 - 80.10% 2 Bangladesh Infratel Networks Limited e June 26, 2011 Bangladesh BDT Apr '16 to Mar '17 March 31, 2017 0.807 - - - - - - - - - - - - 100% 3 Bharti Airtel (France) SAS b June 9, 2010 France EUR Apr '16 to Mar '17 March 31, 2017 69.344 1 160 924 763 - 756 91 30 61 - 149 - 100% 4 Bharti Airtel (Hongkong) Limited b October 12, 2006 Hongkong HKD Apr '16 to Mar '17 March 31, 2017 8.348 41 (163) 410 532 - 529 78 13 65 - 13 - 100% 5 Bharti Airtel (Japan) Kabushiki Kaisha b, d April 5, 2010 Japan JPY Apr '16 to Mar '17 March 31, 2017 0.582 0 0 0 0 - 0 0 0 0 - - - 100% 6 Bharti Airtel Services Limited b March 26, 2001 India INR Apr '16 to Mar '17 March 31, 2017 1.000 1 (1,010) -

7Udqvirupdwlrqdo 1Hwzrun

352 6WDWHPHQW3XUVXDQWWR6HFWLRQRIWKH&RPSDQLHV$FWUHODWLQJWRVXEVLGLDU\FRPSDQLHVIRUWKH\HDUHQGHG0DUFK (` Millions) Sr Name of the Subsidiary Note Country of Reporting Reporting Period Financial Year End Exchange Share Reserves Total Total Investments* Turnover 3URǂW Provision 3URǂW Capital Community % of Annual Report 2015-16 No. Registration Currency Rate as Capital Assets Liabilities (Loss) for (Loss) Proposed Expenditure Contribution ^ shareholding of March Before Taxation After Dividend during the 31, 2016 Taxation Taxation reporting period # 1 Airtel Bangladesh Limited a Bangladesh BDT Apr '15 to Mar '16 0DUFK 0.845 - 38 - 100% 2 Airtel Payments Bank Limited DM India INR Apr '15 to Mar '16 0DUFK 1.000 - 395 (346) - (346) 139 80.10% 3 Bangladesh Infratel Networks Limited EH Bangladesh BDT Apr '15 to Mar '16 0DUFK 0.845 0 (0) 0 0 - - (0) - (0) - 100% 4 Bharti Airtel (France) SAS b France EUR Apr '15 to Mar '16 0DUFK 75.447 1 32 340 307 272 77 97 (20) 183 100% 5 Bharti Airtel (Hongkong) Limited a Hongkong +.' Apr '15 to Mar '16 0DUFK 8.540 42 (225) 546 729 575 140 5 135 172 100% 6 %KDUWL$LUWHO -DSDQ .DEXVKLNL.DLVKD DG -DSDQ -3< Apr '15 to Mar '16 0DUFK 0.590 0 (6) 19 25 8 (18) (0) (18) - 100% 7 Bharti Airtel Services Limited a India INR Apr '15 to Mar '16 0DUFK 1.000 1 - (62) 3 (65) 183 100% 8 %KDUWL$LUWHO 8. /LPLWHG a 8QLWHG.LQJGRP GBP Apr '15 to Mar '16 0DUFK 95.411 32 498 (154) (30) (124) 150 100% 9 Bharti Airtel (USA) Limited DG United States of USD Apr '15 to Mar '16 0DUFK 66.255 - 219 292 (115) 407 97 100% -

Samena Trends Exclusively for Samena Telecommunications Council's Members Building Digital Economies

Volume 07 _ Issue 01 _ Jan 2016 SAMENA TRENDS EXCLUSIVELY FOR SAMENA TELECOMMUNICATIONS COUNCIL'S MEMBERS BUILDING DIGITAL ECONOMIES A SAMENA Telecommunications Council Newsletter Articles Mobile money Page 67 Low earth orbit satellite broadband makes a comeback Page 78 Exclusive Interview Prof. Dr. Ensar GÜL General Manager Türksat A.Ş Page 04 The future of satellite broadband and the need for innovative spectrum management solutions www.samenacouncil.org SAMENA CONTENTS VOLUME _ 07 _ISSUE _ 01_jan 2016 TRENDS The SAMENA TRENDS newsletter is wholly owned and operated by The SAMENA Telecommunications Council FZ, LLC REGIONAL & MEMBERS (SAMENA Council). Information in the UPDATES newsletter is not intended as professional 08. Members news services advice, and SAMENA Council disclaims any liability for use of specific 15. Regional news information or results thereof. Articles and information contained in this publication are the copyright of SAMENA REGULATORY & POLICY Telecommunications Council, (unless UPDATES otherwise noted, described or stated) 22. Regulatory news and cannot be reproduced, copied or printed in any form without the express 31. A snapshot of regulatory activities in written permission of the publisher. SAMENA region The SAMENA Council does not necessar- ily endorse, support, sanction, encour- 42. Regulatory activities beyond the age, verify or agree with the content, SAMENA region comments, opinions or statements made in The SAMENA TRENDS by any entity WHOLESALE UPDATES or entities. Information, products and 55. Wholesale news services offered, sold or placed in the newsletter by other than The SAMENA Council belong to the respective entity TECHNOLOGY UPDATES or entities and are not representative 59. Technology news of The SAMENA Council. -

Standalone Financial Statements

Inside this Report 03 Enriching Lives in the Digital Era 10 Revisiting an Exciting Year 22 Board of Directors 04 Strategic Framework 12 Message from Chairman 24 Awards & Accolades 05 Intrinsic Strengths to Deliver Value 14 Message from MD & CEO (India & 26 Corporate Social Responsibility 06 Our Performance South Asia) & Sustainability 08 A Life-enrichment Network 15 Message from MD & CEO (Africa) 09 Product Performance 16 Digital for all Enriching lives in the Intrinsic strengths to Our Performance digital era deliver value Mn+ ` Bn MMoobbilee oppeerratoor ggloobaallyy CCoonsnsoollidattedd suubssccrribbeerss RReevvennuue in 20115 (in tteerrmms ooff subssccribbeer bbaasee) aaccrroossss vaarrioous bussinnessssees inn (bbaassed on cconsooliddatteedd Innddiaa, Soouutth Assiia aannd AAfriccaa innccoommee sttaateemeent) % % % Y-o-Y ooff thhee addddreesssabble pooppuullattioion TToottaal ssppeecctrrumm PAAT ggrroowwtth (in 2200 coouunttriies) is connnneectteed mmaarrkkeett shharre tthhrroough AAiirrteel neetwwork Pg-3Pg-5 Pg-6 36 Business Responsibility Report 119 Standalone Financial Statements 278 Circle Offices 48 Board’s Report with Auditors’ Report 78 Management Discussion 186 Consolidated Financial Statements and Analysis with Auditors’ Report 96 Report on Corporate Governance 273 Statement Pursuant to Section 129 of the Companies Act, 2013 DigitalDDiggiiDigitaltat gl forfor allalforf lr AllAlA l We believe, this is a key moment in human history, when the digital landscape is shaping all aspects of life. From global trade and commerce to education, entertainment, healthcare and governance; and so on. As the digital universe continues to expand with the help of intuitive and all-pervasive technology, telecommunication is witnessing an unprecedented transformation. WWe devvotedd ourr asssets This is how we annd ttallentt to caateer to responded to this thhe eemeergiinng neeeeds of coounntriies aaccrosss Asia tectonic shift during annd AAfrricaa. -

Abridged Annual Report Bharti Airtel Limited Creating a Digitally Connected World Board of Directors

2017-18 Abridged Annual Report Bharti Airtel Limited Creating a digitally connected world Board of Directors Mr. Sunil Bharti Mittal Mr. Ben Verwaayen Mr. Manish Kejriwal Chairman Independent Director Independent Director Mr. Rakesh Bharti Mittal Ms. Chua Sock Koong Mr. Craig Edward Ehrlich Non-Executive Director Non-Executive Director Independent Director Mr. Shishir Priyadarshi Ms. Tan Yong Choo Mr. D. K. Mittal Independent Director Non-Executive Director Independent Director Mr. Gopal Vittal Mr. V. K. Viswanathan MD & CEO (India & South Asia) Independent Director Chairman Member Committees Audit Committee Risk Management Committee HR & Nomination Committee Stakeholders’ Relationship Committee Corporate Social Responsibility Committee Committee of Directors Read Inside 16 Statutory 53 Reports 16 Board’s Report 25 Management Discussion and Analysis 02 Corporate 15 Overview 02 Corporate Information 54 Financial 03 Performance Highlights 123 Statements 04 Message from the Chairman 54 Abridged Standalone Financial Statements 06 Message from Managing Director & CEO (India & South Asia) 81 Abridged Consolidated Financial Statements 07 Message from Managing Director & CEO (Africa) 119 Statement Pursuant to Section 129 of the Companies Act, 2013 08 Corporate Social Responsibility Report Bharti Airtel Limited Abridged Annual Report 2017-18 Corporate Information Board of Directors Statutory Auditors Mr. Sunil Bharti Mittal, Chairman Deloitte Haskins & Sells LLP Mr. Ben Verwaayen Chartered Accountants Ms. Chua Sock Koong Mr. Craig Edward Ehrlich Internal Assurance Partners Mr. Dinesh Kumar Mittal Ernst & Young LLP Mr. Manish Kejriwal ANB & Co., Chartered Accountants Mr. Rakesh Bharti Mittal Mr. Shishir Priyadarshi Cost Auditors Ms. Tan Yong Choo R.J. Goel & Co. Mr. V. K. Viswanathan Cost Accountants Mr. Gopal Vittal, Managing Director & CEO (India & South Asia) Secretarial Auditors Managing Director & CEO (Africa) Chandrasekaran Associates Company Secretaries Bharti Airtel International (Netherlands) B.V. -

Board's Report

Transformational Network Board’s Report Dear Members, Consolidated Financial Highlights (IGAAP) Your Directors have pleasure in presenting the 21st Board FY 2015-16 FY 2014-15 Report on the Company’s business and operations, together Particulars ` USD ` USD ZLWK DXGLWHG njQDQFLDO VWDWHPHQWV DQG DFFRXQWV IRU WKH Millions Millions* Millions Millions* njQDQFLDO\HDUHQGHG0DUFK Gross revenue 1,009,373 15,415 961,007 15,728 EBITDA before 378,133 5,775 356,978 5,872 Company Overview exceptional Bharti Airtel is among the top three mobile service providers items globally with presence in 20 countries, including India, &DVKSURǟWIURP 291,115 4,446 312,513 5,115 Sri Lanka, Bangladesh and 17 countries in the African operations continent. Earnings before 106,677 1,629 105,398 1,725 taxation 7KH &RPSDQ\šV GLYHUVLnjHG VHUYLFH UDQJH LQFOXGHV PRELOH Net Income / 44,566 680 46,208 756 voice and data solutions, using 2G, 3G and 4G technologies. (Loss) Its service portfolio comprises an integrated suite of telecom * 1 USD = `([FKDQJH5DWHIRUWKHnjQDQFLDO\HDUHQGHG0DUFK solutions to its customers, besides providing long-distance (1 USD = `([FKDQJH5DWHIRUWKHnjQDQFLDO\HDUHQGHG0DUFK connectivity in India, Africa and the rest of the world. The &RPSDQ\DOVRRNjHUV'LJLWDO79DQG,379VHUYLFHVLQ,QGLD Consolidated Financial Highlights (IFRS) $OOWKHVHVHUYLFHVDUHUHQGHUHGXQGHUDXQLnjHGEUDQGŠDLUWHOš FY 2015-16 FY 2014-15 either directly or through subsidiary companies. Particulars ` USD ` USD The Company also deploys and manages passive Millions Millions* Millions Millions* infrastructure pertaining to telecom operations through Gross revenue 965,321 14,742 920,394 15,064 its subsidiary, Bharti Infratel Limited, which also owns EBITDA before 341,902 5,222 314,517 5,148 42% of Indus Towers Limited. -

Skill Development

The in-house magazine of Bharti Enterprises VOL-19 . ISSUE 2 . 2015 HARNESSING POTENTIAL THROUGH SKILL DEVELOPMENT CENTUM LEARNING CHairman’sNOTE Dear Colleagues, t’s heartening to see the way Centum Learning, our In a strategic rejig of our business portfolio, we have skill development and vocational training venture has agreed to merge Bharti Retail, our wholly owned Ishaped up over the years, staying true to its vision of subsidiary in the retail sector, with Future Group’s ‘Enabling sustainable transformation through learning Future Retail to create one of India’s largest organised and skills development’. Within a few years of inception, retail networks. the Company has emerged as a leading organisation in the skilling sector having already transformed the lives of Bharti Airtel crossed a major landmark in its journey over 1.2 million people in 21 countries in Asia and Africa. when London based World Cellular Information Service (WCIS) acknowledged Airtel as the third Driven by our abiding vision to bridge the digital largest mobile operator in the world with 303 million divide we recently acquired a strategic minority stake subscribers across its operations in Asia and Africa. in ‘OneWeb’, a satellite based communication project But beyond the numbers, what really matters to us is to drive internet penetration in rural and unconnected the deep transformational impact that Airtel is having areas of the world. We believe the project will greatly on the lives of people and society at large through complement the efforts of Governments and telecom our innovative business model. As we move on we will operators across the globe to take internet to the masses continue with our quest for new initiatives with wider particularly in the developing and emerging markets of potential.