Statements on Compliance of Frbma to Be Attached to Budget Documents 2007-08

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Army Major Injured in Attack by Suspected NSCN

WWW.EASTERNMIRRORNAGALAND.COM EASTERN MIRROR Woody Allen allegations should Court summons Tharoor as accused be looked into again, says Swiss right-back Lichtsteiner in Sunanda Pushkar death case | P8 Penelope Cruz | P10 signs for Arsenal | P12 NATION ENTERTAINMENT SPORT VOL. XVII NO. 153 | PAGES 12 ` 5/- RNI NO. NAGENG/2002/07906 DIMAPUR, WEDNESDAY, JUNE 6, 2018 ‘Back to our roots for a sustainable village economy’ Army major injured State government planning on declaring Nagaland an organic state soon Our Correspondent also promote, preserve and two piglets, and in the event Kohima, June 5 (EMN): With sustain in a refined way the of successful breeding and the concept of ‘back to our cultural and traditional way reproduction they will make roots’, the Northern Angami of Naga life. contribution to the society in attack by suspected Chükehie Society (NACS) Under this project, Kie- for further chain of distribu- has introduced a project whuo said it will promote tion by the society. called ‘village economic livestock and poultry back- Each beneficiary in development’ which seeks yard farming, paddy field poultry sector will be given NSCN (K) members to take back the people to (aqua) fish farming, pro- twenty chicks along with ‘the roots’ towards rebuild- mote organic agriculture free fodder for one month ing the village economy farming, especially crops while 20 saplings of grafted The attack was carried out at around 2.20 am when traditionally on livestock with GI tagging viz. Naga lemon tree will be given to militants fired a barrage of shots targeting a ‘Charlie farming, poultry farming, King chilly and tree tomato, each beneficiary for early traditional handicraft, han- established market linkages, harvesting of fruits and 25 company’ of the 41 Assam Rifles at Lempong Shingha in dloom, traditional bamboo provide transportation fa- saplings of Avocado fruit for eastern Nagaland’s Mon district. -

6Th Sem Results

Result Gazette Of Nagaland University Three Years Under Graduate Final Semester Examination 2019 Overall Pass Percentage Total Appeared : 8457 Total Passed : 6161 Pass Percentage : 72.85 Page 2 of 263 6 th Semester Examination B.A. GENERAL Total Appeared 2783 Total Passed : 1796 Passed Percent 64.53% 6 th Semester Examination B.A. HONOURS Total Appeared 4197 Total Passed : 3303 Passed Percent 78.70% Page 3 of 263 6 th Semester Examination BBA GENERAL Total Appeared 33 Total Passed : 32 Passed Percent 96.97% Page 4 of 263 6 th Semester Examination B.Com. GENERAL Total Appeared 180 Total Passed : 87 Passed Percent 48.33% 6 th Semester Examination B.Com. HONOURS Total Appeared 767 Total Passed : 529 Passed Percent 68.97% Page 5 of 263 6 th Semester Examination B.Sc. GENERAL Total Appeared 34 Total Passed : 25 Passed Percent 73.53% 6 th Semester Examination B.Sc. HONOURS Total Appeared 463 Total Passed : 389 Passed Percent 84.02% Page 6 of 263 TOPPER LIST, UNDER-GRADUATE EXAMINATION 2019 SL. COURSE HONOURS COLLEGE ROLL NO STUDENT NAME COURSE CGPA NO CATEGORY SUBJECT NAME PHALNEIHOI THEPFÜSONO SAZOLIE COLLEGE, 1. AH16040006 BA HON EDN 6.48 HANGSING JOTSOMA ST. JOSEPHS’COLLEGE 2. AH16010487 KEDOSENO RINO BA HON HIS 6.87 JAKHAMA TETSO COLLEGE, 3. AH16150132 WINSOME SITLHOU BA HON ENG 6.84 DIMAPUR FAZL ALI COLLEGE, 4. AH16350091 MOASENLA BA HON GEOG 6.31 MOKOKCHUNG DON BOSCO COLLEGE, 5. AH16530104 WATISANGLA AO BA HON POL 6.94 KOHIMA JAPFU CHRISTIAN 6. AH16020013 PENLI AIER BA HON ECO 6.68 COLLEGE, KIGWEMA ORIENTAL COLLEGE, 7. -

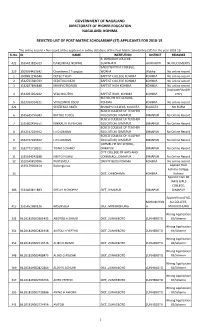

Kohima Rejected List of Post

GOVERNMENT OF NAGALAND DIRECTORATE OF HIGHER EDUCATION NAGALAND: KOHIMA REJECTED LIST OF POST MATRIC SCHOLARSHIP (ST) APPLICANTS FOR 2018-19. *No online record-> No record of the applicant in online database of the Post Matric Scholarship (ST) for the year 2018-19. Sl.No. ID NAME INSTITUTION DISTRICT REMARKS B. BOROOAH COLLEGE, 422 1535431825019 ISAKEURAILE NEWME GUWAHATI GUWAHATI NO DOCUMENTS BAILEY BAPTIST COLLEGE, 323 1509094429642 Chandemo Z Tsanglao WOKHA Wokha No online record 1 1508851196546 DETSO THOPI BAPTIST COLLEGE KOHIMA KOHIMA No online record 2 1532765580709 SEZOTOLU KEZO BAPTIST COLLEGE KOHIMA KOHIMA No online record 3 1532877896848 KHRIEVOTSONUO BAPTIST HIGH KOHIMA KOHIMA No online record Duplicate/double 4 1534091262102 VELO NGOTHA BAPTIST HIGH, KOHIMA KOHIMA entry BETHEL HR SEC SCHOOL, 5 1529390914221 VIVOZONUO USOU KOHIMA KOHIMA No online record 421 SENTIENLA AMER BISHOP'S COLLEGE, KOLKATA KOLKATA NO FORM BOSCO COLLEGE OF TEACHER 6 1535635750049 INATOLI TUCCU EDUCATION, DIMAPUR DIMAPUR No Online Record BOSCO COLLEGE OF TEACHER 7 1535602434551 KINIKALI K YEPTHOMI EDUCATION, DIMAPUR DIMAPUR No Online Record BOSCO COLLEGE OF TEACHER 8 1532747229392 LITO AWOMI EDUCATION, DIMAPUR DIMAPUR No Online Record BOSCO COLLEGE OF TEACHER 9 1532747229392 LITO AWOMI EDUCATION, DIMAPUR DIMAPUR No Online Record CARMEL HR SEC SCHOOL, 10 1532772718321 TOINO S ZHIMO DIMAPUR DIMAPUR No Online Record CITY COLLEGE OF ARTS AND 11 1535634243188 NIKITO N SWU COMMERCE, DIMAPUR DIMAPUR No Online Record 12 1510549819996 PURTEMSU DAINTY BUDS KOHIMA -

Nagaland University Exam Result.Pdf

A central University Estd by the Parliament No. 35 of 1989 HEADQUARTERS: LUMAMI: 798627 No. NU/Ex-43/95 Date: Lumami, 09-06-2012 RESULT NOTIFICATION The Vice Chancellor, Nagaland University is pleased to declare the provisional results of B. A 3 - Year General examinations held during February - March 2012 as follows 2009 Batch GENERAL (REGULAR) Total students appeared : 265 Total students passed : 118 Pass percentage (%) : 44.53 2009 Batch 6/10/2012 Page 1 of 14 First Second Simple Pass Total appeared Total Passed Division Division Pass percentage (%) Oriental College 1 0 0.00 Asian Institute of Hr. Education & 1 0 0.00 Research Pfütsero College 1 0 0.00 Loyem Memorial College 1 0 0.00 Mountain View Christian College 1 1 1 100.00 St. Xavier College 1 1 1 100.00 Bailey Baptist College 1 1 1 100.00 Mt. Tiyi College 1 1 1 100.00 S.D. Jain Girls` College 2 1 1 50.00 Tuli College 2 1 1 50.00 Immanuel College 2 1 1 50.00 Japfü Christian College 3 1 2 3 100.00 Peren Government College 4 0 0.00 Zisaji Presidency College 4 1 1 25.00 City College of Arts and Commerce 4 1 2 3 75.00 Yingli College 5 0 0.00 Unity College 5 2 2 40.00 Sazolie College 5 2 2 4 80.00 Pranabananda Women`s College 6 1 1 16.67 St. John College 6 1 1 2 33.33 Capital College of Higher Education 6 3 3 50.00 Salesian College of Higher Education 6 4 4 66.67 Phek Government College 8 3 3 37.50 Tetso College 9 3 3 33.33 Fazl Ali College 9 1 2 3 33.33 Sao Chang College 10 3 3 6 60.00 Zunheboto Government College 10 7 7 70.00 Dimapur Government College 16 1 8 9 56.25 Alder College -

Kohima Rejected List of State Merit Scholarship 2020-21 1

GOVERNMENT OF NAGALAND DIRECTORATE OF HIGHER EDUCATION NAGALAND: KOHIMA REJECTED LIST OF STATE MERIT SCHOLARSHIP 2020-21 SL.NO. TRANSACTION ID NAME INSTITUTION REMARKS BA 3rd Sem Marksheet Not 1 MRT2039783 Oienla Jamir Adamas University Enclosed 2 MRT2022857 Ase Y Sangtam Alder College, Kohima 3rd Sem Marksheet Not Enclosed BA 1st Sem Marksheet Not 3 MRT2013389 Qhetoka Assumi Brm Govt.Law College Enclosed 4 MRT2053431 Senulu Tetseo Capital College, Kohima BA 2nd Yr Below 70% 5 MRT2024018 Sunepinla Capital College, Kohima BA 1st Yr Below 70% Ba 1st Sem Marksheet Not 6 MRT2014072 Surhohulu Venuh Capital College, Kohima Enclosed 7 MRT2016064 Mharoni Lotha Carmel Hr Sec School, Dimapur Below 80 % Christian Institute Of Health Science And 8 MRT2056002 Lirhoni M Kikon Research (Cihsr) Below 70% Study Break More Than 2 Yers. Last Exam Passed Marksheet 9 MRT2063734 Kadilungbo City Law College, Dimapur 2017. College Of Agriculture Engineering & Post 10 MRT2013121 Ghunaka H Yeptho Harvest Technology Below 70% College Of Fisheries, Assam Agriculture 11 MRT2054016 Kushen P Khiamniungan University Below 80 % 12 MRT2032254 Bisaliba Sangtam Cornerstone College, Dimapur 3Rd Sem Marksheet Not Enclosed No Admission Reciept & 13 MRT2019520 Thol Nokusunu Solesiil D.B.J. College Institution Verification Form Beneficiary From Agriculture 14 MRT2048493 Meribemo Y Khuvung Day Scholar Department Delhi School Of Economics, Delhi 15 MRT2026045 Hurato Rhakho University. Below 70% 16 MRT2027480 P Imtiyala Kichu Dimapur Government College 3Rd Sem Marksheet Not Enclosed -

19 July 2019 Time: 11:00. Am Venue: Dept

NAGALAND UNIVERSITY (A Central University Estd. By the Act of Parliament No. 35 of 1989) Headquarters : Lumami – 798627 Department of Chemistry Date:17-07-2019 NOTIFICATION List of eligible candidates for the M.Sc. Chemistry entrance test Date: 19th July 2019 Time: 11:00. am Venue: Dept of Chemistry, Nagaland University, Lumami Campus For more information please check the earlier Departmental notification dated 16th July 2019. M.Sc. Chemistry Applicants 2019 Sl. Name Sex Category College Gen(G)/ No Hons (H) 1 MHADEMO Y M ST St. Joseph’s College Kohima. H KHUVUNG N.U 2 THUNGCHAMO M ST St. Joseph’s College Kohima. H JAMI N.U 3 AKALU H M ST St. John College Dimapur. N.U H SHOHE 4 VIEKHROLO-O F ST St. Joseph’s College Kohima. H KOZA N.U 5 ECHUNGBEMO M ST FAC Mokokchung N.U. H Z KIKON 6 PHITOVILI F ST St. Joseph’s College Kohima. H SUMI N.U 7 MHALO Y F ST FAC Mokokchung N.U. H NGULLY 8 MENGUKHRIE F ST Model Christian College H NUO KUOTSU 9 SANGANGTOL F ST St. Joseph’s College Kohima. H A A N.U 10 NIKILI K F ST St. Joseph’s College Kohima. H ZHIMO N.U 11 SATARUPA F OBC Moran College, H PRIYA Dibrugarh University DARSHINI 12 NUKSHA M ST St. John College Dimapur. N.U H 13 L. SUROTSABA M ST St. Joseph’s College Kohima. H SANGTAM N.U 14 MARY TEP F ST St. Joseph’s College Kohima. H N.U 15 NEKHRIIKHOLI F ST St. -

Contents a Quarterly News Letter of the COUNCIL of BAPTIST CHURCHES in NORTH EAST INDIA

Baptist News Contents A quarterly news letter of the COUNCIL OF BAPTIST CHURCHES IN NORTH EAST INDIA Editorial Column 2 Annual Report of the General Secretary 5 Annual Report of the Mission Secretary 19 Annual Report of the Finance Secretary 26 Annual Report of the Property Secretary 33 Annual Report of the Medical Secretary 36 Annual Report of the Justice and Peace 46 Annual Report of the Christian Literature Centre 50 Annual Report of Eastern Theological College 52 Annual Report of the North East Christian University 58 Annual Report of Assam Baptist Convention 68 Annual Report of Arunachal Baptist Church Council 72 Annual Report of Garo Baptist Convention 76 Annual Report of Manipur Baptist Convention 80 Annual Report of Nagaland Baptist Church Council 83 Annual Report of Karbi Anglong Baptist Convention 86 Annual Report of Baptist Youth Fellowship North East India 88 Annual Report of Baptist Women Fellowship North East India 89 69th Annual General Meeting 90 Pressing Towards Living the Fullness of Life 95 News Capsules 100 Biography 104 EDITORIAL BOARD: Circulation: Subscription: Jatin Gogoi One Year ` 150 (US$20) Editor: Rev Dr Akheto Sema Jinoy G. Sangma Two Years ` 250 (US$35) Asst Editor: Ms Ch Sweety Babul Boro Three Years ` 400 (US$50) JanitaApril Boro - June 2019Five Years ` 600 (US$80)1 Editorial Column The writer of Ecclesiastes said, “Everything that happens in this world happens at the time God chooses” (Eccles. 3:1). I believe the Council of Baptist Churches in North East India looked forward to a change of leadership in God’s appointed time and season. -

Kohima : Nagaland

Kohima : Nagaland (PROVISIONAL) 18000 16000 14000 12000 10000 Appeared 8000 Passed 6000 4000 2000 0 Arts Commerce Science Total HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2021 Email : [email protected] Websites : www.nbsenl.edu.in / www.nbsenagaland.com HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION, 2021 Contents 1. Notification No.42 1-2 2. Abstract of the Results 3-4 3. Merit list 5-7 4. Subject Toppers 8-10 5. Awards 11-13 6. Notification No. 43 14 7. Performance of Institution 15-28 8. Notification No.44 29-126 9. Arts Stream : 29-100 (a) Kohima 29-46 (b) Mokokchung 46-52 (c) Tuensang 52-55 (d) Mon 55-59 (e) Phek 59-62 (f) Wokha 63-65 (g) Zunheboto 65-68 (h) Dimapur 69-94 (i) Kiphire 94-95 (j) Longleng 96 (k) Peren 97-99 (l) Noklak 100 10. Commerce Stream : 101-110 (a) Kohima 101-103 (b) Mokokchung 103 (c) Tuensang 103 (d) Zunheboto 104 (e) Dimapur 104-110 (f) Peren 110 11. Science Stream : 111-126 (a) Kohima 111-115 (b) Mokokchung 115-116 (c) Tuensang 117 (d) Mon 117-118 (e) Phek 118 (f) Wokha 118 (g) Zunheboto 119 (h) Dimapur 119-126 NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA NOTIFICATION NO. 42/2021 Dated Kohima, the 20th July 2021 No.NBE-13/EX-12/2019-20 : 881 : The following rules/instructions are hereby published for information of all concerned : MARKSHEETS AND PASS CERTIFICATES : (a) The Centre Superintendents of the HSSLC 2021 only shall collect the marksheets and pass certificates of their students and the Centre Superintendent for other categories from 28 th July 2021. -

Higher Secondary School Leaving Certificate Examination 2010 Result

RESULT GAZETTE OF THE HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2010 (PROVISIONAL) Nagaland Board Of School Education P.B.NO.613, KOHIMA : NAGALAND Email : [email protected] Website : www.nbsenagaland.com NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2010 Contents Page No. 1. List of abbreviations 1 2. Notification No. 9/2010 (12) 2-3 3. Abstract of the Results 4-5 4. Merit list 6-8 5. Highest marks 9-11 6. Awards 12 7. Notification No. 10/2010 (12) 13 8. Performance of Institutions 14-19 9. Notification No. 11/2010 (12) 20-76 10. Arts Stream : (a) Dimapur 20-34 (b) Kohima 34-45 (c) Kiphire 45 (d) Longleng 46 (e) Mokokchung 46-50 (f ) Mon 50-51 (g) Peren 51-52 (h) Phek 52-54 (i ) Tuensang 54-55 (j ) Wokha 55-57 (k) Zunheboto 57-58 11. Commerce Stream : (a) Dimapur 59-64 (b) Kohima 64-65 (c) Mokokchung 65-66 (d) Peren 66 (e) Zunheboto 66 12. Science Stream : (a) Dimapur 67-71 (b) Kohima 71-74 (c) Mokokchung 74-75 (d) Mon 75 (e) Phek 75-76 (f ) Tuensang 76 (g) Wokha 76 (h) Zunheboto 76 1 NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2010 List of abbreviations used in this booklet : En : Number of candidates enrolled Ap : Number of candidates appeared Pa : Number of candidates passed Exp : Expelled ENG : English AEN : Alternative English AO : Ao SMI : Sumi LTA : Lotha TNY : Tenyidie BNG : Bengali HND : Hindi EDN : Education PSC : Political Science ECO : Economics HIS : History PSY : Psychology SGY : Sociology PHI : Philosophy GEO : Geography MSC : Music ACC : Accountancy BUS : Business Studies ENT : Entrepreneurship FBM : Fundamentals of Business Mathematics PHY : Physics MAT : Mathematics CHE : Chemistry BIO : Biology CSC : Computer Science INF : Informatics Practices Dated Kohima, (Mrs.Nini Meru) the 30th April 2010 Chairman 2 NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA NOTIFICATION NO. -

NBSE HSSLC Result

RESULT GAZETTE OF THE HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2012 (PROVISIONAL) Nagaland Board Of School Education P.B.NO.613, KOHIMA : NAGALAND Email : [email protected] Website : www.nbsenagaland.com NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2012 Contents Page No. 1. List of abbreviations 1 2. Notification No.3 /2012 (12) 2-3 3. Abstract of the Results 4-5 4. Merit list 6-8 5. Subject Toppers 9-10 6. Awards 11 7. Notification No.4 /2012 (12) 12 8. Performance of Institutions 13-18 9. Notification No.5 /2012 (12) 19-74 10. Arts Stream : 19-54 (a) Dimapur 19-31 (b) Kohima 31-42 (c) Kiphire 42-43 (d) Longleng 43 (e) Mokokchung 43-46 (f ) Mon 46-48 (g) Peren 48-49 (h) Phek 49-50 (i ) Tuensang 51 (j ) Wokha 52-53 (k) Zunheboto 53-54 11. Commerce Stream : 55-61 (a) Dimapur 55-59 (b) Kohima 59-61 (c) Mokokchung 61 (d) Peren 61 (e) Zunheboto 61 12. Science Stream : 62-74 (a) Dimapur 62-67 (b) Kohima 67-72 (c) Mokokchung 72-73 (d) Mon 73 (e) Phek 73 (f ) Tuensang 74 (g) Wokha 74 (h) Zunheboto 74 1 NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA HIGHER SECONDARY SCHOOL LEAVING CERTIFICATE EXAMINATION 2012 List of abbreviations used in this booklet : En : Number of candidates enrolled Ap : Number of candidates appeared Pa : Number of candidates passed Exp : Expelled Can : Cancelled ENG : English AEN : Alternative English AO : Ao SMI : Sumi LTA : Lotha TNY : Tenyidie BNG : Bengali HND : Hindi EDN : Education PSC : Political Science ECO : Economics HIS : History PSY : Psychology SGY : Sociology PHI : Philosophy GEO : Geography MSC : Music ACC : Accountancy BUS : Business Studies ENT : Entrepreneurship FBM : Fundamentals of Business Mathematics PHY : Physics MAT : Mathematics CHE : Chemistry BIO : Biology CSC : Computer Science INF : Informatics Practices BIT : Biotechnology Dated Kohima, (Mrs.Asano Sekhose) the 30th April 2012 Secretary 2 NAGALAND BOARD OF SCHOOL EDUCATION , KOHIMA NOTIFICATION NO. -

Name of Volunteers District

S.NO Name of Volunteers District 1 Akalu Dimapur 2 Akhevili V Awomi Dimapur 3 Alotoli Awomi Dimapur 4 Avika Kiba Dimapur 5 Avito Assumi Dimapur 6 Chiziko Dimapur 7 Dorilla S Yimchunger Dimapur 8 Gideon Yeptho Dimapur 9 Gloria Ghirulila Dimapur 10 Henoka H Chishi Dimapur 11 Hika I Achumi Dimapur 12 Hikali Dimapur 13 Holloka Dimapur 14 Ito Assumi Dimapur 15 Jimri Yimchunger Dimapur 16 K.Alitoli Dimapur 17 Kanoli Chishi Dimapur 18 Kaqheli Dimapur 19 Kavitoli Dimapur 20 Kekrieneizo Rupreo Dimapur 21 Kumugha Chishi Dimapur 22 Kutupu Kiho Dimapur 23 Lalginhao Dimapur 24 Lhousilienuo Doze Dimapur 25 Lobani Odyuo Dimapur 26 Moaienla Longchar Dimapur 27 Abeni Dimapur 28 Ngukato Sumi Dimapur 29 Nika Assumi Dimapur 30 Ovungbeni Yanthan Dimapur 31 P. Yezakha Sumi Dimapur 32 Pulie Konyak Dimapur 33 Rachel Molongmei Dimapur 34 Reuben Surin Dimapur 35 Sentijungla Dimapur 36 Sudila Dimapur 37 Toivali Dimapur 38 Tokato Dimapur 39 Tongpangshilo Dimapur 40 Tono . A Chishi Dimapur 41 Tovito Chophy Dimapur 42 Tsuyanla W. Yimchunger Dimapur 43 Viphikhono Victoria Meyase Dimapur 44 Visheka V Yeptho Dimapur 45 Vito Nuwiry Dimapur 46 Yalena Dimapur 47 Yongwe C Konyak Dimapur 48 Khaketo Yepthomi Dimapur 49 Manjan Konyak Dimapur 50 Kaihrii Dimapur 51 Chongkoi T Dimapur 52 Kushen T Dimapur 53 Akamla Phom Dimapur 54 Yankithung Mozhui Dimapur 55 Helis Dimapur 56 Chenithung Patton Dimapur 57 Lipokla Dimapur 58 Apongmar Jamir Dimapur 59 Langwang Dimapur 60 N Moba Konyak Dimapur 61 Henoka A Yepthomi Dimapur 62 K Viloto Awomi Dimapur 63 Phuhsing Konyak Dimapur 64 PF Elow -

GOVERNMENT of NAGALAND DIRECTORATE of HIGHER EDUCATION NAGALAND: KOHIMA NO.HED/SCHO-1/2016/ Dated, Kohima, the 18 April. 2019. N

GOVERNMENT OF NAGALAND DIRECTORATE OF HIGHER EDUCATION NAGALAND: KOHIMA NO.HED/SCHO-1/2016/ Dated, Kohima, the 18th April. 2019. Notification on Unclaimed Cheques of Scholarships The Department of Higher Education is hereby publishing the list of students whose Scholarships could not be credited into their accounts due to incorrect bank details. In this connection, the Department has given Press releases on 3rd Nov. 2017 and 25th March 2019. In spite of the said notifications, there are a number of cheques lying unclaimed in the Directorate of Higher Education. Therefore, Students whose names/details are listed below may kindly claim the same from the Directorate during the Office hours with Xerox copies of passbook front page along with a proof of one Identification Card. The Department shall issue the said cheques from 1st May 2019 to 29th June 2019 failing which; the Department shall report the matter to the State Government for further necessary action. This information will serve as final notification. For any query students may call the office during office hours 0370-2271030. SCHOLARSHIP BANKERS CHEQUE LYING UNDER THE DIRECTORATE OF HIGHER EDUCATION S.N NAME OF STUDENT NAME OF INSTITUTE DISTRICT ACADEMIC YEAR 1 ANTHONY SANGTAM MT MARRY HR SEC CHUMUKEDIMA DIMAPUR 2014-15 2 THUNGPANG CHIGMAK GHSS TUENSANG TUENSANG 2014-15 3 KEZEA ZELIANG ICFAI UNIVERSITY DIMAPUR DIMAPUR 2014-15 4 KENEINGULIE SHUYA ICFAI UNIVERSITY DIMAPUR DIMAPUR 2014-15 5 WOPENTHUNG EASTERN BIBLE COLLEGE DIMAPUR DIMAPUR 2014-15 6 WANLIH KONYAK BAPTIST THEOLOGICAL