Republic of Cuba Telecommunications Fundamental Plan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

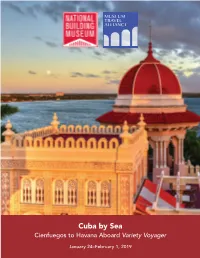

Cuba by Sea Cienfuegos to Havana Aboard Variety Voyager

MUSEUM TRAVEL ALLIANCE Cuba by Sea Cienfuegos to Havana Aboard Variety Voyager January 24–February 1, 2019 MUSEUM TRAVEL ALLIANCE Dear Members and Friends of the National Building Museum, Please join us next January for a cultural cruise along Cuba’s Caribbean coast. From Cienfuegos to Havana, we will journey aboard a privately chartered yacht, discovering well-preserved colonial architecture and fascinating small museums, visiting talented artists in their studios, and enjoying private concerts and other exclusive events. The Museum Travel Alliance (MTA) provides museums with the opportunity to offer their members and patrons high-end educational travel programming. Trips are available exclusively through MTA members and co-sponsoring non- profit institutions. This voyage is co-sponsored by The Metropolitan Museum of Art and the Association of Yale Alumni. Traveling with us on this cultural cruise are a Cuban-American architect and a partner in an award-winning design firm, a curator from The Metropolitan Museum of Art, and a Professor in the Music Department and African American Studies and American Studies at Yale University. In Cienfuegos, view the city’s French-accented buildings on an architectural tour before boarding the sleek Variety Voyager to travel to picturesque Trinidad. Admire the exquisite antiques and furniture displayed in the Romantic Museum and tour the studios of prominent local artists. Continue to Cayo Largo to meet local naturalists, and to remote Isla de la Juventud to see the Panopticon prison (now a museum) that once held Fidel Castro. We will also visit with marine ecologists on María la Gorda, a UNESCO Biosphere Reserve, before continuing to Havana for our two-day finale. -

Proyecto Integral Para La Producción Local De Alimentos

Programa integral para la producción de alimentos en el contexto del Desarrollo Local. La experiencia del municipio Yaguajay, Cuba. Sinaí, Boffill¹, J. Suárez², R.M. Reyes¹, C. Luna³, D. Prado4 y C. Calcines5 1Sede Universitaria Municipal de Yaguajay, Batey Simón Bolívar, Yaguajay, Sancti Spíritus, Cuba E-mail: [email protected] 2Estación Experimental de Pastos y Forrajes “Indio Hatuey”, Matanzas, Cuba 3Grupo de Alimentos del Gobierno Municipal, Yaguajay, Sancti Spíritus, Cuba 4Oficina de Proyectos, Consejo de Administración Municipal, Yaguajay, Sancti Spíritus, Cuba 5Dirección Municipal de Planificación, Yaguajay, Sancti Spíritus, Cuba Resumen El artículo brinda la experiencia de un programa para la producción local de alimentos en el municipio Yaguajay, provincia de Sancti Spíritus, que puede servir de referencia a otros municipios con similares características. Dicho programa abarca las empresas pecuaria y de cultivos varios, la empresa agropecuaria y forestal, así como las cooperativas campesinas. Se desarrolla en el contexto del Macroproyecto Yaguajay, a partir del complejo ECOCIST, que integra Educación Superior-Conocimiento-Tecnología-Innovación-Sociedad para fortalecer las interrelaciones con instituciones del conocimiento en el proceso de su apropiación social en un territorio. El programa integral para la producción local de alimentos surge en el año 2004, posee 29 tareas, insertadas en cuatro subprogramas (Pecuario, Cultivos Varios, Forestal y Frutal, e Industrial), se ejecuta mediante proyectos y prioriza la adopción de tecnologías y la capacitación, a partir de la interacción con universidades, centros de investigación y otras organizaciones. Entre los resultados se destacan el autoabastecimiento de leche fresca, la mejora del rebaño vacuno y de su base alimentaria, el desarrollo de la ganadería ovina, porcina y cunícola, municipio de Referencia Nacional en Agricultura Urbana, producción de biopesticidas y la estrategia de eliminación de plantas leñosas indeseables. -

Title Template

AMPHIBIANS OF CUBA: CHECKLIST AND GEOGRAPHIC DISTRIBUTIONS Vilma Rivalta González, Lourdes Rodríguez Schettino, Carlos A. Mancina, & Manuel Iturriaga Instituto de Ecología y Sistemática Ministerio de Ciencia, Tecnología y Medio Ambiente SMITHSONIAN HERPETOLOGICAL INFORMATION SERVICE NO. 145 2014 . SMITHSONIAN HERPETOLOGICAL INFORMATION SERVICE The first number of the SMITHSONIAN HERPETOLOGICAL INFORMATION SERVICE series appeared in 1968. SHIS number 1 was a list of herpetological publications arising from within or through the Smithsonian Institution and its collections entity, the United States National Museum (USNM). The latter exists now as little more than the occasional title for the registration activities of the National Museum of Natural History. No. 1 was prepared and printed by J. A. Peters, then Curator-in-Charge of the Division of Amphibians & Reptiles. The availability of a NASA translation service and assorted indices encouraged him to continue the series and distribute these items on an irregular schedule. The series continues under that tradition. Specifically, the SHIS series distributes translations, bibliographies, indices, and similar items judged useful to individuals interested in the biology of amphibians and reptiles, and unlikely to be published in the normal technical journals. We wish to encourage individuals to share their bibliographies, translations, etc. with other herpetologists through the SHIS series. If you have such an item, please contact George Zug [zugg @ si.edu] for its consideration for distribution through the SHIS series. Our increasingly digital world is changing the manner of our access to research literature and that is now true for SHIS publications. They are distributed now as pdf documents through two Smithsonian outlets: BIODIVERSITY HERITAGE LIBRARY. -

Cuban Rare Books in the Harold and Mary Jean Hanson Rare Books Collection

Cuban Rare Books in the Harold and Mary Jean Hanson Rare Books Collection This bibliography includes titles published in Cuba from early imprints to present. As we are constantly adding early and contemporary imprints, this list should not be taken as a comprehensive list. Please consult with George A. Smathers Libraries online catalog to be sure newly acquired books are included. It is our intent to update this list quarterly when new books and materials are purchased. The list is not in any order. You will need to use your browser's Find function to locate particular items. Eventually, these titles will receive full cataloging and a Library of Congress classification number. You need to check the online catalog for the correct call number. If you have any questions, please contact the Latin American Collection. Author: Asociación de Dependientes del Comercio de la Habana Title: Memoria de los trabajos llevados a cabo por la Directiva durante al año de 1893 a 1894 y 2o semestre del año de 1894: aprobada por la Directiva en sesión extraordinaria de 19 de enero de 1895 Asociación de Dependientes del Comercio de la Habana. Published: Habana: P. Fernández y Cía., 1895. Description: 46 p., [4] fold. leaves of plates : ill.; 23 cm. Notes The illustrations consist of tables recording statistical specifics of the association's activities. Location: UF SMATHERS, Special Coll Rare Books (Non-Circulating) -- HV160.H3A75 1895 Title: Barquitos del San Juan : la revista de los niños. Published: Matanzas, Cuba: Ediciones Vigía, [199-] Description: v.: ill. (some col.) ; 20-29 cm. Frequency: Irregular Alternate title: Revista de los niños Notes: Each no. -

Federal Register/Vol. 85, No. 188/Monday, September 28, 2020

Federal Register / Vol. 85, No. 188 / Monday, September 28, 2020 / Notices 60855 comment letters on the Proposed Rule Proposed Rule Change and to take that the Secretary of State has identified Change.4 action on the Proposed Rule Change. as a property that is owned or controlled On May 21, 2020, pursuant to Section Accordingly, pursuant to Section by the Cuban government, a prohibited 19(b)(2) of the Act,5 the Commission 19(b)(2)(B)(ii)(II) of the Act,12 the official of the Government of Cuba as designated a longer period within which Commission designates November 26, defined in § 515.337, a prohibited to approve, disapprove, or institute 2020, as the date by which the member of the Cuban Communist Party proceedings to determine whether to Commission should either approve or as defined in § 515.338, a close relative, approve or disapprove the Proposed disapprove the Proposed Rule Change as defined in § 515.339, of a prohibited Rule Change.6 On June 24, 2020, the SR–NSCC–2020–003. official of the Government of Cuba, or a Commission instituted proceedings For the Commission, by the Division of close relative of a prohibited member of pursuant to Section 19(b)(2)(B) of the Trading and Markets, pursuant to delegated the Cuban Communist Party when the 7 Act, to determine whether to approve authority.13 terms of the general or specific license or disapprove the Proposed Rule J. Matthew DeLesDernier, expressly exclude such a transaction. 8 Change. The Commission received Assistant Secretary. Such properties are identified on the additional comment letters on the State Department’s Cuba Prohibited [FR Doc. -

Lessons in Risk Reduction from Cuba

Lessons in Risk Reduction from Cuba Martha Thompson Case study prepared for Enhancing Urban Safety and Security: Global Report on Human Settlements 2007 Available from http://www.unhabitat.org/grhs/2007 Martha Thompson is based at the Unitarian Universalist Service Committee, Massachusetts, US. Comments can be sent to the author at: [email protected] Disclaimer: This case study is published as submitted by the consultant, and it has not been edited by the United Nations. The designations employed and the presentation of the material in this publication do not imply the expression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legal status of any country, territory, city or area, or of its authorities, or concerning delimitation of its frontiers or boundaries, or regarding its economic system or degree of development. The analysis, conclusions and recommendations of the report do not necessarily reflect the views of the United Nations Human Settlements Programme, the Governing Council of the United Nations Human Settlements Programme or its Member States. Lessons in Risk Reduction from Cuba Martha Thompson1 Introduction A snapshot of Cuba’s disaster preparedness in action, (excerpted from the article below) “Staccato bursts of hammer fall punctuated the air, every available jug, bucket and bottle was filled with potable water and radios and televisions beamed the latest from the Cuban Institute of Meteorology into homes and workplaces countrywide. Mean while, evacuation centers were readied to receive tens of thousands, roofs were cleared of debris, farm animals were transferred to safe areas and citrus was picked at lightening speed. -

Yachtcharter - Cuba

VPM Yachtcharter - Cuba Yacht - charter Cuba Cuba is built on myths and metaphors. In the 50’s Cuba was the Monte Carlo of the Caribbean where stars like Errol Flynn or authors like Hemmingway sipped their rum cocktail. Then in the 60’s came the radical revolution and it was followed by the regime of Castro during the last three decades. These are only little episodes in the long history of the Cuban people. Columbus was the first european to discover the island in 1492 and he described it in the following way: "The exceptional beauty beats everything with its magic and grace just as the day surpasses the night with its brilliance." There are thus good reasons for Cuba’s reputation as the pearl of the Antilles. Cuba is located at the entry of the Gulf of Mexico and just below the Northern Tropic. To the west of Cuba lies the Yucatan Peninsula, to the east there is Haiti, to the south there lies Jamaica and to the north at a distance of around 80 nautical miles you will find Florida. 4195 smaller islands and sandbanks are part of the archipelago. Every sailor can trust the north-eastern trade winds. 10 to 25 knots are the norm. There is besides that something noteworthy about Cuba. It has the lowest rate of hurricane appearances in the Antilles. The waters around Cuba Due to the geographical size of Cuba you have to decide in which waters you want to sail. At your disposal are Varadero, which is appealing with its good international flight connections, comfortable hotels and what are probably the island’s most beautiful beaches or Cayo Largo, the Caribbean alternative on the fresher Atlantic coast or even La Habana where you can find one of the world’s most beautiful diving paradises. -

Cuba: Fundamental Telecommunications Plan

CUBA: FUNDAMENTAL TELECOMMUNICATIONS PLAN By Manuel Cereijo INSTITUTE FOR CUBAN AND CUBAN-AMERICAN STUDIES U NIVERSITY OF M IAMI ISBN: 1-932385-16-9. Published in 2004. CUBA: FUNDAMENTAL TELECOMMUNICATIONS PLAN Cuba Transition Project – CTP The Cuba Transition Project (CTP) at the Institute for Cuban and Cuban-American Studies at the University of Miami is an important and timely project to study and make recommenda- tions for the reconstruction of Cuba once the post-Castro transition begins in earnest. This is being accomplished through individual original research, work-study groups, and seminars. The project, which began in January 2002, is funded by a grant from the U.S. Agency for International Development. Research Studies The CTP produces a variety of original studies with practical alternative recommenda- tions on various aspects of the transition process. The studies are available in both English and Spanish. The Spanish translations are sent to Cuba through various means. Databases The CTP is developing several key databases: 1. “Transition Studies” - The full-text, of published and unpublished, articles written on topics of transition in Cuba, as well as articles on transition in Central and Eastern Europe, Nicaragua, and Spain. It also includes an extensive bibliography of published and unpublished books, theses, and dissertations on the topic. 2. “Legal Issues” - In full-text, Cuba’s principal laws (in Spanish), the current Cuban Constitution (in English and Spanish), and other legislation relating to the structure of the existing government. This database also includes a law index and the full-text of numerous law review articles on a variety of transition topics. -

Sancti Spíritus 2018

A T A T A T A A T A T A T A T A T A T A A T A T A A T A T A T A T A T A T A A T A T A T A A T A T A T A T A T A T A T A T A A T A T A T A TANUARIOA T A ESTADÍSTICOT A T A T A A T A T A T A T A T A T A T A T A A T A T A T A T201A T A T 8A T A T A A T A T A T A T A T A T A T A T A A T A T A T A TSANCTIA T A T SPÍRITUSA T A T A A T A T A T A T A T A T A T A T A A T A T A T A T EDICIÓNA T A 201T 9A T A T A A T A T A T A T A T A T A T A T A A T A T A T A T A T A T A T A T A A T A T A T A T A T A T A T A T A ANUARIO ESTADÍSTICO DE SANCTI SPÍRITUS 2018 EDICIÓN 2019 CONTENIDO Capítulos: Página 1. Territorio 15 2. Medio Ambiente 18 3. Población 32 4. Organización Institucional 46 5. Finanzas 50 6. Empleo y Salarios 56 7. -

Cuban Heritage Collection - Cuban Postcard Collection

Cuban Heritage Collection - Cuban Postcard Collection Series I: Cuba: Artists and Personalities Sub-series A: Cuban Artists Box Folder Title 1 Abela, Eduardo (reproduction) Barrios, Pedro (reproduction) Bermúdez, Cundo (reproduction) Bosch, Orlando (reproduction) Diago, Roberto (reproduction) Díaz Escalet, Frank (reproduction) Enríquez, Carlos (reproduction) Lam, Wilfredo Lam, Wilfredo (reproduction) Landaluze, Patricio (reproduction) Lecour, Evelio and García Peña, Ernesto (reproduction) Manuel, Víctor (reproduction) Mijáres, José M. (reproduction) Milián, Raúl (reproduction) Palerzuela (reproduction) Peláez, Amelia (reproduction) Portocarrero, René (reproduction) Rodríguez, Mariano (reproduction) Sub-series B: Cuban Personalities Box Folder Title 8 Castro, Fidel Castro, Fidel, 1959 Castro, Fidel, 1960 Castro, Fidel, 1962 Castro, Fidel, 1964 Castro, Fidel, 1966 1 Finlay, Carlos 8 Guevara, Ernesto "Ché" Guevara, Ernesto "Ché", 1959 Guevara, Ernesto "Ché", 1960 Guevara, Ernesto "Ché", 1961 1 Martí, José Series II: Cuba: General, A-Z Box Folder Title 1 American Intervention, 1907 Architecture: Colonial file:///C|/containerLists/chc0359CL.html (1 of 18) [3/13/2009 1:59:28 PM] Cuban Heritage Collection - Cuban Postcard Collection Bamboo Trees 1, 8 Beaches 8 Beaches: Playa Ancón 1 Birds: Tocororo 8 Birds: Guacamayo 1, 8 Bohío Cubano 8 Cavalry 1 Carriages & Cars: El Carreton Carriages & Cars: La Carreta Carriages & Cars: La Volanta Christmas Cards, 1999 Compañía Cubana Country Life Country Scenes Cruise Ships Cuban Beggar Cuban Bum Boat Dwellings -

Nuevos Precios Para El Transporte Privado

Nuevos precios para el transporte privado ORIGEN DESTINO AUTOS CAMIONETAS CAMIONES Sancti Spíritus Yaguajay 25,00 15,00 10,00 Sancti Spíritus Santa Clara 40,00 25,00 20,00 Sancti Spíritus Ciego de Ávila 35,00 20,00 15,00 Sancti Spíritus Majagua 25,00 15,00 10,00 Sancti Spíritus Mayajigua 35,00 20,00 15,00 Sancti Spíritus Trinidad 40,00 20,00 15,00 Sancti Spíritus Mapos 20,00 15,00 Sancti Spíritus Las Nuevas 18,00 17,00 Sancti Spíritus San Carlos 15,00 10,00 Sancti Spíritus El Jíbaro 30,00 15,00 13,00 Sancti Spíritus La Sierpe 20,00 12,00 8,00 Sancti Spíritus Guasimal 20,00 12,00 8,00 Sancti Spíritus Cabaiguán 10,00 5,00 5,00 Sancti Spíritus Fomento 20,00 15,00 10,00 Sancti Spíritus Jatibonico 15,00 8,00 5,00 Sancti Spíritus Taguasco 15,00 10,00 5,00 Sancti Spíritus Tunas de Zaza 25,00 15,00 10,00 Sancti Spíritus Banao 10,00 8,00 5,00 Sancti Spíritus Placetas 25,00 15,00 12,00 Sancti Spíritus La Rana 10,00 10,00 Sancti Spíritus Pojabo- La Herradura 10,00 5,00 Sancti Spíritus La Larga 8,00 8,00 Sancti Spíritus Habana 180,00 80,00 Sancti Spíritus Pinar del Río 220,00 115,00 Sancti Spíritus Artemisa 200,00 85,00 Sancti Spíritus San José 150,00 70,00 Sancti Spíritus Matanzas 180,00 60,00 Sancti Spíritus Camagüey 110,00 45,00 Sancti Spíritus Las Tunas 130,00 70,00 Sancti Spíritus Holguín 150,00 85,00 Sancti Spíritus Cienfuegos 90,00 50,00 35,00 Sancti Spíritus Bayamo 170,00 90,00 Sancti Spíritus Santiago de Cuba 200,00 110,00 Sancti Spíritus Guantánamo 250,00 130,00 Yaguajay Chambas 20,00 15,00 10,00 Yaguajay Caibarién 15,00 12,00 10,00 Meneses -

A New Cryptic Species of the Genus Eleutherodactylus (Amphibia: Anura: Eleutherodactylidae) from Cuba

TERMS OF USE This pdf is provided by Magnolia Press for private/research use. Commercial sale or deposition in a public library or website is prohibited. Zootaxa 3220: 44–60 (2012) ISSN 1175-5326 (print edition) www.mapress.com/zootaxa/ Article ZOOTAXA Copyright © 2012 · Magnolia Press ISSN 1175-5334 (online edition) A new cryptic species of the genus Eleutherodactylus (Amphibia: Anura: Eleutherodactylidae) from Cuba LUIS M. DÍAZ1, S. BLAIR HEDGES2 & MICHAEL SCHMID3 1Museo Nacional de Historia Natural de Cuba, Obispo #61, Esquina Oficios, Plaza de Armas, Habana Vieja, CP 10100. E-mail: [email protected] 2Department of Biology, 208 Mueller Laboratory, Pennsylvania State University, University Park, Pennsylvania 16802-5301. E-mail: [email protected] 3Department of Human Genetics, Biocenter, University of Würzburg, Würzburg, Germany. E-mail: [email protected] burg.de Abstract The widely distributed grass frog of Cuba, Eleutherodactylus varleyi, is shown here to comprise two species. One, E. var- leyi, occurs in western and central Cuba while the other, E. feichtingeri n. sp., occurs in central and eastern Cuba. The two species are sympatric in central Cuba, and syntopic in the vicinity of Sierra de Cubitas, Camagüey Province. A molecular phylogeny of mitochondrial DNA sequences from 18 localities confirms the existence of two well-supported major clades corresponding to each of these species, and the sympatry of the species. Tympanum size and advertisement call are the most useful diagnostic characters, although the two species are shown to have karyotypic differences as well. Possible character displacement in morphology and vocalization, in the area of sympatry, is discussed.