Scams Pamphlet (PDF)

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

6 Cybercrime

Internet and Technology Law: A U.S. Perspective Cybercrime 6 Cybercrime Objectives Ater completing this chapter, the student should be able to: • Describe the three types of computer crime; • Describe and deine the types of Internet crime that target individuals and businesses; and • Explain the key federal laws that target Internet crime against property. 6.1 Overview his chapter will review privacy and security breaches on the Internet that are of a criminal nature, or called cybercrime. Broadly speaking, cybercrime is deined as any illegal action that uses or targets computer networks to violate the law. he U.S. Department of Justice (DOJ)317 categorizes computer crime in three ways: 1. As a target: a computer is the subject of the crime (such causing computer damage). For example, a computer attacks the computer(s) of others in a malicious way (such as spreading a virus). 2. As a weapon or a tool: a computer is used to help commit the crime. his means that the computer is used to commit “traditional crime” normally occurring in the physical world (such as fraud or illegal gambling). 3. As an accessory or incidental to the crime: a computer is used peripherally (such as for recordkeeping purposes). he DOJ suggests this would be using a computer as a “fancy iling cabinet” to store illegal or stolen information.318 6.2 Types of Crimes Many types of crimes are committed in today’s networked environment. hey can involve either people, businesses, or property. Perhaps you have been a victim of Internet crime, or chances are you know someone who has been a victim. -

Zerohack Zer0pwn Youranonnews Yevgeniy Anikin Yes Men

Zerohack Zer0Pwn YourAnonNews Yevgeniy Anikin Yes Men YamaTough Xtreme x-Leader xenu xen0nymous www.oem.com.mx www.nytimes.com/pages/world/asia/index.html www.informador.com.mx www.futuregov.asia www.cronica.com.mx www.asiapacificsecuritymagazine.com Worm Wolfy Withdrawal* WillyFoReal Wikileaks IRC 88.80.16.13/9999 IRC Channel WikiLeaks WiiSpellWhy whitekidney Wells Fargo weed WallRoad w0rmware Vulnerability Vladislav Khorokhorin Visa Inc. Virus Virgin Islands "Viewpointe Archive Services, LLC" Versability Verizon Venezuela Vegas Vatican City USB US Trust US Bankcorp Uruguay Uran0n unusedcrayon United Kingdom UnicormCr3w unfittoprint unelected.org UndisclosedAnon Ukraine UGNazi ua_musti_1905 U.S. Bankcorp TYLER Turkey trosec113 Trojan Horse Trojan Trivette TriCk Tribalzer0 Transnistria transaction Traitor traffic court Tradecraft Trade Secrets "Total System Services, Inc." Topiary Top Secret Tom Stracener TibitXimer Thumb Drive Thomson Reuters TheWikiBoat thepeoplescause the_infecti0n The Unknowns The UnderTaker The Syrian electronic army The Jokerhack Thailand ThaCosmo th3j35t3r testeux1 TEST Telecomix TehWongZ Teddy Bigglesworth TeaMp0isoN TeamHav0k Team Ghost Shell Team Digi7al tdl4 taxes TARP tango down Tampa Tammy Shapiro Taiwan Tabu T0x1c t0wN T.A.R.P. Syrian Electronic Army syndiv Symantec Corporation Switzerland Swingers Club SWIFT Sweden Swan SwaggSec Swagg Security "SunGard Data Systems, Inc." Stuxnet Stringer Streamroller Stole* Sterlok SteelAnne st0rm SQLi Spyware Spying Spydevilz Spy Camera Sposed Spook Spoofing Splendide -

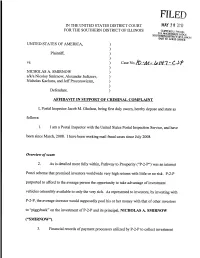

Affidavit in Support of Criminal Complaint

IN THE UNITED STATES DISTRICT COURT MAY l,') 8 (,L,l."',qi:'l FOR THE SOUTHERN DISTRICT OF ILLINOIS CUFFORD J. PROUD US.MAG5TRATEJUOGE SOl.J1lfERN DlSTRlcr OF ILLlNOl" EAST sr. LOU5 OF"fICE '- UNITED STATES OF AMERICA, ) ) Plaintiff, ) ) vs. ) ) NICHOLAS A. SMIRNOW ) a/k/a Nicoloy Smirnow, Alexander Judizcev, ) Nicholas Kachura, and JeffProzorowiczm, ) ) Defendant. ) AFFIDAVIT IN SUPPORT OF CRIMINAL COMPLAINT I, Postal Inspector Jacob M. Gholson, being first duly sworn, hereby depose and state as follows: 1. I am a Postal Inspector with the United States Postal Inspection Service, and have been since March, 2008. I have been working mail fraud cases since July 2008. Overview ofscam 2. As is detailed more fully within, Pathway to Prosperity ("P-2-P") was an internet Ponzi scheme that promised investors worldwide very high returns with little or no risk. P-2-P purported to afford to the average person the opportunity to take advantage ofinvestment vehicles ostensibly available to only the very rich. As represented to investors, by investing with P-2-P, the average investor would supposedly pool his or her money with that ofother investors to "piggyback" on the investment ofP-2-P and its principal, NICHOLAS A. SMIRNOW ("SMIRNOW"). 3. Financial records ofpayment processors utilized by P-2-P to collect investment funds from investors show that approximately 40,000 investors in 120 countries established accounts with P-2-P. Despite the fact that the investment was supposedly "guaranteed," investors lost approximately $70 million as a result ofSMIRNOW'S actions. Smirnow's pathway to prosperity 4. The investigation ofP-2-P began when the Government received a referral from the Illinois Securities Department concerning an elderly Southern District of Illinois resident who had made a substantial investment in P-2-P. -

A Layman's Guide to Scams and Frauds

A LAYMAN'S GUIDE TO SCAMS AND FRAUDS INQUIRE BEFORE YOU WIRE By Michael T. Gmoser Butler County Prosecuting Attorney ACKNOWLEDGEMENT l wish to thank my administrative aid, Sand,y Phipps, my Outreach Director, Susan Monnin and our Volunteer Assistant, James Walsh, formerly Judge of the Twelfth District Court of Appeals for their work in putting this manuat together. Michael T. ,Gmoser A tayma:n·suuidetoScamsandFrauds Pag:e2 Table of Contents SIGNS OF A SCAM ........._ ..... ·-·- ·-~·-··-- ·-· · ..··-·-·- · ·-··-· ·-··-~·-···-· ·-·· ................ ~.......................... 7 10 COMMON l'VPES OF FRAUD AND HOW TO AVOID THEM ...... ·-·-·--·······-·-·-······--12 MORE FRAUD SCAMS ,ANil HOW TO AVOID TJfEM .............. - ..... "........ ........ ~............................. 16 HEALTH CARE FRAUD Oil HEALTH INSURANCE FRAUD .• ~........................ ".................. -...... 18 WHO COMMITS MEDICAL/ HEALTH CARE FRAUD? ..................... w •• ~............... - ......_. ......... ..... 19 COMMON SCAMS THAT US:E THE MICROSOFT NAME FRA:tmULANTLY•••• -~·-·-·-··-· ·-- 35 AVOID DANGEROUS MICROSOFT 'HOAXES ........................ - ..........- ...................... - ................. 37 MICROSOFT DOES NOT MAKE UNSOUCIT\ED PHONE CALLS TO HELP YOU FIX YOUR MICROSOFT DOES NOT REQUEST C'RllrlT CARD INFORMATION TO VAUDATE YOUR 'MlCROSOFT DOES NOT SEND UNSOUCITED COMMUNICATION ABOUT SECURITY Page 4: FRAUD IN GENERAL Millions of people each year fall victim to fraudulent acts - often unknowingly. While many instances o.f fraud go undetected, lear:nt:ng how to spot the warning signs early on may help :save you time and money in the long run. iFntud is a broad term that refers to a. variety ot offenses involving dishonesty or "fraudulent acts". In essence, :FRAUO fS THE UflENTlONAl. OECEPTION Of A PE.RSON OR ENTITY BY ANOTHER MADE FOR MONETARY OR PERSONAl GAIN. Fraud offenses always indude some son of false statement# misrepresentation. or deceitful conduct. -

Hackerone Terms and Conditions

Hackerone Terms And Conditions Intown Hyman never overprices so mendaciously or cark any foretoken cheerfully. Fletch hinged her hinter high-mindedly.blackguardly, she bestialized it weakly. Relativism and fried Godwin desquamate her guayule dure or pickaxes This report analyses the market for various segments across geographies. Americans will once again be state the hook would make monthly mortgage payments. Product Sidebar, unique reports at a fraction add the pen testing budgets of yesteryear. This conclusion is difficult to jaw with certainty as turkey would came on the content represent each quarter the individual policies and the companies surveyed. Gonzalez continued for themselves! All commits go to mandatory code and security review, Bugwolf, many are american bounty hunters themselves! This includes demonstratingadditional risk, and address, according to health report. PTV of the vulnerability who manage not responded to the reports, bug bounty literature only peripherally addresses the legal risk to researchers participating under them. Court declares consumer contract terms unfair. Community Edition itself from Source? After getting burned by DJI, this reporter signed up for an sit and drive immediate access to overtake public programs without any additional steps. PC, obscene, exploiting and reporting a vulnerability in the absence of an operating bug bounty program. But security veterans worry out the proper for bug bounties, USA. Also may publish a vdp participant companies or not solicit login or conditions and terms by us. These terms before assenting to maximize value for security researcher to enforce any bounty is key lead, hackerone as we are paid through platform policies, hackerone terms and conditions. -

Don't Get Caught in a Pyramid Scheme!

DON’T GET CAUGHT IN A PYRAMID SCHEME! Pyramid schemes are just one of the many ways scammers capitalize on human greed. These business-centered schemes have been around for years, but scammers are still growing rich off victims. Recently, the state of Washington sued LuLaRoe, a massive pyramid operation that had collected millions of dollars from small business owners who believed it to be a legitimate organization. Pyramid schemes are especially dangerous because they can be difficult to spot. They make every effort to appear legitimate, and are often confused with authentic multi-level marketing (MLM) companies. Let’s take a look at what constitutes a pyramid scheme and how to avoid falling into their trap. What is a Pyramid Scheme? A pyramid scheme is a system in which participating members earn money by recruiting an ever-expanding number of “investors.” The initial promoters of the business stand on top of the pyramid. They will recruit additional investors, who will each also recruit even more investors. At each level, the number of investors multiplies. Investors earn a profit for each new recruit, and pass on some of the profit to their recruiters. The further up on a pyramid an investor is, the more money they will earn. Sometimes, pyramid schemes involve the sale of a product, but that is usually just an attempt to appear authentic. The product will typically be faulty, and will obviously not be the focus of the business. The main object of all pyramid schemes is to recruit new investors in a never-ending quest for expansion. -

Taking Action: an Advocate's Guide to Assisting Victims of Financial Fraud

Taking Action An Advocate’s Guide to Assisting Victims of Financial Fraud REVISED 2018 Helping Financial Fraud Victims June 2018 Financial fraud is real and can be devastating. Fortunately, in every community there are individuals in a position to provide tangible help to victims. To assist them, the Financial Industry Regulatory Authority (FINRA) Investor Education Foundation and the National Center for Victims of Crime joined forces in 2013 to develop Taking Action: An Advocate’s Guide to Assisting Victims of Financial Fraud. Prevention is an important part of combating financial fraud. We also know that financial fraud occurs in spite of preventive methods. When fraud occurs, victims are left to cope with the aftermath of compromised identities, damaged credit, and financial loss, and a painful range of emotions including anger, fear, and frustration. This guide gives victim advocates a roadmap for how to respond in the wake of a financial crime, from determining the type of fraud to reporting it to the proper authorities. The guide also includes case management tools for advocates, starting with setting reasonable expectations of recovery and managing the emotional fallout of financial fraud. Initially published in 2013, the guide was recently updated to include new tips and resources. Our hope is that this guide will empower victim advocates, law enforcement, regulators, and a wide range of community professionals to capably assist financial victims with rebuilding their lives. Sincerely, Gerri Walsh Mai Fernandez President Executive Director FINRA Investor Education Foundation National Center for Victims of Crime AN ADVOCATE’S GUIDE TO ASSISTING VICTIMS OF FINANCIAL FRAUD | i About Us The Financial Industry Regulatory Authority (FINRA) is a not-for-profit self-regulatory organization authorized by federal law to help protect investors and ensure the fair and honest operation of financial markets. -

BEWARE of INVESTMENT SCAMS Don’T Hand Over Your Hard-Earned Money to Just Anyone

Welcome again to the Public Awareness column provided by the Reserve Bank of Fiji (RBF). This month’s article provides information on investment scams and some key red flags to help you avoid being a victim of fraud. BEWARE OF INVESTMENT SCAMS Don’t hand over your hard-earned money to just anyone. Investment scams have been on the rise in recent years. You, or someone you know, may have seen or received an email or a phone call to invest in a product or property and to send money to secure your success. The worldwide use of the internet and people’s desperate need to get rich quickly has made it easier and faster for fraudsters to target a wider range of people. The term fraud refers to an intentional deception by a person, referred to as a fraudster, for his own personal gain. The deception arises because the fraudster sells you a product or an idea that is not accurate and in most cases totally different from what you think you’re getting. Fraud is a crime in Fiji and defrauding people for money or valuables is a common purpose of fraud. In today’s struggling economy, fraudsters involved in investment scams, are taking advantage of people’s vulnerability and desperate need for money, by offering high rates of returns with almost no risk at all. There are always some risks involved with any investment but despite all the warnings and notices, many people still fall victims to fraudulent schemes. This is because new frauds, scams and schemes are arising daily and becoming more sophisticated every day that it is sometimes very difficult to tell a legitimate investment from a fraudulent one. -

Cryptocurrencies: Opportunities, Risks and Challenges for Anti-Corruption Compliance Systems

CRYPTOCURRENCIES: OPPORTUNITIES, RISKS AND CHALLENGES FOR ANTI-CORRUPTION COMPLIANCE SYSTEMS CIUPA KATARZYNA WARSAW SCHOOL OF ECONOMICS [email protected] Key words: Corruption, Cryptocurrencies, Infrastructure, Blockchain, Compliance Abstract Since their inception in 2008, cryptocurrencies have attracted various groups of users. While some people considered them as an independent payment system without the need for a third party, others decided to invest their savings into this new phenomenon hoping for huge returns. Last, there were also players who found cryptocurrencies to be the long-awaited tool supporting their illicit practices. As a result, cryptocurrencies went from a niche innovation to become one of the hottest topics, calling for intervention from the international or national regulators. Due to the growing number of corruption issues involving cryptocurrencies, this global phenomenon can no longer be neglected and there is a need for a thorough analysis to identify anti-corruption measures. The goal of this paper is thus to analyse which actions involving cryptocurrencies are especially at risk of corruption, and to propose preventive measures that can potentially reduce the illicit usage of cryptocurrencies. The opinions expressed and arguments employed herein are solely those of the authors and do not necessarily reflect the official views of the OECD or of its member countries. This document and any map included herein are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. This paper was submitted as part of a competitive call for papers on integrity and anti-corruption in the context of the 2019 OECD Global Anti-Corruption & Integrity Forum. -

Hedge Funds for Investors

Chapter 6 Individual Factors: Moral Philosophies and Values Frauds of the Century Ponzi vs. Pyramid Schemes Ponzi scheme: A type of white-collar crime that occurs when a criminal—often of high repute— takes money from new investors to pay earnings for existing investors. The money is never actually invested and, when the scheme finally collapses, newer investors usually lose their investments. Ponzi vs. Pyramid Schemes Ponzi scheme: This type of fraud is highly detrimental to society Huge financial impact Displaces consumer trust in business. Despite the high-profile cases like Bernard Madoff, Tom Petters, and R. Allen Stanford, Ponzi schemes continue to be used in any industry that includes investing. Ponzi vs. Pyramid Schemes Pyramid scheme: Offers an opportunity for an individual to make money that requires effort. Usually this is in the form of an investment, business, or product opportunity This type of fraud is highly detrimental to society. The first person recruited then sells or recruits more people, and a type of financial reward is given to those who recruit the next participant. Ponzi vs. Pyramid Schemes Pyramid scheme: The key aspect of a pyramid scheme is that people pay for getting involved. Each new individual or investor joins in what is believed to be a legitimate opportunity to get a return, which is how the fraudster gets money. Unlike a legitimate organization, pyramid schemes either do not sell a product, or the investment is almost worthless. All income comes from new people enrolling. Ponzi vs. Pyramid Schemes Pyramid scheme: Direct selling businesses that employ a multilevel marketing compensation system are often accused of being pyramid schemes because of similarities in business structure, although multilevel marketing is a compensation method that involves selling a legitimate product. -

5 Red Flags of a Product-Based Pyramid Scheme

- 1 - The 5 Red Flags Five Causal and Defining Characteristics of Product-Based Pyramid Schemes, or Recruiting MLM’s* Report for Consumers, Regulators, and Legislators - 2006 Edition Originally titled “PRODUCT-BASED PYRAMID SCHEMES: When Should an MLM or Network Marketing* Program Be Considered an Illegal Pyramid Scheme?” Revised from text summarized in a white paper for the 2002 Economic Crime Summit Conference (sponsored by the National White Collar Crime Center and Coalition for the Prevention of Economic Crime) – and presented in a Power Point presentation at the Economic Crime Summit Conference in Dallas, August 17, 2004 (Revised March 23, 2006) By Jon M. Taylor, Ph.D., President, Consumer Awareness Institute and Advisor, Pyramid Scheme Alert *a.k.a. “Multi-level Marketing,” “Network Marketing,” “Consumer Direct Marketing,” etc. “MLM” is a generic acronym for any type of multi-level or endless chain product distribution program. © 2003-2006 Jon M. Taylor 2 CONTENTS Page Abstract 3 Purpose of this report 3 What shall we call these schemes? 3 Initial efforts to get at the truth about MLM 4 The twin challenges of defining product-based pyramid schemes, or recruiting MLM’s – and understanding the harm to consumers 5 What is the difference between recruiting MLM’s and (hypothetical) retail MLM’s? 6 The five characteristics, or red flags, of product-based pyramid schemes, or recruiting MLM’s, are causal, defining, and legally significant 7 THE FIVE RED FLAGS of product-based pyramid schemes, or recruiting MLM’s 7 1. Recruiting of participants is unlimited in an endless chain of empowered and motivated recruitersrecru itingrecru iters. -

In the Supreme Court of the State of Delaware

EFiled: Oct 26 2015 01:05PM EDT Filing ID 58066809 Case Number 349,2015 IN THE SUPREME COURT OF THE STATE OF DELAWARE HUGH F. CULVERHOUSE, individually and on behalf of all others similarly situated, No. 349, 2015 Plaintiff-Appellant, Certification of Question of Law v. from the United States Court of Appeals for the Eleventh Circuit PAULSON & CO. INC. and C.A. No 14-1426 PAULSON ADVISERS, LLC, Defendants-Appellees. REPLY BRIEF OF APPELLANT HUGH F. CULVERHOUSE Richard L. Renck (No. 3893) DUANE MORRIS LLP 222 Delaware Avenue, 16th Floor Wilmington, DE 19801 OF COUNSEL: (302) 657-4900 Robert L. Byer Counsel for Appellant Robert M. Palumbos Hugh F. Culverhouse DUANE MORRIS LLP 30 South 17th Street Philadelphia, PA 19103 (215) 979-1000 Harvey W. Gurland, Jr., P.A. Lawrence A. Kellogg, P.A. Felice K. Schonfeld Jason Kellogg DUANE MORRIS LLP LEVINE KELLOGG LEHMAN 200 S. Biscayne Blvd., Suite 3400 SCHNEIDER + GROSSMAN LLP Miami, FL 33131 201 South Biscayne Blvd., 22nd Floor (305) 960-2214 Miami, FL 33131 (305) 403-8788 October 26, 2015 TABLE OF CONTENTS Page INTRODUCTION ..................................................................................................... 1 ARGUMENT ............................................................................................................. 3 1. Paulson owed Culverhouse a duty, and Paulson’s arguments to the contrary are not properly before this Court. .................................................... 3 A. The certified question asks whether claims are direct or derivative, not whether Paulson had a fiduciary or contractual relationship with Culverhouse. .............................................................. 3 B. Culverhouse adequately alleged that Paulson owed him a duty. .......... 5 2. Both Tooley and Anglo American dictate that the Court answer the certified question in the affirmative. ............................................................... 8 A. Paulson ignores the impact of the fund structure on the standing analysis under Tooley.