Grocery Universe 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Global Vs. Local-The Hungarian Retail Wars

Journal of Business and Retail Management Research (JBRMR) October 2015 Global Vs. Local-The Hungarian Retail Wars Charles S. Mayer Reza M. Bakhshandeh Central European University, Budapest, Hungary Key Words MNE’s, SME’s, Hungary, FMCG Retailing, Cooperatives, Rivalry Abstract In this paper we explore the impact of the ivasion of large global retailers into the Hungarian FMCG space. As well as giving the historical evolution of the market, we also show a recipe on how the local SME’s can cope with the foreign competition. “If you can’t beat them, at least emulate them well.” 1. Introduction Our research started with a casual observation. There seemed to be too many FMCG (Fast Moving Consumer Goods) stores in Hungary, compared to the population size, and the purchasing power. What was the reason for this proliferation, and what outcomes could be expected from it? Would the winners necessarily be the MNE’s, and the losers the local SME’S? These were the questions that focused our research for this paper. With the opening of the CEE to the West, large multinational retailers moved quickly into the region. This was particularly true for the extended food retailing sector (FMCG’s). Hungary, being very central, and having had good economic relations with the West in the past, was one of the more attractive markets to enter. We will follow the entry of one such multinational, Delhaize (Match), in detail. At the same time, we will note how two independent local chains, CBA and COOP were able to respond to the threat of the invasion of the multinationals. -

Romania: Retail Food Sector

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Voluntary - Public Date: 2/6/2017 GAIN Report Number: RO1703 Romania Post: Bucharest Retail Food Sector Report Categories: Retail Foods Approved By: Russ Nicely Prepared By: Ioana Stoenescu Report Highlights: Over the last three years, Romania has seen strong positive growth, with encouraging developments in the economic and policy areas, becoming one of the most attractive markets in Southeastern Europe. After just a few notable events during 2015, the Romanian retail market experienced remarkable growth in 2016 reaching 2,000 stores operated by international retailers. As modern retail systems grow, exports of U.S. processed and high value foods to Romania will continue to expand. In 2015 U.S. agri- food exports to Romania increased by 45 percent from U.S. $96 million to U.S. $139 million over the last year. Romania's food sector is expected to be among the regional best performers during the next five years, with promising market prospects for U.S. exporters such as tree nuts, distilled spirits and wines. General Information: I. MARKET SUMMARY General Information Romania has been a member of the EU since 2007 and a member of NATO since 2004. Within the 28 EU countries, Romania has the seventh largest population, with 19.5 million inhabitants. Romania is presently a market with outstanding potential, a strategic location, and an increasingly solid business climate. Although there is the need for an exporter to evaluate the market in order to assess the business opportunities, exporting to Romania is steadily becoming less challenging than in previous years in terms of the predictability of the business environment. -

DEMO Competitive Analysis Retail

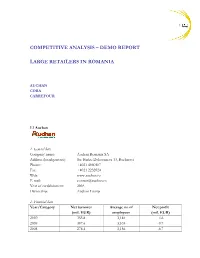

COMPETITIVE ANALYSIS – DEMO REPORT LARGE RETAILERS IN ROMANIA AUCHAN CORA CARREFOUR 1.1 Auchan 1. General data Company name: Auchan Romania SA Address (headquarters): Str. Barbu Delavrancea 13, Bucharest Phone: +4021 4080107 Fax: +4021 2232024 Web: www.auchan.ro E-mail: [email protected] Year of establishment: 2005 Ownership: Auchan Group 2. Financial data Year/Category Net turnover Average no of Net profit (mil. EUR) employees (mil. EUR) 2010 355.8 3,184 -4.6 2009 307.6 3,103 -9.7 2008 278.4 3,156 -6.7 A FRD Center Market Entry Services Demo Publication www.market-entry.ro 3. Key persons Name Position Contact details Mr. Patrick Espasa General Director Email: [email protected] Mr. Tiberiu Danetiu Marketing Director Email: [email protected] Ms. Mariana Dragan Communication Manager Email: [email protected] Tel: +4 021 4080294 4. Brief profile Auchan Romania is part of the French Group Auchan. Auchan opened its first hypermarket on the Romanian market in 2006. This store is located in Bucharest (in the Titan area) and has the surface of over 16,000 sqm. The store records a daily traffic of 30,000 – 45,000 persons and registers the biggest sales in the Auchan network in Romania. At present, Auchan has nine hypermarkets in Romania, located in Bucharest (two stores – in the Titan and Militari areas), Pitesti, Targu Mures, Cluj Napoca, Suceava, Timisoara, Constanta and Craiova. The Auchan hypermarket in Cluj Napoca was opened in November 2007, with an investment of 40 million EUR. The store is located in the Iulius Mall, has the surface of some 10,000 sqm and offers over 45,000 products. -

Netherlands Retail Foods Benelux Food Retail Market

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 1/26/2010 GAIN Report Number: NL0002 Netherlands Retail Foods Benelux Food Retail Market Approved By: Stephen Huete Prepared By: Marcel Pinckaers Report Highlights: Despite the current economic situation, the turnover of the Benelux food retail market in 2009 was €52.7 billion, 4.4% higher than previous year. In addition, the food retail market continues to consolidate further. Post: The Hague Author Defined: Section I. Market Summary Benelux Food Retail Market Approximately 80 percent of the Dutch food retail outlets are full service supermarkets, operating on floor space between 500 and 1,500 square meters located downtown and in residential areas. The remaining 20 percent includes superstores located in industrial parks, convenience stores near human traffic and department stores. In Belgium, full service supermarkets, like Colruyt and AD Delhaize, account for an estimated 75 percent of the market. The share of superstores and convenience stores in Belgium is higher than in the Netherlands, an estimated 25%. In Luxembourg, full service supermarkets like Cactus, Alvo and Match dominate the market as well. In all three markets, independent food retail stores are increasingly leaving the scene. On-going consolidation in the retail market, changing consumer demands and shrinking margins seem to drive this trend. The top 3 biggest retailers in the Netherlands, Albert Heijn, C1000, and Jumbo [1] , have a market share of 56 percent. The market for discounters like Aldi and Lidl has stabilized around 15%. -

Carrefour Group, Building RELATIONSHIPS a L R EPO RT

2007 ANNUAL REPORT CARREFOUR GROUP, BUILDIng RELATIONSHIPS RT EPO R L A U ANN Carrefour SA with capital of 1,762,256,790 euros 2007 RCS Nanterre 652 014 051 www.groupecarrefour.com N°1 in Europe 30 countries N°2 worldwide OTHERS PUBLICATIONS: RAPPORT DÉVELOPPEMENT DURABLE 2007 102.442 billion euros in sales carrEFOUR carrEFOUR incl. tax under GROUP GROUP Group banners 16,899,020 sq.m sales area BUILDING FInancIAL RESPOnsIBLE REPORT RELATIONSHIPS 2007 490,042 employees 2007 Sustainability Report 2007 Financial Report stores More than 3 billion cash 14,991 transactions per year YOU CAN FIND THE LATEST CARREFOUR GROUP NEWS AND THE INTERACTIVE ANNUAL REPORT AT WWW.GROUPECARREFOUR.COM Design, copywriting and production: Translation: Photocredits: Carrefour Photo Library, Lionel Barbe, Christophe Gay/Skyzone, Nicolas Landemard, Gilles Leimdorfer/Rapho, Jean-Erick Pasquier/Rapho, Michel Labelle, all rights reserved - p. 2-3: Getty Images/Bruno Morandi - p. 4-5: Getty Images/ Hans Neleman - p. 6-7: Getty Images/Lonely Planet Images/Krzysztof Dydynski - p. 8-9: Getty Images/Daly & Newton - p. 16: Getty Images/Shannon Fagan - p. 24: Getty Images/Daly & Newton - p. 32: Getty Images/Frank Herholdt - p. 36: Corbis/Beathan - p. 38: Getty Images/fStop - p. 39: Getty Images/Darryl Estrine - p. 40: Corbis/Jose Luis Pelaez - p. 41: Getty Images/Somos/Veer - p. 42: Getty Images/Floresco Images - p. 45: Getty Images/Dimitri Vervitsiotis. CARREFOUR / ATACADAO / CARREFOUR EXPRESS / CARREFOUR BAIRRO / CARREFOUR CITY / CARREFOUR MARKET / 5 MINUT CARREFOUR / Paper: the Carrefour group is committed to the responsible management of its paper sourcing. The paper used for this document is certified PEFC (Programme for the Endorsement of Forest Certification schemes). -

Country Retail Scene Report

SPAIN COUNTRY RETAIL SCENE REPORT December 2012 KANTAR RETAIL 24 – 28 Bloomsbury Way, London WC1A 2PX, UK / Tel. +44 (0)207 031 0272 / www.KantarRetail.com INFORMATION / INSIGHT / STRATEGY / EXECUTION © Kantar Retail 2012 245 First Street 24 – 28 Bloomsbury Way T +44 (0) 207 0310272 Suite 1000 London, WC1A 2PX F +44 (0) 207 0310270 Cambridge, MA 02142 UK [email protected] USA www.kantarretail.com Index I. Key Themes .......................................................................................................... 2 II. Socio – Economic Background .............................................................................. 3 III. Key Players in the Grocery Retail Sector ............................................................ 11 IV. Grocery Retail Channels ..................................................................................... 19 V. Conclusion ........................................................................................................... 24 © 2012 KANTAR RETAIL | 2012 Spain Retail Scene | www.kantarretail.com 1 245 First Street 24 – 28 Bloomsbury Way T +44 (0) 207 0310272 Suite 1000 London, WC1A 2PX F +44 (0) 207 0310270 Cambridge, MA 02142 UK [email protected] USA www.kantarretail.com I. Key Themes National players are capturing growth and increasing concentration in Spain Despite the economic turmoil in Spain, leading Spanish grocery retailers are expected to see their growth accelerate in the coming years, led by retailers such as Mercadona and Dia, both growing at over 5% per year. Mercadona is by far the largest Spanish grocery retailer in terms of sales and has successfully adapted its strategy to the economic crisis that Spain is facing. Its impressive business model has enabled it to retain shopper loyalty and support robust physical expansion and the retailer is looking to further strengthen its domination of the supermarket channel and the grocery market overall. Due to the strong growth of two of the top five grocery retailers in Spain the dominance of a few major players will increase. -

Carrefour Took a New Look at Its Business and Formulated a New Ambition: to Become the Preferred Retailer

22.07.2010 08:20 PDF_QUADRI_300dpi_txvecto 22.07.2010 08:20 PDF_QUADRI_300dpi_txvecto 1 In 2009, Carrefour took a new look at its business and formulated a new ambition: to become the preferred retailer. The retailer that knows its customers, anticipates their desires Report2009 Annual and delights them within its stores. The retailer that inspires trust through product quality, prices and socially-responsible commitments. The retailer that helps customers achieve a better quality of life every day. Carrefour has what it takes to reach its goals: its brand, stores, products, services and teams, all gathered around the same values. In 2009, 475,000 committed employees, caring about customer needs and positive at all times, joined forces to ensure that clients enjoy shopping at Carrefour again and again. 3 billion 7th employer checkouts per year worldwide in the private sector in 2009 2 Our ambition: to become the preferred retailer Satisfying the needs of our customers and consumers is no longer enough. Carrefour must wow and delight them every day. 3 To be recognized Actions speak louder than words. We work hard every day to offer the best products and services at the best prices, creating more value for our customers and consumers. And as we develop this value, we keep building up their recognition. 2009 Annual Report2009 Annual and loved Love begins with very little things. Just like people, a brand is stronger when loved. We do everything in our power to build a relationship with our customers, consumers and partners based on loyalty and trust. And earn their loyalty a little more every day. -

The Benelux Food Retail Market Retail Foods Netherlands

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT POLICY Required Report - public distribution Date: 6/25/2012 GAIN Report Number: NL2014 Netherlands Retail Foods The Benelux Food Retail Market Approved By: Mary Ellen Smith Prepared By: Marcel Pinckaers Report Highlights: The turnover of the Benelux food retail industry for 2011 is estimated at € 56.3 billion. For 2012, turnover is expected to increase by 2.5 percent. The retail market is fairly consolidated. Top 3 food retailers in the Netherlands have a market share of 64 percent while in Belgium the leading 3 retailers have 72 percent of the market. Sustainable food (including organic products) is one of the most important growth markets in food retail. The market share for private label products continues to go up in both Belgium and the Netherlands. The demand for convenient, healthy and new innovative products continues to be strong. Post: The Hague SECTION I. MARKET SUMMARY Benelux Food Retail Market Approximately 80 percent of the Dutch food retail outlets are full service supermarkets, operating on floor space between 500 and 1,500 square meters located downtown and in residential areas. Retailers with full service supermarkets have responded to the need of the Dutch to have these supermarkets close to their house. The remaining 20 percent includes mainly convenience stores (near office buildings and train/metro stations), some wholesalers and just a few superstores (convenient located alongside highways in shopping malls and industrial parks). The Belgians show a different shopping pattern. -

Strategic Retail Management Text and International Cases 3Rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein

Joachim Zentes Dirk Morschett Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Strategic Retail Management Joachim Zentes • Dirk Morschett • Hanna Schramm-Klein Strategic Retail Management Text and International Cases 3rd Edition Joachim Zentes Hanna Schramm-Klein FB Wirtschaftswissenschaften, Universität Siegen Universität des Saarlandes Siegen, Germany Saarbrücken, Germany Dirk Morschett Universität Fribourg Fribourg, Switzerland ISBN 978-3-658-10182-4 ISBN 978-3-658-10183-1 (eBook) DOI 10.1007/978-3-658-10183-1 Springer Gabler Library of Congress Control Number: 2016954795 Springer Gabler © Springer Fachmedien Wiesbaden GmbH 2007, 2011, 2017 This work is subject to copyright. All rights are reserved by the Publisher, whether the whole or part of the material is concerned, specifically the rights of translation, reprinting, reuse of illustrations, recitation, broadcasting, repro- duction on microfilms or in any other physical way, and transmission or information storage and retrieval, elec- tronic adaptation, computer software, or by similar or dissimilar methodology now known or hereafter developed. The use of general descriptive names, registered names, trademarks, service marks, etc. in this publication does not imply, even in the absence of a specific statement, that such names are exempt from the relevant protective laws and regulations and therefore free for general use. The publisher, the authors and the editors are safe to assume that the advice and information in this book are believed to be true and accurate at the date of publication. Neither the publisher nor the authors or the editors give a warranty, express or implied, with respect to the material contained herein or for any errors or omissions that may have been made. -

Outlook of Polish Retail Sector

OUTLOOK OF POLISH RETAIL SECTOR April 15th 2015, World Food Warsaw Fair DIFFERENCES BETWEEN POLAND AND OTHER EU COUNTRIES Poland EU countries The largest number of shops per 1000 persons 0,5 per 1000 persons (2,5) 52 % retail is modern trade 75-80 % retail is modern trade 40 % population lives in rural areas majority of population lives in cities and towns 49 % of population lives in small and medium majority of population lives in big cities and cities towns only 11 % of population lives in major cities majority of population lives in big cities and towns 50 % of consumers buy fruits and vagatables in 33 % consumers buy fresh fruits and vegetables markets and bazaars in markets and bazaars April 15th 2015, World Food Warsaw Fair Modern vs. traditional Number of traditional shops 80-100.000 Number of modern shops 6.400 MARKET IS DEVIDED INTO 2 CHANNELS: TRADITIONAL WITH 48% MARKET SHARE AND MODERN 52 % April 15th 2015, World Food Warsaw Fair POLISH FMCG MARKET IS 80000 WORTH 210-25O BILLION 60000 PLN 40000 Market shares 20000 0 RETAIL SALE IS GROWING Number of shops 3-4 % PER YEAR April 15th 2015, World Food Warsaw Fair Brands of discount stores and hypermarkets on the Polish market Biedronka 2600 Lidl 550 Netto 340 Aldi 90 Czerwona Torebka 40 Auchan 76 Tesco 86 Carrefour 96 Kaufland 183 E.Leclerc 43 DISCOUNT STORES: MARKET SHARE 24 %, HYPERMARKETS: 12 % 15 April 2015, World Food Warsaw Fair Brands of supermarkets on the Polish market Piotr i Paweł 120 Stokrotka 275 Mila 170 Polomarket 270 Alma 45 Marcpol 60 Intermarche 220 Tesco Carrefour -

“The SME's Fight Back: Or David Can Win If He Has Big Enough Stones”

“The SME’s fight back: or David can win if he has big enough stones” AUTHORS Charles S. Mayer M. Reza Bakshandeh ARTICLE INFO Charles S. Mayer and M. Reza Bakshandeh (2014). The SME’s fight back: or David can win if he has big enough stones. Innovative Marketing , 10(1) RELEASED ON Thursday, 03 April 2014 JOURNAL "Innovative Marketing " FOUNDER LLC “Consulting Publishing Company “Business Perspectives” NUMBER OF REFERENCES NUMBER OF FIGURES NUMBER OF TABLES 0 0 0 © The author(s) 2021. This publication is an open access article. businessperspectives.org Innovative Marketing, Volume 10, Issue 1, 2014 Charles S. Mayer (Hungary), M. Reza Bakshandeh (Hungary) The SME’s fight back: or David can win if he has big enough stones Abstract This paper describes how two local Hungarian retail cooperatives, made up of SME’s, have been able to capture a large market share, and put sufficient pressure on a major Belgian multinational, the Louis Delhaize Group, to withdraw from the market. While clearly other factors were also at work in the disenchantment of Delhaize, leading to its withdrawal from Hungary, the case study gives a recipe for the survival of local SME’s facing a frontal attack by MNEs. Two different business models are described. Keywords: SME’s, underdogs, MNE’s, Hungary, retail competition, cooperatives. Introduction In 1999, the Delhaize group acquired one of the early entrants into Hungary, the Julius Meinl group of In December 2011, Belgian-based Louis Delhaize Austria. Julius Meinl consisted of 4 chains (Julius Group, which owned the Match, Cora and Profi Meinl, Jeee Diszkont, Jeee C+C, and Alfa), chains in Hungary, announced that it will cease all consisting of approximately 160 stores and 25 its activities, and exit the Hungarian market [15]. -

Banco Carrefour: Forte Crescimento No Faturamento E EBITDA

Grupo Carrefour Growing momentum of theBrasil omnichannel ecosystem in Q1 Apresentação Institucional Noël Prioux, Grupo Carrefour Brasil CEO Maio de 2019 1 1 Construindo o ecossistema Carrefour Brasil 2 Grupo Carrefour Brasil: Avanços significativos em prioridades estratégicas EXPANSÃO TRANSIÇÃO ALIMENTAR OMNICANALIDADE PARCERIAS CRM SERVIÇOS FINANCEIROS Produtos orgânicos 100 Clientes Portadores 660 Click & Retire cadastrados no Pontos de venda +46% Meu Carrefour 8 milhões vs. ano anterior 13 Retire de Carro Break-even do +39 Marcas próprias 13.9 milhões Cartão Atacadão Aberturas de lojas 11% +1,400 Clientes Sellers no identificados Faturamento Total % das vendas do Carrefour Marketplace no Atacadão* +32% +110% 10 milhões Fonte: Grupo Carrefour Brasil * Na base de clientes do Carrefour Soluções Financeiras GMV 3 Nossas prioridades estão alinhadas ao plano de transformação Carrefour 2022 AÇÕES CONCRETAS PARA SE CONSTRUÇÃO DE UM CULTURA DE EFICIÊNCIA OPERACIONAL TORNAR LÍDER NA TRANSIÇÃO MODELO DE CRESCIMENTO E DISCIPLINA FINANCEIRA ALIMENTAR PARA TODOS • Transformação profunda para • Rápida modernização da proposta • Desenvolvimento da oferta de organizações mais ágeis comercial dentro das lojas, com o apoio de orgânicos parcerias • Promoção da qualidade dos alimentos • Alianças para compras • Agilidade na expansão da oferta omnicanal • Criação do Comitê de Orientação • Industrialização de processos e dinâmica de otimização de custos • Expansão dos formatos em crescimento Alimentar • Proteção ao bem-estar animal • Maior seletividade e