2018 Annual Report Notice of 2019 Annual Meeting & Proxy Statement

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BARC Score Enterprise BI and Analytics Platforms

BARC Score Enterprise BI and Analytics Platforms Authors: Larissa Seidler, Christian Fuchs, Patrick Keller, Carsten Bange, Robert Tischler Publication: September 8th, 2017 Abstract This BARC document is the third edition of our BARC Score business intelligence vendor evaluation and ranking. This BARC Score evaluates enterprise BI and analytics platforms that are able to fulfill a broad set of BI requirements within the enterprise. Based on countless data points from The BI Survey and many analyst interactions, vendors are rated on a variety of criteria, from product capabilities and architecture to sales and marketing strategy, financial performance and customer feedback. This document is not to be shared, distributed or reproduced in any way without prior permission of BARC Table of Contents Overview ...................................................................................................................................................3 Inclusion Criteria .......................................................................................................................................3 Evaluation Criteria ....................................................................................................................................4 Portfolio Capabilities...................................................................................................................... 4 Market Execution ........................................................................................................................... 7 Score -

Customer Engagement Summit 2016

OFFICIAL CUSTOMER EVENT ENGAGEMENT GUIDE SUMMIT 2016 TUESDAY, 8 NOVEMBER 2016 WESTMINSTER PARK PLAZA, LONDON TECHNOLOGY THE GREAT ENABLER PLATINUM GOLD ORGANISED BY: CustomerEngagementSummit.com @EngageCustomer #EngageSummits Find out more: www.verint.com/customer-engagement THE TEAM WELCOME Steve Hurst Editorial Director E: [email protected] T: 01932 506 304 Nick Rust WELCOME Sales Director E: [email protected] T: 01932 506 301 James Cottee Sponsorship Sales E: [email protected] T: 01932 506 309 Claire O’Brien Sponsorship Sales E: [email protected] T: 01932 506 308 Robert Cox A warm welcome to our fifth Customer Engagement Sponsorship Sales E: [email protected] Summit, now firmly established as Europe’s premier T: 01932 302 110 and most highly regarded customer and employee Katie Donaldson Marketing Executive engagement conference. E: [email protected] T: 01932 506 302 Our flagship Summit has gained a reputation for delivering leading-edge world class case-study led content in a business-like yet informal atmosphere which is conducive to delegate, speaker Claire Poole and sponsor networking. It’s a place both to learn and to do business. The overarching theme of Conference Producer this year’s Summit is ‘Technology the Great Enabler’ as we continue to recognise the critical E: [email protected] role that new technologies and innovations are playing in the fields of customer and employee T: 01932 506 300 engagement. Dan Keen We have several new elements to further improve this year’s Summit – not least our move to Delegate Sales E: [email protected] this new bigger venue, the iconic London Westminster Bridge Park Plaza Hotel following on T: 01932 506 306 from four hugely successful Summits at the London Victoria Park Plaza. -

Insight MFR By

Manufacturers, Publishers and Suppliers by Product Category 11/6/2017 10/100 Hubs & Switches ASCEND COMMUNICATIONS CIS SECURE COMPUTING INC DIGIUM GEAR HEAD 1 TRIPPLITE ASUS Cisco Press D‐LINK SYSTEMS GEFEN 1VISION SOFTWARE ATEN TECHNOLOGY CISCO SYSTEMS DUALCOMM TECHNOLOGY, INC. GEIST 3COM ATLAS SOUND CLEAR CUBE DYCONN GEOVISION INC. 4XEM CORP. ATLONA CLEARSOUNDS DYNEX PRODUCTS GIGAFAST 8E6 TECHNOLOGIES ATTO TECHNOLOGY CNET TECHNOLOGY EATON GIGAMON SYSTEMS LLC AAXEON TECHNOLOGIES LLC. AUDIOCODES, INC. CODE GREEN NETWORKS E‐CORPORATEGIFTS.COM, INC. GLOBAL MARKETING ACCELL AUDIOVOX CODI INC EDGECORE GOLDENRAM ACCELLION AVAYA COMMAND COMMUNICATIONS EDITSHARE LLC GREAT BAY SOFTWARE INC. ACER AMERICA AVENVIEW CORP COMMUNICATION DEVICES INC. EMC GRIFFIN TECHNOLOGY ACTI CORPORATION AVOCENT COMNET ENDACE USA H3C Technology ADAPTEC AVOCENT‐EMERSON COMPELLENT ENGENIUS HALL RESEARCH ADC KENTROX AVTECH CORPORATION COMPREHENSIVE CABLE ENTERASYS NETWORKS HAVIS SHIELD ADC TELECOMMUNICATIONS AXIOM MEMORY COMPU‐CALL, INC EPIPHAN SYSTEMS HAWKING TECHNOLOGY ADDERTECHNOLOGY AXIS COMMUNICATIONS COMPUTER LAB EQUINOX SYSTEMS HERITAGE TRAVELWARE ADD‐ON COMPUTER PERIPHERALS AZIO CORPORATION COMPUTERLINKS ETHERNET DIRECT HEWLETT PACKARD ENTERPRISE ADDON STORE B & B ELECTRONICS COMTROL ETHERWAN HIKVISION DIGITAL TECHNOLOGY CO. LT ADESSO BELDEN CONNECTGEAR EVANS CONSOLES HITACHI ADTRAN BELKIN COMPONENTS CONNECTPRO EVGA.COM HITACHI DATA SYSTEMS ADVANTECH AUTOMATION CORP. BIDUL & CO CONSTANT TECHNOLOGIES INC Exablaze HOO TOO INC AEROHIVE NETWORKS BLACK BOX COOL GEAR EXACQ TECHNOLOGIES INC HP AJA VIDEO SYSTEMS BLACKMAGIC DESIGN USA CP TECHNOLOGIES EXFO INC HP INC ALCATEL BLADE NETWORK TECHNOLOGIES CPS EXTREME NETWORKS HUAWEI ALCATEL LUCENT BLONDER TONGUE LABORATORIES CREATIVE LABS EXTRON HUAWEI SYMANTEC TECHNOLOGIES ALLIED TELESIS BLUE COAT SYSTEMS CRESTRON ELECTRONICS F5 NETWORKS IBM ALLOY COMPUTER PRODUCTS LLC BOSCH SECURITY CTC UNION TECHNOLOGIES CO FELLOWES ICOMTECH INC ALTINEX, INC. -

BARC Score Enterprise BI and Analytics Platforms

BARC Score Enterprise BI and Analytics Platforms Authors: Larissa Baier (Seidler), Christian Fuchs, Patrick Keller, Carsten Bange, Robert Tischler Publication: July 16th, 2018 Abstract This BARC document is the fourth edition of our BARC Score business intelligence vendor evaluation and ranking. This BARC Score evaluates enterprise BI and analytics platforms that are able to fulfill a broad set of BI requirements within the enterprise. Based on countless data points from The BI Survey and many analyst interactions, vendors are rated on a variety of criteria, from product capabilities and architecture to sales and marketing strategy, financial performance and customer feedback. This document is not to be shared, distributed or reproduced in any way without prior permission of BARC Table of Contents Overview ...................................................................................................................................................3 Inclusion Criteria .......................................................................................................................................3 Evaluation Criteria ....................................................................................................................................4 Portfolio Capabilities...................................................................................................................... 4 Market Execution .......................................................................................................................... -

Van+ Dec 2015 Aw Layout 1

December 2015 / January 2016 Volume 17 Issue 6 ISSN 1745-1736 ■ ANALYST REPORT Stratecast | Frost & Sullivan explains how CSPs will stop drowning in data and start waving ■ TALKING HEADS DIGITAL IDENTITY UXP Systems' Gemini Waghmare argues that CSPs need to empower & DATA ANALYTICS every user with a digital identity ■ POLICY Are users' digital identities at the heart of IoT becomes the Internet of Everything and then just how things are monetising CSP data? PLUS: Neural Technologies acquires Enterest ■ MDS buys LavaStorm Spend Analyzer and Bunney joins as new CEO ■ Cerillion survey finds two- thirds of businesses unhappy with pricing and payment processes ■ Viavi unveils Velocity partner programme ■ Comptel launches FWD data revenue maximisation product ■ NEC combines services with big data tools for new CEM proposition ■ DigitalRoute scores LG U+ mediation deal ■ Accedian Networks wins Telefónica global network quality partnership ■ Telarix to provide unified routing to PLDT ■ Amdocs lists deals bonanza ■ Griess becomes CSG International chief as Kanan retires ■ Read the latest news, opinion, blogs and features now at www.vanillaplus.com THE GLOBAL VOICE FOR B/OSS Real-TimeReal-Time IntelligenceIntelligence sĞƌŝƐ Zd/ ƵƐĞƐ ƌĞĂůͲƟŵĞ ĐŽŶƚĞdžƚƵĂů ĂǁĂƌĞŶĞƐƐ ƚŽ ŐŝǀĞ LJŽƵƌĐƵƐƚŽŵĞƌƐƚŚĞƌŝŐŚƚŽīĞƌŝŶƚŚĞƌŝŐŚƚƉůĂĐĞĂƚƚŚĞ ƌŝŐŚƚƟŵĞƚŚƌŽƵŐŚƚŚĞƌŝŐŚƚĐŚĂŶŶĞů͘ sĞƌŝƐZd/ŝƐƉĂƌƚŽĨƚŚĞ sĞƌŝƐΡ^^ƉƌŽĚƵĐƚƐƵŝƚĞĨƌŽŵ www.asiainfo.com CONTENTS IN THIS ISSUE 4 EDITOR’S COLUMN George Malim says CSPs can beat the GAFAs to become the gaffer with their data analytics capabilities -

Magic Quadrant for Business Intelligence and Analytics Platforms

2/26/2015 Magic Quadrant for Business Intelligence and Analytics Platforms Magic Quadrant for Business Intelligence and Analytics Platforms 23 February 2015 ID:G00270380 Analyst(s): Rita L. Sallam, Bill Hostmann, Kurt Schlegel, Joao Tapadinhas, Josh Parenteau, Thomas W. Oestreich STRATEGIC PLANNING ASSUMPTIONS VIEW SUMMARY By 2018, data discovery and data management evolution will drive most organizations to augment Traditional BI market share leaders are being disrupted by platforms that expand access to analytics and centralized analytic architectures with decentralized deliver higher business value. BI leaders should track how traditionalists translate their forwardlooking approaches. product investments into renewed momentum and an improved customer experience. By 2017, most data discovery tools will have incorporated smart data discovery capabilities to expand the reach of interactive analysis. By 2017, most business users and analysts in organizations will have access to selfservice tools to Market Definition/Description prepare data for analysis. BI and Analytics Platform Capabilities Definition By 2017, most business intelligence and analytics platforms will natively support multistructured data The BI and analytics platform market is undergoing a fundamental shift. During the past ten years, BI and analysis. platform investments have largely been in ITled consolidation and standardization projects for largescale Through 2016, less than 10% of selfservice business systemsofrecord reporting. These have tended to be highly governed and centralized, where IT intelligence initiatives will be governed sufficiently to authored production reports were pushed out to inform a broad array of information consumers and prevent inconsistencies that adversely affect the business. analysts. Now, a wider range of business users are demanding access to interactive styles of analysis and insights from advanced analytics, without requiring them to have IT or data science skills. -

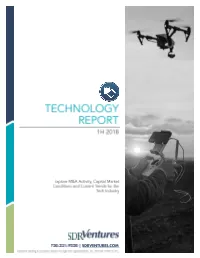

Technology Report 1H 2018

16 70,000 45 160,000 40 14 60,000 140,000 35 12 120,000 50,000 TEV ($mm) TEV ($mm) 30 10 100,000 40,000 25 8 80,000 30,000 20 6 60,000 15 20,000 Transaction Count Transaction Count 4 40,000 10 10,000 2 5 20,000 0 0 0 0 Date TEV Target Acquirer(s) Deal Overview Announced (mm) BMC Software is a global leader in digital enterprise software solutions. The acquisition of 5/29/18 BMC continues KKR's long record of supporting B2B software companies, such as its current $8,300 portfolio of Epicor and Calabrio. Microsoft agreed to acquire GitHub in a push to empower developers, boost enterprise use of 6/4/18 GitHub, and continue to build out its developer tools. More than 28 million developers use 7,500 GitHub as a community to build, collaborate and share ideas. Athenahealth provides cloud-based business services and mobile applications for medical groups and health systems. Elliott has made an activist takeover offer, believing that it could 5/7/18 6,900 help provide the operational change necessary for athenahealth to fundamentally change the Healthcare IT industry. Partners Group will take a majority stake in software development firm GlobalLogic. 5/21/18 GlobalLogic helps clients construct innovative digital products that enhance customer 2,000 engagement. Web.com is a global provider of full range internet services and online marketing tools. SIRIS 6/21/18 Capital wants to acquire Web.com believing that it can add the strategic and operational 1,885 expertise to help grow Web.com. -

Primary & Secondary Sources

Primary & Secondary Sources Brands & Products Agencies & Clients Media & Content Influencers & Licensees Organizations & Associations Government & Education Research & Data Multicultural Media Forecast 2019: Primary & Secondary Sources COPYRIGHT U.S. Multicultural Media Forecast 2019 Exclusive market research & strategic intelligence from PQ Media – Intelligent data for smarter business decisions In partnership with the Alliance for Inclusive and Multicultural Marketing at the Association of National Advertisers Co-authored at PQM by: Patrick Quinn – President & CEO Leo Kivijarv, PhD – EVP & Research Director Editorial Support at AIMM by: Bill Duggan – Group Executive Vice President, ANA Claudine Waite – Director, Content Marketing, Committees & Conferences, ANA Carlos Santiago – President & Chief Strategist, Santiago Solutions Group Except by express prior written permission from PQ Media LLC or the Association of National Advertisers, no part of this work may be copied or publicly distributed, displayed or disseminated by any means of publication or communication now known or developed hereafter, including in or by any: (i) directory or compilation or other printed publication; (ii) information storage or retrieval system; (iii) electronic device, including any analog or digital visual or audiovisual device or product. PQ Media and the Alliance for Inclusive and Multicultural Marketing at the Association of National Advertisers will protect and defend their copyright and all their other rights in this publication, including under the laws of copyright, misappropriation, trade secrets and unfair competition. All information and data contained in this report is obtained by PQ Media from sources that PQ Media believes to be accurate and reliable. However, errors and omissions in this report may result from human error and malfunctions in electronic conversion and transmission of textual and numeric data. -

The Big Data Market: 2015 – 2030 Opportunities, Challenges, Strategies, Industry Verticals & Forecasts

The Big Data Market: 2015 – 2030 Opportunities, Challenges, Strategies, Industry Verticals & Forecasts Table of Contents 1 Chapter 1: Introduction ................................................................................... 18 1.1 Executive Summary ....................................................................................................................................... 18 1.2 Topics Covered .............................................................................................................................................. 20 1.3 Historical Revenue & Forecast Segmentation ............................................................................................... 21 1.4 Key Questions Answered ............................................................................................................................... 23 1.5 Key Findings ................................................................................................................................................... 24 1.6 Methodology ................................................................................................................................................. 25 1.7 Target Audience ............................................................................................................................................ 26 1.8 Companies & Organizations Mentioned ....................................................................................................... 27 2 Chapter 2: An Overview of Big Data ................................................................ -

Weathering the Storm

INSIGHTDO MAGAZINEWNLOAD TELLABS BUSineSS anaLYSIS FOR teLECOMS PROFESSIOnaLS JULY/AUGUST 2012 LEADER CONTENTS NEWS IN BRIEF WEATHERING THE STORM 3 Timeline A round-up of some of the Operators everywhere have challenges to overcome, but regu- major stories reported in our daily news service latory regimes are particularly difficult in Asia www.totaltele.com n typically British fashion, as But there are parallels to be HETNETS we go to press with the summer drawn between Asian markets, as 7 Joined-up Iedition of Total Telecom+ our regional focus (page 10) shows. thinking torrential rain is beating against Telcos in a number of countries are the office windows. The country battling with regulatory regimes Heterogeneous networks faces the threat of severe flooding that make it difficult for them to represent a cost-effective solution to the mobile as the Met Office predicts a month’s make the most of the considerable capacity crunch, but there worth of rain will fall in one day in growth potential that still remains. Mary Lennighan is still a lot to think Editor some places. Meanwhile, incumbent operators about for telcos. Total Telecom It’s a far cry from the blue skies in East Asian markets in particular and brilliant sunshine that greeted find themselves well-placed to capi- REGIONAL REPORT us in Singapore a couple of weeks talise on a relatively new cloud 10 Focus on Asia ago as we touched down for services opportunity. Indonesian mobile CommunicAsia 2012 and the Asia Asian operators also share many providers face spectrum Communication Awards. of the same issues facing telcos shortage; India’s There was a clear message at worldwide. -

Upcoming Conferences Big Data – Q1 2018 Gretchen Frary Seay Philo Tran

Market Perspective Sector Spotlight M&A and Capital Raising Activity Public Market Performance Big Data – Q1 2018 While the Big Data headlines continue to be dominated by Upcoming Conferences topics such as artificial intelligence (“AI”), machine learning, and blockchain, Gartner’s 2018 CIO Survey recently June 17 - 21 concluded some surprising phenomenon. For example, the DataWorks Summit #1 “top differentiating technology” for companies surveyed is San Jose, CA still Business Intelligence (and has been for over a decade now), while AI came in at #7. Additionally, 451 Research June 27 - 28 Real Business Intelligence recently forecasted the total data market would surpass $146 Boston, MA billion by 2022, representing a 10%+ CAGR (3x the growth Gretchen Frary rate expected for overall global IT spending through 2020) July 10 - 20 Seay from the 2017 figure of $89 billion. Enterprise World Co-Founder & Managing Director While AI, machine learning, and other next-generation Toronto, CA Email Gretchen analytics applications are certainly becoming more and more important, there are many large organizations globally that August 20 - 23 just haven’t gotten to the point in their digital transformation Gartner Catalyst San Diego, CA journey where they can focus on those types of cutting-edge applications. Instead, a much larger focus for CIOs today is centered around cloud adoption and governance. However, only 20% of CIOs are looking to the cloud as a replacement strategy, while 80% of enterprises are managing heterogenous data portfolios that combine traditional data warehousing (e.g., IBM) with contemporary platforms like Hadoop combined with cloud services from Amazon / Google / Microsoft. -

BARC Score Data Discovery

BARC Score Data Discovery Data Preparation, Visual Analysis and Guided Advanced Analytics for Business Analysts Authors: Robert Tischler, Larissa Seidler, Julia Henneberger Publication: June 13th, 2018 Abstract This document is the second edition of BARC’s data discovery vendor evaluation using our proven ranking methodology, called BARC Score. This BARC Score evaluates data discovery tools that properly support business users through all steps of the data discovery process. Based on countless data points from The BI Survey, many analyst interactions and detailed test case demonstrations, vendors are rated on a variety of criteria, from product capabilities and architecture to sales and marketing strategy, financial performance and customer feedback. Table of Contents Overview ...................................................................................................................................................3 Inclusion Criteria .......................................................................................................................................5 Evaluation Criteria ....................................................................................................................................6 Portfolio Capabilities...................................................................................................................... 6 Market Execution ........................................................................................................................... 8 Score ....................................................................................................................................................