Harvard I BUSTNESS I SCHOOL

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Coca-Cola: a Powerful Brand – an Effective Marketing Strategy

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by eLibrary National Mining University Zaloznykh K., Kaimashnikova K. T.V. Kogemyakina, research supervisor Kriviy Rih Economic Institute of National Vadim Hetman Economic University of Kyiv COCA-COLA: A POWERFUL BRAND – AN EFFECTIVE MARKETING STRATEGY Branding is one of the most important aspects of any business, large or small, retail or business to business. It's important to spend time investing in researching, defining, and building your brand. An effective brand strategy gives you a major edge in increasingly competitive markets. To succeed in branding you must understand the needs and wants of your customers and prospects. You do this by integrating your brand strategies through your company at every point of public contact. Brand looks like the relationship between a product and its customer. A strong brand is invaluable as the battle for customers intensifies day by day. Brand is the source of a promise to your consumer. It's a foundational piece in your marketing communication and one you do not want to be without. For the last several years, when we ask people to think about a successful brand, we often ask them to think of Coca-Cola because, well, Coke is it. That’s why we decide to investigate the world’s powerful brand – coca - cola. The Coca-Cola Company is the world's largest beverage company, largest manufacturer, distributor and marketer of non-alcoholic beverage concentrates and syrups in the world, and one of the largest corporations in the United States. -

Keurig to Acquire Dr Pepper Snapple for $18.7Bn in Cash

Find our latest analyses and trade ideas on bsic.it Coffee and Soda: Keurig to acquire Dr Pepper Snapple for $18.7bn in cash Dr Pepper Snapple Group (NYSE:DPS) – market cap as of 17/02/2018: $28.78bn Introduction On January 29, 2018, Keurig Green Mountain, the coffee group owned by JAB Holding, announced the acquisition of soda maker Dr Pepper Snapple Group. Under the terms of the reverse takeover, Keurig will pay $103.75 per share in a special cash dividend to Dr Pepper shareholders, who will also retain 13 percent of the combined company. The deal will pay $18.7bn in cash to shareholders in total and create a massive beverage distribution network in the U.S. About Dr Pepper Snapple Group Incorporated in 2007 and headquartered in Plano (Texas), Dr Pepper Snapple Group, Inc. manufactures and distributes non-alcoholic beverages in the United States, Mexico and the Caribbean, and Canada. The company operates through three segments: Beverage Concentrates, Packaged Beverages, and Latin America Beverages. It offers flavored carbonated soft drinks (CSDs) and non-carbonated beverages (NCBs), including ready-to-drink teas, juices, juice drinks, mineral and coconut water, and mixers, as well as manufactures and sells Mott's apple sauces. The company sells its flavored CSD products primarily under the Dr Pepper, Canada Dry, Peñafiel, Squirt, 7UP, Crush, A&W, Sunkist soda, Schweppes, RC Cola, Big Red, Vernors, Venom, IBC, Diet Rite, and Sun Drop; and NCB products primarily under the Snapple, Hawaiian Punch, Mott's, FIJI, Clamato, Bai, Yoo- Hoo, Deja Blue, ReaLemon, AriZona tea, Vita Coco, BODYARMOR, Mr & Mrs T mixers, Nantucket Nectars, Garden Cocktail, Mistic, and Rose's brand names. -

ENERGY DRINK Buyer’S Guide 2007

ENERGY DRINK buyer’s guide 2007 DIGITAL EDITION SPONSORED BY: OZ OZ3UGAR&REE OZ OZ3UGAR&REE ,ITER ,ITER3UGAR&REE -ANUFACTUREDFOR#OTT"EVERAGES53! !$IVISIONOF#OTT"EVERAGES)NC4AMPA &, !FTERSHOCKISATRADEMARKOF#OTT"EVERAGES)NC 777!&4%23(/#+%.%2'9#/- ENERGY DRINK buyer’s guide 2007 OVER 150 BRANDS COMPLETE LISTINGS FOR Introduction ADVERTISING EDITORIAL 1123 Broadway 1 Mifflin Place The BEVNET 2007 Energy Drink Buyer’s Guide is a comprehensive compilation Suite 301 Suite 300 showcasing the energy drink brands currently available for sale in the United States. New York, NY Cambridge, MA While we have added some new tweaks to this year’s edition, the layout is similar to 10010 02138 our 2006 offering, where brands are listed alphabetically. The guide is intended to ph. 212-647-0501 ph. 617-715-9670 give beverage buyers and retailers the ability to navigate through the category and fax 212-647-0565 fax 617-715-9671 make the tough purchasing decisions that they believe will satisfy their customers’ preferences. To that end, we’ve also included updated sales numbers for the past PUBLISHER year indicating overall sales, hot new brands, and fast-moving SKUs. Our “MIA” page Barry J. Nathanson in the back is for those few brands we once knew but have gone missing. We don’t [email protected] know if they’re done for, if they’re lost, or if they just can’t communicate anymore. EDITORIAL DIRECTOR John Craven In 2006, as in 2005, niche-marketed energy brands targeting specific consumer [email protected] interests or demographics continue to expand. All-natural and organic, ethnic, EDITOR urban or hip-hop themed, female- or male-focused, sports-oriented, workout Jeffrey Klineman “fat-burners,” so-called aphrodisiacs and love drinks, as well as those risqué brand [email protected] names aimed to garner notoriety in the media encompass many of the offerings ASSOCIATE PUBLISHER within the guide. -

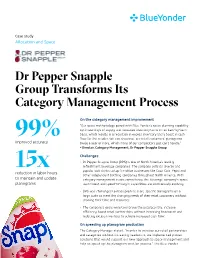

Dr Pepper Snapple Group Transforms Its Category Management Process

Case study Allocation and Space Dr Pepper Snapple Group Transforms Its Category Management Process On the category management improvement “Our space methodology paired with Blue Yonder’s space planning capability optimizes days of supply and increases inventory turns on an item-by-item basis, which results in a reduction in excess inventory and a boost in cash 99% flow for the retailer. We can also reset our retail customers’ planograms improved accuracy twice a year or more, which many of our competitors just can’t handle.” - Director, Category Management, Dr Pepper Snapple Group Challenges • Dr Pepper Snapple Group (DPS) is one of North America’s leading refreshment beverage companies. The company sells its diverse and 15x popular soft drinks to top franchise businesses like Coca-Cola, Pepsi and reduction in labor hours other independent bottling companies throughout North America. With to maintain and update category management a core competency, the beverage company’s space, planograms assortment and speed-to-insight capabilities are continuously evolving. • DPS was challenged to mass produce store-specific planograms on a large scale to meet the changing needs of their retail customers without draining their time and resources. • The company’s goals were to improve the accuracy rate, increase efficiency, boost retail partnerships without increasing headcount and reducing excess inventory to achieve increased cash flow. On speeding up planogram production The Category Manager stated, “In order to increase our retail partnerships and categories without increasing headcount, we implemented proven solutions that would support our new approach to space management and help us speed up the planogram creation process.” The Blue Yonder solution automated the large-scale production of Blue Yonder’s expertise optimized, store-specific planograms, increasing Dr Pepper Snapple Group’s accuracy rate to 99 percent. -

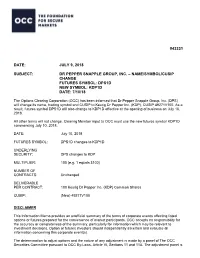

Dr Pepper Snapple Group, Inc. – Name/Symbol/Cusip Change Futures Symbol: Dps1d New Symbol: Kdp1d Date: 7/10/18

#43331 DATE: JULY 9, 2018 SUBJECT: DR PEPPER SNAPPLE GROUP, INC. – NAME/SYMBOL/CUSIP CHANGE FUTURES SYMBOL: DPS1D NEW SYMBOL: KDP1D DATE: 7/10/18 The Options Clearing Corporation (OCC) has been informed that Dr Pepper Snapple Group, Inc. (DPS) will change its name, trading symbol and CUSIP to Keurig Dr Pepper Inc. (KDP), CUSIP 49271V100. As a result, futures symbol DPS1D will also change to KDP1D effective at the opening of business on July 10, 2018. All other terms will not change. Clearing Member input to OCC must use the new futures symbol KDP1D commencing July 10, 2018. DATE: July 10, 2018 FUTURES SYMBOL: DPS1D changes to KDP1D UNDERLYING SECURITY: DPS changes to KDP MULTIPLIER: 100 (e.g. 1 equals $100) NUMBER OF CONTRACTS: Unchanged DELIVERABLE PER CONTRACT: 100 Keurig Dr Pepper Inc. (KDP) Common Shares CUSIP: (New) 49271V100 DISCLAIMER This Information Memo provides an unofficial summary of the terms of corporate events affecting listed options or futures prepared for the convenience of market participants. OCC accepts no responsibility for the accuracy or completeness of the summary, particularly for information which may be relevant to investment decisions. Option or futures investors should independently ascertain and evaluate all information concerning this corporate event(s). The determination to adjust options and the nature of any adjustment is made by a panel of The OCC Securities Committee pursuant to OCC By-Laws, Article VI, Sections 11 and 11A. The adjustment panel is comprised of representatives from OCC and each exchange which trades the affected option. The determination to adjust futures and the nature of any adjustment is made by OCC pursuant to OCC By- Laws, Article XII, Sections 3, 4, or 4A, as applicable. -

Coca-Cola La Historia Negra De Las Aguas Negras

Coca-Cola La historia negra de las aguas negras Gustavo Castro Soto CIEPAC COCA-COLA LA HISTORIA NEGRA DE LAS AGUAS NEGRAS (Primera Parte) La Compañía Coca-Cola y algunos de sus directivos, desde tiempo atrás, han sido acusados de estar involucrados en evasión de impuestos, fraudes, asesinatos, torturas, amenazas y chantajes a trabajadores, sindicalistas, gobiernos y empresas. Se les ha acusado también de aliarse incluso con ejércitos y grupos paramilitares en Sudamérica. Amnistía Internacional y otras organizaciones de Derechos Humanos a nivel mundial han seguido de cerca estos casos. Desde hace más de 100 años la Compañía Coca-Cola incide sobre la realidad de los campesinos e indígenas cañeros ya sea comprando o dejando de comprar azúcar de caña con el fin de sustituir el dulce por alta fructuosa proveniente del maíz transgénico de los Estados Unidos. Sí, los refrescos de la marca Coca-Cola son transgénicos así como cualquier industria que usa alta fructuosa. ¿Se ha fijado usted en los ingredientes que se especifican en los empaques de los productos industrializados? La Coca-Cola también ha incidido en la vida de los productores de coca; es responsable también de la falta de agua en algunos lugares o de los cambios en las políticas públicas para privatizar el vital líquido o quedarse con los mantos freáticos. Incide en la economía de muchos países; en la industria del vidrio y del plástico y en otros componentes de su fórmula. Además de la economía y la política, ha incidido directamente en trastocar las culturas, desde Chamula en Chiapas hasta Japón o China, pasando por Rusia. -

The Minute Maid Company WORLDWIDE REVIEW

now & always now is why we’re confident about always Even amid uncertain economic times, we refreshed more thirsty people with more of our products in 1998 than ever before. Nearly a billion unit cases more. M. DOUGLAS IVESTER, Chairman of the Board and Chief Executive Officer, at a noodle shop in Tokyo, one of numerous customer visits he made last year. Dear Fellow Share Owners, The economic conditions we saw in a number of marke t s in 1998 — such as Ja p a n , G e rm a ny,Thailand and Brazil — “ N ow and alway s ” :T h a t , in three wo rd s , is how we view c e rtainly dampened our short - t e rm re s u l t s . But they re m i n d this bu s i n e s s . us why we manage this business with a view to the long That dual vision, si m ultaneously nearsighted and fars i g h t e d , t e rm . Global economic wo rries are new to some compa- is only natural for a Company with our history and our future. n i e s , but in a sense, we have seen this movie before. In 113 And I can’t think of another year when it was more useful or ye a rs ,t h e re is scarcely a place where we have not we a t h e red mo r e appro p ri a t e. economic storm s . Last ye a r, as our stock slid from its July high, pundits we re Our unparalleled business system was built by decades of quick to pronounce us and other multinational companies i nve s t m e n t , commitment and fa i t h . -

The Cola Wars

Journal of Business Case Studies – March/April 2009 Volume 5, Number 2 Brands As Ideological Symbols: The Cola Wars Praveen Aggarwal, University of Minnesota Duluth, USA Kjell Knudsen, University of Minnesota Duluth, USA Ahmed Maamoun, University of Minnesota Duluth, USA ABSTRACT The Coca-Cola Company is the undisputed global leader in the cola industry. Despite its size and marketing savvy, the company has faced a barrage of competition from new companies in the Middle East and some parts of Europe. These companies have tried to create a niche for themselves by tapping into the anti-U.S. sentiment that prevails among a section of population in these markets. We review three such competitors, Zam Zam Cola, Mecca Cola, and Qibla Cola and their strategies for challenging the global giant. Keywords: Cola Wars, Anti-U.S. sentiment, Beverages industry. THE COCA-COLA COMPANY ith sales and operations in over 200 countries, The Coca-Cola Company is the worlds’ largest producer and marketer of nonalcoholic beverage concentrates in the world. While Coca-Cola W beverages have been sold in the United States since 1886, the company has made significant advances in its global reach and dominance in the last few decades. Of the roughly 50 billion beverage servings consumed worldwide on any given day. The Coca-Cola Company serves 1.3 billion of those servings. In terms of worldwide sales of nonalcoholic beverages, the company claimed a 10% market share in 2004, while employing approximately 50,000 people. As of 2004, the company divided its global operations into six segments or “operating groups”: • North America • Africa • Asia • Europe, Eurasia and Middle East • Latin America • Corporate The relative size and contributions of these segments are given in Table 1. -

Strategic Analysis of the Coca-Cola Company

STRATEGIC ANALYSIS OF THE COCA-COLA COMPANY Dinesh Puravankara B Sc (Dairy Technology) Gujarat Agricultural UniversityJ 991 M Sc (Dairy Chemistry) Gujarat Agricultural University, 1994 PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS FOR THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION In the Faculty of Business Administration Executive MBA O Dinesh Puravankara 2007 SIMON FRASER UNIVERSITY Summer 2007 All rights reserved. This work may not be reproduced in whole or in part, by photocopy or other means, without permission of the author APPROVAL Name: Dinesh Puravankara Degree: Master of Business Administration Title of Project: Strategic Analysis of The Coca-Cola Company. Supervisory Committee: Mark Wexler Senior Supervisor Professor Neil R. Abramson Supervisor Associate Professor Date Approved: SIMON FRASER UNIVEliSITY LIBRARY Declaration of Partial Copyright Licence The author, whose copyright is declared on the title page of this work, has granted to Simon Fraser University the right to lend this thesis, project or extended essay to users of the Simon Fraser University Library, and to make partial or single copies only for such users or in response to a request from the library of any other university, or other educational institution, on its own behalf or for one of its users. The author has further granted permission to Simon Fraser University to keep or make a digital copy for use in its circulating collection (currently available to the public at the "lnstitutional Repository" link of the SFU Library website <www.lib.sfu.ca> at: ~http:llir.lib.sfu.calhandle/l8921112>)and, without changing the content, to translate the thesislproject or extended essays, if technically possible, to any medium or format for the purpose of preservation of the digital work. -

Introducing Keurig Dr Pepper

Introducing Keurig Dr Pepper Investor Presentation Creating a New Challenger In the Beverage Industry Highly Confidential January 2018 Forward Looking Statements Certain statements contained herein are “forward-looking statements” within the meaning of applicable securities laws and regulations. These forward-looking statements can generally be identified by the use of words such as “anticipate,” “expect,” “believe,” “could,” “estimate,” “feel,” “forecast,” “intend,” “may,” “plan,” “potential,” “project,” “should,” “will,” “would,” and similar words, phrases or expressions and variations or negatives of these words, although not all forward-looking statements contain these identifying words. Forward-looking statements by their nature address matters that are, to different degrees, uncertain, such as statements regarding the estimated or anticipated future results of the combined company following the proposed merger, the anticipated benefits of the proposed merger, including estimated synergies, the expected timing of completion of the proposed merger and related transactions and other statements that are not historical facts. These statements are based on the current expectations of Keurig Green Mountain Parent Holdings Corp. and Dr Pepper Snapple Group, Inc. management and are not predictions of actual performance. These forward-looking statements are subject to a number of risks and uncertainties regarding the combined company’s business and the proposed merger and actual results may differ materially. These risks and uncertainties -

1 BAB I PENDAHULUAN A. Latar Belakang Masalah Pesatnya

BAB I PENDAHULUAN A. Latar Belakang Masalah Pesatnya perkembangan media cetak dan elektronik memunculkan persaingan di industri saat ini. Perusahaan berkompetisi untuk mempertahankan brand position di benak konsumen dengan menciptakan standarisasi mutu maupun peningkatan kualitas pelayanan melalui strategi promosi. Banyak cara yang dilakukan oleh perusahaan agar brand – nya dapat merebut hati masyarakat. Beberapa brand yang telah memiliki nama besar tentunya memiliki cara untuk bertahan agar tidak digeser oleh kompetitor dan meraih posisi terbaik. Keseluruhan prestasi yang diraih oleh sebuah brand besar pun tidak dapat diraih secara instan melainkan perlu melalui tahapan dalam kurun waktu yang juga tidak singkat. Posisi sebuah produk ditentukan juga dari bagaimana perusahaan mengimplementasikan perencanaan dengan baik dan tepat sasaran. Brand position diraih melalui proses perencanaan yang matang dengan menghasilkan suatu keputusan untuk memperkuat posisi merek. Advertising campaign merupakan salah satu faktor esensial dalam menunjukkan eksistensi suatu produk, bukan hanya sekedar kualitas produk tetapi bagaimana cara mengkomunikasikan kepada masyarakat agar diterima dan memperoleh tempat di tengah persaingan. 1 Advertising campaign muncul tidak serta merta dengan sendirinya, melainkan terdapat beberapa hal yang perlu dipertimbangkan, karena tujuannya adalah mengkomunikasikan merek. Merumuskan komunikasi untuk mencapai tanggapan yang diinginkan akan menuntut pemecahan tiga masalah: 1, apa yang harus dikatakan (strategi pesan), 2, bagaimana mengatakannya (strategi kreatif) dan 3, siapa yang harus mengatakannya (sumber pesan) (Kotler, 2007 : 214). Sebagai bagian dari strategi kreatif dalam Integrated Marketing Communication (IMC), advertising campaign dirancang melalui berbagai riset sebelum akhirnya diimplementasikan. Berbagai riset yang dilakukan antara lain riset konsumen yang mencakup target market dan riset kompetisi yakni apa saja yang dilakukan oleh kompetitor terutama kompetitor utama. -

Annual Report 2018 ABN 26 004 139 397 Contents Page at Coca-Cola Amatil, Our Products And

Annual Report 2018 ABN 26 004 139 397 Contents Page At Coca-Cola Amatil, our products and 2018: Our Year 2 people delight millions, and create moments Where We Operate 4 of happiness and possibilities every day. Chairman’s Review 6 Group Managing Director’s Review 8 Operating with purpose matters – Board of Directors 10 it’s not just what we do, it’s how we Group Leadership Team 12 do it. As a multi-beverages powerhouse, Corporate Governance 14 we are committed to delivering on our Operating and Financial Review 16 growth agenda while building sustainable Directors’ Report 49 Remuneration Report 52 outcomes across the regions in which Financial Report 75 we operate. Independent Auditor's Report 127 Auditor's Independence Declaration 131 We’ve developed in more ways than Shareholder Information 132 one – for our shareholders, customers, Five-Year Financial History 135 consumers, communities and our Glossary 136 people, and we’ll continue to create Directories 137 millions of moments of happiness Calendar of Events 2019 137 and possibilities … every day. Coca-Cola Amatil Limited Annual Report 2018 1 2018: OUR YEAR 2018 was a transition year for the Group, with earnings impacted by the planned investment in our Accelerated Australian Growth Plan and the implementation of container deposit schemes, compounded by economic factors in Indonesia and operational challenges in Papua New Guinea. Our performance in many areas remained strong, with New Zealand & Fiji delivering another year of strong EBIT growth and Alcohol & Coffee achieving another year of double-digit EBIT growth. We are proud of the progress we have made on our plans and commitments, and saw encouraging signs in Australian Beverages and Indonesia in the second half.