ANNUAL REPORT 2006 Shaw Communications ANNUAL REPORT August 31, 2006

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Broadcasting Decision CRTC 2013-6

Broadcasting Decision CRTC 2013-6 PDF version Route reference: 2012-370 Ottawa, 9 January 2013 Novus Entertainment Inc. Metro Vancouver, British Columbia Application 2012-0528-7, received 27 April 2012 Public hearing in Montréal, Quebec 10 September 2012 Video-on-demand service The Commission approves an application for a broadcasting licence to operate a regional video-on-demand service. The application 1. Novus Entertainment Inc. (Novus) filed an application for a broadcasting licence to operate a regional video-on-demand (VOD) programming undertaking to serve Metro Vancouver, British Columbia. The Commission did not receive any interventions in connection with this application. 2. Novus is controlled by Terrence C. Hui. 3. The applicant indicated that the new VOD service would consist primarily of feature films, but would also include other types of programs, such as television series, documentaries, children’s programs, animation, music, sports, adult programming and community programming. 4. Novus confirmed that it would make its VOD program offering available to customers in both official languages. While the programming would be predominantly in English, the applicant made a commitment to offer approximately 5% of all programming in French. In addition, the applicant indicated that approximately 5% of the service’s programming would be in either Mandarin or Cantonese. 5. In its application, Novus indicated that it would abide by the standard requirements for VOD services, set out in the appendix to Broadcasting Regulatory Policy 2011- 59-1, and proposed to abide by an additional condition of licence requiring it to allocate exclusively to the production of community programming all revenues generated by a subscriber fee for the distribution of community programming offered on the service. -

Broadcasting Decision CRTC 2009-145

Broadcasting Decision CRTC 2009-145 Ottawa, 17 March 2009 Various specialty, pay, pay-per-view, video on demand and, satellite-to-cable undertakings and community-based television programming undertakings Across Canada Administrative renewals 1. The Commission renews the broadcasting licences for the various programming undertakings set out in the appendix to this decision from 31 August 2009 to 31 August 2010, subject to the terms and conditions in effect under the current licences. 2. This decision will enable the Commission to consider the further renewal of various specialty, pay, pay-per-view, video on demand and satellite-to-cable undertaking licences by taking into account the determinations in Regulatory frameworks for broadcasting distribution undertakings and discretionary programming services, Broadcasting Public Notice CRTC 2008-100, 30 October 2008. 3. In addition, this decision will enable the Commission to consider the further renewal of community-based television programming undertakings by taking into account the determinations that will result from its review of the regulatory frameworks for community-based media to be scheduled in November 2009. 4. It will also permit the Commission to consider the renewal of the major conventional broadcasters at public hearings to be scheduled in April 2009 (CTV, Canwest, Rogers, TVA) and September 2009 (CBC/SRC). 5. This decision does not dispose of any substantive issue that may exist with respect to the renewal of these licences and interested parties will have an opportunity to comment at the appropriate time. Secretary General This decision is to be appended to each licence. It is available in alternative format upon request and may also be examined PDF Format or in HTML at the following Internet site: http://www.crtc.gc.ca. -

Submission Regarding Competition Bureau Market Study Notice: Competition in Broadband Services

Submission Regarding Competition Bureau Market Study Notice: Competition in Broadband Services August 31, 2018 Executive Summary ES1 The Canadian broadband market is extremely competitive. Driven primarily by facilities-based competitors, Canada is one of the few countries in the world where almost every consumer across the country enjoys the choice between competing physical broadband networks. This choice in turn has continuously driven network investment, amongst the highest in the world, as the carriers have competed by evolving from twisted pair and co-axial cable to DSL and cable/fibre hybrids to fibre to the home. ES2 Competition has driven facilities-based competitors to invest $69.2 billion over the past 10 years to satisfy consumer demand for faster and higher capacity wireline services. Demand increased ten-fold over the 10-year period. These investments now provide world-leading networks to 92% of Canadian households. At the same time, this level of competition has reduced the price of higher speed services by 3% per year since the CRTC started tracking these plans. In short, the facilities-based providers in Canada have delivered more internet to Canadians for a lower price. ES3 Resellers, on the other hand, while making inroads, have had a very modest impact on the market and industry. Since their inception, they have won a 13% market share of a very capital-intensive industry despite only having invested less than one-half of one percent the investment facilities-based providers have made in new and innovative services. After 15 years of mandated wholesale resale, resellers have not moved up the Ladder of Investment. -

Major National Associations Canadian Cable of Farm

Major National Associations Major National Associations Page, Valleyfield Transvision Inc.; Ken Stein, Shaw Jerianne Timmerman, assoc gen counsels; Karen Cabletelevision Communications Inc.; John A. Wilson, Comlink Kirsch, VP regulatory affrs; Ann Zuvekas, staff atty; Systems Inc.; Glenn Wong, Rogers Cablesystems Joan Sutton, rsch asst. Ltd. Advertising Bureau Information Resource Center: Vivian Pollard, VP; Tina Nunn, Virgie Coulboum, Brian Baxter, Sarah Inc. (CAB) Fitzsimmons & Steven Mitchel, info specialists. Media Rating Management and Marketing Information Headquarters: 830 3rd Ave., New York, NY 10022. Systems: Darrell Poe, VP; (212) 508 -1200. FAX: (212) 832 -3268. Web Site: Oscar Moreno, sr database engr; hffp://www.cabletvadbureau.com. Council Kenneth Savitsky, network administrator; Brian Campblin, software developer; Maruthi Tella, Executives: Steve Heyer, chmn; Joseph W. Ostrow, Headquarters: 200 W. 57th St., Suite 204, New York, applications programmer; Cindy Stemerick, tech pres/CEO; Robert H. Alter, vice -chmn; Kim Kelly, NY 10019. (212) 765-0200. FAX: (212) 765 -1868. facilities coord; Aloys Nang, support asst. vice -chmn; George Bodenheimer, treas; Curtis Richard Weinstein, exec Tim Symonds, sec; Kevin Barry, VP loc sls & mktg; Officers: dir; Brooks Meetings and Conference Services: Kathy Muller, sr (chmn of bd MRC), USA Network, New York, NY; Jonathon B. Sims, VP rsch; Ken Damsky, VP finance VP; Giulia Frumento & Monica Snipes, conference David Poltrack (ex officio MRC), CBS, New York, NY; & admin, asst sec, asst treas; Lynne Nordone, VP planners; Jonathan Feinberg, dir travel, convention & Ron Werth (chmn Radio Committee), Westwood One, member svcs; Steve Raddock, VP creative svcs; Jerry housing; Yvette Harris, York, housing coord; Teresa Dominus, VP network sls & mktg. -

Annual Report 2010 Annual Report 2010

Score Score Score Together is We, the leading entertainment and communications Amazing. company, deliver exceptional customer experience through Amazing. outstanding people sharing Shaw Values. ACCOUNTABLE BALANCE CUSTOMER FOCUSED INTEGRITY LOYALTY POSITIVE, CAN DO ATTITUDE TEAM PLAYER Annual Report 2010 Score Score Score Score 1 Report to Shareholders 4 Management’s Discussion and Analysis 64 Management’s Responsibility for Financial Statements and Report on Internal Control over Financial Reporting 66 Independent Auditors’ Reports 68 Consolidated Financial Statements 72 Notes to Consolidated Financial Statements 119 Five Years in Review 120 Shareholders’ Information 121 Corporate Information The Annual General Meeting of Shareholders will be held on January 13 , 201 1 at 11:00 am (Mountain Time) at the Shaw Barlow Trail Building, 2400 – 32 Avenue NE, Calgary, Alberta. When we work together, we can achieve amazing things. We have never been more committed to providing exceptional customer service while creating best in class products and services. We are committed to the communities where we live and work and to our 13,000 employees who make it possible. We are working together, one team – one Shaw, towards an amazing future. 06 265 07 356 08 455 09 506 10 515 FREE CASH FLOW 06 103 06 265 07 201 07 356 08 304 08 455 09 352 09 506 10 372 10 515 DVIDENDS FREE CASH FLOW 06 103 06 1.1 07 201 07 1.2 08 304 08 1.4 09 352 09 1.5 10 372 10 1.8 DVIDENDS EBITDA (in billions) 06 265 07 356 06 2.5 06 1.1 08 455 07 2.8 07 1.2 09 506 08 3.1 08 1.4 -

Wireless Competition in Canada: an Assessment

Volume 6•Issue 27•September 2013 WIRELESS COMPETITION IN CANADA: AN ASSESSMENT Jeffrey Church † Professor, Department of Economics and Director, Digital Economy Program, The School of Public Policy, University of Calgary Andrew Wilkins † Research Associate, Digital Economy Program, The School of Public Policy, University of Calgary SUMMARY If there’s one thing Canadians agree on, it’s that Canada’s wireless industry can and should be more competitive. The federal government is on side with the policy objective of having four carriers in every region and has responded with policies that provide commercial advantages to entrants. But, the rub is that there has not been a study that actually assesses the state of competition in wireless services in Canada, until now. Those in favour of policies that will promote and sustain entry point to Canada’s high average revenue per user and low wireless penetration rate (mobile connections per capita) as evidence that there is insufficient competition. The difficulty is that the facts are not consistent with this simplistic analysis. Measurements of wireless penetration are skewed toward countries that maintain the Calling Party Pays Protocol and favour pay-as-you-go plans, both of which encourage inflated user counts. Canada’s participation per capita on monthly plans and minutes of voice per capita are not outliers. Moreover, in terms of smartphone adoption and smartphone data usage, Canada is a global leader, contributing to high average revenue per user. Consistent with being world leaders in the rollout of high speed wireless networks, Canada lead its peer group in capital expenditures per subscriber in 2012: the competition of importance to Canadians is not just over price, but also over the quality of wireless networks. -

View Annual Report

Focused on the future. 2014 Annual Report 1 Report to Shareholders 4 Management’s Discussion and Analysis 57 Management’s Responsibility for Financial Statements and Report on Internal Control over Financial Reporting 59 Independant Auditors’ Reports 63 Consolidated Financial Statements 68 Notes to Consolidated Financial Statements 122 Five Years in Review 123 Shareholders’ Information 124 Corporate Information The Annual General Meeting of Shareholders will be held on January 14, 2015 at 11:00 am (Mountain Time) at the Shaw Barlow Trail Building, 2400 – 32 Avenue NE, Calgary, Alberta. Shaw Communications Inc. 2014 Annual Report At Shaw, every decision we make, and every initiative we launch, is driven by customer choice and the imperative to bring quality, reliability, innovation and value to the customer and viewer experience. Shaw Communications Inc. 2014 Annual Report Revenue* Dividends Figures in billions Figures in millions 5.2 5.1 485 5.0 445 4.7 416 391 372 3.7 10 11 12 13 14 10 11 12 13 14 Operating income before Free cash flow* restructuring costs and Figures in millions amortization* Figures in billions 698 2.3 2.2 2.1 2.1 617 604 1.8 515 482 10 11 12 13 14 10 11 12 13 14 *Financial information for fiscal 2010 is prepared in accordance with previous Canadian generally accepted accounting principles. Shaw Communications Inc. REPORT TO SHAREHOLDERS August 31, 2014 Dear Fellow Shareholders: Our performance in fiscal 2014 reflects our continued focus on the delivery of exceptional experiences and leading technology to our customers and viewers, a disciplined focus on operational efficiencies, and sound capital management creating value for all stakeholders. -

Anti-Raffle Policy Hurts Local Groups by JEFF NAGEL Money Raised Last Year Is Set Aside to Ern Health, Authority

AimingarrOws : ' , i!'!~ LocalMP.sa~)Sa~ece.nt ieport:i The whiSke~JaCl~ archers , :..:...-./.....~.:...):,.....~:....:.......,.~:... ... should bee~nough;;¢o::keep,the fling arrowsattheir3-D Stint-at the Sout h Pole= '.., : -moratorium off bffsh:or:~ oil tournament at !C'opperside : kCOMMUNi~:B/ i, / " ~~ .drilling..&NEWS/~8.-: ~ Stables I\sPoRiI'~:B4! - • . .. • :.:..: '.. :," . : ... .:. i " ."! , . ,. ?.,:. ):.. -: ., • ,. - • ": .: , ., ,,- '. - • . 4 • " . ............. "- O --O i $ !.00. PLUS7 ¢:!GS . ($1A0 plus-8¢GST - i-outside of the.Terrace are 2 T N D R D Anti-raffle policy hurts local groups By JEFF NAGEL Money raised last year is set aside to ern Health, Authority. Because the NHA had been threatened by budget cuts. was effective. .A GOVERNMENT crackdown on who payfor this month's Christmas dinner, but is:a government-linanced health provider. ]'he foundation's latest raflli" applica- -"With our little raffle, if we're lucky, can hold raffles is threatening an inno- 2005 may norbe as jolly, gaming money is off limits, tion has been rcjeqted because it supports we make $3,000 or $4,000," Kerr said/ vative school .band program and annual. The raffle money'also helps Clielits go :/:: Up until.April:of this.year the.govern- education;which the province pays for. "We .were try!rig: to have two p~r year Christmas dinners for•the mentally handi- on day trips throughout•the• region and.haS< ment agent'.:s Office here had •authOrity tO .!:Gaming funds, ~including..licensed :) ~ One in thefal/and one-in the spring- to capped.. ' . ".. : .-:-. i. i""i . : ••paidfora variety•of clUbhouse:amenitieS .approve-raffieapplicati0ns • themselves,: .gaming moneys, ~:an .t be u'sed::foritrans- ' misethemajority.of thembrleyJ' ~. -

22-A 2012 Social Baseline Report

APPENDIX 22-A 2012 SOCIAL BASELINE REPORT TM Seabridge Gold Inc. KSM PROJECT 2012 Social Baseline Report Rescan™ Environmental Services Ltd. Rescan Building, Sixth Floor - 1111 West Hastings Street Vancouver, BC Canada V6E 2J3 January 2013 Tel: (604) 689-9460 Fax: (604) 687-4277 Executive Summary Seabridge Gold Inc. is proposing to develop the KSM Project (the Project), a gold, copper, silver, and molybdenum mine located in northwestern British Columbia. The proposed Project is approximately 950 km northwest of Vancouver and 65 km northwest of Stewart, within 30 km of the British Columbia–Alaska border (Figure 1.2-1). The estimated initial capital cost of the Project is US$5.3 billion. The Project is split between two geographical areas: the Mine Site and Processing and Tailing Management Area (PTMA), connected by twin 23-km tunnels (Mitchell-Treaty Twinned Tunnels; Figure 1.2-2). The Mine Site will be located south of the closed Eskay Creek Mine, within the Mitchell Creek, McTagg Creek, and Sulphurets Creek valleys. Sulphurets Creek is a main tributary of the Unuk River, which flows to the Pacific Ocean. The PTMA will be located in the upper tributaries of Teigen and Treaty creeks. Both creeks are tributaries of the Bell-Irving River, which flows into the Nass River and Pacific Ocean. The PTMA is located about 19 km southwest of Bell II on Highway 37. This social baseline report presents a comprehensive overview of the past and present social environment and context of the proposed Project, including patterns, trends, and changes over time. It outlines relevant social factors for which data on communities in the Project area are available, such as society and governance; population and demographics; education, skills and training (level of achievement, elementary, secondary, post-secondary, and adult education); health and social services (facilities, services, trends, and issues); recreation; protection services (crime index, police, fire, and ambulance); and infrastructure (utilities, communications, transportation, and housing). -

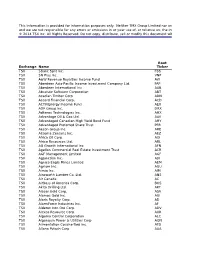

This Information Is Provided for Information Purposes Only. Neither

This information is provided for information purposes only. Neither TMX Group Limited nor any of its affiliated companies represents, warrants or guarantees the accuracy or completeness of the information contained in this document and we are not responsible for any errors or omissions in or your use of, or reliance on, the information provided. © 2014 TSX Inc. All Rights Reserved. Do not copy, distribute, sell or modify this document without TSX Inc.'s prior written consent. Root Exchange Name Ticker TSX 5Banc Split Inc. FBS TSX 5N Plus Inc. VNP TSX A&W Revenue Royalties Income Fund AW TSX Aberdeen Asia-Pacific Income Investment Company Ltd. FAP TSX Aberdeen International Inc. AAB TSX Absolute Software Corporation ABT TSX Acadian Timber Corp ADN TSX Accord Financial Corp. ACD TSX ACTIVEnergy Income Fund AEU TSX ADF Group Inc. DRX TSX Adherex Technologies Inc. AHX TSX Advantage Oil & Gas Ltd. AAV TSX Advantaged Canadian High Yield Bond Fund AHY TSX Advantaged Preferred Share Trust PFR TSX Aecon Group Inc. ARE TSX AEterna Zentaris Inc. AEZ TSX Africa Oil Corp. AOI TSX Africo Resources Ltd. ARL TSX AG Growth International Inc AFN TSX Agellan Commercial Real Estate Investment Trust ACR TSX AGF Management Limited AGF TSX AgJunction Inc. AJX TSX Agnico Eagle Mines Limited AEM TSX Agrium Inc. AGU TSX Aimia Inc. AIM TSX Ainsworth Lumber Co. Ltd. ANS TSX Air Canada AC TSX AirBoss of America Corp. BOS TSX Akita Drilling Ltd. AKT TSX Alacer Gold Corp. ASR TSX Alamos Gold Inc. AGI TSX Alaris Royalty Corp. AD TSX AlarmForce Industries Inc. AF TSX Alderon Iron Ore Corp. -

Arzinbooks-Karbordi94.Pdf

ﺑﺴﻤﻪ ﺗﻌﺎﻟﻲ ﻗﺎﺑﻞ ﺗﻮﺟﻪ اﻋﻀﺎء ﻫﻴﺌﺖ ﻋﻠﻤﻲ داﻧﺸﮕﺎه ﻫﺎ، ﻛﺘﺎﺑﺨﺎﻧﻪ ﻫﺎ، ﻣﺮاﻛﺰ ﺗﺤﻘﻴﻘﺎﺗﻲ و ﭘﮋوﻫﺸﻲ و ﺳﺎﻳﺮ ﻋﻼﻗﻪ ﻣﻨﺪان ﺑﻪ ﻛﺘﺐ ﻻﺗﻴﻦ داﻧﺶ ارزﻳﻦ ﺟﻬﺎن در ﺳﻴﺰدﻫﻤﻴﻦ ﻧﻤﺎﻳﺸﮕﺎه ﺑﻴﻦ اﻟﻤﻠﻠﻲ ﻛﺘﺐ ﻛﺎر ﺑﺮدي داﻧﺸﮕﺎﻫﻲ ﺑﺎ ﻋﺮﺿﻪ ﺣﺪود 3000 ﻋﻨﻮان از ﺟﺪﻳﺪﺗﺮﻳﻦ ﻛﺘﺐ ﻣﻨﺘﺸﺮ ،ه ،ه ﻋﻤﺪﺗﺎ 2014 و 2015 از ﻣﻌﺘﺒﺮﺗﺮﻳﻦ ﻧﺎﺷﺮان ﺟﻬﺎن در زﻣﻴﻨﻪ ﻫﺎي ﻋﻠﻮم اﻧﺴﺎﻧﻲ ، ﻓﻨﻲ و ﻣﻬﻨﺪﺳﻲ ، ﻫﻨﺮ و ﻣﻌﻤﺎري ، ﻋﻠﻮم ﭘﺎﻳﻪ ، ﭘﺰﺷﻜﻲ و داروﺳﺎزي ﺣﻀﻮر ﻓﻌﺎل دارد . ﻛﺘﺎب ﻫﺎي ﻧﺎﺷﺮان ﻣﻌﺘﺒﺮ زﻳﺮ ﺗﻮﺳﻂ داﻧﺶ ارزﻳﻦ ﺟﻬﺎن در ﺳﻴﺰدﻫﻤﻴﻦ ﻧﻤﺎﻳﺸﮕﺎه ﺑﻴﻦ اﻟﻤﻠﻠﻲ ﻛﺘﺐ ﻛﺎرﺑﺮدي ﻋﺮﺿﻪ ﻣﻲ ﮔﺮدد: IGI Global / Pharmaceutical Press / Guilford Press / SAGE / Hart Publishing / Royal Society of Chemistry (RSC) Berghahn Publishing / Hurst Publishers / Jessica Kingsley Publishers / Pluto Press / I.B.Tauris / SAQI Cambridge Scholars Publishing / Oxford University press / American Society of Health-System Pharmacists ﺟﻬﺖ درﻳﺎﻓﺖ ﻓﺎﻳﻞ اﻛﺴﻞ ﻛﺘﺐ ﻧﻤﺎﻳﺸﮕﺎه ﻣﻲ ﺗﻮاﻧﻴﺪ ﺑﻪ ﺳﺎﻳﺖ ﺷﺮﻛﺖ ﻣﺮاﺟﻌﻪ ﻧﻤﻮده ﺎﻳ ﺗﻤﺎس ﺣﺎﺻﻞ ﻓﺮﻣﺎﺋﻴﺪ. ﻛﺘﺎب ﻫﺎ ﺑﺎ ﺗﺨﻔﻴﻒ 15 ﺗﺎ 35 % ﺑﺪو ن ﭽﻫﻴ ﮕﻮﻧﻪ ﻣﺤﺪودﻳﺖ ﺧﺮﻳﺪ ﻋﺮﺿﻪ ﻣﻴﺸﻮد . در ﺻﻮرﺗﻲ ﻛﻪ اﻣﻜﺎن ﺣﻀﻮر ﻣﺴﺘﻘﻴﻢ ﺗﻮﺳﻂ ﻣﺘﻘﺎ ﺿﻴﺎن ﻣﻴﺴﺮ ﻧﺒﺎﺷﺪ ، ﻣﺸﺘﺮﻳﺎن ﻣ ﻲ ﺗﻮاﻧﻨﺪ ﻟﻴﺴﺖ ﻛﺘﺎﺑﻬﺎي ﻣﻮرد ﻧﻴﺎز ﺧﻮد را ﺑﻪ آدرس اﻳﻤﻴﻞ ﻳﺎ ﻓﺎﻛﺲ اﻳﻦ ﺷﺮﻛﺖ ارﺳﺎل ﻛﻨﻨﺪ ﺗﺎ در ﺧﺼﻮص ارﺳﺎل ﻛﺘﺎﺑﻬﺎ اﻗﺪام ﻣﻘﺘﻀﻲ ﺻﻮرت ﮔﻴﺮد . در ﺻﻮرت اﺗﻤﺎم ﻣ ﻮﺟﻮدي ﻛﺘﺐ در ﺧﻮاﺳﺘﻲ ، ﻛﺘﺎب ﻫﺎي ﻣﻮرد ﻧﻴﺎز ﺑﻪ ﺻﻮرت ﺛﺒﺖ ﺳﻔﺎرش ﻗﺎﺑﻞ ﺗﻬﻴﻪ ﻣﻲ ﺑﺎﺷﺪ و داﻧﺶ ارزﻳﻦ ﺟﻬﺎن ﻛﺘﺎﺑﻬﺎي ﺛﺒﺖ ﺳﻔﺎرش ﺷﺪه را ﺣﺪ اﻛﺜﺮ ﺗﺎ ﻣﺪت زﻣﺎن 2 ﻣﺎه ﭘﺲ از اﺗﻤﺎ م ﻧﻤﺎﻳﺸﮕﺎه در اﺧﺘﻴﺎر ﻣﺘﻘﺎﺿﻴﺎن ﻗﺮار ﺧﻮاﻫﺪ داد.ﻫﻤﭽﻨﻴﻦ اﻳﻦ ﺷﺮﻛﺖ اﻣﻜﺎن ﺛﺒﺖ ﺳﻔﺎرش و ﺗﺎ ﻣﻴﻦ ﻛﻠﻴ ﻪ ﻛﺘﺎﺑﻬﺎي ﻣﻮرد ﻧﻴﺎز ﺷﻤﺎ را در ﻃﻮل ﺳﺎل دارد. -

Tuning Into a Radio Station

AM/FM Radio Receiving Function Tuning into a Radio Station Tuning into stations automatically 1. Press Tuner on the main unit several times to select either "AM" or "FM". 2. Press Tuning Mode so that the "AUTO" indicator on the display stays lit. 3. Press Tuning to start automatic tuning. Searching automatically stops when a station is found. When tuned into a radio station, the " TUNED " indicator on the display lights. If FM stereo broadcasting is tuned, the "FM STEREO" indicator lights. No sound is output while the " TUNED " indicator is off. When the signal from an FM radio station is weak: Radio wave may be weak depending on the building structure and environmental conditions. In that case, manually tune into the radio station of your choice by referring to the next section. Tuning into stations manually 1. Press Tuner on the main unit several times to select either "AM" or "FM". 2. Press Tuning Mode so that the "AUTO" indicator on the display goes off. 3. Press Tuning to select the desired radio station. The frequency changes by 1 step each time you press the button. The frequency changes continuously if the button is held down and stops when the button is released. Tune by looking at the display. To return the display to "AUTO": Press Tuning Mode on the main unit again. A station is automatically tuned. Normally "AUTO" should be displayed. Tuning into stations by frequency It allows you to directly enter the frequency of the radio station you want to listen to. 1. Press Tuner on the remote controller several times to select either "AM" or "FM".