View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

View Annual Report

Focused on the future. 2014 Annual Report 1 Report to Shareholders 4 Management’s Discussion and Analysis 57 Management’s Responsibility for Financial Statements and Report on Internal Control over Financial Reporting 59 Independant Auditors’ Reports 63 Consolidated Financial Statements 68 Notes to Consolidated Financial Statements 122 Five Years in Review 123 Shareholders’ Information 124 Corporate Information The Annual General Meeting of Shareholders will be held on January 14, 2015 at 11:00 am (Mountain Time) at the Shaw Barlow Trail Building, 2400 – 32 Avenue NE, Calgary, Alberta. Shaw Communications Inc. 2014 Annual Report At Shaw, every decision we make, and every initiative we launch, is driven by customer choice and the imperative to bring quality, reliability, innovation and value to the customer and viewer experience. Shaw Communications Inc. 2014 Annual Report Revenue* Dividends Figures in billions Figures in millions 5.2 5.1 485 5.0 445 4.7 416 391 372 3.7 10 11 12 13 14 10 11 12 13 14 Operating income before Free cash flow* restructuring costs and Figures in millions amortization* Figures in billions 698 2.3 2.2 2.1 2.1 617 604 1.8 515 482 10 11 12 13 14 10 11 12 13 14 *Financial information for fiscal 2010 is prepared in accordance with previous Canadian generally accepted accounting principles. Shaw Communications Inc. REPORT TO SHAREHOLDERS August 31, 2014 Dear Fellow Shareholders: Our performance in fiscal 2014 reflects our continued focus on the delivery of exceptional experiences and leading technology to our customers and viewers, a disciplined focus on operational efficiencies, and sound capital management creating value for all stakeholders. -

Anti-Raffle Policy Hurts Local Groups by JEFF NAGEL Money Raised Last Year Is Set Aside to Ern Health, Authority

AimingarrOws : ' , i!'!~ LocalMP.sa~)Sa~ece.nt ieport:i The whiSke~JaCl~ archers , :..:...-./.....~.:...):,.....~:....:.......,.~:... ... should bee~nough;;¢o::keep,the fling arrowsattheir3-D Stint-at the Sout h Pole= '.., : -moratorium off bffsh:or:~ oil tournament at !C'opperside : kCOMMUNi~:B/ i, / " ~~ .drilling..&NEWS/~8.-: ~ Stables I\sPoRiI'~:B4! - • . .. • :.:..: '.. :," . : ... .:. i " ."! , . ,. ?.,:. ):.. -: ., • ,. - • ": .: , ., ,,- '. - • . 4 • " . ............. "- O --O i $ !.00. PLUS7 ¢:!GS . ($1A0 plus-8¢GST - i-outside of the.Terrace are 2 T N D R D Anti-raffle policy hurts local groups By JEFF NAGEL Money raised last year is set aside to ern Health, Authority. Because the NHA had been threatened by budget cuts. was effective. .A GOVERNMENT crackdown on who payfor this month's Christmas dinner, but is:a government-linanced health provider. ]'he foundation's latest raflli" applica- -"With our little raffle, if we're lucky, can hold raffles is threatening an inno- 2005 may norbe as jolly, gaming money is off limits, tion has been rcjeqted because it supports we make $3,000 or $4,000," Kerr said/ vative school .band program and annual. The raffle money'also helps Clielits go :/:: Up until.April:of this.year the.govern- education;which the province pays for. "We .were try!rig: to have two p~r year Christmas dinners for•the mentally handi- on day trips throughout•the• region and.haS< ment agent'.:s Office here had •authOrity tO .!:Gaming funds, ~including..licensed :) ~ One in thefal/and one-in the spring- to capped.. ' . ".. : .-:-. i. i""i . : ••paidfora variety•of clUbhouse:amenitieS .approve-raffieapplicati0ns • themselves,: .gaming moneys, ~:an .t be u'sed::foritrans- ' misethemajority.of thembrleyJ' ~. -

22-A 2012 Social Baseline Report

APPENDIX 22-A 2012 SOCIAL BASELINE REPORT TM Seabridge Gold Inc. KSM PROJECT 2012 Social Baseline Report Rescan™ Environmental Services Ltd. Rescan Building, Sixth Floor - 1111 West Hastings Street Vancouver, BC Canada V6E 2J3 January 2013 Tel: (604) 689-9460 Fax: (604) 687-4277 Executive Summary Seabridge Gold Inc. is proposing to develop the KSM Project (the Project), a gold, copper, silver, and molybdenum mine located in northwestern British Columbia. The proposed Project is approximately 950 km northwest of Vancouver and 65 km northwest of Stewart, within 30 km of the British Columbia–Alaska border (Figure 1.2-1). The estimated initial capital cost of the Project is US$5.3 billion. The Project is split between two geographical areas: the Mine Site and Processing and Tailing Management Area (PTMA), connected by twin 23-km tunnels (Mitchell-Treaty Twinned Tunnels; Figure 1.2-2). The Mine Site will be located south of the closed Eskay Creek Mine, within the Mitchell Creek, McTagg Creek, and Sulphurets Creek valleys. Sulphurets Creek is a main tributary of the Unuk River, which flows to the Pacific Ocean. The PTMA will be located in the upper tributaries of Teigen and Treaty creeks. Both creeks are tributaries of the Bell-Irving River, which flows into the Nass River and Pacific Ocean. The PTMA is located about 19 km southwest of Bell II on Highway 37. This social baseline report presents a comprehensive overview of the past and present social environment and context of the proposed Project, including patterns, trends, and changes over time. It outlines relevant social factors for which data on communities in the Project area are available, such as society and governance; population and demographics; education, skills and training (level of achievement, elementary, secondary, post-secondary, and adult education); health and social services (facilities, services, trends, and issues); recreation; protection services (crime index, police, fire, and ambulance); and infrastructure (utilities, communications, transportation, and housing). -

Tuning Into a Radio Station

AM/FM Radio Receiving Function Tuning into a Radio Station Tuning into stations automatically 1. Press Tuner on the main unit several times to select either "AM" or "FM". 2. Press Tuning Mode so that the "AUTO" indicator on the display stays lit. 3. Press Tuning to start automatic tuning. Searching automatically stops when a station is found. When tuned into a radio station, the " TUNED " indicator on the display lights. If FM stereo broadcasting is tuned, the "FM STEREO" indicator lights. No sound is output while the " TUNED " indicator is off. When the signal from an FM radio station is weak: Radio wave may be weak depending on the building structure and environmental conditions. In that case, manually tune into the radio station of your choice by referring to the next section. Tuning into stations manually 1. Press Tuner on the main unit several times to select either "AM" or "FM". 2. Press Tuning Mode so that the "AUTO" indicator on the display goes off. 3. Press Tuning to select the desired radio station. The frequency changes by 1 step each time you press the button. The frequency changes continuously if the button is held down and stops when the button is released. Tune by looking at the display. To return the display to "AUTO": Press Tuning Mode on the main unit again. A station is automatically tuned. Normally "AUTO" should be displayed. Tuning into stations by frequency It allows you to directly enter the frequency of the radio station you want to listen to. 1. Press Tuner on the remote controller several times to select either "AM" or "FM". -

Of Analogue: Access to Cbc/Radio-Canada Television Programming in an Era of Digital Delivery

THE END(S) OF ANALOGUE: ACCESS TO CBC/RADIO-CANADA TELEVISION PROGRAMMING IN AN ERA OF DIGITAL DELIVERY by Steven James May Master of Arts, Ryerson University, Toronto, Ontario, Canada, 2008 Bachelor of Applied Arts (Honours), Ryerson University, Toronto, Ontario, Canada, 1999 Bachelor of Administrative Studies (Honours), Trent University, Peterborough, Ontario, Canada, 1997 A dissertation presented to Ryerson University and York University in partial fulfillment of the requirements for the degree of Doctor of Philosophy in the Program of Communication and Culture Toronto, Ontario, Canada, 2017 © Steven James May, 2017 AUTHOR'S DECLARATION FOR ELECTRONIC SUBMISSION OF A DISSERTATION I hereby declare that I am the sole author of this dissertation. This is a true copy of the dissertation, including any required final revisions, as accepted by my examiners. I authorize Ryerson University to lend this dissertation to other institutions or individuals for the purpose of scholarly research. I further authorize Ryerson University to reproduce this dissertation by photocopying or by other means, in total or in part, at the request of other institutions or individuals for the purpose of scholarly research. I understand that my dissertation may be made electronically available to the public. ii ABSTRACT The End(s) of Analogue: Access to CBC/Radio-Canada Television Programming in an Era of Digital Delivery Steven James May Doctor of Philosophy in the Program of Communication and Culture Ryerson University and York University, 2017 This dissertation -

Unions to Log Export

Unequal access Personal teleporter Uphill thrill The city says no to a wheelchair A local lad knows what we'll be World class snowmobilers ramp up at the Terrace .wearing on our wrists in the year converge in Terrace to take on the arena\NEWS A13 2050\COMMUNITY B4 mighty A.O.T.\SPORTS B4 VOL. 13 NO. 50 iniO "O WEDNESDAY O Ire March 21, 2001 t.O 03 ,;70 $1.00 PLUS7¢ GST p,. ($1.10 plus S¢ GST outside of the Terracearea) TANDARD II "Terreace hs ool "Fore=$try Cctp,tct['" Natural gas bills Unions to too high Poor. estimates block raw. inflate PNG bills By JEFF NAGEL PACIFIC NORTHERN log export: Gas has been told to look into reports that faulty gas By JEFF NAGEL consumption estimates THE IWA is refusing to sign a deal that would allow have caused some natural Skeena Cellulose to export raw logs and possibly re- gas customers to pay too duce the duration of logging and sawmill shutdowns much money. this year. Gas utilities routinely The union, which represents workers now laid off at make physical meter read- Skeena Cellulose's Terrace sawmill, views raw log ex- ings every two months but ports as effectively exporting B.C. sawmill jobs, said simply estimate the IWA Canada local 2171 president Darrell Wong. months in between based "We are not prepared to sit down and negotiate a raw on each customer's histor- log export agreement," Wong said from the Vancouver ic consumption. Island head office of Local 2171. But problems with the He said the five-year estimating system being economic plan being pre- used by several utilities at pared for SCI by provin- [] City council backs a time when natural gas cial Job Protection Corn- log exports for Inter- rates were rising quickly missioner Eric van Seer- for, Page A13 may have resulted in over- EUROPEAN cheeses are scarce after an import ban was slapped on anything that may spread foot-and- en gives no guarantees billing, B.C. -

Federal Register/Vol. 64, No. 18/Thursday, January 28, 1999

Federal Register / Vol. 64, No. 18 / Thursday, January 28, 1999 / Notices 4469 the amount of $7.00 payable to the Cheswick, PA; Tut Systems, Pleasant COLUMBIA have been added as parties Consent Decree Library. Hill, CA; Transwitch, Shelton, CT; and to this venture. Joel Gross, VTT Electronics, Oulu, FINLAND have No other changes have been made in Chief, Environmental Enforcement Section, been added as parties to this venture. either the membership or planned Environment and Natural Resources Division. SMC, Irvine, CA has changed its name activity of the group research project. [FR Doc. 99±2033 Filed 1±27±99; 8:45 am] to Escalate Networks, Irvine, CA. Membership in this group research BILLING CODE 4410±15±M SouthWestern Bell, Austin, TX has project remains open, and Cable changed its name to SBC Technology Television Laboratories, Inc. Resources, Austin, TX. Ericsson Austria (``CableLabs'') intends to file additional DEPARTMENT OF JUSTICE AG, Vienna, AUSTRIA has changed its written notification disclosing all name to LM Ericsson, Vienna, changes in membership. Antitrust Division AUSTRIA. On August 8, 1988, Cable Television Amati, San Jose, CA has merged with Laboratories, Inc. (``CableLabs'') filed its Notice Pursuant to the National Texas Instruments, Dallas, TX. original notification pursuant to section Cooperative Research and Production Also, Sourcecom, Santa Clarita, CA; 6(a) of the Act. The Department of Act of 1993ÐThe Asymmetrical Digital Justice published a notice in the Federal Subscriber Line Forum and Interphase, Dallas, TX have been dropped as parties to this venture. Register pursuant to section 6(b) of the Act on September 7, 1988 (53 FR Notice is hereby given that, on March No other changes have been made in 34593). -

Shaw Communications Inc. Annual Report 2004

SHAW COMMUNICATIONS INC. ANNUAL REPORT 2004 Shaw Communications Inc. ANNUAL REPORT August 31, 2004 SHAW COMMUNICATIONS INC. ANNUAL REPORT CONTENTS Page Report to Shareholders 1 Management’s Discussion and Analysis 3 Management’s Responsibility for Financial Reporting 45 Auditors’ Report 46 Consolidated Financial Statements 47 Notes to the Consolidated Financial Statements 50 Five Years in Review 96 Shareholders’ Information 97 Corporate Information 98 The Annual General Meeting of Shareholders will be held on January 13, 2005 at 11:00am at The Fairmont Hotel Macdonald, 10065 – 100 Street, Edmonton, Alberta T5J 0N6. Shaw Communications Inc. REPORT TO SHAREHOLDERS August 31, 2004 Dear Fellow Shareholders: Fiscal 2004 was marked by a number of significant achievements. In addition to almost tripling free cash flow1, we continued to grow our cable subscriber base, and we reached one million Internet customers in June. Our satellite division significantly improved its operating income before amortization and became free cash flow positive for the first time. Our financial position has improved as a result of this strong performance, enabling us to reduce debt by $210.6 million and increase the quarterly dividend on the Class B Non-Voting Shares to $0.07 per share effective September 30, 2004. While reducing overall levels of capital expenditures, we started a number of capital projects to prepare for new services such as Digital Phone, which is scheduled for launch in calendar 2005. The foundation of our success this year resulted from the continuation of a number of strategies: leveraging our network infrastructure to offer customers a wider variety of products and services; delivering quality customer service to increase penetration; implementing price/packaging structures that provide value to both Shaw and the customer; and, generating operating efficiencies to keep our competitive edge. -

Broadcasting Public Notice CRTC 2004-50

Broadcasting Public Notice CRTC 2004-50 Ottawa, 15 July 2004 Requests to add non-Canadian third-language services to the lists of eligible satellite services for distribution on a digital basis In this public notice, the Commission approves the addition of eight non-Canadian third- language services, consisting of five mainly Spanish-language services, one German- language service, one Romanian-language service, and one Arabic-language service, to its lists of eligible satellite services for distribution on a digital basis (the digital lists). The Commission also denies requests to add six other non-Canadian, third-language services. The Commission further addresses the addition of non-Canadian third-language services to the digital lists in three other public notices issued today. In Requests to add Al Jazeera to the lists of eligible satellite services for distribution on a digital basis, Broadcasting Public Notice CRTC 2004-51, 15 July 2004 (Public Notice 2004-51), the Commission approves the addition of the Arabic-language service Al Jazeera to the digital lists, subject to conditions set out in that public notice. In Revised lists of eligible satellite services, Broadcasting Public Notice CRTC 2004-52, 15 July 2004, the Commission sets out revised lists of satellite services reflecting the determinations in this public notice and in Public Notice 2004-51. These lists replace those contained in Revised lists of eligible satellite services, Broadcasting Public Notice CRTC 2003-43, 5 August 2003, and reflect the addition of nine non-Canadian third- language services to the lists of Part 2 and Part 3 eligible satellite services for digital distribution and to Section C of the list of DTH eligible satellite services. -

Investor Presentation

INVESTOR PRESENTATION June 2020 WESTERN OVERVIEW PURPOSE To create long-term wealth for shareholders by building and maintaining a diversified portfolio of strong, stable and profitable Western-based companies and helping them grow. STRATEGY Acquire significant ownership positions in successful companies by: 1. Offering “Continuity Capital” 2. Provide oversight using “Pattison Principles” and “Rockefeller Habits” 3. Maximize return to shareholders through “Western Sensibility” FOUNDING GOALS $100 million in enterprise value investments by 2021 (on track) 3 industry sectors by 2019 (achieved) 2 WESTERN EPS Below summarizes the contribution by quarter for Western — 2019 Price to Earnings ratio of ~7x based on $0.041 2019 EPS and a current share price of $0.30 2019 Earnings per Share1 Book Value Per Share1 EPS Impairment loss resulting from COVID-19 0.6000 0.040 0.020 0.5000 0.000 0.4000 (0.020) 0.3000 (0.040) (0.060) 0.2000 (0.080) 0.1000 (0.100) (0.120) - 2018Q1 2018Q2 2018Q3 2018Q4 2019Q1 2019Q2 2019Q3 2018Q1 2018Q2 2018Q3 2018Q4 2019Q1 2019Q2 2019Q3 2019Q4 2020Q1 2019Q4 2020Q1 1 Basic and diluted common shares 3 SUMMARY OF WIC ACQUISITIONS Summary of WIC Acquisitions Purchase WIC WIC Debt at Debt at Current Price Ownership Equity1 Closing2 Dec 31, 2018 Status ($mm) (%) ($mm) ($mm) ($mm) Closed (Dec 16, $16.4 50.1% $4.01 $8.8 $6.3 2016) Closed (Sept 1, $5.0 30% $5.0 $12.1 $11.2 2017) Closed (Jan 1, $9.5 75% $3.45 $5.1 $4.6 2018) Closed (Mar 1, $24.1 50.4% $3.25 $15.7 $15.0 2018) Closed (May 6, $3.4 50% $2.00 -- -- 2019) 1. -

2017 Annual Information Form Shaw Communications Inc

November 28, 2017 TABLE OF CONTENTS CORPORATE STRUCTURE 1 DESCRIPTION OF THE BUSINESS 2 CAPITAL STRUCTURE, DIVIDENDS AND RELATED MATTERS 6 1. Description of Capital Structure 6 2. Dividends 12 3. Ratings 13 4. Market for Securities 14 DIRECTORS AND OFFICERS 15 1. Directors 15 2. Board Committee Members 16 3. Executive Officers 16 4. Shareholdings of Directors and Executive Officers 17 5. Conflicts of Interest 17 6. Cease Trade Orders, Bankruptcies, Penalties or Sanctions 17 AUDIT COMMITTEE 18 1. Audit Committee Charter 18 2. Audit Committee Composition, Education and Experience 18 3. Audit Fees 19 LEGAL PROCEEDINGS AND REGULATORY ACTIONS 19 INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS 20 REGISTRAR AND TRANSFER AGENT 20 INTERESTS OF EXPERTS 20 ADDITIONAL INFORMATION 20 CAUTION CONCERNING FORWARD LOOKING STATEMENTS 20 MATERIAL CONTRACTS 22 SCHEDULE A – AUDIT COMMITTEE CHARTER A-1 CORPORATE STRUCTURE Shaw Communications Inc. (“Shaw” or the “Company”) is an enhanced connectivity provider. Our Consumer division provides customers with broadband Internet, Shaw Go WiFi, video, and digital phone. Our Wireless division provides wireless voice and data services through an expanding and improving mobile wireless network infrastructure. The Business Network Services division provides business customers with Internet, data, WiFi, telephony, and video. The Company was incorporated under the laws of the Province of Alberta on December 9, 1966 under the name Capital Cable Television Co. Ltd. and was subsequently continued under the Business Corporations Act (Alberta) on March 1, 1984 under the name Shaw Cablesystems Ltd. Its name was changed to Shaw Communications Inc. on May 12, 1993. Shaw was reorganized pursuant to a plan of arrangement under the Business Corporations Act (Alberta) effective September 1, 1999, and amended its articles on January 28, 2004 to limit the number of Class A Voting Participating Shares that may be issued and on May 26, 2011 to create the Series A Shares and Series B Shares (each as hereinafter defined). -

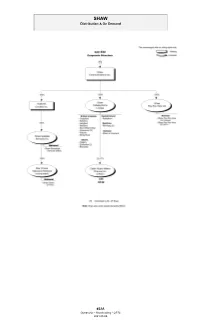

Ownership Charts Reflect the Transactions Approved by the Commission and Are Based on Information Supplied by Licensees

SHAW Distribution & On Demand #32A Ownership – Broadcasting - CRTC 2021-05-05 UPDATE CRTC 2017-47 – revoked the licence issued to Shaw Cablesystems Limited for CJBN-TV Kenora. Update – 2018-03-20 – of Shaw Satellite Services Inc.’s shareholding as per information supplied in the 2018 Broadcasting Ownership Information Annual Filing. CRTC 2018-390 – revoked the licence issued to Shaw Cablesystems Limited for the terrestrial broadcasting distribution undertaking serving Lethbridge. It meets the exemption criteria. CRTC 2019-331 – revoked the licence issued to Shaw Cablesystems Limited for the the terrestrial broadcasting distribution undertaking serving Duncan. It meets the exemption criteria. Update – 2019-10-10 – on 1 September 2019, Shaw Cablesystems Limited, Shaw Cablesystems (VCI) Limited, Shaw Real Estate Ltd. and eight other entities amalgamated to continue as Shaw Cablesystems Limited. CRTC 2020-12 – revoked the licence issued to Shaw Cablesystems Limited for the the terrestrial broadcasting distribution undertaking serving Thunder Bay. It meets the exemption criteria. CRTC 2020-13 – revoked the licence issued to Shaw Cablesystems Limited for the the terrestrial broadcasting distribution undertaking serving Fort McMurray. It meets the exemption criteria. Update – 2020-07-03 – minor change. CRTC 2021-160 – revoked the licence issued to Shaw Cablesystems Limited for terrestrial broadcasting distribution undertaking serving Sault Ste. Marie. SEE ALSO SHAW – 32 CORUS – 32B, 32C, 32D, 32H and 32I NOTICE The CRTC ownership charts reflect the transactions approved by the Commission and are based on information supplied by licensees. The CRTC does not assume any responsibility for discrepancies between its charts and data from outside sources or for errors or omissions which they may contain.