Department of the Auditor General of Pakistan

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

BANNU EDUCATION FACILITIES - KPK Lebgend College

70°30'0"E 70°40'0"E 70°50'0"E BANNU EDUCATION FACILITIES - KPK LeBgend College ! !> !> !> Town Ship, Bannu !> High School !>!> !>!> !> UNIVERSITY OF !> !B SCIENCE AND !> !> FR BANNU !>!>!> !> TECHNOLOGY, BANNU !> Higher Secondary !>!>!> !> !> !> !> !!> N. WAZIRASTAN !>!> !> ! !>!> !> KGN G G P S K O T K A U M A R !>!> !>!> !> ! B ! R !> ! !> d Masjid School S H A H (C H A S H M I) !>!> !>!> !> !> !> !> !> at Rd BB DISTRICT oTh !> Nizam KARAK K JAIL !> !> !>!> !> U !> !> Middle School !> !> !> !> T !> Baza!>r!> !> !> A ! ! Boza N !> !> D !> !>!> A Sa A Khel !> d !> !> G !> !>!>!> !> Model Primary School !> !> R G G P S K O TK A G U L !> !> r L !>!> !> aw !> A !> !> a !> A !> !> !> !>!> B !> R A U F K H A N P IR B A n !> !> GPS Z!>INDI K H E L D O M E L Sheri !> !> Primary School GGPS L !> !> GG!>PS R A KILLA !> !!> d SITTI !> !> G !> GPS LANDI L!>AN!DI !> Kula KILLA N !> !!> GMS DABAK KILLA KILLA !> !> !> !> A !>!> !>!!>!> ! GGPS ABADI GGPS ARAL GMPS !> !> !> !> T Technical Institute T SYED KHEL K GGPS WANDA HATI KHEL ! !!> !>!> GUL AHMED ! GPS ZARI !> SYED!> REHMAN U !>!> !> !> !>!> !> !> R GHAFAR !> !> !> !>!> ! !> !B !> !> R KAS KALA!> d GUL FAQEER GPS SHER !> KHUJARI !> !> !> !> R A !> !> !>!>!> !> GPS B GPS KURRM !> I !> !> !> !> R !> !> !> !> !> !> !> A !> !> !> V M !> !> !> !> al ALI BEZEN!B !> !!> !> University R E !> !> !> !> !> h !> JAM!>EER BIZEN KHEL U GARHI !> R GPS SOH!>BAT !> !> !>!>!> A M!> !>!> !> !>!>!>T !> !> !> !> KHEL !> H N !> !> !>a !> !> !>!> - !> !>!>!> !> !> S L !> m KHAN S!>U!>R!>ANI u !>!> !>!> !> !!> !> !> -

Bannu DRC Rapid Needs Assessment II November 2014

Rapid Needs Assessment II Summary of Findings - November 2014 Displaced Populations of North Waziristan Agency in District Bannu Union Councils: Koti Sadat, Fatma Khel, Bazar Ahmad Khan, Ghoriwala, Amandi, Kausar Fateh Khel, Bharat, Nar Jaffer & Khaujari Monitoring & Evaluation Unit, Danish Refugee Council, Pakistan 0 | 14 For further details please contact: [email protected] ; [email protected] DRC| DANISH REFUGEE COUNCIL Acronyms CoRe Community Restoration cluster DRC Danish Refugee Council FATA Federally Administered Tribal Areas FDMA FATA Disaster Management Authority GoP Government of Pakistan IVAP IDP Vulnerability Assessment & Profiling KII Key Informant Interviews KP Khyber Pakhtunkhwa MIRA Multi-sector Initial Rapid Assessment NADRA National Database & Registration Authority NWA North Waziristan Agency PDMA Provincial Disaster Management Authority PKR Pakistan Rupee RRS Return and Rehabilitation Strategy TDPs Temporarily Dislocated Persons UC Union Council UNHCR United Nations High Commissioner for Refugees UNICEF United Nations International Children's Emergency Fund UNOCHA United Nations Office for the Coordination of Humanitarian Affairs Monitoring & Evaluation Unit, Danish Refugee Council, Pakistan 1|14 For further details please contact: [email protected] ; [email protected] DRC| DANISH REFUGEE COUNCIL Introduction The present report provides a snapshot of some of the most pressing needs as of the 24th of November 2014 among the Temporarily Dislocated Persons1 (TDPs) from North Waziristan Agency (NWA) in nine union councils (UCs) of District Bannu: Koti Sadat, Fatma Khel, Bazar Ahmad Khan, Ghoriwala, Amandi, Kausar Fateh Khel, Bharat, Nar Jaffar & Khaujari. This report is based on the second2 Bannu rapid needs assessment conducted by Danish Refugee Council (DRC) in late November 2014, which focused specifically on needs within winterization, shelter and livelihoods – both in place of displacement and origin. -

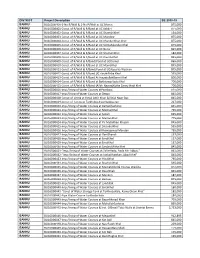

BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000

DISTRICT Project Description BE 2018-19 Final Budget Releases Expenditure BANNU BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000 875,000 875,000 875,000 BANNU BU16D00401-Const. of R/Wall & P/Band at UC Kakki-I 875,000 875,000 875,000 875,000 BANNU BU16D00402-Const. of R/Wall & P/Band at UC ShamshiKhel 134,000 134,000 134,000 134,000 BANNU BU16D00403-Const. of R/Wall & P/Band at UC Mandew 875,000 875,000 875,000 875,000 BANNU BU16D00404-Const. of R/Wall & P/Band at UC KhanderKhan khel 875,000 875,000 875,000 875,000 BANNU BU16D00405-Const. of R/Wall & P/Band at UC SlemaSikander Khel 875,000 875,000 875,000 875,000 BANNU BU16D00406-Const. of R/Wall & P/Band at UC Nurar 825,000 825,000 825,000 825,000 BANNU BU16D00407-Const. of R/Wall & P/Band at UC ShamshiKhel 184,000 184,000 184,000 184,000 BANNU BU16D00408-Const. of R/Wall & P/Band at UC JhanduKhel 825,000 825,000 825,000 825,000 BANNU BU16D00409-Const. of R/Wall & P/Band/Pond at UCDomel 865,000 865,000 865,000 865,000 BANNU BU16D00410-Const. of R/Wall & P/Band at UC MamaKhel 875,000 875,000 875,000 875,000 BANNU BU16D00411-Const. of R/Wall & P/Band/Pond at UCAsperka Waziran 875,000 875,000 875,000 875,000 BANNU BU16D00412-Const. of R/Wall & P/Band UC ZerakiPirba Khel 595,000 595,000 595,000 595,000 BANNU BU16D00413-Const. -

Census of Pakistan 1951 Village List

< .. Census 51 -No. :lo -i~ (I ) • I \. .' '~ ,; ·I .. - ' , . CEf\JSUS OF PAl<ISTAN, 1951 I )llkLAGE LIST . .. ~ I . l N.-W.F .P.- Banitu Distdcl -, OFFICE OF THE PROVINCIAL SUPERINTENDENT OF CENSUS, ~. 4 NORTH-WEST FRONTIER PnOVINCE, ~ .~ • PESHAWAR. ' .'. : , . ... ! March 1952 Price :'' l/-f- PR1NTED DY THE MANAGE R, GoVERNME I'}~' OF PAKISTAi... Pm;ss, K ARACHI PUBLISH ED DY 'l'HE MANAGER OF PUBLICA'l'JONS, KflRACH1: 1953 ' . -· ;'.~ , - b -· •S... ~ -· ~- .1 - -A~ --- L ·, . .· \ I .~~. ~. --~.~...._~~................... .._., .A£iliirJl1•£ NCE s I c:::::::; DIHR.IC T H'fr . T£14SIL uy 1111oiA wlio . lf!,OVINGf. OA STA Tl -·-"l't.... 011riu'r ----. I• .' ~£J.ISIL ....... ~ . lfAILWAY$ '~ . ~OAD.J R(VEA~ ~ .. ·~ . , lia!'1q ,f~: ict P. 1" ~ ;· Pa)·~fand " . lieJaiveM epe~ \~~i~I BN umd:r·~' l:i:<l tMl"fr,ie~ . out in tli~Fii:st.~~~·1)8 or,~akist~n· duritig . l es the p@p~l:at1on .,0f th~ s~a ~ep areas and thus ~reserves rnformwfion which would . iu ~he sfa:tisi~~al tota:ls of_the ~e ~ ~s Report.. I~ is ·hQped that the preparatien of.- this a has~s :f011 h,e cozyt1mied collection i!>f Village· Siatisp.cs. · . • . • • ·1 ·1·1> • . 'I . --!. .. ~ • • . ~ . ~ !iii ViiU1agq lisHsrin ·three parts ; first, the s~Friary Table of the District showing the p0pulation and ber,ot:houses, 'in tli.ousand.s, and the area in~·- miles; second, the list of Villages in al~habetical oi;der ·µ e~cll R'.e:ve~U!.\~~Fde sh,0win~ revenue nu b~r~, population, number of houses and 10cal de~ails; , a·Tha~p>'hao~u1eall mclex of tiht;i villages.of each e s11. -

1 Annexure - D Names of Village / Neighbourhood Councils Alongwith Seats Detail of Khyber Pakhtunkhwa

1 Annexure - D Names of Village / Neighbourhood Councils alongwith seats detail of Khyber Pakhtunkhwa No. of General Seats in No. of Seats in VC/NC (Categories) Names of S. Names of Tehsil Councils No falling in each Neighbourhood Village N/Hood Total Col Peasants/Work S. No. Village Councils (VC) S. No. Women Youth Minority . district Council Councils (NC) Councils Councils 7+8 ers 1 2 3 4 5 6 7 8 9 10 11 12 13 Abbottabad District Council 1 1 Dalola-I 1 Malik Pura Urban-I 7 7 14 4 2 2 2 2 Dalola-II 2 Malik Pura Urban-II 7 7 14 4 2 2 2 3 Dabban-I 3 Malik Pura Urban-III 5 8 13 4 2 2 2 4 Dabban-II 4 Central Urban-I 7 7 14 4 2 2 2 5 Boi-I 5 Central Urban-II 7 7 14 4 2 2 2 6 Boi-II 6 Central Urban-III 7 7 14 4 2 2 2 7 Sambli Dheri 7 Khola Kehal 7 7 14 4 2 2 2 8 Bandi Pahar 8 Upper Kehal 5 7 12 4 2 2 2 9 Upper Kukmang 9 Kehal 5 8 13 4 2 2 2 10 Central Kukmang 10 Nawa Sher Urban 5 10 15 4 2 2 2 11 Kukmang 11 Nawansher Dhodial 6 10 16 4 2 2 2 12 Pattan Khurd 5 5 2 1 1 1 13 Nambal-I 5 5 2 1 1 1 14 Nambal-II 6 6 2 1 1 1 Abbottabad 15 Majuhan-I 7 7 2 1 1 1 16 Majuhan-II 6 6 2 1 1 1 17 Pattan Kalan-I 5 5 2 1 1 1 18 Pattan Kalan-II 6 6 2 1 1 1 19 Pattan Kalan-III 6 6 2 1 1 1 20 Sialkot 6 6 2 1 1 1 21 Bandi Chamiali 6 6 2 1 1 1 22 Bakot-I 7 7 2 1 1 1 23 Bakot-II 6 6 2 1 1 1 24 Bakot-III 6 6 2 1 1 1 25 Moolia-I 6 6 2 1 1 1 26 Moolia-II 6 6 2 1 1 1 1 Abbottabad No. -

Rapid Needs Assessment

Rapid Needs Assessment Summary of Findings September 2014 Displaced populations of North Waziristan Agency in District Bannu (Six Union Councils - Amandi, Bazar Ahmad Khan, Fatma khel, Ghoriwala, Kausar Fateh Khel, and Koti Sadat) September 2014 Displaced populations of North Waziristan Agency in District Bannu (Six Union Councils - Amandi, Bazar Ahmad Khan, Fatma khel, Ghoriwala, Kausar Fateh Khel, and Koti Sadat) September, 2014 Railway Road 10-CII, University Town, Peshawar Tel: 92 (0) 91 570 1896, [email protected] N e e d s A s s e s s m e n t R e p o r t , Displaced Populations of North Waziristan Agency (September, 2014) Introduction This report provides a snapshot of the current situation (as of 9th of September 2014) of displaced persons from North Waziristan Agency (NWA) in six Union Councils (UCs) in District Bannu (Fatmakhel, Ghoriwala, Amandi, Kausar Fateh Khel Bazar Ahmad Khan and Koti Sadat), primarily within WASH, but also with findings relating to Shelter and NFIs. The rapid assessment is primarily intended to inform the planning of DRC’s emergency response and should be seen as such. Since there is a relative dearth of information to inform the response in Bannu we however choose to make our data freely available so that if necessary they can be used for triangulation purposes by other humanitarian actors in Bannu. Primary data was obtained by DRC assessment teams who interviewed TDPs1 and host community members. Reliable secondary sources such as FATA Disaster Management Authority (FDMA), Provincial Disaster Management Authority (PDMA), Khyber Pakhtunkhwa, United Nations Office for the Coordination of Humanitarian Affairs (UNOCHA), provided additional data to this report. -

BANNU DISTRICT REFERENCE MAP - KPK Legend GGPS KOTKA UMAR SHAH(CHASHMI) 9 Bank !> N

70°30'0"E 70°40'0"E 70°50'0"E BANNU DISTRICT REFERENCE MAP - KPK Legend GGPS KOTKA UMAR SHAH(CHASHMI) 9 Bank !> N. WAZIRASTAN FR BANNU !® Courier Service U T l³ A Fuel Station N D GPS KOTKA GUL A !> G A !> RAUF KHAN PIRBA G G!>PS ZINDI G R L !> KHEL DOMEL Health Facility A A !> KILLA !> GGPS KARAK GGPS B !> L !> GPS LANDI LANDI SITTI A CIVIL DISP. !> G !> GMPS SYED KILLA KILLA ö !> GMS DABAK Masjid GGPS ARAL !>!> KILLA N DABAK GPS KURRM GGPS WANDA SYED KHEL REHMAN U ! A !> SYED KHEL HATI KHEL l³ !> H GARHI !>!> !> !> KHUJA!>!>RI !> T !>!> !> GHAFAR GPS SHER G!>!> !> S !> !> !> B GPS!> SOHBAT !> !>!> !> !> A a !> !> !> !> !> GPS A !> !> !> !> !> !> !> GPS JAMEER A!>LI BEZEN !> K Police Station R GPS AJMAL KHAN !> !> !> !> !> !> RHC c !> KHAN SURANI !>!> !> !> !>!>!>!> A !>!> !>G!>!>!> !> !> ZARI GUL BIZEN KHEL !> !> N !> !> !>!> !> GP!>S K!>!>ACHKOT !>!> !>!>!> G KHEL !> ca!>DOMEL L BARLASHTI !> G !>!>!> !>!> !>!> !> !!> !> !> A !> !> !> !> !>!> !> !> !>!> FAQEER ! !> !> G!> SPINA TANGI BHU MUSA K !> ASAD !> !> !>!> a ö !> !> !> E DAUD SHAH !> !> !>!> !>!> !> !>!> !> !>!> !>cG! !> l³ S tolk ! GPS AMANDI !> G!>PS ö GPS KO!>T!KA !> pina Tangi Pa !>hel Rd !>!>G PATOLKHEL BHU HOSPITAL !> !> !> !>G !> a ! ö G D KHEL !® Post office !>!>!> !> !>!> !> KHA!>N !> !!> BHU NIZAM !> c ö !> !> !> !>!>!> !>!> !>!> !> !> !> !> KohGat Rd SHARABAT o !> !> !> SHAH PARIZ KHONI !> ö m GGPS!> !>SPIN !> !> !> !> !> !> !> !> !> !> ö WALAGAI !> BH!>U !> !> BAZAR a Rd G !>JEHAN KHEL !> !> a DISTT JAIL KHAN DOMEL il !> TANGI NO.2 GPS MUSA KHEL VOLIGAIG!> ink BHU -

At Least 2Nd Division Bachlor Degree District: Mardan (Posts-1) Scoring Key: 1St Div: 2Nd Div: 3Rd Div: Age 25-30 Years 1

At least 2nd Division Bachlor Degree District: Mardan (Posts-1) Scoring Key: 1st Div: 2nd Div: 3rd Div: Age 25-30 Years 1. (a) Basic qualification Marks S.S.C 20 15 12 Date of Advertisement:- 22-08-2020 2. Higher Qualification Marks (One Step above-7 Marks, Two Stage Above-10 Marks) F.A/FSc 20 15 12 Junior Clerk (BPS-11) 3. Experience Certificate BA/BSc 20 15 12 4. Interviews Marks Total;- 60 45 36 5. Professional Training Marks Total;- LIST OF CANDIDATES FOR APPOINTMENT TO THE POST OF JUNIOR CLERK B-11 BASIC QUALIFICATION Higher Qual: SSC FA/FSC BA/BSC S. # on Name/Father's Name and address Total S. # Appli: Domicile Remarks Malrks= 7 Malrks= Total Marks Total Date of Birth of Date Qualification Marks Marks Marks Division Division Division Marks of Experience of Marks Professional/Training Professional/Training One Stage AboveStage 7 One Two Stage AboveStage Two 10 Interview Marks 8 Marks 8 Marks Interview Year of Experience of Year 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 1 1 Mr. Muhammad Usman S/O Hussain Ahmad, Dalazak Road, House No. L-6, Street No. 3, Mohallah Corporation colony No. 2, Peshawar. 11/2/1992 MSc (Hons) + DIT Charsadda 1st 20 1st 20 1st 20 10 70 70 2 2 Mr. Muhammad Adnan Khalid S/O Khalid Pervez, Street No.1-B, Maki Road Gulbahar, No. 4, Flat No. 21 Peshawar. 28-9-1992 M.Phil + DIT Peshawar 1st 20 1st 20 1st 20 10 70 70 3 3 Mr. -

(MALE) BANNU STATEMENT SHOWING the SCHOOL WISE DETAIL of FOLLOWING VACANT POSTS AS STOOD on 2020 ( Revised List of Vacant Post On.2020) PST B-12 S.No

OFFICE OF THE DISTRICT EDUCATION OFFICER (MALE) BANNU STATEMENT SHOWING THE SCHOOL WISE DETAIL OF FOLLOWING VACANT POSTS AS STOOD ON 2020 ( Revised list of Vacant Post on.2020) PST B-12 S.No. EMIS Union Council/Ward Total Name of School M 1 37289 GPS Paila Balqiz Nurar-I 1 1 2 11728 GPS Wali Zaman Nurar Nurar-I 1 1 3 11312 GPS Amandi Sheikh Amir Bannu Amandi 1 1 4 28023 GPS Amandi Ayub Bannu Amandi 1 1 5 11314 GPS Amandi Umer Khan (Shahzad) Amandi 1 1 6 38235 GPS Nusrat Shal Daud Shah Bannu Amandi 1 1 7 11719 GPS Taza Khan Chasua Bannu Aral-I 2 2 8 11456 GPS Mir Alam Cha:Bannu Aral-I 2 2 9 11755 GPS Umer Gul Waligai Bannu Aral-I 1 1 10 11664 GPS Gul Rauf Bannu Aral-I 1 1 11 11457 GPS Sher Azam Chashmai Bannu Aral-I 1 1 12 11449 GPS Kabir Kharghai Bannu Aral-I 1 1 13 11371 GPS Domel Khas Bannu Aral-II 2 2 14 11319 GPS Aqleem Khan Bannu Aral-II 2 2 15 37771 GPS Spina Tangi Patol Khel Bannu Aral-II 1 1 16 40883 GPS Ihsan Ullah Baik Khel Bannu Aral-II 1 1 17 11632 GPS Quli Khel Bannu Aral-II 1 1 18 11745 GPS Zardad Baikkhel Bannu Aral-II 1 1 19 40873 GPS Bokal Khel Bannu Aspirka Wazir 1 1 20 40338 GPS Widan Kala Bannu Aspirka Wazir 1 1 21 40326 GPS Saleem Khan Gadi Top Bannu Aspirka Wazir 1 1 22 39285 GPS Sher Ajam Wazir Bannu Aspirka Wazir 1 1 23 37777 GPS Topan Kala Bannu Aspirka Wazir 1 1 24 37604 GPS Sada Khel Wazir Bannu Aspirka Wazir 1 1 25 11383 GPS Gadi Top Bannu Aspirka Wazir 1 1 26 39817 GPS AMANULLAH BAKA KHEL BAKA KHEL 1 1 27 11443 GPS MUHAMMAD ANWAR NARMI KHEL BAKA KHEL 1 1 28 39820 GPS SHER M. -

*Successful Students Are Advised to Check Their Particulars Mentioned Below I.E

STUDENTS LOAN SCHEME – NAMES OF SUCCESSFUL STUDENTS FOR THE SESSION 2015-2016 ANNOUNCEMENT The State Bank of Pakistan's Apex Committee, a high powered body on Students Loan Scheme (SLS) has approved an amount of Rs.174.923 million (Against 14th Advertisement) of Interest free loan to 1,044 deserving students for their entire period of studies. These students have been pursuing their studies in different technical and professional disciplines leading to Graduation, Masters, M.Phil and Ph.D within Pakistan in public sector universities/colleges during the Session 2015-2016. Important :- Please Note that the current year disbursement has to be made within 45 days from the date of receipt of the Sanction Advice by the eligible student. Thereafter, no disbursement will be allowed without prior clearance of the Students Loan Wing, NBP, Head Office, Karachi. In case the student’s copy is misplaced/undelivered, the Principal/Registrar may provide photocopy of the “Sanction Advice” to the student to facilitate disbursement by the concerned Branch. IMPORTANT INSTRUCTIONS *Successful Students are advised to check their particulars mentioned below i.e. names, permanent & postal address, institutions, their CNIC numbers and their Domiciles. If there is any correction required they should send email with existing particulars or applicant’s eligibility reference No. to Mr. Shamim Iqbal, Senior Vice President, NBP at e-mail [email protected] within fifteen (15) days of this announcement. ** All those un-successful students who could not meet the qualification/eligibility criteria of the Students Loan Scheme are advised that if they are eager to know the assigned reason of their disqualification they may send e-mail at the above mentioned address. -

Development Budget Estimates 2018-19

DISTRICT Project Description BE 2018-19 BANNU BU16D00400-1-No R/Wall & 1-No P/Wall at UC Bharat 875,000 BANNU BU16D00401-Const. of R/Wall & P/Band at UC Kakki-I 875,000 BANNU BU16D00402-Const. of R/Wall & P/Band at UC ShamshiKhel 134,000 BANNU BU16D00403-Const. of R/Wall & P/Band at UC Mandew 875,000 BANNU BU16D00404-Const. of R/Wall & P/Band at UC KhanderKhan khel 875,000 BANNU BU16D00405-Const. of R/Wall & P/Band at UC SlemaSikander Khel 875,000 BANNU BU16D00406-Const. of R/Wall & P/Band at UC Nurar 825,000 BANNU BU16D00407-Const. of R/Wall & P/Band at UC ShamshiKhel 184,000 BANNU BU16D00408-Const. of R/Wall & P/Band at UC JhanduKhel 825,000 BANNU BU16D00409-Const. of R/Wall & P/Band/Pond at UCDomel 865,000 BANNU BU16D00410-Const. of R/Wall & P/Band at UC MamaKhel 875,000 BANNU BU16D00411-Const. of R/Wall & P/Band/Pond at UCAsperka Waziran 875,000 BANNU BU16D00412-Const. of R/Wall & P/Band UC ZerakiPirba Khel 595,000 BANNU BU16D00413-Const. of R/Wall & P/Band At InayatullahBarmi Khel 800,000 BANNU BU16D00414-Const. of R/Wall & P/Band at BakhtawarSada Khel 700,000 BANNU BU16D00415-Const. of R/Wall & P/Band (Allah Nawaz)Kotka Zaray Madi Khel 700,000 BANNU BU16D00416-Imp:/lining of Water Courses atPanakzai. 695,000 BANNU BU16D00417-Imp:/lining of Water Courses at Degan 845,000 BANNU BU16D00418-Const: of Lining at Hinjal Amir Khan &Hinjal Noor Baz. 845,000 BANNU BU16D00419-Const: of Lining at Tarkhoba AsperkaWaziran 217,000 BANNU BU16D00420-Imp:/lining of Water Courses at KamaChashmai 845,000 BANNU BU16D00421-Imp:/lining of Water Courses -

Multi-Cluster Initial Rapid Assessment BANNU REPORT

Multi-Cluster Initial Rapid Assessment BANNU REPORT JULY 2014 1 | Page Table of Contents 1.0 Executive Summary........................................................................................................3 2.0 Background....................................................................................................................4 3.0 Objectives.......................................................................................................................6 4.0 Methodology...................................................................................................................6 5.0 Limitations......................................................................................................................7 6.0 Cluster Findings 6.1 Education.........................................................................................................7 6.2 Food Security.....................................................................................................10 6.3 Health................................................................................................................13 6.4 Nutrition............................................................................................................20 6.5 Protection..........................................................................................................23 6.6 Shelter..............................................................................................................34 6.7 Water Sanitation and Hygiene (WASH)............................................................36