Deals in Greece 2017 One More Year of Low Investment Activity Mainly Driven by the Disposal of Non-Core Assets by the Systemic Banks

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

National Competition Report Q2 2017

NATIONAL COMPETITION QUARTERLY REPORT APRIL– JUNE 2017 BELGIUM basis of their “Best and Final Offer.” Third, Infrabel issued individual calls for specific orders within the This section reviews developments under Book IV of the terms and conditions of the framework agreement. The Belgian Code of Economic Law (“CEL”) on the selected companies had to submit their best offer for Protection of Competition, which is enforced by the each call, and the orders were awarded to the lowest Belgian Competition Authority (“the BCA”). Within the bidder. BCA, the Prosecutor General and its staff of prosecutors (collectively, the “Auditorate”) investigate In 2013, the Auditorate started investigating this public alleged restrictive practices and concentrations, while procurement following ABB’s leniency application. the Competition College (the “College”) functions as The investigation revealed that the bidders had agreed the decision-making body. Prior to September 6, 2013, to allocate the orders placed by Infrabel amongst Belgian competition law was codified in the Act on the themselves. For each call, they exchanged price Protection of Economic Competition of September 15, information and instructions to ensure that the 2006 (“APEC”) and enforced by the Belgian pre-designated participant would present the lowest Competition Authority, then composed of the price and win the tender. The Auditorate found that Directorate General for Competition and the these practices had started in 2010–2011 and continued Competition Council. When relevant, entries in this until June 2016. The Auditorate notified its objections report will refer to the former sub-bodies of the BCA. to the companies in August 2016, and settlement talks began a month later. -

Annual Report 2007 Design - Production: 2007 2007

NEMESIS S.A. Annual Report 2007 Design - Production: 2007 2007 12A Irodou Attikou str., Annual Report Maroussi 151 24, Athens - GREECE Tel.: (+30) 210 809 4000, Fax: (+30) 210 809 4444 www.moh.gr CMYK CORINTH REFINERIES S.A. Annual Report 2007 TableTable of of contents contents 1 INFORMATION CONCERNING THIS ANNUAL REPORT AND THE COMPANY AUDITORS............................6 2 SHAREHOLDERS’ RIGHTS ..............................................................................................................................8 2.1 General Information ..................................................................................................................................8 2.2 Dividend Taxation......................................................................................................................................9 3 MARKET INFORMATION AND STRUCTURE ................................................................................................10 3.1 Structure of the Oil Refining Market in Greece ..........................................................................................10 3.2 Regulatory Framework ............................................................................................................................11 3.3 Recent Developments in the International Oil Market ................................................................................14 4 COMPANY PROFILE ......................................................................................................................................15 -

AXIA Research

Greece Outlook 2019: The year of the elections AXIA Research Table of Contents Start of a new era ......................................................................................................... 3 Early elections or at the end of the government’s term? ....................................................................... 3 Unexciting economic performance, while fiscal space shrinks without pro-growth ........................................... 4 Elections is the key catalyst for the markets .................................................................................... 5 Top picks ......................................................................................................................... 5 2019, the year of the elections ......................................................................................... 6 The day after the Prespa Agreement ......................................................................................................................................... 6 Timing of elections: May vs. September/October ...................................................................................................................... 7 Looking at recent polls ............................................................................................................................................................... 9 Strategies by Syriza and ND ahead and after the elections ...................................................... 13 Syriza to try to close the gap with ND as is already regrouping -

Copy of Censusdata

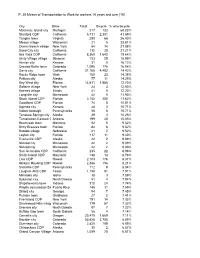

P. 30 Means of Transportation to Work for workers 16 years and over [16] City State Total: Bicycle % who bicycle Mackinac Island city Michigan 217 132 60.83% Stanford CDP California 5,711 2,381 41.69% Tangier town Virginia 250 66 26.40% Mason village Wisconsin 21 5 23.81% Ocean Beach village New York 64 14 21.88% Sand City city California 132 28 21.21% Isla Vista CDP California 8,360 1,642 19.64% Unity Village village Missouri 153 29 18.95% Hunter city Kansas 31 5 16.13% Crested Butte town Colorado 1,096 176 16.06% Davis city California 31,165 4,493 14.42% Rocky Ridge town Utah 160 23 14.38% Pelican city Alaska 77 11 14.29% Key West city Florida 14,611 1,856 12.70% Saltaire village New York 24 3 12.50% Keenes village Illinois 41 5 12.20% Longville city Minnesota 42 5 11.90% Stock Island CDP Florida 2,152 250 11.62% Goodland CDP Florida 74 8 10.81% Agenda city Kansas 28 3 10.71% Volant borough Pennsylvania 56 6 10.71% Tenakee Springs city Alaska 39 4 10.26% Tumacacori-Carmen C Arizona 199 20 10.05% Bearcreek town Montana 52 5 9.62% Briny Breezes town Florida 84 8 9.52% Barada village Nebraska 21 2 9.52% Layton city Florida 117 11 9.40% Evansville CDP Alaska 22 2 9.09% Nimrod city Minnesota 22 2 9.09% Nimrod city Minnesota 22 2 9.09% San Geronimo CDP California 245 22 8.98% Smith Island CDP Maryland 148 13 8.78% Laie CDP Hawaii 2,103 176 8.37% Hickam Housing CDP Hawaii 2,386 196 8.21% Slickville CDP Pennsylvania 112 9 8.04% Laughlin AFB CDP Texas 1,150 91 7.91% Minidoka city Idaho 38 3 7.89% Sykeston city North Dakota 51 4 7.84% Shipshewana town Indiana 310 24 7.74% Playita comunidad (Sa Puerto Rico 145 11 7.59% Dillard city Georgia 94 7 7.45% Putnam town Oklahoma 27 2 7.41% Fire Island CDP New York 191 14 7.33% Shorewood Hills village Wisconsin 779 57 7.32% Grenora city North Dakota 97 7 7.22% Buffalo Gap town South Dakota 56 4 7.14% Corvallis city Oregon 23,475 1,669 7.11% Boulder city Colorado 53,828 3,708 6.89% Gunnison city Colorado 2,825 189 6.69% Chistochina CDP Alaska 30 2 6.67% Grand Canyon Village Arizona 1,059 70 6.61% P. -

Folli - Follie Commercial Manufacturing and Technical

“FOLLI - FOLLIE COMMERCIAL MANUFACTURING AND TECHNICAL SOCIETE ANONYME” REG. NO.: 3027701000 23rd km ATHENS – LAMIA HIGHWAY 145 65, AG. STEFANOS, ATTICA ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD 01.01.2016 TO 31.12.2016 PURSUANT TO LAW 3556/2007 The attached financial statements for the period 01.01.2016-31.12.2016 were approved by the Company’s Board of Directors on April 7th of 2017 and were published by being posted in the internet, at www.ffgroup.com. They have been translated from the original statutory financial statements which have been prepared in Greek language. In the event that differences exist between this translation and the original Greek language financial statements, the Greek language financial statements will still prevail over this document. WorldReginfo - 79abb848-9027-4d49-b8b3-c6789fc2ca3e CONTENTS A. Statement of the Board of Directors ....................................................................... 5 B. Board of directors Annual Report for the fiscal period 01.01-31.12.2016 .................. 6 C. Independent certified auditors’ accountants report ............................................... 33 D. Financial Statements ........................................................................................... 35 1. Statements of Financial Position for the Group and the Company ........................... 35 1.1 Statement of Financial Position of the Group ................................................................................. 35 1.2 Statement of Financial Position of the Company ........................................................................... -

Exakm Sa Reference List of Major Project & Supplies 2000 – 2015

EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 Industrial Commercial & Technical Co. CLIENT EQUIPMENT BRAND PROJECT YEAR NEW INTERNATIONAL AIRPORT OF ERGOKAT ATE HYDRANTS ERHARD GmbH ATHENS 2000 “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF SAFETY VALVES FOR WATER SUPPLY ERGOKAT ATE BAILEY BIRKETT ATHENS 2000 NETWORK “EL. VENIZELOS” NEW INTERNATIONAL AIRPORT OF J/V ERGOKAT-ELTER-PYRAMIS Co- PENSTOCKS ERHARD GmbH ATHENS 2000 OPERATION “EL. VENIZELOS” BALL VALVES, BUTTERFLY VALVES, EVINOS & MORNOS RIVERS JUNCTION, TERNA SA ERHARD GmbH 2000 CONTROL VALVES TUNEL & DIVERTION GREEK SUGAR INDUSTRY PNEUMATIC CONTROL VALVES SAMSON AG EZA S.A 2000 FISCHER & UNILEVER S.A - ELAIS VARIABLE ARE FLOWMETERS PEIRAOS FACTORY 2000 PORTER – ABB EYATH - SEWAGE CENTRAL J/V ATHENA S.A – X. KONSTANTINIDIS PENSTOCKS ERHARD GmbH TRANSMISSION NETWORK OF 2000 S.A THESSALONIKI FISCHER & ATHENIAN BREWERY S.A ELECTROMAGNETIC FLOWMETERS “IOLI” NATURAL WATER PLANT 2000 PORTER – ABB MUNICIPAL ENTERPRISE OF WATER 122 DISTRICT HEATING CONSUMER SUPPLY AND SEWAGE OF KOZANI EXAKM SA KOZANI DISTRICT HEATING 2000 THERMAL SUBSTATIONS HYDROELECTRIC POWER PLANT OF HYDROENERGIAKI S.A PENSTOCKS ERHARD GmbH 2000 “ANTHOCHORI” EXAKM SA Page 1 of 21 Ave. Kallirrois 39 Tel.: +30 210 9215332, +30 210 9218441, +30 210 9216887 GR-11743 Athens Fax: +30 210 9218761 http://www.exakm.gr Factory & North Greece Branch: Ο.Τ 039Β – Insustrial Area of Sindos, GR-57022 Thessaloniki, Τel. +30 2310 799954, +30 2310 570387 EXAKM SA REFERENCE LIST OF MAJOR PROJECT & SUPPLIES 2000 – 2015 -

³Privatisation, Employment and Employees´ Nikiforos Manolas

&RQIHUHQFHRQ ³3ULYDWLVDWLRQ(PSOR\PHQWDQG(PSOR\HHV´ 1LNLIRURV0DQRODV (FRQRPLVW 0LQLVWU\RI(FRQRP\DQG)LQDQFH *UHHFH 5HJXODWRU\ 5HIRUPV 6WUXFWXUDO &KDQJHV DQG 3ULYDWLVDWLRQ LQ *UHHFH GXULQJ V 3DSHU VXEPLWWHG EXW QRW SUHVHQWHG ± 2FWREHU $WDN|\ ,VWDQEXO 7XUNH\ 5HJXODWRU\5HIRUPV6WUXFWXUDO&KDQJHVDQG3ULYDWLVDWLRQLQ*UHHFHGXULQJV ,%DFNJURXQG During 90s, for the fist time in post-war history, Greek strategies for economic development shifted markedly reliance on market forces rather than on state-managed growth. In the pre-1974 period Greece’s state-led development strategy based on import substitution and credit allocation produced strong growth (7% with manufacturing on the average at 11.4% annually), combined with low inflation (4%) and small balance of payments deficits (2.1% of GDP) until 1974. From 1974 until 1995 the economy showed a completely different picture. GDP annual growth rate averaged 2%, manufacturing growth slowed to almost zero, annual inflation averaged 18%, and the average external deficit, as a share of GDP, doubled. This performance was much worse than that of its neighbors and the other countries of the European Union (EU). The economic slowdown can be attributed almost completely to two major factors, namely the decline in the share of total investments in GDP, and the decline in the productivity of new investments. In an environment which had led to a downward spiral in economic performance, ultimately resulting in crisis (of slowing growth) and many large private firms that had grown rapidly in -

Constantinos Lambadarios

Constantinos Lambadarios Constantinos Lambadarios is one of the leading transactional lawyers in Greece. He is the firm’s managing partner and head of the M&A, Real Estate and Competition/Antitrust practice groups. Under his bold and progressive leadership, Lambadarios has grown to become a modern, internationally minded firm and is increasingly recognized as one of the legal powerhouses in Athens. Constantinos himself is a dynamic and highly experienced corporate lawyer and is ranked and listed in the major legal directories. He has played a leading role in many landmark transactions, supporting domestic and international clients in realizing their strategic goals, and has a reputation for being relentless in his pursuit of practical solutions to even the most complex challenges. He is recognized by clients and directories alike as a thoroughly modern lawyer, combining acute commercial awareness and strategic thinking with deep technical expertise and outstanding communication, team and leadership skills. As well as advising on sophisticated financial arrangements and corporate transactions, Constantinos is also a highly skilled arbitrator and accredited mediator. He has also been instrumental in establishing the firm’s Epaminondas Lambadarios Scholarship, a scholarship set up in partnership with The Geneva LL.M. in International Dispute Settlement (MIDS) for aspiring Greek lawyers interested in pursuing a career in international dispute management. M&A As head of the firm’s M&A practice, Constantinos is an experienced and astute legal adviser and dealmaker. He has supported domestic and international clients from many sectors on a wide range of complex corporate transactions, from privatizations, domestic and cross-border mergers and acquisitions and restructurings to spin offs and disposals, joint ventures and share-purchase agreements. -

FACTSHEET - AS of 27-Sep-2021 Solactive GBS Greece Large & Mid Cap USD Index PR

FACTSHEET - AS OF 27-Sep-2021 Solactive GBS Greece Large & Mid Cap USD Index PR DESCRIPTION The Solactive GBS Greece Large & Mid Cap USD Index PR is part of the Solactive Global Benchmark Series which includes benchmark indices for developed and emerging market countries. The index intends to track the performance of the large and mid cap segment covering approximately the largest 85% of the free-float market capitalization in the Greek market. It is calculated as a price returnindex in USD and weighted by free-float market capitalization. HISTORICAL PERFORMANCE 30,000 25,000 20,000 15,000 10,000 5,000 0 Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018 Jan-2020 Jan-2022 Solactive GBS Greece Large & Mid Cap USD Index PR CHARACTERISTICS ISIN / WKN DE000SLA88M4 / SLA88M Base Value / Base Date 20567.58 Points / 08.05.2006 Bloomberg / Reuters / .SGRLMCUP Last Price 1007.83 Index Calculator Solactive AG Dividends Not included Index Type Price Return Calculation 8:00 am to 10:30 pm (CET), every 15 seconds Index Currency USD History Available daily back to 08.05.2006 Index Members 11 FACTSHEET - AS OF 27-Sep-2021 Solactive GBS Greece Large & Mid Cap USD Index PR STATISTICS 30D 90D 180D 360D YTD Since Inception Performance -3.79% -1.94% 3.19% 42.80% 9.25% -95.10% Performance (p.a.) - - - - - -17.80% Volatility (p.a.) 14.64% 18.14% 18.18% 24.49% 19.34% 39.78% High 1061.99 1061.99 1090.57 1090.57 1090.57 29018.58 Low 1005.59 934.88 934.88 615.28 842.27 523.70 Sharpe Ratio -2.57 -0.43 0.35 1.77 0.65 -0.45 Max. -

Winter in Prague 144 Companies Representing 15 Countries Can Be Selected for Meetings Online

emerging europe conference Winter in Prague 144 companies representing 15 countries can be selected for meetings online Atrium / X5 / Banca Transilvania / Torunlar REIC have recently signed up click here Registration closes on Friday Tuesday to Friday 4 November For more information please contact your WOOD sales representative: 29 November to 2 December 2016 Warsaw +48 222 22 1530 Prague +420 222 096 452 Radisson Blu Alcron Hotel London +44 20 3530 0611 [email protected] Companies by country Bolded confirmed Companies by sector Bolded confirmed Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Biztonsagi Nyomda Nyrt. Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Agora AT&S Magyar Telekom Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka Asseco Poland CA Immobilien MOL Group Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim AT&S Conwert OTP Bank Electrica Cimsa Arcelik Banca Transilvania CME Erste Bank Wizz Air Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Cyfrowy Polsat S.A. Immofinanz Hidroelectrica Dogan Holding Atlantic Grupa BGEO Ciech LiveChat Software PORR Poland Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Pekao Cimsa Luxoft Raiffeisen Bank Agora OMV Petrom Ford Otosan CCC Bank Zachodni WBK Dogus Otomotiv Magyar Telekom RHI Alior Bank Romgaz Garanti Coca-Cola Icecek Bucharest Stock Exchange Ford Otosan O2 Czech Republic Uniqa AmRest SIF-2 Moldova Halkbank DIXY CSOB Grupa Azoty Orange Polska Vienna Insurance Group Asseco Poland Transelectrica Lokman Hekim Eurocash Erste Bank Grupa Kęty OTE Warimpex Bank Millennium Transgaz Migros Ticaret Folli Follie Eurobank HMS Group Turk Telekom Wienerberger Bank Pekao Pegasus Airlines Fortuna Garanti Industrial Milk Company Wirtualna Polska Holding Bank Zachodni WBK Russia Sabanci Holding Gorenje Getin Noble Bank Intercars Croatia CCC DIXY Teknosa Hellenic Petroleum Halkbank Mytilineos Atlantic Grupa Ciech Gazprom Tofas Kernel Hellenic Bank Pegas Nonwovens Podravka Cyfrowy Polsat S.A. -

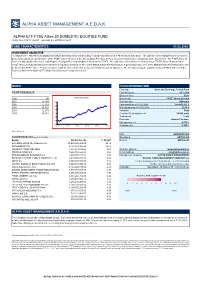

Alpha Asset Management Α.Ε.D.Α.Κ

ALPHA ASSET MANAGEMENT Α.Ε.D.Α.Κ. ALPHA ETF FTSE Athex 20 DOMESTIC EQUITIES FUND HCMC Rule 789/13.12.2007 Gov.Gaz. s.n. 2474/B/31.12.07 FUND CHARACTERISTICS 01.02.2008 INVESTMENT OBJECTIVE The Alpha ETF FTSE Athex 20 DOMESTIC EQUITIES FUND is the first Exchange Traded Fund listed on the Athens Stock Exchange. The objective of the Mutual Fund’s investment policy is to replicate the performance of the FTSE® Athex 20 Index of the Athens Stock Exchange in Euro, by mirror matching the composition of the Benchmark. The FTSE® Athex 20 Index is a big capitalization Index, capturing the 20 largest blue chip companies listed on the ATHEX. The total value of investments in shares of the FTSE® Athex 20 Index and in FTSE® Athex 20 Index derivatives accounts for a regulatory minimum of 95% of the Mutual Fund’s Net Asset Value. A percentage up to 35% of the Mutual Fund’s Net Asset Value may be invested in FTSE® Athex 20 Index derivatives with the aim of achieving the Mutual Fund’s investment objectives. The derivatives may be tradable (such as FTSE® Athex 20 Index futures) and/or non-tradable (OTC Swap Transactions) in a regulated market. INDEX FUND INFORMATION Fund type Domestic Exchange Traded Fund PERFORMANCE First listing date 24.1.2008 Base currency Euro Year (%) FTSE Athex 20 Index Benchmark FTSE® Athex 20 Index 2007 15,79% 3300 Currency risk Minimum 2006 17,73% Fund assets as of 01.02.2008 141.403.221 € 2800 2005 30,47% Net unit price as of 01.02.2008 23,40 € 2004 32,27% 2300 Valuation Daily 2003 35,43% 1800 Creation / Redemption unit 50.000 units 1300 Trading unit 1 unit Dividends Annual - 30 June 800 Management fee 0,275% 300 31/12/02 31/12/03 31/12/04 31/12/05 31/12/06 31/12/07 Custodian fee 0,100% Source: Bloomberg ISIN GRF000013000 COMPOSITION (as of 01.02.2008) Bloomberg AETF20 GA Equity Market Cap (€) % Weight Reuters AETF20.AT NATIONAL BANK OF GREECE S.A. -

WOOD's Winter in Prague

emerging europe conference WOOD’s Winter in Prague Tuesday 5 December to Friday 8 December 2017 Please join us for our flagship event - now in its6th year - spanning 4 jam-packed days. We expect to host over 160 companies representing more than 15 countries. Click here & For more information please contact your WOOD sales representative: Tuesday: Energy, Industrials and Materials Register Warsaw +48 222 22 1530 Wednesday: TMT and Utilities Now! Prague +420 222 096 453 Thursday: Consumer, Healthcare and Real Estate London +44 20 3530 7685 Friday: Diversified and Financials [email protected] Invited Companies by country Bolded confirmed Austria Hungary Kruk LUKOIL Aygaz AT & S ANY LPP Luxoft BIM Atrium Budapest Stock Exchange Mabion M.video Bizim Toptan BUWOG Gedeon Richter mBank Magnit Brisa DO&CO Graphisoft Park Medicalgorithmics MMK Cimsa Erste Group Bank MOL Group Orange Polska Moscow Exchange Coca-Cola Icecek Immofinanz OTP Bank Pfleiderer Group Mostotrest Dogus Otomotiv OMV Waberer’s PGE MTS Erdemir PORR Wizz Air PGNiG NLMK Garanti Raiffeisen Bank Iraq PKN Orlen Norilsk Nickel Halkbank Strabag DNO PKO BP NovaTek Is REIT Telekom Austria Genel Energy PKP Cargo O’KEY Isbank Uniqa Kazakhstan PLAY PIK Kardemir Vienna Insurance Group KMG EP Prime Car Management Polymetal International Koc Holding Warimpex Nostrum Oil & Gas PZU Polyus Lokman Hekim Croatia Steppe Cement Synthos Raven Russia Migros Ticaret Podravka Lithuania Tauron Rosneft Otokar Czech Republic Siauliu Bankas Warsaw Stock Exchange Rostelecom Pegasus Airlines CEZ Poland