AXIA Research

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Folli - Follie Commercial Manufacturing and Technical

“FOLLI - FOLLIE COMMERCIAL MANUFACTURING AND TECHNICAL SOCIETE ANONYME” REG. NO.: 3027701000 23rd km ATHENS – LAMIA HIGHWAY 145 65, AG. STEFANOS, ATTICA ANNUAL FINANCIAL STATEMENTS FOR THE PERIOD 01.01.2016 TO 31.12.2016 PURSUANT TO LAW 3556/2007 The attached financial statements for the period 01.01.2016-31.12.2016 were approved by the Company’s Board of Directors on April 7th of 2017 and were published by being posted in the internet, at www.ffgroup.com. They have been translated from the original statutory financial statements which have been prepared in Greek language. In the event that differences exist between this translation and the original Greek language financial statements, the Greek language financial statements will still prevail over this document. WorldReginfo - 79abb848-9027-4d49-b8b3-c6789fc2ca3e CONTENTS A. Statement of the Board of Directors ....................................................................... 5 B. Board of directors Annual Report for the fiscal period 01.01-31.12.2016 .................. 6 C. Independent certified auditors’ accountants report ............................................... 33 D. Financial Statements ........................................................................................... 35 1. Statements of Financial Position for the Group and the Company ........................... 35 1.1 Statement of Financial Position of the Group ................................................................................. 35 1.2 Statement of Financial Position of the Company ........................................................................... -

Winter in Prague 144 Companies Representing 15 Countries Can Be Selected for Meetings Online

emerging europe conference Winter in Prague 144 companies representing 15 countries can be selected for meetings online Atrium / X5 / Banca Transilvania / Torunlar REIC have recently signed up click here Registration closes on Friday Tuesday to Friday 4 November For more information please contact your WOOD sales representative: 29 November to 2 December 2016 Warsaw +48 222 22 1530 Prague +420 222 096 452 Radisson Blu Alcron Hotel London +44 20 3530 0611 [email protected] Companies by country Bolded confirmed Companies by sector Bolded confirmed Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Biztonsagi Nyomda Nyrt. Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Agora AT&S Magyar Telekom Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka Asseco Poland CA Immobilien MOL Group Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim AT&S Conwert OTP Bank Electrica Cimsa Arcelik Banca Transilvania CME Erste Bank Wizz Air Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Cyfrowy Polsat S.A. Immofinanz Hidroelectrica Dogan Holding Atlantic Grupa BGEO Ciech LiveChat Software PORR Poland Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Pekao Cimsa Luxoft Raiffeisen Bank Agora OMV Petrom Ford Otosan CCC Bank Zachodni WBK Dogus Otomotiv Magyar Telekom RHI Alior Bank Romgaz Garanti Coca-Cola Icecek Bucharest Stock Exchange Ford Otosan O2 Czech Republic Uniqa AmRest SIF-2 Moldova Halkbank DIXY CSOB Grupa Azoty Orange Polska Vienna Insurance Group Asseco Poland Transelectrica Lokman Hekim Eurocash Erste Bank Grupa Kęty OTE Warimpex Bank Millennium Transgaz Migros Ticaret Folli Follie Eurobank HMS Group Turk Telekom Wienerberger Bank Pekao Pegasus Airlines Fortuna Garanti Industrial Milk Company Wirtualna Polska Holding Bank Zachodni WBK Russia Sabanci Holding Gorenje Getin Noble Bank Intercars Croatia CCC DIXY Teknosa Hellenic Petroleum Halkbank Mytilineos Atlantic Grupa Ciech Gazprom Tofas Kernel Hellenic Bank Pegas Nonwovens Podravka Cyfrowy Polsat S.A. -

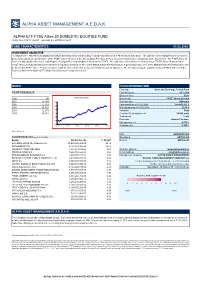

Alpha Asset Management Α.Ε.D.Α.Κ

ALPHA ASSET MANAGEMENT Α.Ε.D.Α.Κ. ALPHA ETF FTSE Athex 20 DOMESTIC EQUITIES FUND HCMC Rule 789/13.12.2007 Gov.Gaz. s.n. 2474/B/31.12.07 FUND CHARACTERISTICS 01.02.2008 INVESTMENT OBJECTIVE The Alpha ETF FTSE Athex 20 DOMESTIC EQUITIES FUND is the first Exchange Traded Fund listed on the Athens Stock Exchange. The objective of the Mutual Fund’s investment policy is to replicate the performance of the FTSE® Athex 20 Index of the Athens Stock Exchange in Euro, by mirror matching the composition of the Benchmark. The FTSE® Athex 20 Index is a big capitalization Index, capturing the 20 largest blue chip companies listed on the ATHEX. The total value of investments in shares of the FTSE® Athex 20 Index and in FTSE® Athex 20 Index derivatives accounts for a regulatory minimum of 95% of the Mutual Fund’s Net Asset Value. A percentage up to 35% of the Mutual Fund’s Net Asset Value may be invested in FTSE® Athex 20 Index derivatives with the aim of achieving the Mutual Fund’s investment objectives. The derivatives may be tradable (such as FTSE® Athex 20 Index futures) and/or non-tradable (OTC Swap Transactions) in a regulated market. INDEX FUND INFORMATION Fund type Domestic Exchange Traded Fund PERFORMANCE First listing date 24.1.2008 Base currency Euro Year (%) FTSE Athex 20 Index Benchmark FTSE® Athex 20 Index 2007 15,79% 3300 Currency risk Minimum 2006 17,73% Fund assets as of 01.02.2008 141.403.221 € 2800 2005 30,47% Net unit price as of 01.02.2008 23,40 € 2004 32,27% 2300 Valuation Daily 2003 35,43% 1800 Creation / Redemption unit 50.000 units 1300 Trading unit 1 unit Dividends Annual - 30 June 800 Management fee 0,275% 300 31/12/02 31/12/03 31/12/04 31/12/05 31/12/06 31/12/07 Custodian fee 0,100% Source: Bloomberg ISIN GRF000013000 COMPOSITION (as of 01.02.2008) Bloomberg AETF20 GA Equity Market Cap (€) % Weight Reuters AETF20.AT NATIONAL BANK OF GREECE S.A. -

Marfin Investment Group Financial Results: First Half 2013

Investor Relations +30 210 3504046 www.marfininvestmentgroup.com Investor Release 2 September 2013 MARFIN INVESTMENT GROUP FINANCIAL RESULTS: FIRST HALF 2013 MIG achieves operating EBITDA profitability from recurring business operations (€11.1m vs. €1.6m losses in H1 2012) Consolidated H1 2013 revenues of €581.3m, 3.6% annual reduction, amid ongoing adverse economic and market conditions. Consolidated Q2 2013 revenues of €313.2m, vs. €323.3m in Q2 2012, implying a deceleration to the annual rate of revenue decline on a quarterly basis. H1 2013 EBITDA from recurring business operations 1 of €11.1m, a significant improvement vs. €1.6m loss in H1 2012, attributed to market share gains, expanding gross profit margins, cost containment effectiveness and improved efficiency. Reported group EBITDA of €4.0m, vs. €7.6m loss in H1 2012. Consolidated net loss, after tax and minorities, of €139.7m, adversely impacted by one-off deferred taxes (€35m) and discontinued operations’ losses (€22.8m), vs. €960.5m losses in H1 2012. H1 2013 Net Asset Value (NAV) of €1.23bn (vs. €1.30bn in FY2012), translating to a NAV per share of €1.59 (vs. €1.68 in FY2012). Cash balances, including restricted cash, of €177m at group and €100m at parent company level. Group receivables from the Greek state at €130m in H1 2013 vs. €146m in FY2012. Continuous dynamic asset rebalancing, aimed at deleveraging, yields the desired results, as consolidated gross debt declined by €61m vs. FY2012. Convertible Bond Loan (CBL) issue (29.07.2013) was covered by a total amount of €215m, of which €211.9m originated from the tender for exchange of bonds issued by the Company on 19.03.2010 and €3.1m represents new capital from the exercise of pre-emption rights. -

Winter in Prague Tuesday 5 December to Friday 8 December 2017

emerging europe conference Winter in Prague Tuesday 5 December to Friday 8 December 2017 Our 2017 event held over 4 informative and jam-packed days, will continue the success of the previous five years and host almost 3,000 investor meetings, with over 160 companies representing 17 countries, covering multiple sectors. For more information please contact your WOOD sales representative: WOOD & Company Save Warsaw +48 222 22 1530 the Date! Prague +420 222 096 452 conferences 2017 London +44 20 3530 0611 [email protected] Participating companies in 2016 - by country Participating companies in 2016 - by sector Austria Hungary Romania Turkey Consumer Financials Healthcare TMT Atrium ANY Banca Transilvania Anadolu Efes Aegean Airlines Alior Bank Georgia Healthcare Group Asseco Poland AT&S Budapest Stock Exchange Bucharest Stock Exchange Arcelik AmRest Alpha Bank Krka AT&S CA Immobilien Magyar Telekom Conpet Bizim Toptan Anadolu Efes Athex Group (Hellenic Exchanges) Lokman Hekim CME Conwert MOL Group Electrica Cimsa Arcelik Banca Transilvania Cyfrowy Polsat S.A. Erste Bank OTP Bank Fondul Proprietatea Coca-Cola Icecek Astarta Bank Millennium Industrials Luxoft Immofinanz Wizz Air Hidroelectrica Dogan Holding Atlantic Grupa BGEO Aeroflot Magyar Telekom PORR Nuclearelectrica Dogus Otomotiv Bizim Toptan Bank Zachodni WBK Cimsa O2 Czech Republic RHI Kazakhstan OMV Petrom Ford Otosan CCC Bucharest Stock Exchange Ciech Orange Polska Uniqa Insurance Group Steppe Cement Romgaz Garanti Coca-Cola Icecek Budapest Stock Exchange Dogus Otomotiv OTE Vienna -

Company Country

Company Country 1 Teva Pharmaceutical ISR 2 Coca-Cola HBC AG GRC 3 Bank Hapoalim ISR 4 Israel Chemicals ISR 5 Bank Leumi ISR 6 Bezeq ISR 7 Azrieli Group ISR 8 Hellenic Telecommunications Organization S.A. GRC 9 Nice Systems ISR 10 Elbit Systems ISR 11 OPAP GRC 12 Mizrahi Tefahot Bank Ltd. ISR 13 Delek Group ISR 14 Frutarom ISR 15 Osem Investments ISR 16 Israel Discount Bank ISR 17 Israel Corporation ISR 18 Hellenic Petroleum S.A. GRC 19 Gazit Globe (1982) Ltd ISR 20 BANK OF CYPRUS PUBLIC COMPANY LTD CYP 21 Titan Cement Co. S.A. GRC 22 Melisron ISR 23 Alpha Bank S.A. GRC 24 National Bank of Greece S.A. GRC 25 Paz Oil ISR 26 Strauss Group ISR 27 Folli Follie GRC 28 Motor Oil Hellas Corinth Refineries S.A. GRC 29 First Intl Bank of Israel (5) ISR 30 Public Power Corp. S.A. GRC 31 Jumbo S.A. GRC 32 Oil Refineries ISR 33 Alony Hetz Properties & Inv ISR 34 Tower Semiconductor Ltd ISR 35 Migdal Insurance & Financial Holdings Ltd. ISR 36 Grivalia Properties R.E.I.C GRC 37 Harel Investments & Finance ISR 38 Delek Automotive Systems ISR 39 Amot Investments Ltd. ISR 40 Clal Insurance ISR 41 Delta Galil Industries ISR 42 Shikun & Binui Ltd ISR 43 Airport City Ltd ISR 44 Kenon Holdings ISR 45 Athens Water Supply & Sewerage GRC 46 Ezchip Semiconductor ISR 47 Jerusalem Oil Exploration ISR 48 Phoenix Holdings ISR Company Country 49 IDI Insurance Company Ltd ISR 50 Cellcom Israel Ltd. ISR 51 Partner Communications ISR 52 VIOHALCO SA/NV (CB) GRC 53 Mytilineos Holdings S.A. -

Folli-Follie Commercial Manufacturing and Technical Societe Anonyme Interim Financial Statements for the Period 01.01.2016 To

“FOLLI-FOLLIE COMMERCIAL MANUFACTURING AND TECHNICAL SOCIETE ANONYME” REG. NO.: 3027701000 23RD KM ATHENS – LAMIA HIGHWAY 145 65, AG. STEFANOS, ATTICA INTERIM FINANCIAL STATEMENTS ΕΞΑΜΗΝΙΑΙΑ ΟΙΚΟΝΟΜΙΚΗ ΕΚΘΕΣΗ FOR THE PERIOD 01.01.2016 TO 30.06.2016 ΤΗΣ ΠΕΡΙΟΔΟΥ ΑΠΟ 01.01.2014 ΕΩΣ 30.06.2014 According to International Financial Reporting Standards Σύμφωνα με τα Διεθνή Πρότυπα Χρηματοοικονομικής (IFRS) Αναφοράς (ΔΠΧΑ) (IAS 34) (Δ.Λ.Π. 34) The attached interim financial statements for the period 01.01.2016 – 30.06.2016 were approved by the Company’s Board of Directors on September 12th of 2016 and were published by being posted in the Internet, at www.ffgroup.com. WorldReginfo - f205a615-664a-4035-a365-e76309bc1d9d Table of Contents A. Statement of the Board of Directors ................................................................................................... 4 B. Directors’ Management Report for the period 01.01.2016 – 30.06.2016 ........................................ 5 C. Auditor’s review report on interim financial statements ............................................................... 16 D. Interim Financial Statements for the period 01/01/2016 to 30/06/2016 ........................................ 17 1. Statements of Financial Position for the Group and the Company .............................................. 17 1.1 Statement of Financial Position of the Group ......................................................................................... 17 1.2 Statement of Financial Position of the Company .................................................................................. -

PRESS RELEASE Q1 2016 Results

27 May 2016 PRESS RELEASE Q1 2016 Results Consolidated EBITDA from business operations 1 increased 60.2% to €26.5m vs. €16.5m in Q1 2015 Consolidated Q1 2016 revenues amounted to €245m, recording a marginal decline of €1.2m, or -0.5% vs. Q1 2015. The marginal reduction is attributed to the prolonged economic recession in Greece, as the GDP in Q1 2016 declined by -1.3% vs. Q1 2015, as well as to the ongoing challenging economic and market conditions in the majority of the business sectors. Consolidated EBITDA from business operations increased 60.2% to €26.5m vs €16.5m in Q1 2015. The increase is primarily attributed to the marked profitability improvement of subsidiaries ATTICA, VIVARTIA and HYGEIA. Group consolidated EBITDA (including holding companies) increased 75.6% to €23.4m vs. €13.3m in Q1 2015. Group consolidated EBITDA margin almost doubled to 9.6% vs. 5.4% in Q1 2015. The widening margin is attributed to efficiency improvements as well as cost containment effectiveness. In May 2016, the Company issued a new common bond loan amounting to €150m, which EUROBANK ERGASIAS undertook to cover, to refinance an equivalent amount of an existing debt facility. The refinancing agreement provides for the long-term restructuring of the said debt, by extending the maturity by 3 years (October 2019). With this agreement, the Company completed the long-term restructuring of the entirety of its outstanding common bond loans, achieving the extension of the maturity horizon. 1 Consolidated EBITDA from business operations is defined as Group EBITDA excluding holding companies and non-recurring items. -

4Q:15 Results Release Tuesday March 29 PPC Wednesday March 30, OPAP,LAMDA Thursday March 31Frigoglass, Ellaktor, Gek Terna, Athens Water, Anemos

Weekly Review 24 03 2016 News Flow Eurogroup Head Jeroen Dijsselbloem in a formal statement stated that talks between the Greek government and institutions have been productive, with significant progress made on outstanding issues such as income tax and pension reforms, while work is ongoing and will continue over the Easter break. The statement also noted that mission chiefs will return to Athens on 2 April to resume the discussions with a view to conclude them as soon as possible. Greek Finance Minister Euclid Tsakalotos told Parliament that the government aims to conclude the negotiations over the program review by April 12-13, so an agreement with the institutions can be reached on both the obligations of Greece (under the new program) and the debt issue by April 22. German Finance Minister Wolfgang Schaeuble stated that alternatives must be found if Greece cannot deliver on pension reforms. At the same time, the Greek government continues to blame the stance of the IMF on the review negotiations, while US Treasury Secretary Jack Lew repeated that the IMF will not participate in the current Greek program if there is no debt relief. Macro/Political State Budget primary balance for Jan-Feb 2016 surplus EUR3.038bn vs. target of EUR1.065bn. Current account deficit (Jan-16) at EUR 742m, up EUR 461m y-o-y Reportedly GR deposits declined by EUR 1.0bn in February 2016 Turnover Index in Industry (Jan-16) -13.3% y-o-y. Travel receipts in January 2016 decreased by 4.7% y-o-y According to press Eurobank is in the final stages of entering -

28,9% Group Share of Net Profit 52,5 49,3 6,3% Amortisation - Depreciation 13,0 11,9 9,2% EBITDA 105,5 97,8 7,9%

FOLLI FOLLIE GROUP First Half 2012 Financial Results August 30th, 2012 Revenue split by geographical region North America 2,0% Greece 40,0% Asia incl. Japan 49,0% Europe 9,0% FF Group – First Half 2012 Financial Results Presentation August 30th, 2012, p.2 FF Group – Financial Highlights First Half 2012 . Taking into consideration the strong recession in Greece impacted by double elections, a further hike in unemployment, strong pressure on the socioeconomic environment and pessimism regarding new measures, the FF Group succeeded to increase its top to bottom line performance. The Jewellery, Watches and Accessories activity exceeded the Group’s expectation and increased revenues by 20.3%. Despite the brands expansions margins could be kept at high levels. The Travel Retail activity was impacted by a decline in departing passengers, negative news flow on Greece as a travel destination, but also on high last year comparables. The retail activity of the travel retail segment increased revenues in the first half by 5% reaching €109.7, whereas revenues of the wholesale activity declined by 18,1% to €9.3m. The Retail and Wholesale segment was clearly affected by adverse local conditions, which intensified especially in the second quarter of the year. First half revenues declined single digit (-6.5%), the second quarter declined by 7.6%. Revenues of Department Stores declined by 3.4% in the second quarter, compared to a decline of 11.5% in Q1, mainly supported by the operation of the third attica store in Thessaloniki. FF Group – First Half 2012 -

A Policy for Success

bponline.amcham.gr MAY-JUNE 2014 Vol. XIII | No. 72 Thought Leaders Golden Bullets in Technolgy BUSINESS MATTERS— JIM DAVIS OF NEW BALANCE ▼ PANAGIOTIS G. MIHALOS, SECRETARY GENERAL, MFA ▼ GOOGLE, THE INTERNET, AND IMPACTING SOCIETY ▼ PLUS BIZ BUZZ TRENDS & TRADE MAKERS VIEWPOINT MetLife— AMERICAN-HELLENIC A Policy For Success CHAMBER OF COMMERCE www.amcham.gr Dimitris Mazarakis Vice Chairman BoD & Managing Director, MetLife Register Now Greek Investment June 11-12, 2014 Forum The Athens Exchange and the AEGEAN AIRLINES American-Hellenic Chamber of Commerce ALPHA BANK are pleased to invite you to this year’s ATTICA BANK Investment Forum: CORINTH PIPEWORKS ELLAKTOR Participants: GR for Growth EUROBANK EUROBANK PROPERTIES JUNE 11-12, 2014 FOLLI FOLLIE GROUP Harmonie Club, 4 East 60th St, GEK TERNA New York, NY 10022 GR. SARANTIS HELLENIC EXCHANGES The Forum will bring together HELLENIC PETROLEUM key government of cials and INTRALOT leading Greek and U.S. LAMDA DEVELOPMENT business leaders to explore Greece’s MARFIN INVESTMENT GROUP improving investment climate, METKA key privatization initiatives MOTOR OIL MYTILINEOS and investment opportunities. NATIONAL BANK of GREECE Institutional investors OPAP will also have the opportunity to meet PIRAEUS BANK with senior executives PLAISIO of Greece’s leading listed companies. TERNA ENERGY THRACE PLASTICS The Forum will take place on June 11. TITAN One-on-one investor meetings will take HELLENIC REPUBLIC ASSET place on June 11-12. DEVELOPMENT FUND Gold sponsors: Silver sponsors: Hellenic American -

Investor Release 1 April 2014

Investor Relations +30 210 3504046 www.marfininvestmentgroup.com Investor Release 1 April 2014 MARFIN INVESTMENT GROUP FINANCIAL RESULTS: FULL YEAR 2013 Significant profitability improvement: EBITDA from business operations at €62.0m vs. €29.1m in FY2012 Consolidated FY2013 revenues of €1,189.0m vs €1,264.4m a year ago, due to the prolonged challenging economic and market conditions and the exceptional impact to Hygeia Group (€28m charge booked in Q4 2013) related to the legal obligation to implement the automatic claw back and rebate mechanisms in the healthcare sector. Excluding this exceptional impact, consolidated revenues declined 3.7% y-o-y, matching the annual real GDP contraction in Greece. EBITDA from business operations 1 at €62.0m, 113% improvement vs. €29.1m in FY2012, attributed to widening gross profit margins, cost containment effectiveness and improved efficiency. The profitability improvement is primarily associated to better results from ATTICA, VIVARTIA and FAI. Reported consolidated EBITDA turns profitable at €8.6m, vs. €50.9m loss a year ago, reflecting the substantial profitability improvement of business operations, despite the significant €28m impact to Hygeia Group EBITDA related to the aforesaid government policy decisions in the healthcare sector. Consolidated net loss, after tax and minorities, of €203.3m, adversely impacted by one-off deferred taxes (€35m), negative revaluation of investment property (€10.8m vs €43.2m a year ago) and impairment charges (€47.5m vs. €1,091m in FY2012). The relevant bottom-line loss in FY2012 stood at €1,298.0m. Net Asset Value (NAV) at €967m (vs. €1,297m on 31.12.2012), translating to a NAV per share of €1.26 (vs.