Company Presentation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

ELLAKTOR Presentation March 5Th, 2020 Table of Contents

ELLAKTOR Presentation March 5th, 2020 Table of contents 1 Executive summary 2 Business Overview 3 Capital Structure 4 9M 2019 Financials 1 1 Executive summary 2 Business Overview 3 Capital Structure 4 9M 2019 Financials 2 Executive Summary ELLAKTOR history 1950s-1990s 1990s-2000s 2000-2009 2010-2018 2018 - forward 1950s: Establishment of 1999: Led domestic 2007: Acquisition of TEB, ELLINIKI construction sector Pantechniki, leading to Industry TECHNODOMIKI and consolidation (Merger of controlling stake in Attiki consolidation AKTOR TEB, Elliniki Odos (59%) Technodomiki & AKTOR) 1996: Signed first 2003: Entry into concession projects environment segment Diversification (Attiki Odos and Rio- 2008: Signed 3 out of 5 of activities Antirrio Bridge) major concession projects awarded in Greece 2004: First international 2012: c. €600m of construction contracts in projects in the Balkans Romania and Kuwait Geographic 2014: €3.2bn Doha metro 2005: Internationalisation diversification project in Qatar of HELECTOR through acquisition of Herhof GmbH 2010-2012: Sale of gold 2018: Sale of Athens Resort assets Casino (€13.5 ml) Focus on core 2014: ELTECH ANEMOS 2018: Increased stake in IPO Attiki Odos by 6.5% competencies 2019: Sold Corporate Headquarters (€25.5 ml) and stake in Elpedison (€ 18 ml) 2015: 1st Waste PPP in July 2018: Newly elected Greece Board post 1st proxy fight in Renewed 2016: Moreas completed Greece opportunity / in full operation July 2019: Group 2017-18 :Olympia Odos rationalization / ELTECH & Maliakos completed ANEMOS absorption 4 The ELLAKTOR group led the construction sector consolidation in Greece H’ (Highest) grade construction companies in 1998 (€m) 7th grade(1) construction companies in 2018 (€m)(2) Thessaliki SA Etep SA Parnon SA Themeli SA Odon & Odostromaton SA Ekter SA INTRAKAT SA Gekat SA Europaiki Techniki SA I.G. -

Elteb Annual Report 2003

22000033 A N N U A L R E P O R T TABLE OF CONTENTS IMPORTANT NOTICE………………………………………………………..5 1. COMPANY SUMMARY FINANCIAL FIGURES…………………………..5 2. CONSOLIDATED SUMMARY FINANCIAL DATA………………………..9 3. INFROMATION ON THE PERSONS RESBONSIBLE FOR THE ANNUAL REPORT AND THE COMPANY AUDITORS…………………………… 12 4. SHAREHOLDERS’ RIGHTS……………………………………………… 19 4.1 General………………………………………………………………………… 19 4.2 Taxation of dividends……………………………………………………………… 21 4.3 Shareholders’ obligations……………………………………………………… 21 5. STOCK EXCHANGE INFORMATION ON COMPANY SHARES…… 22 6. INFORMATION ON THE SHARES…………………………………… 24 7. INFORMATION ABOUT THE COMPANY………………………… 24 7.1 General Information …………………………………………………………… 24 7.2 Brief History………………………………………………………………… 26 7.3 Outline of Operations ………………………………………………………. 27 7.4 Co-financed projects…………………………………………………………….... 30 7.5 Fixed Assets …………………………………………………………………… 36 7.6 General Information on the Company’s Share Capital………………………… 38 7.7 Shareholders………………………………………………………………….........41 7.8 Management – Administration …………………………………………………....42 7.9 Participation of Elliniki Technodomiki Teb’s main Shareholders and members of the Board of Directors in the capital or management of other companies………………48 7.10 Organizational Chart……………………………………………………………… 52 7.11 Personnel……………………………………………………………………… 53 7.12 Investments ………………………………………………………………… 53 7.13 Use of capital raised through the last share capital increase…………………… 56 8. FINANCIAL HIGHLIGHTS……………………………………………… 59 8.1 Activity………………………………………………………………………… 59 8.2 Profit/Loss for 2001-2003…………………………………………………… -

Interim Condensed Financial Information in Accordance with International Accounting Standard 34 for the Period from 1 January to 30 September 2020

Interim condensed financial information in accordance with International Accounting Standard 34 for the period from 1 January to 30 September 2020 ELLAKTOR S.A. 25 ERMOU ST - 145 64 KIFISIA Tax Registration No: 094004914 ATHENS TAX OFFICE FOR SOCIÉTÉS ANONYMES Société Anonyme Registration No: 874/06/Β/86/16 – File No: 100065 General Electronic Commercial Registry (G.E.MI.) Reg. No: 251501000 (1) / (53) ELLAKTOR SA Interim condensed financial information in accordance with International Accounting Standard 34 for the period from 1 January to 30 September 2020 All amounts are in € thousand, unless stated otherwise Contents of Interim condensed financial information Statement of Financial Position .................................................................................................3 Income Statement for the 9-month period 2020 and 2019 .........................................................4 Income Statement Q3 2020 and 2019 ........................................................................................5 Statement of Comprehensive Income of the 9-month period 2020 and 2019 ..............................6 Statement of Comprehensive Income Q3 2020 and 2019 ...........................................................7 Statement of Changes in Equity ................................................................................................8 Statement of Cash Flows ......................................................................................................... 10 Notes to the interim condensed financial information -

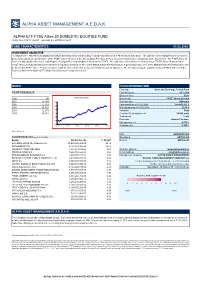

Alpha Asset Management Α.Ε.D.Α.Κ

ALPHA ASSET MANAGEMENT Α.Ε.D.Α.Κ. ALPHA ETF FTSE Athex 20 DOMESTIC EQUITIES FUND HCMC Rule 789/13.12.2007 Gov.Gaz. s.n. 2474/B/31.12.07 FUND CHARACTERISTICS 01.02.2008 INVESTMENT OBJECTIVE The Alpha ETF FTSE Athex 20 DOMESTIC EQUITIES FUND is the first Exchange Traded Fund listed on the Athens Stock Exchange. The objective of the Mutual Fund’s investment policy is to replicate the performance of the FTSE® Athex 20 Index of the Athens Stock Exchange in Euro, by mirror matching the composition of the Benchmark. The FTSE® Athex 20 Index is a big capitalization Index, capturing the 20 largest blue chip companies listed on the ATHEX. The total value of investments in shares of the FTSE® Athex 20 Index and in FTSE® Athex 20 Index derivatives accounts for a regulatory minimum of 95% of the Mutual Fund’s Net Asset Value. A percentage up to 35% of the Mutual Fund’s Net Asset Value may be invested in FTSE® Athex 20 Index derivatives with the aim of achieving the Mutual Fund’s investment objectives. The derivatives may be tradable (such as FTSE® Athex 20 Index futures) and/or non-tradable (OTC Swap Transactions) in a regulated market. INDEX FUND INFORMATION Fund type Domestic Exchange Traded Fund PERFORMANCE First listing date 24.1.2008 Base currency Euro Year (%) FTSE Athex 20 Index Benchmark FTSE® Athex 20 Index 2007 15,79% 3300 Currency risk Minimum 2006 17,73% Fund assets as of 01.02.2008 141.403.221 € 2800 2005 30,47% Net unit price as of 01.02.2008 23,40 € 2004 32,27% 2300 Valuation Daily 2003 35,43% 1800 Creation / Redemption unit 50.000 units 1300 Trading unit 1 unit Dividends Annual - 30 June 800 Management fee 0,275% 300 31/12/02 31/12/03 31/12/04 31/12/05 31/12/06 31/12/07 Custodian fee 0,100% Source: Bloomberg ISIN GRF000013000 COMPOSITION (as of 01.02.2008) Bloomberg AETF20 GA Equity Market Cap (€) % Weight Reuters AETF20.AT NATIONAL BANK OF GREECE S.A. -

Building the Future December 2020

Building the future December 2020 CONFIDENTIAL 1 Disclaimer This presentation including the information and opinions presented therein (‘Information’) is confidential and is not to be circulated to any person or entity without the prior written consent of Reggeborgh. References to Reggeborgh should be interpreted to include any of its affiliates or subsidiaries. The Information has been obtained or derived from sources believed by Reggeborgh to be reliable at the date of publication of this presentation. Reggeborgh’s opinions and estimates constitute Reggeborgh’s judgement and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification thereof, the accuracy and completeness of all Information available. The Information may be subject to change, and Reggeborgh assumes no undertaking to revise or amend the Information provided, or to provide any update in respect of any change related thereto. No representation or warranty express or implied, is or will be made in relation to, and no responsibility or liability is or will be accepted by Reggeborgh (or any of its respective directors, officers, employees, advisers, agents, representatives) as to or in relation to, the accuracy or completeness of this presentation or any further written or oral information made available to you or your advisers. Reggeborgh expressly disclaims any and all liability for loss which may be based on the Information contained in this presentation, errors therein or omissions there from. In particular, no representation or warranty is given as to the accuracy of any Information (financial or otherwise) contained herein, or as to the achievement or reasonableness of any forecasts, projections, management targets, prospects or returns. -

Marfin Investment Group Financial Results: First Half 2013

Investor Relations +30 210 3504046 www.marfininvestmentgroup.com Investor Release 2 September 2013 MARFIN INVESTMENT GROUP FINANCIAL RESULTS: FIRST HALF 2013 MIG achieves operating EBITDA profitability from recurring business operations (€11.1m vs. €1.6m losses in H1 2012) Consolidated H1 2013 revenues of €581.3m, 3.6% annual reduction, amid ongoing adverse economic and market conditions. Consolidated Q2 2013 revenues of €313.2m, vs. €323.3m in Q2 2012, implying a deceleration to the annual rate of revenue decline on a quarterly basis. H1 2013 EBITDA from recurring business operations 1 of €11.1m, a significant improvement vs. €1.6m loss in H1 2012, attributed to market share gains, expanding gross profit margins, cost containment effectiveness and improved efficiency. Reported group EBITDA of €4.0m, vs. €7.6m loss in H1 2012. Consolidated net loss, after tax and minorities, of €139.7m, adversely impacted by one-off deferred taxes (€35m) and discontinued operations’ losses (€22.8m), vs. €960.5m losses in H1 2012. H1 2013 Net Asset Value (NAV) of €1.23bn (vs. €1.30bn in FY2012), translating to a NAV per share of €1.59 (vs. €1.68 in FY2012). Cash balances, including restricted cash, of €177m at group and €100m at parent company level. Group receivables from the Greek state at €130m in H1 2013 vs. €146m in FY2012. Continuous dynamic asset rebalancing, aimed at deleveraging, yields the desired results, as consolidated gross debt declined by €61m vs. FY2012. Convertible Bond Loan (CBL) issue (29.07.2013) was covered by a total amount of €215m, of which €211.9m originated from the tender for exchange of bonds issued by the Company on 19.03.2010 and €3.1m represents new capital from the exercise of pre-emption rights. -

AXIA Research

AXIA Research Bloomberg <AXVA> Greece-Daily Note April 13, 2018 Headlines Athens General Index Macroeconomic News According to press, EuroWorking Group (EWG) officials told the Greek government that the draft growth strategy it presented for the day after Greece’s exit from the adjustment program, needs to be more precise in specific areas and to clearly account for the associated costs on the budget. According to Kathimerini, in parallel to the EWG meeting yesterday, there was also a Washington Group meeting yesterday. Debt relief and reforms will be the focus in today’s meeting between the Greek Finance Minister Euclid Tsakalotos and his German counterpart Olaf Scholz in Berlin. ELSTAT announced that the seasonally adjusted unemployment rate for January 2018 came to 20.6% compared to the upward revised 23.2% in January 2017 and 20.8% in December 2017. According to ELSTAT, total building activity in Jan’18 on the basis of issued permits increased close daily % Ytd % by 18.0% y-o-y, by 45.8% in volume terms while increased by 45.2% in surface terms. For the Athens General 806.08 0.85% 0.46% Market Turnover (EURm) 60.847 21.35% rolling 12-month period, building permits are up 9.2% (+20.7% surface, +23.5% volume). Market Cap (EURbn) 55.507 Market Cap / GDP* 29.67% Additional Headlines *2016 th ECB’s Governing Council on April 11 lowered the ELA ceiling for Greek banks by EUR 1.9bn to FTSE ASE movers (last trading day) EUR 14.7bn TOP Aegean Airlines announced that traffic volumes in 1Q18 increased by 12%. -

PRESS RELEASE Q1 2016 Results

27 May 2016 PRESS RELEASE Q1 2016 Results Consolidated EBITDA from business operations 1 increased 60.2% to €26.5m vs. €16.5m in Q1 2015 Consolidated Q1 2016 revenues amounted to €245m, recording a marginal decline of €1.2m, or -0.5% vs. Q1 2015. The marginal reduction is attributed to the prolonged economic recession in Greece, as the GDP in Q1 2016 declined by -1.3% vs. Q1 2015, as well as to the ongoing challenging economic and market conditions in the majority of the business sectors. Consolidated EBITDA from business operations increased 60.2% to €26.5m vs €16.5m in Q1 2015. The increase is primarily attributed to the marked profitability improvement of subsidiaries ATTICA, VIVARTIA and HYGEIA. Group consolidated EBITDA (including holding companies) increased 75.6% to €23.4m vs. €13.3m in Q1 2015. Group consolidated EBITDA margin almost doubled to 9.6% vs. 5.4% in Q1 2015. The widening margin is attributed to efficiency improvements as well as cost containment effectiveness. In May 2016, the Company issued a new common bond loan amounting to €150m, which EUROBANK ERGASIAS undertook to cover, to refinance an equivalent amount of an existing debt facility. The refinancing agreement provides for the long-term restructuring of the said debt, by extending the maturity by 3 years (October 2019). With this agreement, the Company completed the long-term restructuring of the entirety of its outstanding common bond loans, achieving the extension of the maturity horizon. 1 Consolidated EBITDA from business operations is defined as Group EBITDA excluding holding companies and non-recurring items. -

4Q:15 Results Release Tuesday March 29 PPC Wednesday March 30, OPAP,LAMDA Thursday March 31Frigoglass, Ellaktor, Gek Terna, Athens Water, Anemos

Weekly Review 24 03 2016 News Flow Eurogroup Head Jeroen Dijsselbloem in a formal statement stated that talks between the Greek government and institutions have been productive, with significant progress made on outstanding issues such as income tax and pension reforms, while work is ongoing and will continue over the Easter break. The statement also noted that mission chiefs will return to Athens on 2 April to resume the discussions with a view to conclude them as soon as possible. Greek Finance Minister Euclid Tsakalotos told Parliament that the government aims to conclude the negotiations over the program review by April 12-13, so an agreement with the institutions can be reached on both the obligations of Greece (under the new program) and the debt issue by April 22. German Finance Minister Wolfgang Schaeuble stated that alternatives must be found if Greece cannot deliver on pension reforms. At the same time, the Greek government continues to blame the stance of the IMF on the review negotiations, while US Treasury Secretary Jack Lew repeated that the IMF will not participate in the current Greek program if there is no debt relief. Macro/Political State Budget primary balance for Jan-Feb 2016 surplus EUR3.038bn vs. target of EUR1.065bn. Current account deficit (Jan-16) at EUR 742m, up EUR 461m y-o-y Reportedly GR deposits declined by EUR 1.0bn in February 2016 Turnover Index in Industry (Jan-16) -13.3% y-o-y. Travel receipts in January 2016 decreased by 4.7% y-o-y According to press Eurobank is in the final stages of entering -

A Policy for Success

bponline.amcham.gr MAY-JUNE 2014 Vol. XIII | No. 72 Thought Leaders Golden Bullets in Technolgy BUSINESS MATTERS— JIM DAVIS OF NEW BALANCE ▼ PANAGIOTIS G. MIHALOS, SECRETARY GENERAL, MFA ▼ GOOGLE, THE INTERNET, AND IMPACTING SOCIETY ▼ PLUS BIZ BUZZ TRENDS & TRADE MAKERS VIEWPOINT MetLife— AMERICAN-HELLENIC A Policy For Success CHAMBER OF COMMERCE www.amcham.gr Dimitris Mazarakis Vice Chairman BoD & Managing Director, MetLife Register Now Greek Investment June 11-12, 2014 Forum The Athens Exchange and the AEGEAN AIRLINES American-Hellenic Chamber of Commerce ALPHA BANK are pleased to invite you to this year’s ATTICA BANK Investment Forum: CORINTH PIPEWORKS ELLAKTOR Participants: GR for Growth EUROBANK EUROBANK PROPERTIES JUNE 11-12, 2014 FOLLI FOLLIE GROUP Harmonie Club, 4 East 60th St, GEK TERNA New York, NY 10022 GR. SARANTIS HELLENIC EXCHANGES The Forum will bring together HELLENIC PETROLEUM key government of cials and INTRALOT leading Greek and U.S. LAMDA DEVELOPMENT business leaders to explore Greece’s MARFIN INVESTMENT GROUP improving investment climate, METKA key privatization initiatives MOTOR OIL MYTILINEOS and investment opportunities. NATIONAL BANK of GREECE Institutional investors OPAP will also have the opportunity to meet PIRAEUS BANK with senior executives PLAISIO of Greece’s leading listed companies. TERNA ENERGY THRACE PLASTICS The Forum will take place on June 11. TITAN One-on-one investor meetings will take HELLENIC REPUBLIC ASSET place on June 11-12. DEVELOPMENT FUND Gold sponsors: Silver sponsors: Hellenic American -

Terna Energy – Company Update

Terna Energy – Company Update Terna Energy S.A. Renewable Energy / Greece Reuters/Bloomberg: TENr.AT / TENERGY GA October 16, 2018 Rating Buy Raising expectation and TP Previous Buy Terna Energy (TE) has posted a stellar performance, being one of the best performing names of the Greek market for 2018. The combination of sector dynamics, company fundamentals and management initiatives, Target Price 8.50 has driven TE’s share price up by 18.0% since our previous Buy recommendation (May 14th) and 36% ytd (EUR)Previous 6.50 (compared to Athex ytd losses of 21.0 %). During 1H18 results, management raised cash distribution guidance, Current Share Price* (EUR) 6.01 *15/10/ 2018 announcing EUR 0.30/sh capital return for Jan’19 (pending EGM approval) and pointing to annual cash distributions of EUR 50m (EUR 0.44/sh) in the coming years. At the same time 2018 is shaping, as we Stock Data highlighted in the beginning of the year (here), to an important period for the Greek RES sector, with maturing Market Cap (EUR m) 682.1 market conditions providing better clarity over the longer term and with the sector attracting significant Free Float 31% investment interest. Amid this environment we review our estimates and valuation on TE and we now raise EV (EUR m) 1,212 our TP to EUR 8.50/sh (vs. EUR 6.50/sh previously) and reiterate our Buy recommendation with a targeted Num. of Shares (m) 113m upside of 46% (including announced capital return). Having said that, we view the recent stock price decline due to the volatility in the domestic and global markets as an excellent opportunity to buy into the company. -

Investor Release 1 April 2014

Investor Relations +30 210 3504046 www.marfininvestmentgroup.com Investor Release 1 April 2014 MARFIN INVESTMENT GROUP FINANCIAL RESULTS: FULL YEAR 2013 Significant profitability improvement: EBITDA from business operations at €62.0m vs. €29.1m in FY2012 Consolidated FY2013 revenues of €1,189.0m vs €1,264.4m a year ago, due to the prolonged challenging economic and market conditions and the exceptional impact to Hygeia Group (€28m charge booked in Q4 2013) related to the legal obligation to implement the automatic claw back and rebate mechanisms in the healthcare sector. Excluding this exceptional impact, consolidated revenues declined 3.7% y-o-y, matching the annual real GDP contraction in Greece. EBITDA from business operations 1 at €62.0m, 113% improvement vs. €29.1m in FY2012, attributed to widening gross profit margins, cost containment effectiveness and improved efficiency. The profitability improvement is primarily associated to better results from ATTICA, VIVARTIA and FAI. Reported consolidated EBITDA turns profitable at €8.6m, vs. €50.9m loss a year ago, reflecting the substantial profitability improvement of business operations, despite the significant €28m impact to Hygeia Group EBITDA related to the aforesaid government policy decisions in the healthcare sector. Consolidated net loss, after tax and minorities, of €203.3m, adversely impacted by one-off deferred taxes (€35m), negative revaluation of investment property (€10.8m vs €43.2m a year ago) and impairment charges (€47.5m vs. €1,091m in FY2012). The relevant bottom-line loss in FY2012 stood at €1,298.0m. Net Asset Value (NAV) at €967m (vs. €1,297m on 31.12.2012), translating to a NAV per share of €1.26 (vs.