Game Developer Index 2011 Swedish Games Industry’S Reports 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Master's Thesis: Visualizing Storytelling in Games

Chronicle Developing a visualisation of emergent narratives in grand strategy games EDVARD RUTSTRO¨ M JONAS WICKERSTRO¨ M Master's Thesis in Interaction Design Department of Applied Information Technology Chalmers University of Technology Gothenburg, Sweden 2013 Master's Thesis 2013:091 The Authors grants to Chalmers University of Technology and University of Gothen- burg the non-exclusive right to publish the Work electronically and in a non-commercial purpose make it accessible on the Internet. The Authors warrants that they are the authors to the Work, and warrants that the Work does not contain text, pictures or other material that violates copyright law. The Authors shall, when transferring the rights of the Work to a third party (for example a publisher or a company), acknowledge the third party about this agreement. If the Authors has signed a copyright agreement with a third party regarding the Work, the Authors warrants hereby that they have obtained any necessary permission from this third party to let Chalmers University of Technology and University of Gothenburg store the Work electronically and make it accessible on the Internet. Chronicle Developing a Visualisation of Emergent Narratives in Grand Strategy Games c EDVARD RUTSTROM,¨ June 2013. c JONAS WICKERSTROM,¨ June 2013. Examiner: OLOF TORGERSSON Department of Applied Information Technology Chalmers University of Technology, SE-412 96, G¨oteborg, Sweden Telephone +46 (0)31-772 1000 Gothenburg, Sweden June 2013 Abstract Many games of high complexity give rise to emergent narratives, where the events of the game are retold as a story. The goal of this thesis was to investigate ways to support the player in discovering their own emergent stories in grand strategy games. -

THIS WEEK ...We Focus on Some More Titles That Have Made an Impression on Eurogamer Readers, and Reveal Why

Brought to you by Every week: The UK games market in less than ten minutes Issue 6: 14th - 20th July WELCOME ...to GamesRetail.biz, your weekly look at the key analysis, news and data sources for the retail sector, brought to you by GamesIndustry.biz and Eurogamer.net. THIS WEEK ...we focus on some more titles that have made an impression on Eurogamer readers, and reveal why. Plus - the highlights of an interview with Tony Hawk developer Robomodo, the latest news, charts, Eurogamer reader data, price comparisons, release dates, jobs and more! Popularity of Age of Conan - Hyborian Adventures in 2009 B AGE OF CONAN VS WII SPORTS RESORT #1 A This week we look at the Eurogamer buzz performance around two key products since the beginning of 2009. First up is the MMO Age of #10 Conan - a game which launched to great fanfare this time last year, but subsequently suffered from a lack of polish and endgame content. #100 Eurogamer.net Popularity (Ranked) Recently the developer, Funcom, attempted to reignite interest in the game by marketing the changes made in the build-up to its first anniversary - point A notes a big feature and #1000 Jul free trial key launch, while point B shows the Feb Mar Apr May Jun Jan '09 Age of Conan - Hyborian Adventures re-review which put the game right at the top of the pile earlier this month - whether that interest can be converted into subs is a different question, but the team has given itself a good Popularity of Wii Sports Resort in 2009 chance at least. -

The Videogame Style Guide and Reference Manual

The International Game Journalists Association and Games Press Present THE VIDEOGAME STYLE GUIDE AND REFERENCE MANUAL DAVID THOMAS KYLE ORLAND SCOTT STEINBERG EDITED BY SCOTT JONES AND SHANA HERTZ THE VIDEOGAME STYLE GUIDE AND REFERENCE MANUAL All Rights Reserved © 2007 by Power Play Publishing—ISBN 978-1-4303-1305-2 No part of this book may be reproduced or transmitted in any form or by any means – graphic, electronic or mechanical – including photocopying, recording, taping or by any information storage retrieval system, without the written permission of the publisher. Disclaimer The authors of this book have made every reasonable effort to ensure the accuracy and completeness of the information contained in the guide. Due to the nature of this work, editorial decisions about proper usage may not reflect specific business or legal uses. Neither the authors nor the publisher shall be liable or responsible to any person or entity with respects to any loss or damages arising from use of this manuscript. FOR WORK-RELATED DISCUSSION, OR TO CONTRIBUTE TO FUTURE STYLE GUIDE UPDATES: WWW.IGJA.ORG TO INSTANTLY REACH 22,000+ GAME JOURNALISTS, OR CUSTOM ONLINE PRESSROOMS: WWW.GAMESPRESS.COM TO ORDER ADDITIONAL COPIES OF THE VIDEOGAME STYLE GUIDE AND REFERENCE MANUAL PLEASE VISIT: WWW.GAMESTYLEGUIDE.COM ACKNOWLEDGEMENTS Our thanks go out to the following people, without whom this book would not be possible: Matteo Bittanti, Brian Crecente, Mia Consalvo, John Davison, Libe Goad, Marc Saltzman, and Dean Takahashi for editorial review and input. Dan Hsu for the foreword. James Brightman for his support. Meghan Gallery for the front cover design. -

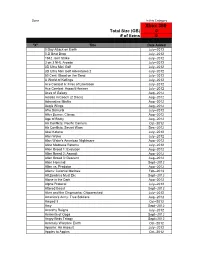

Xbox 360 Total Size (GB) 0 # of Items 0

Done In this Category Xbox 360 Total Size (GB) 0 # of items 0 "X" Title Date Added 0 Day Attack on Earth July--2012 0-D Beat Drop July--2012 1942 Joint Strike July--2012 3 on 3 NHL Arcade July--2012 3D Ultra Mini Golf July--2012 3D Ultra Mini Golf Adventures 2 July--2012 50 Cent: Blood on the Sand July--2012 A World of Keflings July--2012 Ace Combat 6: Fires of Liberation July--2012 Ace Combat: Assault Horizon July--2012 Aces of Galaxy Aug--2012 Adidas miCoach (2 Discs) Aug--2012 Adrenaline Misfits Aug--2012 Aegis Wings Aug--2012 Afro Samurai July--2012 After Burner: Climax Aug--2012 Age of Booty Aug--2012 Air Conflicts: Pacific Carriers Oct--2012 Air Conflicts: Secret Wars Dec--2012 Akai Katana July--2012 Alan Wake July--2012 Alan Wake's American Nightmare Aug--2012 Alice Madness Returns July--2012 Alien Breed 1: Evolution Aug--2012 Alien Breed 2: Assault Aug--2012 Alien Breed 3: Descent Aug--2012 Alien Hominid Sept--2012 Alien vs. Predator Aug--2012 Aliens: Colonial Marines Feb--2013 All Zombies Must Die Sept--2012 Alone in the Dark Aug--2012 Alpha Protocol July--2012 Altered Beast Sept--2012 Alvin and the Chipmunks: Chipwrecked July--2012 America's Army: True Soldiers Aug--2012 Amped 3 Oct--2012 Amy Sept--2012 Anarchy Reigns July--2012 Ancients of Ooga Sept--2012 Angry Birds Trilogy Sept--2012 Anomaly Warzone Earth Oct--2012 Apache: Air Assault July--2012 Apples to Apples Oct--2012 Aqua Oct--2012 Arcana Heart 3 July--2012 Arcania Gothica July--2012 Are You Smarter that a 5th Grader July--2012 Arkadian Warriors Oct--2012 Arkanoid Live -

Playing with Race: the Ethics of Racialized Representations in E-Games

IRIE International Review of Information Ethics Vol. 4 (12/2005) Dean Chan Playing with Race: The Ethics of Racialized Representations in E-Games Abstract: Questions about the meanings of racialized representations must be included as part of developing an ethical game design practice. This paper examines the various ways in which race and racial contexts are repre- sented in a selected range of commercially available e-games, namely war, sports and action-adventure games. The analysis focuses on the use of racial slurs and the contingencies of historical re-representation in war games; the limited representation of black masculinity in sports games and the romanticization of ‘ghetto play’ in urban street games; and the pathologization and fetishization of race in ‘crime sim’ action-adventure games such as True Crime: Streets of LA. This paper argues for, firstly, a continuous critical engagement with these dominant representations in all their evolving forms; secondly, the necessary inclusion of reflexive precepts in e-games development contexts; and thirdly, the importance of advocating for more diverse and equitable racialized representations in commercial e-games. Agenda Introduction ........................................................................................................................................ 25 War Games and the Contingencies of Historical ‘Authenticity’................................................................... 26 Sports Games, Urban Spaces and ‘Pixilated Minstrelsy’ ........................................................................... -

«Акційні Товари З Кредитом До 25 Платежів Від Банків Пумб, «Отп Банк», «Альфа-Банк», «Укрсіббанк»», Мережею Магазинів Цитрус -Гаджети Та Аксесуари

ПРАВИЛА ПРОВЕДЕННЯ АКЦІЇ «Акційні товари з кредитом до 25 платежів від банків ПУМБ, «ОТП Банк», «Альфа-банк», «Укрсіббанк»», МЕРЕЖЕЮ МАГАЗИНІВ ЦИТРУС -ГАДЖЕТИ ТА АКСЕСУАРИ м. Одеса «29» липня 2020 р. 1. Організатори Акції 1.1. ТОВ «Цетехно». 1.2. Перший Український Міжнародний Банк, АТ «ОТП Банк», АТ «Альфа-банк», АТ «Укрсіббанк»». 2. Період проведення Акції: 2.1. Акція з акційним товаром триває з «30» липня 2020 р. до «03» серпня 2020 р. включно. 2.2. Для участі в Акції необхідно здійснити покупку акційного товару з акційного списку в мага- зині Цитрус або в інтернет-магазині citrus.ua у період з «30» липня 2020 р. до 21:00 «03» сер- пня 2020 р. включно. 2.3 Останнє замовлення, яке бере участь в акції, від інтернет-магазину citrus.ua повинно бути от- римано і сплачено до 21 години 00 хвилин «03» серпня 2020 року. Останнє замовлення, яке приймає участь у акції від роздрібних магазинів повинно бути спла- чено до 21:00 «03» серпня 2020 р. 3. Місце проведення Акції. 3.1. Акція проводиться на території України, крім зони проведення ООС та тимчасово окупо- ваних територій, у мережі магазинів «Цитрус», які знаходяться за адресою: 3.1.1. м. Одеса, пр-т Ак. Глушко, 16 Телефон: (048) 777 59 22 3.1.2. м. Одеса, Аркадійська Алея Телефон: (048) 705-47-04 3.1.3. м. Одеса, пр-т Добровольського, 114/2 (р-к Північний) Телефон: (048) 735-81-99 3.1.4. м. Одеса, вул. Корольова, 94 Телефон: (048) 735-81-01 3.1.5. м. Одеса, вул. Пантелеймонівська, 64 Телефон: (048) 35-67-27 3.1.6. -

Journal of Games Is Here to Ask Himself, "What Design-Focused Pre- Hideo Kojima Need an Editor?" Inferiors

WE’RE PROB NVENING ABLY ALL A G AND CO BOUT V ONFERRIN IDEO GA BOUT C MES ALSO A JournalThe IDLE THUMBS of Games Ultraboost Ad Est’d. 2004 TOUCHING THE INDUSTRY IN A PROVOCATIVE PLACE FUN FACTOR Sessions of Interest Former developers Game Developers Confer We read the program. sue 3D Realms Did you? Probably not. Read this instead. Computer game entreprenuers claim by Steve Gaynor and Chris Remo Duke Nukem copyright Countdown to Tears (A history of tears?) infringement Evolving Game Design: Today and Tomorrow, Eastern and Western Game Design by Chris Remo Two founders of long-defunct Goichi Suda a.k.a. SUDA51 Fumito Ueda British computer game developer Notable Industry Figure Skewered in Print Crumpetsoft Disk Systems have Emil Pagliarulo Mark MacDonald sued 3D Realms, claiming the lat- ter's hit game series Duke Nukem Wednesday, 10:30am - 11:30am infringes copyright of Crumpetsoft's Room 132, North Hall vintage game character, The Duke of industry session deemed completely unnewswor- Newcolmbe. Overview: What are the most impor- The character's first adventure, tant recent trends in modern game Yuan-Hao Chiang The Duke of Newcolmbe Finds Himself design? Where are games headed in the thy, insightful next few years? Drawing on their own in a Bit of a Spot, was the Walton-on- experiences as leading names in game the-Naze-based studio's thirty-sev- design, the panel will discuss their an- enth game title. Released in 1986 for swers to these questions, and how they the Amstrad CPC 6128, it features see them affecting the industry both in Japan and the West. -

Gabriel Flamm +46 736 987 582 [email protected]

Gabriel Flamm +46 736 987 582 [email protected] “My objective is to make sure you feel the intended emotion in every moment” May 2012 – present • Battlefiled V, EA Dice Cinematic Animator Took scenes from mockup in animation software to functional and ready for render farm in Frostbite Polished and finalized several scenes – characters, props, vehicles. • Star Wars Battlefront II, Lucasfilm, EA Dice Cinematics Heroes vs Villains – Intro My responsibility was to come up with ideas for intro moves and direct mocap actors Animate the cameras and set up the logic Galactic Assault - Intros & Outros I created all intros when it comes to character and vehicle animations timed to the systematic camera. I did also set up the cameras, unique for each team on all levels. The outros are real time events where I animated cameras, characters, vehicles and some of the existing VFX assets. Emotes I came up with all Emotes - both VO and motion, planned and directed motion capture I gave direction to a VO actor, to be used as a reference for all other VO actors I created briefs, material and demand lists for outsourcing as well as being part of the feedback process with the animation director • Battlefield 1, EA Dice Cinematic Animator Took scenes from mockup in animation software to functional and ready for render farm in Frostbite Polished and finalized several scenes Animated airplanes in Friends in high places Animated cameras, characters and objects in Nothing is written real time cinematic, timed to VO Added background characters where needed Implemented and polished a few in-game 1p and 3p animations. -

Video Games and the Mobilization of Anxiety and Desire

PLAYING THE CRISIS: VIDEO GAMES AND THE MOBILIZATION OF ANXIETY AND DESIRE BY ROBERT MEJIA DISSERTATION Submitted in partial fulfillment of the requirements for the degree of Doctor of Philosophy in Communications in the Graduate College of the University of Illinois at Urbana-Champaign, 2012 Urbana, Illinois Doctoral Committee: Professor Kent A. Ono, Chair Professor John Nerone Professor Clifford Christians Professor Robert A. Brookey, Northern Illinois University ABSTRACT This is a critical cultural and political economic analysis of the video game as an engine of global anxiety and desire. Attempting to move beyond conventional studies of the video game as a thing-in-itself, relatively self-contained as a textual, ludic, or even technological (in the narrow sense of the word) phenomenon, I propose that gaming has come to operate as an epistemological imperative that extends beyond the site of gaming in itself. Play and pleasure have come to affect sites of culture and the structural formation of various populations beyond those conceived of as belonging to conventional gaming populations: the workplace, consumer experiences, education, warfare, and even the practice of politics itself, amongst other domains. Indeed, the central claim of this dissertation is that the video game operates with the same political and cultural gravity as that ascribed to the prison by Michel Foucault. That is, just as the prison operated as the discursive site wherein the disciplinary imaginary was honed, so too does digital play operate as that discursive site wherein the ludic imperative has emerged. To make this claim, I have had to move beyond the conventional theoretical frameworks utilized in the analysis of video games. -

Game Developer Index 2012 Swedish Games Industry’S Reports 2013 Table of Contents

GAME DEVELOPER INDEX 2012 SWEDISH GAMES INDUSTRY’S REPORTS 2013 TABLE OF CONTENTS EXECUTIVE SUMMARY 2 WORDLIST 3 PREFACE 4 TURNOVER AND PROFIT 5 NUMBER OF COMPANIES 7 NUMBER OF EMPLOYEES 7 GENDER DISTRIBUTION 7 TURNOVER PER COMPANY 7 EMPLOYEES PER COMPANY 8 BIGGEST PLAYERS 8 DISTRIBUTION PLATFORMS 8 OUTSOURCING/CONSULTING 9 SPECIALISED SUBCONTRACTORS 9 DLC 10 GAME DEVELOPER MAP 11 LOCATION OF COMPANIES 12 YEAR OF REGISTRY 12 GAME SALES 13 AVERAGE REVIEW SCORES 14 REVENUES OF FREE-TO-PLAY 15 EXAMPLE 15 CPM 16 eCPM 16 NEW SERVICES, NEW PIRACY TARGETS 16 VALUE CHAIN 17 DIGITAL MIDDLEMEN 18 OUTLOOK 18 SWEDISH AAA IN TOP SHAPE 19 CONSOLES 20 PUBISHERS 20 GLOBAL 20 CONCLUSION 22 METHODOLOGY 22 Cover: Mad Max (in development), Avalanche Studios 1 | Game Developer Index 2012 EXECUTIVE SUMMARY The Game Developer Index maps, reports and analyzes the Swedish game devel- opers’ annual operations and international trends by consolidating their respective annual company accounts. Swedish game development is an export industry and operates in a highly globalized market. In just a few decades the Swedish gaming industry has grown from a hobby for enthusiasts into a global industry with cultural and economic importance. The Game Developer Index 2012 compiles Swedish company accounts for the most recently reported fiscal year. The report highlights: • Swedish game developers’ turnover grew by 60 percent to 414 million euro in 2012. A 215% increase from 2010 to 2012. • Most game developer companies (~60 percent) are profitable and the industry reported a combined profit for the fourth consecutive year. • Job creation and employment is up by 30 percent. -

Game Developer Index 2010 Foreword

SWEDISH GAME INDUSTRY’S REPORTS 2011 Game Developer Index 2010 Foreword It’s hard to imagine an industry where change is so rapid as in the games industry. Just a few years ago massive online games like World of Warcraft dominated, then came the breakthrough for party games like Singstar and Guitar Hero. Three years ago, Nintendo turned the gaming world upside-down with the Wii and motion controls, and shortly thereafter came the Facebook games and Farmville which garnered over 100 million users. Today, apps for both the iPhone and Android dominate the evolution. Technology, business models, game design and marketing changing almost every year, and above all the public seem to quickly embrace and follow all these trends. Where will tomorrow’s earnings come from? How can one make even better games for the new platforms? How will the relationship between creator and audience change? These and many other issues are discussed intensively at conferences, forums and in specialist press. Swedish success isn’t lacking in the new channels, with Minecraft’s unprecedented success or Battlefield Heroes to name two examples. Independent Games Festival in San Francisco has had Swedish winners for four consecutive years and most recently we won eight out of 22 prizes. It has been touted for two decades that digital distribution would outsell traditional box sales and it looks like that shift is finally happening. Although approximately 85% of sales still goes through physical channels, there is now a decline for the first time since one began tracking data. The transformation of games as a product to games as a service seems to be here. -

Jack Menhorn

JACK MENHORN address 1300 East Rollingwood Circle Profile Winston-Salem, NC 27105 My name is Jack Menhorn and I am a professional sound designer, tel 336-457-2225 implementer and composer. I have been making music and sounds for mail [email protected] games for over 7 years. I am currently the Editor in Chief of url www.jackmenhorn.com twitter @JackMenhorn DesigningSound.org. I like cats and robots linkedin JackMenhorn My most recent music and sound design demo reels may be found on my website. Experience Composer/Sound Designer, Freelance 2005-Present Projects: Oddworld: New ‘n’ Tasty - PS3, PS4, PS Vita, Wii U, PC, Mac, Linux (Out Spring 2014) -Additional Dialogue Editing and Additional Sound Design Nova-111 - Mac, PC, Linux -Sound Design, Technical Sound Design (FMOD), Music Star Trek Rivals - iOS -Sound Editing/Sound Design Gunhouse - PS Vita -Sound Design Leap Motion - PC -Sound Design/Composition for various projects including New User Orientation tutorial, The Weather Channel, “Volantes” and “Telekinetic”. Offworld- iOS -Sound design (sci-fi), audio implementation using Unity3D with custom animation and scripting plugins, additional music Kyoto - PC -Composer, Sound Design, Implementation (Ambient) Ravensword: Shadowlands - iOS/OSX/Steam -Additional Sound Design. Nominated for G.A.N.G Award 2013 for “Best Handheld Audio.” Hack Slash Loot - PC/Steam/Atari Lynx -Composer (Orchestral) Deep Dungeons of Doom - Ouya/iOS/Android -Sound Design The Haunted: Hells Reach- PC/Steam -Music, sound design (horror, character foley, monster voices,