FMC: Did We Miss It?

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

MCS AT&T Mobility User Rates

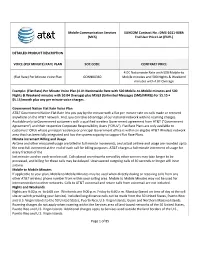

Mobile Communication Services SUNCOM Contract No.: DMS-1011-008A (MCS) End User Price List (EUPL) DETAILED PRODUCT DESCRIPTION VOICE (PER MINUTE) RATE PLAN SOC CODE CONTRACT PRICE 4.0¢ Nationwide Rate with 500 Mobile-to (Flat Rate) Per Minute Voice Plan ODNN00360 Mobile minutes and 500 Nights & Weekend minutes with 4.0¢ Overage Example: (Flat Rate) Per Minute Voice Plan (4.0¢ Nationwide Rate with 500 Mobile-to-Mobile minutes and 500 Nights & Weekend minutes with $0.04 Overage) plus MSG3 (Unlimited Messages (SMS/MMS)) for $5.15 = $5.15/month plus any per minute voice charges. Government Nation Flat Rate Voice Plan AT&T Government Nation Flat Rate lets you pay by the minute with a flat per-minute rate on calls made or received anywhere on the AT&T network. And, you can take advantage of our national network with no roaming charges. Available only to Government customers with a qualified wireless Government agreement from AT&T (“Government Agreement”) and their respective Corporate Responsibility Users (“CRUs”). Flat Rate Plans are only available to customers’ CRUs whose principal residence or principal Government office is within an eligible AT&T Wireless network area that has been fully integrated and has the system capacity to support Flat Rate Plans. Minute Increment Billing and Usage Airtime and other measured usage are billed in full-minute increments, and actual airtime and usage are rounded up to the next full increment at the end of each call for billing purposes. AT&T charges a full-minute increment of usage for every fraction of the last minute used on each wireless call. -

Exchange Pro VIO8 Skype™ on All of Your Office Phones

Your Ultimate Gateway to Skype™ Exchange Pro VIO8 Skype™ on All of Your Office Phones oSKY simplifies the deployment of Skype for the business environment with its turn-key VoSKY Exchange Pro VIO8 Connecting through Skype has its advantages. As the world's largest VPBX-to-Skype gateway to enable businesses of all sizes to VoIP network (over 200 million user worldwide), Skype can be used enhance communications and reduce telecom costs via Skype, the to leverage a trunking solution that allows businesses to realize world's largest VoIP network. The VoSKY Exchange Pro VIO8 is a tremendous savings over the cost of PSTN lines. Calls to other Skype stand alone, rack-mountable FXO PBX gateway that does not require users are free, while call to non-Skype users are charged at low-cost a PC. This plug & play appliance seamlessly integrates with any SkypeOut rates (or at a flat rate using Skype Unlimited). existing TDM or IP PBX through the analog station ports to add up to 8 lines to Skype. Multiple Exchange Pro gateways in different office Integration is another factor inVIO8's favor.Along with its single-box locations can be interconnected together to enable free calls between solution form factor and simple set up,VIO8 connects to an existing colleagues.Calls to other Skype users are free,while calls to non-Skype PBXphonesystemwithouttheneedtooverhaultheentirephonesystem, users are charged at low-cost SkypeOut rates. which can be a costly and time-consuming process. With its seamless installation (a VoSKY trademark), the VIO8 allows Leverage the Power of Skype with Four Business- anyone in the office to access a Skype line in record time. -

Voip for the Small Business Reducing Your Telecommunications Costs

VoIP for the Small Business Reducing your telecommunications costs Research firm IDC1 has estimated that a VoIP system can reduce telephony-related expenses by 30%. Voice over Internet Protocol (VoIP) has become a viable solution for even the smallest of companies as broadband internet access has become af- fordable and much more widespread. VoIP offers a low cost alternative to expensive traditional phone services, and is rapidly becoming the commu- nications system of choice to reduce telecommunications costs. Hosted VoIP services are also gaining popularity among smaller companies since these services do not require any investment in hardware. Your Rising Telecommunications Costs As a small business owner, you are under constant pressure to control your costs. You may have employees who work from home or who are mobile, such as salespeople, who make a high number of long-distance calls. As your business grows, your monthly phone bill likewise increases, TechAdvisory.org SME Reports sponsored by so you need to look for new but effective ways to minimize your telecom- munications costs. Based in Vancouver, Transparent focuses on Until recently, small businesses had no other real alternative to Public establishing long-term, mutually beneficial Switched Telephone Network (PSTN). However, today a technology called relationships with clients. Instead of banking Voice over Internet Protocol (VoIP) has become a viable solution for even on your system failures, our success is mea- small companies since broadband internet access has become more af- sured by your stability. Rather than sit around fordable and popular among small businesses. VoIP is a revolutionary and wait to profit from your problems, we work to prevent them. -

Exchange9140

Your Ultimate Gateway to Skype™ 9140/ EXCHANGE 9180 Skype™ on All of Your Office Phones Model # 9180 above & Model # 9140 below oSKY Technologies extends its VoIP product line with a new Works with almost any Analog or IP PBX generation of VoSKY Exchange, a family of PBX-to-Skype A major advantage of the VoSKY Exchange is its seamless integration gateways that enable businesses of all sizes to make and V with existing analog or IP PBX phone systems. Businesses are able to receive free and low-cost long-distance and international calls over preserve the investment in their existing phone systems while Skype,the world’s largestVoice over Internet Protocol (VoIP) network, enjoying the cost savings and flexibility of Skype without a major using existing office phone systems. forklift in equipment. The VoSKY Exchange 91xx is rack-mountable and adds up to eight outgoing Skype lines without changes to existing PBX or phone Easy to Use…No End User Training Required equipment. Multiple Exchange boxes can be set up to interconnect After installation, anyone in the office can access a Skype line. Just multiple offices anywhere in the world, enabling free calls between pick up the phone and press a preset number (8,for example),and the locations. Calls to other Skype users are free, while calls to non-Skype VoSKY Exchange finds an open line. And, since Exchange routes users are charged at low-cost SkypeOut rates or at a flat rate when Skype calls through the office PBX, calls are now made and received using Skype Unlimited. -

Cellular Mobile Pricing Structures and Trends”, OECD Digital Economy Papers, No

Please cite this paper as: OECD (2000-05-19), “Cellular Mobile Pricing Structures and Trends”, OECD Digital Economy Papers, No. 47, OECD Publishing, Paris. http://dx.doi.org/10.1787/236455705214 OECD Digital Economy Papers No. 47 Cellular Mobile Pricing Structures and Trends OECD Unclassified DSTI/ICCP/TISP(99)11/FINAL Organisation de Coopération et de Développement Economiques OLIS : 16-May-2000 Organisation for Economic Co-operation and Development Dist. : 19-May-2000 __________________________________________________________________________________________ Or. Eng. DIRECTORATE FOR SCIENCE, TECHNOLOGY AND INDUSTRY Unclassified DSTI/ICCP/TISP(99)11/FINAL COMMITTEE FOR INFORMATION, COMPUTER AND COMMUNICATIONS POLICY Working Party on Telecommunication and Information Services Policies CELLULAR MOBILE PRICING STRUCTURES AND TRENDS Or. Eng. 91220 Document complet disponible sur OLIS dans son format d’origine Complete document available on OLIS in its original format DSTI/ICCP/TISP(99)11/FINAL FOREWORD In November 1999, this report was presented to the Working Party on Telecommunications and Information Services Policy (TISP) and was recommended to be made public by the Committee for Information, Computer and Communications Policy (ICCP). The report was prepared by Dr. Sam Paltridge of the OECD’s Directorate for Science, Technology and Industry. It is published on the responsibility of the Secretary-General of the OECD. Copyright OECD, 2000 Applications for permission to reproduce or translate all or part of this material should be made to: -

The Economics of Internet Flat Rates*

THE ECONOMICS OF INTERNET FLAT RATES* Marc Bourreau** ENST – Department of Economics May 2001 Abstract Some studies suggest that the European Union lags behind the United States in Internet developments. The differences in pricing structures for Internet access may be one of the key factors to explain differences in Internet developments. For about a year, some Internet access providers have been experimenting unlimited Internet access services – “flat rates”. However, most of these unmetered Internet access services have been withdrawn soon after their launching. Some Internet access providers claim that the introduction of unmetered Internet wholesale services is needed to make “flat rates” commercially viable. This paper aims at providing a simple economic analysis of Internet flat rates, both at the retail and wholesale levels. In particular, I suggest that wholesale unmetered interconnection does not necessarily encourage the development of flat rates, but may encourage innovative pricing. Keywords: Internet access, Flat rate, Network economics. * This paper has benefited from the comments of Johannes Bauer. I am also grateful to Elisabeth Dognin, Christian Gacon, Philippe Barbet, Massimo Columbo and Jérôme Bezzina for useful comments and suggestions. The usual disclaimer applies. ** ENST, Department of Economics, 46 rue Barrault, 75634 Paris Cedex 13, France; Tel: +33 1 45 81 72 46; Fax: +33 1 45 65 95 15; E-mail: [email protected]. 1 1. Introduction Some studies suggest that the European Union (EU) lags behind the United States (US) in Internet developments. For instance, in a recent study, OECD develops indicators to compare countries with regard to Internet development. The study shows that there are far less Internet hosts or secure servers in European countries than in the US.1 It has been suggested that the differences in pricing structures for Internet access may be one of the key factors to explain differences in Internet developments. -

Softbank Catalogue (English)

E nglish INDEX PRICE PLAN INTERNATIONAL SERVICE Merihari Unlimited ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-1 Global Roaming Service/International Voice Calls and International SMS ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-11 Mini Fit Plan+・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-2 Smartphone Debut Plan・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-3 INFORMATION Mobile Handset Call Plan/ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-12 Mobile Handset 100 MB Plan・・・・・・・・・・・・・・・・・・・・・・・・ E-4 Notes on Usage ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-13 Data-Only 50 GB Plan/Data Share Plus Plan・・・・ E-5 Important Notes Tethering Option/ How to Apply ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-14 New All in the Family Discount ・・・・・・・・・・・・・・・・・・・・・ E-6 CAMPAIGN Supported Models iPhone iPhone 5s, iPhone 5c and later Home Discount ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-7 iPad iPad mini 2 and later Top-value Support+・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-8 Smartphones 4G/5G smartphones OPTIONAL SERVICES Mobile handset 4G mobile handsets, Simple Phone 10 Mobile data Warranty Service ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-9 communications Models on mobile data communications plans Security Service ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-10 Tablet Tablets MCHI1083 PRICE PLAN NEW English [Application] Required [New SoftBank members] Starts from the next billing month Merihari Unlimited [Existing SoftBank members] Starts from the next billing month; calls charge by usage For people who want to make the most of their smartphone! Basic charge -

Radio Access Network Dimensioning for 3G UMTS

Communication Networks University of Bremen Prof. Dr. rer. nat. habil. C. Görg Dissertation Radio Access Network Dimensioning for 3G UMTS by Xi Li from Hunan, China First examiner: Prof. Dr. rer. nat. habil. Carmelita Görg Second examiner: Prof. Dr.-Ing. Ralf Lehnert Submitted on: April 16, 2009 Date of exam: May 28, 2009 ACKNOWLEDGEMENT This thesis was written during my research as doctorate candidate at the Communication Networks Group (ComNets) at the University of Bremen within TZI (Center for Computer Science and Information Technology). Throughout the years at ComNets I have always enjoyed the very inspiring, encouraging, deeply rewarding, and exceptionally collegial research atmosphere. To the greatest extent I would like to thank Prof. Dr. rer. nat. habil. Carmelita Görg for her supervising this thesis, for her guidance, and her encouragements. She has given me a lot of great advices and inspiring ideas, not only to my thesis but also other scientific work. She has provided me an open and challenging research environment in the ComNets group where it is a pleasure to conduct research and to take teaching responsibilities. Furthermore, she has given me a lot of opportunities to participate in national and international workshops and conferences, which helped me keep an open mind and view on the ongoing research fields that have inspired me in many ways for my research work. Besides, I am also deeply grateful for the comments and suggestions by Prof. Dr.- Ing. Ralf Lehnert, who has been my Professor during my master study at Dresden University of Technology and who also is the second examiner of this thesis. -

Skype Goes Mobile

THE SUNDAY TIMES . MAY 11, 2008 InGear 7 Hello world, this is a cheap call doubt among some operators, and there Millions of mobile users can have been cases where Skype has been blocked by them,” said Gareth O’Loughlin, wave goodbye to hefty bills general manager of mobile and hardware devices at Skype. “Consumers should for international calls thanks absolutely have the right to choose which phone service they use.” to a new service. But how Not all the mobile networks have resorted to brute force, though. The fourth big good is it, asks Mark Harris network, Vodafone, takes a more pragmatic view. It offers unlimited browsing to most new contract customers, and has decided not to block mobile Voip applications. new mobile phone service that A Vodafone spokesman said: “Our internet allows users to chat with offering is unlimited so you can use it for friends in China for the anything you want. However, most of our price of calling their customers don’t use mobile Voip because they local takeaway sounds get customer service and quality of service Atoo good to be true. Last month, already with their traditional calling plan.” however, such an application was The mobile network 3 has embraced Skype made available as a free download and Voip technology, routing 100,000 minutes to almost anyone with a modern of calls via Skype every day. For a monthly fee of 3G phone. £12 it gives customers up to 4,000 minutes of It means that cheap free Skype-to-Skype calls each month — plus 100 international calls are available to minutes of normal calls — on its Skypephone millions of phone users — most mobile phone. -

Unlimited Voice Calls and Data with Softbank! for Smartphone! 3G Mobile Phone Too! INDEX PRODUCTS

English Unlimited voice calls and data with SoftBank! For smartphone! 3G mobile phone too! INDEX PRODUCTS 4G Smartphone E-1 Models / Specifications List E-2 PREPAID SERVICE Simple Style E-3 Wi-Fi ROUTER Mobile Data Communication E-4 PRICE PLAN Price Plan E-5 Discount Services Smartphone & Internet Bundle Discount E-7 SoftBank Hikari E-8 Tablet/Router Data Sharing E-9 Smartphone Flat-rate Family Discount, Long-term Loyalty Bonus E-10 Switchover & Trade-in Program, Feature Phone Switchover Discount E-11 Upgrade & Trade-in Program, Free Smartphone Exchange Program E-12 Early Upgrade Program E-13 Optional Services Backup Service Package (i) Plus, Backup Service Package Plus, Backup Service Package Plus E-14 iPhone Basic Pack, SMARTPHONE Basic Pack, Keitai Basic Pack E-15 Other Price Plans /Discounvt Services White Plan, Double White, White Plan Family Discount 24, Unlimited Packet Discount Flat, Unlimited Packet Discount E-16 Discounts for Purchasers Monthly Discounts E-17 Global Services Service Areas E-18 America Flat-rate Option E-19 INFORMATION Point Services T-Points, SoftBank Card E-20 Notes on usage E-21 How to Subscribe E-22 Customer Support General Information • Be sure to enter the telephone number correctly. From SoftBank handsets From fixed-line phones For assistance from abroad Japanese 1 5 7 (toll-free)* Japanese 0800-919-0157 (toll-free)* +81-92-687-0025 Inquiries English 1 5 7 (toll-free) 8 * English - - (toll-free) 8 * (International charges apply/Free from 0800 919 0157 SoftBank handsets.) (Chinese, Korean, Portuguese and Spanish are not available) (Chinese, Korean, Portuguese and Spanish are not available) *Only within Japan Japanese and English only (Chinese, Korean, • Not available from SoftBank handsets. -

Biased Choice of a Mobile Telephony Tariff Type

ZfTM-Work in Progress Nr. 84: Biased Choice of a Mobile Telephony Tariff Type – Exploring usage boundary perceptions as a cognitive cause in choosing between a use-based or a flat rate plan – Torsten J. Gerpott* 2007 * Univ.-Prof. Dr. Torsten J. Gerpott, Lehrstuhl Unternehmens- und Technologiemanagement, Schwerpunkt Telekommunikationswirtschaft, Uni- versität Duisburg-Essen, Lotharstr. 65, 47057 Duisburg. ZfTM-Work in Progress Nr. 84 Biased Choice of Tariff Type Abstract Most mobile network operators provide newly acquired or existing customers with the possibility to choose between a monthly flat rate for unlimited voice calls (to certain target networks) and pay-per-minute price schemes when they initially subscribe to the operator’s telephony service or change their tariff. Consumers who maximize their utility should select the tariff type that leads to the lowest invoice amount given their anticipated service usage volume. However, previous research looking at users of fixed network telephony, broadband Internet access and other services suggests that a significant share of consumers prefers a flat rate to use-dependent price plans even though their invoice will be higher. One cognitive explanation for such biased choices is that consumers consider the ra- tio of the likelihood of calling enough to justify a flat rate to the probability of not call- ing enough to save money with a fixed price (= “ratio rule”) when choosing between the two tariff types. In this assessment they overestimate the first likelihood in pro- portion to the second one. Drawing on a sample of 203 mobile telephony customers in Germany the present study shows that mobile users are biased in favor of a flat rate because they overestimate their future call usage and behave in line with the “ratio rule” when choosing a tariff type. -

Mobile Phone Service Guide English

E nglish MOBILE PHONE INDEX PRICE PLAN INTERNATIONAL SERVICE Global Roaming Service, Ultra GIGA MONSTER+ ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-1 International Voice Calls and International SMS ・・・・・・・・・・・・ E-9 Mini Monster ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-2 iPad/Tablet Price Plan ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-3 INFORMATION Mobile Handset Price Plan・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-4 Notes on Usage ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-10 Important Notes ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-11 CAMPAIGN How to Apply・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-12 Half Price Support and Monthly Discounts ・・・・・・・・・・・・・・・・・・ E-5 Home Bundle Discount Hikari Set・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-6 Supported Models iPhone iPhone 5s, iPhone 5c and later OPTIONAL SERVICES iPad iPad mini 2 and later 4G mobile handsets, 3G mobile handsets, E-7 Mobile handset Warranty Service ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ and Simple Phone 9 Security Service ・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・・ E-8 Mobile data communications 4G mobile handsets and Simple Phone 9 Tablet Tablets PRICE PLAN English [Application] Required iPhone [New SoftBank members] Starts from the rst month Ultra GIGA MONSTER Plus 4G smartphones [Existing SoftBank members] Starts from the next billing month No matter how much you use these 8 eligible services, GIGA No Count! GIGA No Count for all services during the available period! Limited time offer! GIGA unlimited use campaign on now (until