Monetary Policy in the Roman Empire Kevin Butcher University of Warwick

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

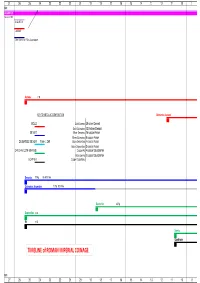

TIMELINE of ROMAN IMPERIAL COINAGE

27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 B.C. AUGUSTUS 16 Jan 27 BC AUGUSTUS CAESAR Other title: e.g. Filius Augustorum Aureus 7.8g KEY TO METALLIC COMPOSITION Quinarius Aureus GOLD Gold Aureus 25 silver Denarii Gold Quinarius 12.5 silver Denarii SILVER Silver Denarius 16 copper Asses Silver Quinarius 8 copper Asses DE-BASED SILVER from c. 260 Brass Sestertius 4 copper Asses Brass Dupondius 2 copper Asses ORICHALCUM (BRASS) Copper As 4 copper Quadrantes Brass Semis 2 copper Quadrantes COPPER Copper Quadrans Denarius 3.79g 96-98% fine Quinarius Argenteus 1.73g 92% fine Sestertius 25.5g Dupondius 12.5g As 10.5g Semis Quadrans TIMELINE of ROMAN IMPERIAL COINAGE B.C. 27 26 25 24 23 22 21 20 19 18 17 16 15 14 13 12 11 10 9 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 9 10 11 A.D.A.D. denominational relationships relationships based on Aureus Aureus 7.8g 1 Quinarius Aureus 3.89g 2 Denarius 3.79g 25 50 Sestertius 25.4g 100 Dupondius 12.4g 200 As 10.5g 400 Semis 4.59g 800 Quadrans 3.61g 1600 8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8 91011 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 19 Aug TIBERIUS TIBERIUS Aureus 7.75g Aureus Quinarius Aureus 3.87g Quinarius Aureus Denarius 3.76g 96-98% fine Denarius Sestertius 27g Sestertius Dupondius 14.5g Dupondius As 10.9g As Semis Quadrans 3.61g Quadrans 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36 37 38 39 40 41 42 43 44 45 46 47 48 49 TIBERIUS CALIGULA CLAUDIUS Aureus 7.75g 7.63g Quinarius Aureus 3.87g 3.85g Denarius 3.76g 96-98% fine 3.75g 98% fine Sestertius 27g 28.7g -

Agorapicbk-15.Pdf

Excavations of the Athenian Agora Picture Book No. 1s Prepared by Fred S. Kleiner Photographs by Eugene Vanderpool, Jr. Produced by The Meriden Gravure Company, Meriden, Connecticut Cover design: Coins of Gela, L. Farsuleius Mensor, and Probus Title page: Athena on a coin of Roman Athens Greek and Roman Coins in the Athenian Agora AMERICAN SCHOOL OF CLASSICAL STUDIES AT ATHENS PRINCETON, NEW JERSEY 1975 1. The Agora in the 5th century B.C. HAMMER - PUNCH ~ u= REVERSE DIE FLAN - - OBVERSE - DIE ANVIL - 2. Ancient method of minting coins. Designs were cut into two dies and hammered into a flan to produce a coin. THEATHENIAN AGORA has been more or less continuously inhabited from prehistoric times until the present day. During the American excava- tions over 75,000 coins have been found, dating from the 6th century B.c., when coins were first used in Attica, to the 20th century after Christ. These coins provide a record of the kind of money used in the Athenian market place throughout the ages. Much of this money is Athenian, but the far-flung commercial and political contacts of Athens brought all kinds of foreign currency into the area. Other Greek cities as well as the Romans, Byzantines, Franks, Venetians, and Turks have left their coins behind for the modern excavators to discover. Most of the coins found in the excavations were lost and never recovered-stamped into the earth floor of the Agora, or dropped in wells, drains, or cisterns. Consequently, almost all the Agora coins are small change bronze or copper pieces. -

Hadrian and the Greek East

HADRIAN AND THE GREEK EAST: IMPERIAL POLICY AND COMMUNICATION DISSERTATION Presented in Partial Fulfillment of the Requirements for the Degree Doctor of Philosophy in the Graduate School of the Ohio State University By Demetrios Kritsotakis, B.A, M.A. * * * * * The Ohio State University 2008 Dissertation Committee: Approved by Professor Fritz Graf, Adviser Professor Tom Hawkins ____________________________ Professor Anthony Kaldellis Adviser Greek and Latin Graduate Program Copyright by Demetrios Kritsotakis 2008 ABSTRACT The Roman Emperor Hadrian pursued a policy of unification of the vast Empire. After his accession, he abandoned the expansionist policy of his predecessor Trajan and focused on securing the frontiers of the empire and on maintaining its stability. Of the utmost importance was the further integration and participation in his program of the peoples of the Greek East, especially of the Greek mainland and Asia Minor. Hadrian now invited them to become active members of the empire. By his lengthy travels and benefactions to the people of the region and by the creation of the Panhellenion, Hadrian attempted to create a second center of the Empire. Rome, in the West, was the first center; now a second one, in the East, would draw together the Greek people on both sides of the Aegean Sea. Thus he could accelerate the unification of the empire by focusing on its two most important elements, Romans and Greeks. Hadrian channeled his intentions in a number of ways, including the use of specific iconographical types on the coinage of his reign and religious language and themes in his interactions with the Greeks. In both cases it becomes evident that the Greeks not only understood his messages, but they also reacted in a positive way. -

The Use of Propaganda on an Augustan Denarius

Pepperdine University Pepperdine Digital Commons Featured Research Undergraduate Student Research Fall 11-2013 The Use of Propaganda on an Augustan Denarius Jens Ibsen Pepperdine University, [email protected] Melissa Miller Pepperdine University Follow this and additional works at: https://digitalcommons.pepperdine.edu/sturesearch Part of the Biblical Studies Commons, History of Religion Commons, and the Other History of Art, Architecture, and Archaeology Commons Recommended Citation Ibsen, Jens and Miller, Melissa, "The Use of Propaganda on an Augustan Denarius" (2013). Pepperdine University, Featured Research. Paper 79. https://digitalcommons.pepperdine.edu/sturesearch/79 This Research Poster is brought to you for free and open access by the Undergraduate Student Research at Pepperdine Digital Commons. It has been accepted for inclusion in Featured Research by an authorized administrator of Pepperdine Digital Commons. For more information, please contact [email protected], [email protected], [email protected]. The Use of Propaganda on an Augustan Denarius Jens Ibsen & Melissa Miller ABSTRACT Our coin is a silver denarius minted in Lugdunum (now Lyon), most likely under the reign of Augustus, the first emperor of Rome. There are factors which point to a possibility of the coin being a restitution Above: A Comparable Trajan AR Denarius(c. 98 -117 CE) issue minted under either Trajan or Hadrian, such as its pristine Source; http://tjbuggey.ancients.info/ condition, which implies a lack of use, and the similarity of symbols employed on this denarius and denarii of Trajan’s era. The coin is a prime example of Augustus’ use of propaganda inserted into Roman daily life to sell the idea of empire to a Roman people who ardently defended a long-standing tradition of republican government. -

VESPASIAN. AD 68, Though Not a Particularly Constructive Year For

138 VESPASIAN. AD 68, though not a particularly constructive year for Nero, was to prove fertile ground for senators lion the make". Not that they were to have the time to build anything much other than to carve out a niche for themselves in the annals of history. It was not until the dust finally settled, leaving Vespasian as the last contender standing, that any major building projects were to be initiated under Imperial auspices. However, that does not mean that there is nothing in this period that is of interest to this study. Though Galba, Otho and Vitellius may have had little opportunity to indulge in any significant building activity, and probably given the length and nature of their reigns even less opportunity to consider the possibility of building for their future glory, they did however at the very least use the existing imperial buildings to their own ends, in their own ways continuing what were by now the deeply rooted traditions of the principate. Galba installed himself in what Suetonius terms the palatium (Suet. Galba. 18), which may not necessarily have been the Golden House of Nero, but was part at least of the by now agglomerated sprawl of Imperial residences in Rome that stretched from the summit of the Palatine hill across the valley where now stands the Colosseum to the slopes of the Oppian, and included the Golden House. Vitellius too is said to have used the palatium as his base in Rome (Suet. Vito 16), 139 and is shown by Suetonius to have actively allied himself with Nero's obviously still popular memory (Suet. -

The Romanization of Romania: a Look at the Influence of the Roman Military on Romanian History and Heritage Colleen Ann Lovely Union College - Schenectady, NY

Union College Union | Digital Works Honors Theses Student Work 6-2016 The Romanization of Romania: A Look at the Influence of the Roman Military on Romanian History and Heritage Colleen Ann Lovely Union College - Schenectady, NY Follow this and additional works at: https://digitalworks.union.edu/theses Part of the Ancient History, Greek and Roman through Late Antiquity Commons, European History Commons, and the Military History Commons Recommended Citation Lovely, Colleen Ann, "The Romanization of Romania: A Look at the Influence of the Roman Military on Romanian History and Heritage" (2016). Honors Theses. 178. https://digitalworks.union.edu/theses/178 This Open Access is brought to you for free and open access by the Student Work at Union | Digital Works. It has been accepted for inclusion in Honors Theses by an authorized administrator of Union | Digital Works. For more information, please contact [email protected]. The Romanization of Romania: A Look at the Influence of the Roman Military on Romanian History and Heritage By Colleen Ann Lovely ********* Submitted in partial fulfillment of the requirements for Honors in the Departments of Classics and Anthropology UNION COLLEGE March 2016 Abstract LOVELY, COLLEEN ANN The Romanization of Romania: A Look at the Influence of the Roman Military on Romanian History and Heritage. Departments of Classics and Anthropology, March 2016. ADVISORS: Professor Stacie Raucci, Professor Robert Samet This thesis looks at the Roman military and how it was the driving force which spread Roman culture. The Roman military stabilized regions, providing protection and security for regions to develop culturally and economically. Roman soldiers brought with them their native cultures, languages, and religions, which spread through their interactions and connections with local peoples and the communities in which they were stationed. -

The Roman Empire – Roman Coins Lesson 1

Year 4: The Roman Empire – Roman Coins Lesson 1 Duration 2 hours. Date: Planned by Katrina Gray for Two Temple Place, 2014 Main teaching Activities - Differentiation Plenary LO: To investigate who the Romans were and why they came Activities: Mixed Ability Groups. AFL: Who were the Romans? to Britain Cross curricular links: Geography, Numeracy, History Activity 1: AFL: Why did the Romans want to come to Britain? CT to introduce the topic of the Romans and elicit children’s prior Sort timeline flashcards into chronological order CT to refer back to the idea that one of the main reasons for knowledge: invasion was connected to wealth and money. Explain that Q Who were the Romans? After completion, discuss the events as a whole class to ensure over the next few lessons we shall be focusing on Roman Q What do you know about them already? that the children understand the vocabulary and events described money / coins. Q Where do they originate from? * Option to use CT to show children a map, children to locate Rome and Britain. http://www.schoolsliaison.org.uk/kids/preload.htm or RESOURCES Explain that the Romans invaded Britain. http://resources.woodlands-junior.kent.sch.uk/homework/romans.html Q What does the word ‘invade’ mean? for further information about the key dates and events involved in Websites: the Roman invasion. http://www.schoolsliaison.org.uk/kids/preload.htm To understand why they invaded Britain we must examine what http://www.sparklebox.co.uk/topic/past/roman-empire.html was happening in Britain before the invasion. -

The Burial of the Urban Poor in Italy in the Late Republic and Early Empire

Death, disposal and the destitute: The burial of the urban poor in Italy in the late Republic and early Empire Emma-Jayne Graham Thesis submitted for the degree of Doctor of Philosophy Department of Archaeology University of Sheffield December 2004 IMAGING SERVICES NORTH Boston Spa, Wetherby West Yorkshire, LS23 7BQ www.bl.uk The following have been excluded from this digital copy at the request of the university: Fig 12 on page 24 Fig 16 on page 61 Fig 24 on page 162 Fig 25 on page 163 Fig 26 on page 164 Fig 28 on page 168 Fig 30on page 170 Fig 31 on page 173 Abstract Recent studies of Roman funerary practices have demonstrated that these activities were a vital component of urban social and religious processes. These investigations have, however, largely privileged the importance of these activities to the upper levels of society. Attempts to examine the responses of the lower classes to death, and its consequent demands for disposal and commemoration, have focused on the activities of freedmen and slaves anxious to establish or maintain their social position. The free poor, living on the edge of subsistence, are often disregarded and believed to have been unceremoniously discarded within anonymous mass graves (puticuli) such as those discovered at Rome by Lanciani in the late nineteenth century. This thesis re-examines the archaeological and historical evidence for the funerary practices of the urban poor in Italy within their appropriate social, legal and religious context. The thesis attempts to demonstrate that the desire for commemoration and the need to provide legitimate burial were strong at all social levels and linked to several factors common to all social strata. -

Ancient Narrative Volume 5

The Ancient Novels and the New Testament: Possible Contacts1 ILARIA RAMELLI Catholic University of Milan Late in the reign of Nero, in Rome, Petronius, a member of the so-called ‘Neronian Circle’ and Nero’s arbiter in matters of taste or arbiter elegantia- rum, wrote his novel, Satyricon. It was during the time of, or soon after, the first Christian persecution,2 which was initiated by Nero himself against the members of a religion that a decision of the Senate in A.D. 35 had labelled as an ‘illicit superstition.’ According to Tertullian, Tiberius in the Senate proposed to recognize the Christians’ religion, but the senators refused, and proclaimed Christianity a superstitio illicita, so that every Christian could be put to death. But Tiberius, thanks to his tribunicia potestas, vetoed the Chris- tians’ condemnations, and there was no Roman persecution until the time of Nero.3 According to Tacitus (Ann. 15, 44), in A.D. 64, at the time of the ————— 1 This article is the revised version of the paper presented at the SBL Annual Meeting, Atlanta, Nov. 22–25 2003, Ancient Fiction and Early Christian and Jewish Narrative Group. 2 See e.g. Rowell 1958, 14–24, who identifies Petraites, mentioned in Sat. 52, 3 and 71, 6 with the famous gladiator of the Neronian age; Schnur 1959, and Moreno 1962/4, accord- ing to whom the economic background of the Satyricon points to the Neronian age; Rose 1962, who dates the novel between the end of A.D. 64 and the summer of 65; Id. 1971, esp. -

A New Perspective on the Early Roman Dictatorship, 501-300 B.C

A NEW PERSPECTIVE ON THE EARLY ROMAN DICTATORSHIP, 501-300 B.C. BY Jeffrey A. Easton Submitted to the graduate degree program in Classics and the Graduate Faculty of the University of Kansas in partial fulfillment of the requirements for the degree of Master’s of Arts. Anthony Corbeill Chairperson Committee Members Tara Welch Carolyn Nelson Date defended: April 26, 2010 The Thesis Committee for Jeffrey A. Easton certifies that this is the approved Version of the following thesis: A NEW PERSPECTIVE ON THE EARLY ROMAN DICTATORSHIP, 501-300 B.C. Committee: Anthony Corbeill Chairperson Tara Welch Carolyn Nelson Date approved: April 27, 2010 ii Page left intentionally blank. iii ABSTRACT According to sources writing during the late Republic, Roman dictators exercised supreme authority over all other magistrates in the Roman polity for the duration of their term. Modern scholars have followed this traditional paradigm. A close reading of narratives describing early dictatorships and an analysis of ancient epigraphic evidence, however, reveal inconsistencies in the traditional model. The purpose of this thesis is to introduce a new model of the early Roman dictatorship that is based upon a reexamination of the evidence for the nature of dictatorial imperium and the relationship between consuls and dictators in the period 501-300 BC. Originally, dictators functioned as ad hoc magistrates, were equipped with standard consular imperium, and, above all, were intended to supplement consuls. Furthermore, I demonstrate that Sulla’s dictatorship, a new and genuinely absolute form of the office introduced in the 80s BC, inspired subsequent late Republican perceptions of an autocratic dictatorship. -

Cryptocurrencies As an Alternative to Fiat Monetary Systems David A

View metadata, citation and similar papers at core.ac.uk brought to you by CORE provided by Digital Commons at Buffalo State State University of New York College at Buffalo - Buffalo State College Digital Commons at Buffalo State Applied Economics Theses Economics and Finance 5-2018 Cryptocurrencies as an Alternative to Fiat Monetary Systems David A. Georgeson State University of New York College at Buffalo - Buffalo State College, [email protected] Advisor Tae-Hee Jo, Ph.D., Associate Professor of Economics & Finance First Reader Tae-Hee Jo, Ph.D., Associate Professor of Economics & Finance Second Reader Victor Kasper Jr., Ph.D., Associate Professor of Economics & Finance Third Reader Ted P. Schmidt, Ph.D., Professor of Economics & Finance Department Chair Frederick G. Floss, Ph.D., Chair and Professor of Economics & Finance To learn more about the Economics and Finance Department and its educational programs, research, and resources, go to http://economics.buffalostate.edu. Recommended Citation Georgeson, David A., "Cryptocurrencies as an Alternative to Fiat Monetary Systems" (2018). Applied Economics Theses. 35. http://digitalcommons.buffalostate.edu/economics_theses/35 Follow this and additional works at: http://digitalcommons.buffalostate.edu/economics_theses Part of the Economic Theory Commons, Finance Commons, and the Other Economics Commons Cryptocurrencies as an Alternative to Fiat Monetary Systems By David A. Georgeson An Abstract of a Thesis In Applied Economics Submitted in Partial Fulfillment Of the Requirements For the Degree of Master of Arts May 2018 State University of New York Buffalo State Department of Economics and Finance ABSTRACT OF THESIS Cryptocurrencies as an Alternative to Fiat Monetary Systems The recent popularity of cryptocurrencies is largely associated with a particular application referred to as Bitcoin. -

Collector's Checklist for Roman Imperial Coinage

Liberty Coin Service Collector’s Checklist for Roman Imperial Coinage (49 BC - AD 518) The Twelve Caesars - The Julio-Claudians and the Flavians (49 BC - AD 96) Purchase Emperor Denomination Grade Date Price Julius Caesar (49-44 BC) Augustus (31 BC-AD 14) Tiberius (AD 14 - AD 37) Caligula (AD 37 - AD 41) Claudius (AD 41 - AD 54) Tiberius Nero (AD 54 - AD 68) Galba (AD 68 - AD 69) Otho (AD 69) Nero Vitellius (AD 69) Vespasian (AD 69 - AD 79) Otho Titus (AD 79 - AD 81) Domitian (AD 81 - AD 96) The Nerva-Antonine Dynasty (AD 96 - AD 192) Nerva (AD 96-AD 98) Trajan (AD 98-AD 117) Hadrian (AD 117 - AD 138) Antoninus Pius (AD 138 - AD 161) Marcus Aurelius (AD 161 - AD 180) Hadrian Lucius Verus (AD 161 - AD 169) Commodus (AD 177 - AD 192) Marcus Aurelius Years of Transition (AD 193 - AD 195) Pertinax (AD 193) Didius Julianus (AD 193) Pescennius Niger (AD 193) Clodius Albinus (AD 193- AD 195) The Severans (AD 193 - AD 235) Clodius Albinus Septimus Severus (AD 193 - AD 211) Caracalla (AD 198 - AD 217) Purchase Emperor Denomination Grade Date Price Geta (AD 209 - AD 212) Macrinus (AD 217 - AD 218) Diadumedian as Caesar (AD 217 - AD 218) Elagabalus (AD 218 - AD 222) Severus Alexander (AD 222 - AD 235) Severus The Military Emperors (AD 235 - AD 284) Alexander Maximinus (AD 235 - AD 238) Maximus Caesar (AD 235 - AD 238) Balbinus (AD 238) Maximinus Pupienus (AD 238) Gordian I (AD 238) Gordian II (AD 238) Gordian III (AD 238 - AD 244) Philip I (AD 244 - AD 249) Philip II (AD 247 - AD 249) Gordian III Trajan Decius (AD 249 - AD 251) Herennius Etruscus