Telemar Corporate Restructuring Oi Holdings

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Gsma Lança Iniciativas De Serviços Móveis Com O Governo E As Operadoras Brasileiras

GSMA LANÇA INICIATIVAS DE SERVIÇOS MÓVEIS COM O GOVERNO E AS OPERADORAS BRASILEIRAS 25 de fevereiro de 2014, Barcelona: A GSMA anunciou hoje várias iniciativas para melhorar o alcance e a escala dos serviços móveis no Brasil, em benefício de seus cidadãos e empresas. Paulo Bernardo, ministro das Comunicações do Brasil, e Anne Bouverot, diretora geral da GSMA, assinaram um acordo sob o qual a GSMA e o Governo brasileiro vão trabalhar juntos para acelerar a adoção da banda larga móvel e a entrega de novos serviços móveis no Brasil. Além disso, a GSMA e todas as operadoras de celular do Brasil – Algar Telecom, Claro, Nextel, Oi, Sercomtel, TIM Brasil e Vivo – anunciaram sua colaboração para proporcionar aos usuários experiências móveis mais convenientes e seguras, por meio de um conjunto de iniciativas que abordam questões como spam por SMS, roubo de aparelhos e proteção à criança. “Com aproximadamente 115 milhões de assinantes exclusivos e 277 milhões de conexões móveis, o Brasil é o maior mercado móvel na América Latina,” afirmou Anne Bouverot, diretora geral, GSMA. “Trabalhando em conjunto com o governo do Brasil e as operadoras móveis do país, continuaremos a expandir o alcance das redes e serviços móveis no Brasil, e a garantir que todos os clientes possam desfrutar dos benefícios de um ambiente mais confiável e protegido.” GSMA e Memorando de Entendimento com o Brasil A GSMA e o Ministério das Comunicações vão abordar uma série de áreas principais para acelerar a adoção de redes de banda larga móvel e serviços em todo o país. A GSMA vai oferecer sua experiência global e facilitar o diálogo em áreas como comunicações máquina a máquina (M2M), mHealth e mEducation, entre outras. -

Net Serviços De Comunicação SA

MARK A. WALKER DAVID L. SUGERMAN KRISTOFER W HESS CLEARY GOTTLIEB STEEN & HAMILTON LLP LESLIE B. SAMUELS HOWARD S. ZELBO JUAN G. GIRALDEZ EDWARD F. GREENE DAVID E. BRODSKY DUANE MCLAUGHLIN ALLAN G. SPERLING ARTHUR H. KOHN BREON S PEACE EVAN A. DAVIS RAYMOND B. CHECK MEREDITH E. KOTLER LAURENT ALPERT RICHARD J. COOPER CHANTAL E. KORDULA ONE LIBERTY PLAZA VICTOR I. LEWKOW JEFFREY S LEWIS BENET J. O'REILLY LESLIE N. SILVERMAN PAUL J. SHIM DAVID AMAN ROBERT L. TORTORIELLO STEVEN L. WILNER ADAM E. FLEISHER NEW YORK, NY 10006-1470 A. RICHARD SUSKO ERIKA W. NIJENHUIS SEAN A. O'NEAL LEE C BUCHHEIT LlNDSEE P. GRANFIELD GLENN P MCGRORY JAMES M. PEASLEE ANDRES DE LA CRUZ CHRISTOPHER P MOORE (212) 225-2000 ALAN L. BELLER DAVID C LOPEZ JOON H. KIM THOMAS J. MOLONEY CARMEN A. CORRALES MATTHEW P SALERNO WILLIAM F. GORIN JAMES L. BROMLEY MICHAEL J. ALBANO FACSIMILE (212) 225-3999 MICHAEL L. RYAN PAUL E. GLOTZER VICTOR L. HOU ROBERT P. DAVIS MICHAEL A. GERSTENZANG RESIDENT PARTNERS YARON Z REICH LEWIS J. LlMAN WWW.CLEARYGOTTLIEB.COM RICHARD 5 LlNCER LEV L DASSIN JAIME A. EL KOURY NEIL Q. WHORISKEY SANDRA M. ROCKS STEVEN G. HOROWITZ JORGE U JUANTORENA ELLEN M CREEDE ANDREA G. PODOLSKY MICHAEL D. WEINBERGER S. DOUGLAS BORISKY JAMES A. DUNCAN DAVID LEINWAND JUDITH KASSEL STEVEN M. LOEB JEFFREY A. ROSENTHAL DAVID E WEBB DANIEL 5 STERNBERG ETHAN A. KLlNGSBERG PENELOPE L CHRISTOPHOROU WASHINGTON. DC' PARIS' BRUSSELS DONALD A. STERN MICHAEL J. VOLKOVITSCH BOAZ S MORAG CRAIG B. BROD MICHAEL D. DAYAN MARY E ALCOCK LONDON· MOSCOW· FRANKFURT· COLOGNE SHELDON H. -

Prospecto-Preliminar-Gvt.Pdf

Prospecto Preliminar de Oferta Pública de Distribuição Primária de Ações Ordinárias de Emissão da GVT (Holding) S.A. ospecto Preliminar está sujeito a a sujeito está Preliminar ospecto GVT (HOLDING) S.A. Companhia Aberta de Capital Autorizado - CVM nº 02011-7 CNPJ nº 03.420.904/0001-64 - NIRE nº 41300071331 Rua Lourenço Pinto, nº 299, 4º andar, Curitiba, PR Código ISIN BRGVTTACNOR8 52.000.000 Ações Valor da Distribuição: R$[●] odo de distribuição. No contexto desta Oferta (conforme definido abaixo), estima-se que o Preço por Ação (conforme definido abaixo) estará situado entre R$11,00 e R$16,00, ressalvado, no entanto, que o Preço por Ação poderá, eventualmente, ser fixado fora dessa faixa indicativa. nifestou a seu respeito. O presente Pr A GVT (Holding) S.A. (“Companhia”) está realizando uma oferta pública primária de 52.000.000 ações ordinárias (“Oferta”), todas nominativas, escriturais, sem valor nominal (“Ações”), a ser realizada na República Federativa do Brasil (“Brasil”), sob a coordenação do Banco de Investimentos Credit Suisse (Brasil) S.A. (“Coordenador Líder”) e do Banco UBS Pactual S.A. (“UBS Pactual” e, em conjunto com o Coordenador Líder “Coordenadores”), com esforços de colocação no exterior a serem realizados por Credit Suisse Securities (USA) LLC, UBS Securities LLC, ABN AMRO Inc. e J.P. Morgan Securities, Inc. A Oferta e o aumento de capital com a emissão das Ações foram aprovados por deliberação do Conselho de Administração da Companhia, em reunião realizada em 12 de janeiro de 2007, conforme ata a ser publicada no Diário Oficial do Estado do Paraná e nos jornais “Gazeta do Povo” de Curitiba e “Valor Econômico”, edição nacional. -

Latin America 2019

The Mobile Economy Latin America 2019 Copyright © 2019 GSM Association The GSMA represents the interests of mobile operators GSMA Intelligence is the definitive source of global mobile worldwide, uniting more than 750 operators with almost operator data, analysis and forecasts, and publisher of 400 companies in the broader mobile ecosystem, including authoritative industry reports and research. Our data handset and device makers, software companies, equipment covers every operator group, network and MVNO in every providers and internet companies, as well as organisations country worldwide – from Afghanistan to Zimbabwe. It is in adjacent industry sectors. The GSMA also produces the the most accurate and complete set of industry metrics industry-leading MWC events held annually in Barcelona, available, comprising tens of millions of individual data Los Angeles and Shanghai, as well as the Mobile 360 Series points, updated daily. GSMA Intelligence is relied on by of regional conferences. leading operators, vendors, regulators, financial institutions and third-party industry players, to support strategic For more information, please visit the GSMA corporate decision-making and long-term investment planning. The website at www.gsma.com data is used as an industry reference point and is frequently cited by the media and by the industry itself. Our team Follow the GSMA on Twitter: @GSMA of analysts and experts produce regular thought-leading research reports across a range of industry topics. www.gsmaintelligence.com [email protected] -

Annual Report 2000

2000 Annual Report 2 PRESENTATION OF FINANCIAL INFORMATION Embratel Participações S.A., a corporation organized under the laws of the Federative Republic of Brazil, was formed upon the reorganization of Telecomunicações Brasileiras S.A. Telebrás, a corporation organized under the laws of Brazil that, together with its operating subsidiaries, was the primary provider of public telecommunications services in Brazil. We refer to Telebrás, together with its operating subsidiaries, as the Telebrás System. On May 22, 1998, the shareholders of Telebrás approved the restructuring of the Telebrás System to form, in addition to Telebrás, twelve new telecommunication companies, known as the New Holding Companies, by means of a procedure under Brazilian Corporate Law called cisão or split-up. The New Holding Companies were allocated substantially all of the assets and liabilities of Telebrás, including the shares held by Telebrás of the operating subsidiaries of the Telebrás System. The New Holding Companies, together with their respective subsidiaries, comprise three regional fixed-line operators, eight regional cellular operators and one domestic and international long-distance operator. The restructuring of the Telebrás System into the New Holding Companies and their respective subsidiaries is referred to in this annual report on Form 20-F as the Breakup of Telebrás. We are one of the New Holding Companies formed upon the Breakup of Telebrás. In the Breakup, all of the share capital of Empresa Brasileira de Telecomunicações, or Embratel, held by Telebrás, which represented 98.75% of the total share capital of Embratel, was transferred to us. We are the premier communications provider in Brazil offering a wide array of advanced communications services over our own state-of-the-art network. -

América Móvil's Second Quarter of 2012

Carlos García-Moreno Chief Financial Officer [email protected] Daniela Lecuona Torras Investor Relations Office [email protected] Highlights AMÉRICA MÓVIL’S SECOND QUARTER OF 2012 Relevant FINANCIAL AND OPERATING REPORT Events Mexico City, July 26, 2012 - América Móvil, S.A.B. de C.V. (“América Móvil”) [BMV: Subscribers AMX] [NYSE: AMX] [NASDAQ: AMOV] [LATIBEX: XAMXL], announced today its financial and operating results for the second quarter of 2012. América Móvil Consolidated 313M accesses• América Móvil added 5.9 million wireless subscribers—including 1.1 million Mexican from the acquisition of Simple Mobile—and 1.7 million fixed-line revenue gener- Operations ating units (RGUs) in the second quarter. At the end of June, we had 251.8 million wireless subscribers, 30.0 million landlines, 16.1 million broadband accesses and Mexico 15.1 million PayTV clients, for a total of 313.1 million accesses, 7.8% more than a Telcel year before. Telmex 1.4M net adds • We added 1.4 million new wireless subs in each of Mexico and Brazil, 577 thou- International in Mexico sand in Central America and the Caribbean and 406 thousand in Peru. Colombia Operations and Brazil and the Argentinean block obtained around 350 thousand new subs each. Mercosur Postpaid net • We made important inroads in the postpaid segment in a number of countries. Claro Argentina adds +34% in Net additions in Colombia and Mexico, 140 thousand and 272 thousand respec- Claro Paraguay Colombia Claro Uruguay tively, were 34% and 23.9% higher than those registered the year before. Claro Chile 2Q Revenues • Second quarter revenues were 191.7 billion pesos, up 9.3% year-on-year, with up 9.3% YoY Brazil wireless revenues rising 14.1% and fixed-line revenues 1.7%. -

Processo Nº 53500.010080/2019-55 Interessado: Algar Telecom S/A, ALGAR CELULAR S.A., Algar Multimídia S/A, Brasil Telecom Comunicação Multimídia Ltda

13/06/2019 2301 Página 1 de 1 Imprimir Boletim de Serviço Eletrônico em 13/06/2019 AGÊNCIA NACIONAL DE TELECOMUNICAÇÕES DESPACHO DECISÓRIO Nº 3/2019/RCTS/SRC Processo nº 53500.010080/2019-55 Interessado: Algar Telecom S/A, ALGAR CELULAR S.A., Algar Multimídia S/A, Brasil Telecom Comunicação Multimídia Ltda. (02.041.460/0001-93), OI S.A. - EM RECUPERAÇÃO JUDICIAL, OI MÓVEL S.A. - EM RECUPERAÇÃO JUDICIAL, Telemar Norte Leste S.A., Claro S.A., TELMEX DO BRASIL S/A, Embratel TVsat Telecomunicações S.A., Empresa Brasileira de Telecomunicações S.A. (Embratel), Nextel Telecomunicações Ltda., Sercomtel Participações S.A., Sercomtel S.A. - Telecomunicações, Telefônica Brasil S.A., TIM S.A., Sky Serviços de Banda Larga Ltda. A SUPERINTENDENTE DE RELAÇÕES COM CONSUMIDORES DA AGÊNCIA NACIONAL DE TELECOMUNICAÇÕES, no uso de suas atribuições legais e regulamentares, em especial a disposta no art. 160, I e IV, do Regimento Interno da ANATEL, aprovado pela Resolução nº 612, de 29 de abril de 2013, considerando: - as razões e justificativas constantes do Informe nº 49/2019/RCTS/SRC (4265244), e - a conveniência e oportunidade da proposta de implementação de mecanismo nacional e centralizado para o registro de intenções de bloqueio dos consumidores para que não recebam ligações de telemarketing, apresentada pelos Interessados em correspondências protocoladas nos autos dos processos nº 53500.012093/2019-69 (Grupo Oi), 53500.012094/2019-11 (Grupo Algar), 53500.012095/2019-58 (Grupo Claro), 53500.012098/2019-91 (Nextel), 53500.012100/2019-22 (Grupo Sercomtel), 53500.012102/2019-11 (Sky), 53500.012103/2019-66 (Grupo Tim), 53500.012104/2019-19 (Grupo Telefônica), DECIDE, com fundamento nos arts. -

Data De Referência Do Relatório: 05/06/2012 Demanda

Data de Referência do Relatório: 05/06/2012 Multas aplicadas nos últimos 3 anos (abr/2009 a abr/2012) em decorrência de descumprimento de plano geral de metas de qualidade identificando o Demanda: tipo de serviço (Serviço Móvel Pessoal, TV por assinatura, Serviço Telefônico Fixo Comutado), o motivo da multa e a operadora penalizada. QUANTIDADE 190 TOTAL 275.429.825,32 ANO DE ENTIDADE PROCESSO DESCRIÇÃO SERVIÇO VALOR APLICADO REFERÊNCIA SERCOMTEL S.A. TELECOMUNICACOES 535160049302004 2009 SERVICO TELEFONICO FIXO COMUTADO 519.399,24 SERCOMTEL S.A. TELECOMUNICACOES 535000238592008 2009 SERVICO TELEFONICO FIXO COMUTADO 878.744,51 SERCOMTEL S.A. TELECOMUNICACOES 535160075292004 2009 SERVICO TELEFONICO FIXO COMUTADO 489.531,50 SERCOMTEL S.A. TELECOMUNICACOES 535000139942005 2009 SERVICO TELEFONICO FIXO COMUTADO 1.240.985,77 SERCOMTEL S.A. TELECOMUNICACOES 535160016202003 2009 SERVICO TELEFONICO FIXO COMUTADO 476.625,50 AMERICEL S.A. 535000134932008 2009 SERVIÇO MOVEL PESSOAL 485.313,33 TELEMIG CELULAR S.A 535000134912008 2009 SERVIÇO MOVEL PESSOAL 17.451,69 INTELIG TELECOMUNICACOES LTDA 535000152642005 2009 SERVICO TELEFONICO FIXO COMUTADO 1.820.426,88 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 34.556,34 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 35.315,00 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 147.886,96 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 7.117,84 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 3.312,94 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 88.443,17 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 65.424,78 VIVO S.A. 535000134912008 2009 SERVIÇO MOVEL PESSOAL 51.447,53 VIVO S.A. -

OECD Telecommunication and Broadcasting Review of Brazil 2020 Brazil 2020 Brazil of Review Broadcasting and Telecommunication OECD

OECD Telecommunication and Broadcasting Review of azil 2020 Br OECD Telecommunication and Broadcasting Review of Brazil 2020 OECD Telecommunication and Broadcasting Review of Brazil 2020 This work is published under the responsibility of the Secretary-General of the OECD. The opinions expressed and arguments employed herein do not necessarily reflect the official views of OECD member countries. This document, as well as any data and map included herein, are without prejudice to the status of or sovereignty over any territory, to the delimitation of international frontiers and boundaries and to the name of any territory, city or area. The statistical data for Israel are supplied by and under the responsibility of the relevant Israeli authorities. The use of such data by the OECD is without prejudice to the status of the Golan Heights, East Jerusalem and Israeli settlements in the West Bank under the terms of international law. Please cite this publication as: OECD (2020), OECD Telecommunication and Broadcasting Review of Brazil 2020, OECD Publishing, Paris, https://doi.org/10.1787/30ab8568-en. ISBN 978-92-64-31744-4 (print) ISBN 978-92-64-93255-5 (pdf) Photo credits: Cover © Sarunyu_foto/Shutterstock; © ElenVD/Shutterstock. Corrigenda to publications may be found on line at: www.oecd.org/about/publishing/corrigenda.htm. © OECD 2020 The use of this work, whether digital or print, is governed by the Terms and Conditions to be found at http://www.oecd.org/termsandconditions. FOREWORD 3 Foreword The OECD Directorate for Science, Technology and Innovation (DSTI) carried out this study under the auspices of the Committee on Digital Economy Policy (CDEP) and the Working Party of Communication Infrastructures and Services Policy (WPCISP). -

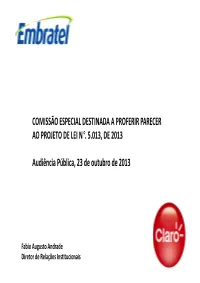

Claro/Embratel

COMISSÃO ESPECIAL DESTINADA A PROFERIR PARECER AO PROJETO DE LEI N °. 5.013, DE 2013 Audiência Pública, 23 de outubro de 2013 Fabio Augusto Andrade Diretor de Relações Institucionais O GRUPO AMÉRICA MÓVIL 6 milhões de acessos banda larga 30% do mercado NET 5,8 milhões Embratel 200 mil 29% dos minutos de Longa Distância Nacional e Internacional 11 milhões de acessos de telefonia fixa 23% do mercado local 66 milhões 9,1 milhões de acessos móveis TV por assinatura 25% do mercado 53% do mercado NET 5,7 milhões Embratel 3,4 milhões (cabo) (satélite) Infraestrutura de Rede Características da Rede Extensão de cabos : 52.889,33 km Extensão de fibras : 1.164.456,01 km Capacidade nominal: 14,2 Tbits/s 169 Switches Metro Ethernet – 212 Gbit/s Centros de roteamento em malha: 145 Anéis ópticos do backbone: 63 Rotas rádio longa distância : 16.000 km 7 satélites em órbita 3.634 cidades cobertas com telefonia móvel 476 cidades atendidas no Brasil com telefonia fixa local 91,3% População coberta com telefonia móvel 14.500 sites de telefonia móvel Novo cabo submarino Cidades cobertas com para transmissão de dados e longa distância telefonia móvel VISÃO DA REDE ÓPTICA & REDUNDÂNCIA INVESTIMENTOS PREVISTOS • Investimentos em Milhões de Reais • Metas estaduais detalhadas – disponível no site da Anatel ANATEL - Pesquisa de Qualidade Telefonia Fixa * APENAS 7,5% APENAS 3,6% DECLARAM-SE DECLARAM-SE INSATISFEITOS INSATISFEITOS Residencial Não Residencial 95,6 96,4 95,9 94,8 93,4 94,0 92,5 90,7 92,6 89,4 86,1 83,4 GVT SERCOMTEL EMBRATEL CTBC OI TELEFÔNICA EMBRATEL -

Prepared for 5G Americas

Region Country Operator LTE 5G Latin America 124 13 Anguilla Total 20 Anguilla Digicel Anguilla 10 Anguilla Flow (Anguilla) 10 Antigua and Barbuda Total 30 Antigua Public Utilities Authority (APUA, branded Antigua and Barbuda inet) 10 Antigua and Barbuda Digicel (Antigua and Barbuda) 10 Antigua and Barbuda Flow (Antigua and Barbuda) 10 Argentina Total 31 Argentina Claro Argentina 10 Argentina Telecom Personal (Argentina) 11 Argentina Telefonica Argentina (Movistar) 10 Aruba Total 20 Aruba Digicel (Aruba) 10 Aruba SETAR 10 Bahamas Total 20 Bahamas ALIV 10 Bahamas Bahamas Telecommunications Company (BTC) 10 Barbados Total 20 Barbados Digicel (Barbados) 10 Barbados Flow (Barbados) 10 Belize Total 20 Belize Belize Telemedia Limited (BTL, Digi) 10 Belize SpeedNet Communications (Smart) 10 Bermuda Total 20 Digicel Bermuda (incl. Bermuda Telephone Bermuda Company) 10 Bermuda One Communications 10 Bolivia Total 30 Bolivia Entel Movil 10 Bolivia NuevaTel PCS (Viva) 10 Bolivia Tigo Bolivia 10 Brazil Total 72 Brazil Algar Telecom 10 Brazil Claro Brasil (incl. Embratel & NET Servicos) 11 Brazil Claro‐nxt (formerly Nextel Telecomunicacoes) 10 Brazil EUTV (Surf Telecom) 10 Brazil Oi 10 Brazil Telefonica Brasil (Vivo) 11 Brazil TIM Brasil 10 Cayman Islands Total 20 Cayman Islands Digicel (Cayman Islands) 10 Cayman Islands Flow (Cayman Islands) 10 Chile Total 40 Chile Claro Chile 10 Chile Entel Chile 10 Chile Telefonica Moviles Chile (Movistar) 10 Chile WOM 10 Colombia Total 51 Colombia Avantel (Colombia) 10 Claro Colombia (previously Comcel, Telmex Colombia -

View Annual Report

ˆ200F4SiTSmCf0j!ZMŠ 200F4SiTSmCf0j!ZM NY8690AM021467 OI S.A. RR Donnelley ProFile11.9.13 NCR keebj0nm19-May-2016 17:10 EST 171431 FS 1 8* FORM 20-F NYC HTM ESS 0C Page 1 of 2 As filed with the Securities and Exchange Commission on May 20, 2016 UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 FORM 20-F REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934 OR ⌧ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015 OR TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 OR SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Commission file number: 001-15256 OI S.A. (Exact Name of Registrant as Specified in Its Charter) N/A The Federative Republic of Brazil (Translation of Registrant’s Name into English) (Jurisdiction of Incorporation or Organization) Rua Humberto de Campos, 425 Leblon, Rio de Janeiro, RJ, Brazil 22430-190 (Address of Principal Executive Offices) Flavio Nicolay Guimarães Investor Relations Officer Rua Humberto de Campos, 425 8º andar Leblon, Rio de Janeiro, RJ, Brazil 22430-190 Tel: +55 21 3131-2918 [email protected] ˆ200F4SiTSmCf0j!ZMŠ 200F4SiTSmCf0j!ZM NY8690AM021467 OI S.A. RR Donnelley ProFile11.9.13 NCR keebj0nm19-May-2016 17:10 EST 171431 FS 1 8* FORM 20-F NYC HTM ESS 0C Page 2 of 2 (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) Securities registered or to be registered