9. Arms Production

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Daily Shipping Newsletter 2003 – 203 Vlierodam Wire

DAILY SHIPPING NEWSLETTER 2003 – 203 Number 203 ****DAILY SHIPPING NEWSLETTER***Thursday 30-10-2003 THIS NEWSLETTER IS BROUGHT TO YOU BY : VLIERODAM WIRE ROPES Ltd. wire ropes, chains, hooks, shackles, webbing slings, lifting beams, crane blocks, turnbuckles etc. Binnenbaan 36 3161VB RHOON The Netherlands Telephone: (+31)105018000 (+31) 105015440 (a.o.h.) Fax : (+31)105013843 Internet & E-mail www.vlierodam.nl [email protected] Have a look for shipping movements around Hoek van Holland at : http://www.scheepvaarthoek.nl The FRIEDRICH RUSS moored in Lubeck Photo : Joop Keesmaat © PSi-Daily Shipping News Page 1 10/29/2003 DAILY SHIPPING NEWSLETTER 2003 – 203 EVENTS, INCIDENTS & OPERATIONS Queen to name new flagship next year Cunard has confirmed that the Queen will name its new flagship Queen Mary 2 , at Southampton on January 8, next year. The company's current flagship, Queen Elizabeth 2 , this port's longest and largest visitor, was launched by Her Majesty at the Clydebank yard of John Brown and Company on September 20, 1967. A much earlier, notable royal occasion on August 17, 1954, was when the Queen launched the Shaw Savill Line's Southern Cross at Harland and Wolff's Belfast shipyard. This vessel's long career has just ended. Billed as the largest, longest, widest and most expensive cruise ship ever built, QM2 is expected to be handed over by its St Nazaire builders, Chantiers de l'Atlantique, on December 22. It will undergo its second set of sea trials from November 7 to 11. The ship is expected to attract considerable interest when it arrives at Southampton later in December. -

Case No COMP/M.4640 - BAE SYSTEMS / VT / JV

EN Case No COMP/M.4640 - BAE SYSTEMS / VT / JV Only the English text is available and authentic. REGULATION (EC) No 139/2004 MERGER PROCEDURE Article 6(1)(b) NON-OPPOSITION Date: 17/10/2007 In electronic form on the EUR-Lex website under document number 32007M4640 Office for Official Publications of the European Communities L-2985 Luxembourg COMMISSION OF THE EUROPEAN COMMUNITIES Brussels, 17-X-2007 SG-Greffe(2007) D/206184 In the published version of this decision, some PUBLIC VERSION information has been omitted pursuant to Article 17(2) of Council Regulation (EC) No 139/2004 concerning non-disclosure of business secrets and other confidential information. The omissions are shown thus […]. Where possible the information omitted has been replaced by ranges of figures or a MERGER PROCEDURE general description. ARTICLE 6(1)(b) DECISION To the notifying parties: Dear Sir/Madam, Subject: Case No COMP/M.4640 - BAE Systems / VT / JV Notification of 12 September 2007 pursuant to Article 4 of Council Regulation No 139/20041 1. On 12 September 2007, the Commission received notification of a proposed concentration pursuant to Article 4 of Council Regulation (EC) No. 139/2004 ('the Merger Regulation') by which the undertakings BAE Systems plc ('BAES', United Kingdom) and VT Group plc ('VT', United Kingdom) acquire within the meaning of Article 3(1)(b) of the Council Regulation joint control of a newly created company ('ShipCo') constituting a joint venture. 2. After examination of the notification, the Commission has concluded that the notified operation falls within the scope of the Merger Regulation and does not raise serious doubts as to its compatibility with the common market and the functioning of the EEA Agreement. -

April 2011 Inside

April 2011 Inside • 25 years of SIPS • In the beginning • Scheme membership fast facts • Show me the money • Changing times • Thanks to the team at the top • Crossing the t’s and dotting the i’s 25 years of SIPS On 6 April 2011 SIPS reaches its 25th anniversary and to celebrate this occasion we have produced this commemorative brochure. Much has happened during the last 25 years and the following articles show how SIPS has evolved over the years. We hope you’ll enjoy looking back on the last quarter century of SIPS. In the beginning On 6 April 1986, SIPS was established as a centralised SIPS began with the following participating companies: pension scheme. Any employer who was working in shipbuilding, ship repair, or allied industries could • AMARC (Training, Education & Safety) Limited join SIPS. The Scheme was designed to replace the • British Shipbuilders British Shipbuilders Pension Scheme which had been • Energy & Marine Industries plc established in 1981 so that, following privatisation, • Falmouth Ship Repair Limited employers could continue to provide a cost effective • Hadrian Trustees Limited pension arrangement. On 6 April 1986, Hadrian Trustees Limited was appointed as the Independent Trustee of • Hall Russell Limited the Scheme. A Trustee Board of 15 Trustee Directors • Vickers Shipbuilding & Engineering Limited was set up, comprising 7 Directors appointed by the • Vosper Ship Repairers Limited employers, 7 Directors nominated by the Confederation • Vosper Thornycroft (UK) Limited of Shipbuilding & Engineering Unions (CSEU), together with an independent Managing Director. This meant that Joining SIPS meant that the individual employers could the Scheme could truly represent and act in the best participate in their own stand-alone section within the interests of all members and beneficiaries. -

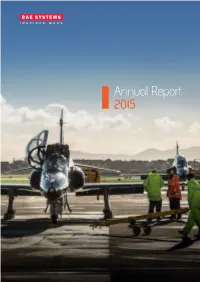

Annual Report 2015 Welcome to the BAE Systems Annual Report 2015

Annual Report 2015 Welcome to the BAE Systems Annual Report 2015 Further information can be found online by visiting baesystems.com Cautionary statement: All statements other than statements of historical fact included in this document, including, without limitation, those regarding the financial condition, results, operations and businesses of BAE Systems and its strategy, plans and objectives and the markets and economies in which it operates, are forward-looking statements. Such forward-looking statements, which reflect management’s assumptions made on the basis of information available to it at this time, involve known and unknown risks, uncertainties and other important factors which could cause the actual results, performance or achievements of BAE Systems or the markets and economies in which BAE Systems operates to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. BAE Systems plc and its directors accept no liability to third parties in respect of this report save as would arise under English law. Accordingly, any liability to a person who has demonstrated reliance on any untrue or misleading statement or omission shall be determined in accordance with Schedule 10A of the Financial Services and Markets Act 2000. It should be noted that Schedule 10A and Section 463 of the Companies Act 2006 contain limits on the Cover liability of the directors of BAE Systems plc so that their liability is solely to BAE Systems plc. Hawk aircraft at RAF Valley. Strategic report | BAE Systems at a glance (i) At BAE Systems, we provide some of the world’s most advanced technology defence, aerospace and security solutions. -

The Australian Naval Architect

THE AUSTRALIAN NAVAL ARCHITECT Volume 20 Number 2 May 2016 HMAS Parramatta ready for undocking in April after her Anti-Ship Missile Defence upgrade at BAE Systems, Henderson Shipyard, Western Australia. (RAN photograph) THE AUSTRALIAN NAVAL ARCHITECT Journal of The Royal Institution of Naval Architects (Australian Division) Volume 20 Number 2 May 2016 Cover Photo: CONTENTS The 72 m high-speed support vessel RNOV Al Mub- shir, built by Austal for the Royal Navy of Oman, 2 From the Division President during sea trials off Western Australia in March 3 Editorial (Photo courtesy Austal) 4 Letters to the Editor 6 News from the Sections The Australian Naval Architect is published four times per year. All correspondence and advertising copy should be 18 Coming Events sent to: 20 Classification Society News The Editor The Australian Naval Architect 20 General News c/o RINA PO Box No. 462 34 From the Crows Nest Jamison Centre, ACT 2614 36 The 21st Century Aircraft Carrier — John AUSTRALIA email: [email protected] Jeremy The deadline for the next edition of The Australian Naval Ar- 45 Education News chitect (Vol. 20 No. 3, August 2016) is Friday 29 July 2016. 50 Industry News Articles and reports published in The Australian Naval 53 The Profession Architect reflect the views of the individuals who prepared them and, unless indicated expressly in the text, do not neces- 54 The Future Naval Architect — Jesse Millar sarily represent the views of the Institution. The Institution, its officers and members make no representation or warranty, 56 Membership expressed or implied, as to the accuracy, completeness or 57 The Internet correctness of information in articles or reports and accept no responsibility for any loss, damage or other liability 58 Naval Architects on the Move arising from any use of this publication or the information which it contains. -

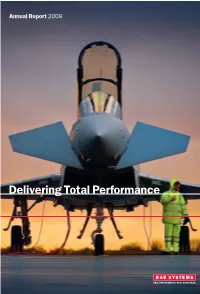

Delivering Total Performance

Preliminary Announcement and Presentation 2009 Delivering Total Pe rformance REAL PERFORMANCE. REAL ADVANTAGE. Cover image: Cautionary statement: All statements other than statements of historical fact included in this document, including, without limitation, those regarding the financial Typhoon condition, results, operations and businesses of BAE Systems and its strategy, plans and objectives and the markets and economies in which it operates, are forward- looking statements. Such forward-looking statements which reflect management’s assumptions made on the basis of information available to it at this time, involve known and unknown risks, uncertainties and other important factors which could cause the actual results, performance or achievements of BAE Systems or the markets and economies in which BAE Systems operates to be materially different from future results, performance or achievements expressed or implied by such forward-looking statements. Nothing in this document shall be regarded as a profit forecast. BAE Systems plc and its directors accept no liability to third parties in respect of this report save as would arise under English law. Accordingly, any liability to a person who has demonstrated reliance on any untrue or misleading statement or omission shall be determined in accordance with section 90A of the Financial Services and Markets Act 2000. It should be noted that section 90A and section 463 Companies Act 2006 contain limits on the liability of the directors of BAE Systems plc so that their liability is solely to BAE -

Babcock International Group

THIS DOCUMENT AND ANY ACCOMPANYING DOCUMENTS ARE IMPORTANT AND REQUIRE YOUR IMMEDIATE ATTENTION. If you are in any doubt as to the action you should take, you are recommended to seek immediately your own financial advice from your stockbroker, bank manager, solicitor, accountant, fund manager or other appropriate independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 (FSMA) if you are resident in the United Kingdom or, if not, from another appropriately authorised independent financial adviser. This document, which comprises: (i) a circular prepared in accordance with the Listing Rules of the Financial Conduct Authority (“FCA”) for the purposes of the General Meeting convened pursuant to the Notice of General Meeting set out at the end of this document; and (ii) a prospectus relating to the Ordinary Shares prepared in accordance with the Prospectus Rules of the FCA made under section 73A of FSMA, has been approved by the FCA in accordance with section 87A of FSMA and made available to the public in accordance with Rule 3.2 of the Prospectus Rules. Subject to the restrictions set out below, if you sell or transfer or have sold or otherwise transferred all of your Existing Ordinary Shares (other than ex-rights) held in certificated form before 8.00 a.m. on 17 April 2014 (the “ex-rights date”), please send this document together with the accompanying Form of Proxy and any Provisional Allotment Letter (duly renounced), if and when received, as soon as possible to the purchaser or transferee or to the stockbroker, bank or other agent through whom the sale or transfer was effected, for transmission to the purchaser or transferee. -

Shared Modular Build of Warships: How a Shared Build Can Support Future Shipbuilding

CHILDREN AND FAMILIES The RAND Corporation is a nonprofit institution that helps improve policy and EDUCATION AND THE ARTS decisionmaking through research and analysis. ENERGY AND ENVIRONMENT HEALTH AND HEALTH CARE This electronic document was made available from www.rand.org as a public service INFRASTRUCTURE AND of the RAND Corporation. TRANSPORTATION INTERNATIONAL AFFAIRS LAW AND BUSINESS Skip all front matter: Jump to Page 16 NATIONAL SECURITY POPULATION AND AGING PUBLIC SAFETY Support RAND SCIENCE AND TECHNOLOGY Purchase this document TERRORISM AND Browse Reports & Bookstore HOMELAND SECURITY Make a charitable contribution For More Information Visit RAND at www.rand.org Explore the RAND National Defense Research Institute View document details Limited Electronic Distribution Rights This document and trademark(s) contained herein are protected by law as indicated in a notice appearing later in this work. This electronic representation of RAND intellectual property is provided for non- commercial use only. Unauthorized posting of RAND electronic documents to a non-RAND website is prohibited. RAND electronic documents are protected under copyright law. Permission is required from RAND to reproduce, or reuse in another form, any of our research documents for commercial use. For information on reprint and linking permissions, please see RAND Permissions. This product is part of the RAND Corporation technical report series. Reports may include research findings on a specific topic that is limited in scope; present discussions of the methodology employed in research; provide literature reviews, survey instru- ments, modeling exercises, guidelines for practitioners and research professionals, and supporting documentation; or deliver preliminary findings. All RAND reports un- dergo rigorous peer review to ensure that they meet high standards for research quality and objectivity. -

Delivering Total Performance

BAE Systems plc Report Annual BAE Systems plc Annual Report 6 Carlton Gardens 2009 London SW1Y 5AD United Kingdom Telephone +44 (0)1252 373232 CONTENTS Registered in England and Wales No. 1470151 Website details www.baesystems.com 1. Overview 2. Strategy 2009 Results in brief, highlights and outlook 1 Strategic review 10 Chairman’s letter 2 Market review 16 Chief Executive’s review 4 Global initiatives 20 Strategy in action 22 3. Group performance 4. Segmental performance Key Performance Indicators (KPIs) 26 Operating group performance summary 54 Financial review 30 Electronics, Intelligence & Support 56 Corporate Responsibility review 38 Land & Armaments 60 Risk management 46 Programmes & Support 64 Principal risks 48 International 68 HQ & Other Businesses 72 5. Governance 6. Financial statements Delivering Total Performance Board of directors 76 Independent auditors’ report 119 Corporate governance 78 Consolidated financial statements 120 Remuneration report 90 Notes to the Group accounts 124 Other statutory and regulatory information, Company balance sheet 171 including statement of directors’ responsibilities 112 Notes to the Company accounts 172 Five-year summary 180 Shareholder information 182 Financial calendar 183 Glossary 184 Sections 1 to 5 make up the Directors’ Report in accordance with the Companies Act 2006. YOU CAN VIEW THIS ANNUAL REPORT AND OTHER INFORMATION FOR SHAREHOLDERS ONLINE AT: WWW.BAESYSTEMS.COM Cautionary statement: All statements other than statements of historical fact included in this document, including, without limitation, those regarding the financial condition, results, operations and businesses of BAE Systems and its strategy, plans and objectives and the markets and economies in which it operates, are forward-looking statements. -

National Approaches to Shipbuilding and Ship Procurement

National Approaches to Shipbuilding and Ship Procurement National Approaches to Shipbuilding and Ship Procurement Edited by Douglas L. Bland Defence Management Studies Program School of Policy Studies, Queen’s University 2010 Library and Archives Canada Cataloguing in Publication National approaches to shipbuilding and ship procurement / edited by Douglas L. Bland. (The Claxton papers, ISSN 1491-137X ; 11) Includes bibliographical references. ISBN 978-1-55339-294-1 1. Warships—Design and construction—Government policy. 2. Shipbuilding—Government policy. 3. Shipbuilding industry—Military aspects. I. Bland, Douglas L. II. Queen’s University (Kingston, Ont.). Defence Management Studies Program III. Series: Claxton papers ; 11 V750.N37 2010 359.6’212 C2010-903512-7 Copyright © Defence Management Studies Program, School of Policy Studies, Queen’s University, Kingston, 2010 The Claxton Papers The Queen’s University Defence Management Studies Program, established with the support of the Canadian Department of National De- fence (DND), is intended to engage the interest and support of scholars, members of the Canadian Forces, public servants, and participants in the defence industry in the examination and teaching of the management of national defence policy and the Canadian Forces. The program has been carefully designed to focus on the development of the theories, concepts, and skills required to manage and make decisions within the Canadian defence establishment. The Chair of the Defence Management Studies Program is located within the School of Policy Studies, and the program builds on Queen’s University’s strengths in the fields of public policy and administration, strategic studies, management, and law. Among other aspects, the program offers an integrated package of teaching, research, and conferences, all of which are designed to build expertise in the field and to contribute to wider debates within the defence community. -

Mr S Mccollam Phone: 0141 287 6021

PLANNING APPLICATIONS COMMITTEE Report by Executive Director of Development and Regeneration Services Contact: Mr S McCollam Phone: 0141 287 6021 APPLICATION TYPE Full Planning Permission RECOMMENDATION Grant Subject to Condition(s) S69 and S75 APPLICATION 08/01826/DC DATE VALID 14.08.2008 SITE ADDRESS Site At Govan Road/ Elder Street Glasgow PROPOSAL (a) Erection of flatted residential development with associated vehicular access, car parking and bin stores, (b) use of existing Class 4 office as Class 2 and Class 4 offices with ancillary heritage interpretive space, and (c) alterations to listed building comprising enlargement of window opening to form new rear entrance with disabled access, external repairs and new gate to main entrance on Govan Road/Elder Street: Potentially contrary to Policy Principle DEV3 Industry and Business of the City Plan. APPLICANT Clydeport PLC AGENT ADF Architecture And Design 16 Robertson Street Cumbrae House Glasgow 15 Carlton Court G2 8DS Glasgow G5 9JP WARD NO(S) 05, Govan COMMUNITY 02_073, Govan COUNCIL CONSERVATION LISTED A AREA Govan ADVERT TYPE Contrary to Development Plan PUBLISHED 3 October 2008 CITY PLAN Industry and Business REPRESENTATIONS/ CONSULTATIONS Three letters of objection have been received. These are from a local resident, a representative of BVT Surface Fleet, who currently operates from the shipyard forming part of the site, and the Architectural Heritage Society of Glasgow. Specific issues from the objections can be summarised as follows:- • The most north-easterly building within the defined red boundary is part of BVT Surface Fleet Limited tenure and is likely to be in use for at least the next 20 years. -

View Annual Report

Annual Report and Accounts 2019 The trusted partner Babcock International Group PLC Annual Report and Accounts 2019 The trusted partner. Babcock is a leading provider of critical, complex engineering services which support national defence, save lives and protect communities. We focus on three highly regulated markets – defence, aerial emergency services and civil nuclear – delivering vital services and managing complex assets in the UK and internationally. We are a trusted partner who understands the key roles that our technology, our expertise, our infrastructure and our assets play in ensuring our customers can deliver. We share risk with them in delivering innovation, and we share the benefits. Strategic report Group financial statements Financial and operational highlights 1 Group income statement 152 Chairman’s review 2 Group statement of Strategic framework 5 comprehensive income 153 Babcock at a glance 6 Group statement of changes in equity 153 Business model 8 Group balance sheet 154 Strategy 10 Group cash flow statement 155 Market review 12 Notes to the Group financial Defence 12 statements 156 Aerial emergency services 16 Civil nuclear 18 Company financial statements Chief Executive’s review 22 Company balance sheet 208 babcockinternational.com Strategic Partnering Programme 24 Company statement of Key Performance Indicators 26 changes in equity 209 Financial review 28 Notes to the Company Operational review: 40 financial statements 210 Marine 40 Land 43 Other information Aviation 46 Shareholder information 215 Cavendish Nuclear