Return on Investment for the Department of Transportation's

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Green Roads L UXURY RESIDENCES the ROADS MIAMI the ROADS

Green Roads L UXURY RESIDENCES THE ROADS MIAMI THE ROADS THE NEIGHBORHOOD The Roads is a residential neighborhood that has a strategic location and great accessibility to the city of Miami. Enjoy the luxury to be in the heart of it all with all the best surroundings and in a luscious community closely connected to nature. Vegetation is all along the streets and vehicle circulation is almost imperceptible thanks to its constant fluency. Calmness is always present in this peaceful environment just minutes away from Miami’s most vibrant neighborhoods and the exclusive beaches of Key Biscayne. THE PROJECT Green Roads is a set of unique Townhouses. Each of them is composed of three stories with exclusive facilities including: garage, elevator and rooftop terraces with outstanding views of Brickell and the Miami Skyline. It’s unique design defines Green Roads as the architectural vanguard of The Roads. Green Roads is your place to make a house into a home. LOOKING FOR ANOTHER VIEW LOCATION & LIFESTYLE Walking distance to Very close to BRICKELL KEY BISCAYNE BALANCE, PEACE Green Roads offers the great benefit of being part of a 2 Minutes from Brickell residential neighborhood but also the advantage of being 5 Minutes from Key Biscayne Beaches near the vertiginous center of Miami. 5 Minutes from Coconut Grove 7 Minutes from the Design District There is a convenient connection with motorways US1 and 10 Minutes from South Beach I-95, easy access to the airport and a great closeness to 15 Minutes from the Miami the main attractions of the city – which are an excellent International Airport reflection of Miami’s lifestyle. -

2017 Waivers

CITY OF MIAMI OFFICE OF ZONING IN COMPLIANCE WITH THE MIAMI NEIGHBORHOOD COMPREHENSIVE PLAN AND MIAMI 21, NOTICE OF APPLICATION AND FINAL DECISION FOR WAIVERS IS ISSUED FOR THE FOLLOWING ITEMS: THE FINAL DECISION OF THE ZONING ADMINISTRATOR MAY BE APPEALED TO THE PLANNING, ZONING AND APPEALS BOARD BY ANY AGGRIEVED PARTY, WITHIN FIFTEEN (15) DAYS OF THE DATE OF THE POSTING OF THE DECISION TO THIS WEBSITE BY FILING A WRITTEN APPEAL AND APPROPRIATE FEE WITH THE OFFICE OF HEARING BOARDS, LOCATED AT 444 SW 2ND AVENUE 3rd Floor, MIAMI, FL 33130. TEL. (305) 416-2030 Final Final Decision Waiver Transect Date of First App. Referral Plans Decision Posting Name Address NET Area Use cannot be Status Number Zone Notice Received Date Reviewer (Issuance) Date issued prior Date to: T3-R/NCD- 2016-0167 3012 Kirk Street Coconut Grove DEMO 11/14/2016 10/12/2016 11/4/2016 FG 12/14/2016 1/16/2017 1/18/2017 Kunl Demo 3 Approved with conditions Downtown/ 2016-0173 Zom Living 221-237 SW 12 St T6-24A-O Mixed Use 10/17/2016 7/1/2016 8/19/2016 JK 11/16/2016 1/16/2017 1/18/2017 Brickell Approved with conditions T3-R/NCD- 2016-0176 3553 Charles Ave 3553 Charles Ave Coconut Grove Demo 12/8/2016 11/21/2016 12/1/2013 FG 1/8/2017 1/16/2017 1/18/2017 2 Approved with conditions SW Coconut SW Coconut 2015-0159 Grove Haus Bldng. 3265 Bird Avenue T4-L/NCD-3 11/4/2015 10/8/2015 10/29/2015 FG 12/4/2015 1/24/2017 1/25/2017 Grove Grove Approved with conditions T3-R/NCD- 2017-0001 4160 RAYNOLDS AV DEMO 4160 RAYNOLDS AV Coconut Grove DEMO 12/8/2016 5/24/2016 CT 1/9/2017 1/24/2017 -

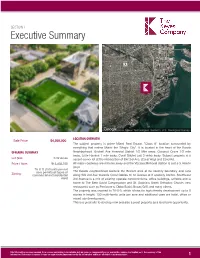

Executive Summary

SECTION | Executive Summary LOCATION OVERVIEW Sale Price $4,950,000 The subject property is prime Miami Real Estate, "Class A" location surrounded by everything that makes Miami the "Magic City". It is located in the heart of the Roads OFFERING SUMMARY Neighborhood. Brickell Ave Financial District 1/2 Mile away, Coconut Grove 1/2 mile away, Little Havana 1 mile away, Coral Gables just 3 miles away. Subject property is a Lot Size: 0.32 Acres vacant corner lot at the intersection of SW 3rd Ave, (Coral Way) and 22nd Rd. Price / Acre: $15,468,750 All major roadways are minutes away and the Vizcaya Metrorail station is just a 5 minute stroll. T6-8-O (150 units per net acre permits all types of The Roads neighborhood borders the Brickell area at its easterly boundary and runs Zoning: commercial and residential along SW 3rd Ave towards Coral Gables to 12 Avenue at it westerly border. Southwest uses) 3rd Avenue is a mix of existing upscale condominiums, office buildings, schools and is home to The Beth David Congregation and St. Sophia's Greek Orthodox Church, new restaurants such as Perricone's, Obba Sushi, Bocas Grill, and many others. The property was rezoned to T6-8-0, which allows for high density development up to 8 stories in height, 150 multi-family units per acre and additional uses are hotel, office or mixed use development. This is a great site to develop now and also a great property as a land bank opportunity. This information has been secured from sources we believe to be reliable, but we make no representations nor warranties, express nor implied as to the accuracy of the information. -

Stuck in Traffic:Or F Greater Miami to Become a Leading Startup Hub, Better Mobility Is a Must Richard Florida

Florida International University FIU Digital Commons Miami Urban Future Initiative College of Communication, Architecture + The Arts 2019 Stuck in Traffic:or F Greater Miami to Become a Leading Startup Hub, Better Mobility Is a Must Richard Florida Steven Pedigo Miami Urban Future Initiative, Florida International University Follow this and additional works at: https://digitalcommons.fiu.edu/mufi-reports Part of the Urban, Community and Regional Planning Commons This work is brought to you for free and open access by the College of Communication, Architecture + The Arts at FIU Digital Commons. It has been accepted for inclusion in Miami Urban Future Initiative by an authorized administrator of FIU Digital Commons. For more information, please contact [email protected]. REPORT STUCK IN TRAFFIC: For Greater Miami to Become a Leading Startup Hub, Better Mobility Is a Must Richard Florida and Steven Pedigo REPORT THE AUTHORS STUCK IN TRAFFIC: RICHARD FLORIDA For Greater Miami to Become a Leading Richard Florida is one of the world’s leading Startup Hub, Better Mobility Is a Must urbanists. He is founder of the Miami Future Initiative and a distinguished Fellow at Florida International University. He is a University Professor at University MIAMI URBAN FUTURE INITIATIVE of Toronto’s School of Cities and Rotman School of The Miami Urban Future Initiative is a joint effort between the Creative Class Group Management and a Distinguished Fellow at NYU. and Florida International University’s College of Communication, Architecture + @Richard_Florida He is author the award-winning book, The Rise of The Arts (CARTA) to develop new research and insights for building a stronger, more the Creative Class and most recently, The New Urban innovative, and more inclusive economy in Greater Miami. -

Transit Hub SUNNY

HALLANDALE BEACH BLVD E MIRAMAR PKWY E E 95 BROWARD COUNTY K I NW 215 ST 99 P MIAMI-DADE COUNTY NW 211 ST N R 95 U TO FORT TO LAUDERDALE NE 207 ST T D NE 205 ST GOLDEN S E NW 206 ST 297 ’ R BEACH NW 2 AVE NE 203 ST NE 2 AVE Y The Bus Terminal A RED ROAD 27 27 IR AVE NE 12 D A at Aventura Mall NW 202 ST I IVES D R FLAMINGO RD FLAMINGO NW 199 ST O 99 3,9 WI LLIAM LEHMAN CSWY 199 ST99 L M IAMI GARDENS F 183 17 210 95 E,S NE 192 ST 99,183 NW 52 AVE NW 52 NW 191 ST NW 47 AVE NW 47 NW 191 ST 95 99 MIAM 75 NE 186 ST NW 186 ST I GA 32 93, 95, 120 RDENS DR AV E AV E NW 183 ST MIAMI GARDENS DR 183 NORTH E 73 42 2,3 16 32 MIAMI-DADE COUNTY 54 95 MIAMI 267 286 CAROL 77 9,10 19 AVENTURA 120 286 NW NW 75 BEACH CITY NW 175 ST 17 E,H 22 93 E S 75 246 NE 19 AVE 286 NW 167 ST 75 D 3 BLV Golden Glades ES NW 167 ST E 246 2 210 SUNNY ISL E 75 826 PALMETTO EXPY 22 NE 163 ST 54 Golden Glades Northeast H 32 Terminal E Transit Hub SUNNY TRANSIT SYSTEM e NW 87 AVE 75 22 MIAMI v 217 155 19 75 ISLES 29 A LUDLAM RD LUDLAM LAKES 77 7 OPA-LOCKA BEACH 3 NW 156 ST 155 MIAMI LAKES DR NW 151 ST NE 151 ST 3 H H W 246 NE 6 AVE 27 267 N 277 16 135 120 OPA-LOCKA 17 77 9 10 EXECUTIVE AIRPORT 42 95 75 METROBUS ROUTES OKEECHOBEE ROAD 277 NW 138 ST NW 135 ST Opa-Locka 217 W DIXIE HWY 135 135 135 G Limited-Stop Service R 217 NORTH A 297 73 29 37 T 95 MIAMI BAY HARBOR IG WEST BRO A AVE COLLINS N 27 D CSW ISLANDS W 28 AVE G Y Express Service Y VIEW 96 ST W 68 ST EX 1 29 PY NW 12 AVE NW 119 ST E 65 ST HIALEAH 19 16 G BAL HARBOUR 54 19 D East–West Local-Stop Service GARDENS G MIAMI -

Road Closure Advisory

ROAD CLOSURE ADVISORY SUNDAY, JANUARY 28th, 2018 6:00 A.M. – 2:00 P.M. MIAMI, FL – The following road closures will take place around the city on Sunday, January 28th, 2018 for the 16th Annual Miami Marathon and Half Marathon produced by Life Time – Athletic Events. The race will begin at 6:00 a.m. at the American Airlines Arena downtown and will proceed to Miami Beach via the MacArthur Causeway, up Ocean Drive, over the Venetian Causeway and as far south as Coconut Grove. All participants are completely off the of the course by 2:00 PM for the reopening of the roads, however, most of the roadways will be clear before then due to the rolling reopening procedures. Roads will be closed and managed by the City of Miami, Miami Beach and Miami Dade Police Departments. It is recommended that the Julia Tuttle Causeway be utilized for access to and from Miami Beach until 10:00 a.m. Street Direction From To Rolling Anticipated Street Street Closure Reopening Biscayne Blvd (Sat 1/28) Northbound SE 3rd Street NE 2nd Street 8:00 AM 4:00 PM Biscayne Blvd (Sun 1/29) Northbound SE 3rd Street NE 11th Terrace 12:00 AM 9:00 AM SE 1st Street Eastbound N Miami Ave Biscayne Blvd 2:30 AM 2:30 PM MacArthur Causeway Eastbound Biscayne Blvd Alton Rd/5th Street 5:00 AM 8:10 AM Alton Rd/5th/South Pointe Drive NB/SB 5th Street South Point Drive 5:00 AM 8:25 AM Ocean Drive NB/SB South Point Drive 15th Street 5:55 AM 8:25 AM Washington Ave NB/SB 7th Street 17th Street 6:00 AM 8:50 AM Pennsylvania Ave NB/SB 7th Street 8th Street 6:10 AM 9:00 AM 17th St Westbound Washington -

Cultural and Spatial Perceptions of Miami‟S Little Havana

CULTURAL AND SPATIAL PERCEPTIONS OF MIAMI‟S LITTLE HAVANA by Hilton Cordoba A Thesis Submitted to the Faculty of The Charles E. Schmidt College of Science in Partial Fulfillment of the Requirements for the Degree of Master of Arts Florida Atlantic University Boca Raton, Florida August 2011 Copyright by Hilton Cordoba 2011 ii CULTURAL AND SPATIAL PERCEPTIONS OF MIAMI'S LITTLE HAVANA by Hilton Cordoba This thesis was prepared under the direction ofthe candidate's thesis advisor, Dr. Russell Ivy, Department ofGeosciences, and has been approved by the members ofhis supervisory committee. It was submitted to the faculty ofthe Charles E. Schmidt College ofScience and was accepted in partial fulfillment ofthe requirements for the degree of Master ofArts. SUPERVISORY COMMITTEE: ~s~~.Q~ a;;;::;.~. - Maria Fadiman, Pli.D. a~~ Es~ f2~_--- Charles Roberts, Ph.D. _ Chair, Department ofGeosciences ~ 8. ~- ..f., r;..r...-ry aary:pelT)(kll:Ii.- Dean, The Charles E. Schmidt College ofScience B~7Rlso?p~.D~~~ Date . Dean, Graduate College iii ACKNOWLEDGEMENTS I wish to express my gratitude to Dr. Russell Ivy for his support, encouragement, and guidance throughout my first two years of graduate work at Florida Atlantic University. I am grateful for the time and interest he invested in me in the midst of all his activities as the chair of the Geosciences Department. I am also thankful for having the opportunity to work with the other members of my advisory committee: Dr. Maria Fadiman and Dr. Charles Roberts. Thank you Dr. Fadiman for your input in making the survey as friendly and as easy to read as possible, and for showing me the importance of qualitative data. -

Wynwood Hotel OK'd to Check In

WEEK OF THURSDAY, JANUARY 29, 2015 A Singular Voice in an Evolving City WWW.MIAMITODAYNEWS.COM $4.00 HEALTH UPDATE Jackson team reviews spending GE’s CT scanner at forefront plan above $100 million, pg. 13 in broad clinical range, pg. 15 FP&L SELLS RIVER LAND: Ytech Interna- tional, a Miami-based development and real estate investment firm, and Carlos Mattos, an Wynwood investor/developer, paid Florida Power & Light THE ACHIEVER $21 million for 2.24 acres just north of the Miami River and east of Southeast Second Avenue. hotel OK’d Asked where FP&L will re-locate its equipment on the site and how long it will take, a spokes- man could not provide information Tuesday to check in evening. The land, in Miami’s central business district, is almost a full city block with entitlements to build 2.15 million BY JOHN CHARLES ROBBINS square feet, according to Colliers International spokespeople. Brokers Larry Stockton of Colliers International and Michael Fay, Jay Ziv and New York developer Sonny Xavier Cossard of Avison Young teamed up on the transaction. Mr. Bazbaz wants to build a hotel in Stockton, who was not available Tuesday evening, said in a written Wynwood. Miami’s Urban De- release the property was essentially an off-market transaction. Colliers spokespeople report Ytech International, led by Yamal Yidios Char, has velopment Review Board last redeveloped more than 3,000 multi-family units in South Florida and week recommended approval of currently owns a $300 million real estate portfolio in Florida and Texas; his mixed-use project at 2110 N and Mr. -

The King's and Pablo Roads Challenges the Combined Research Skills of a Historian and Geographer

THE KING’S AND PABLO ROADS FLORIDA’S FIRST HIGHWAYS A NARRATIVE HISTORY OF THEIR CONSTRUCTION AND ROUTES IN ST. JOHNS COUNTY Historic Property Associates, Inc. St. Augustine, Florida July 2009 THE KING’S AND PABLO ROADS FLORIDA’S FIRST HIGHWAYS A NARRATIVE HISTORY OF THEIR CONSTRUCTION AND ROUTES IN ST. JOHNS COUNTY Prepared for ST. JOHNS COUNTY GROWTH MANAGEMENT SERVICES By Paul L. Weaver, MA Historic Property Associates, Inc. P.O. Box 1002 St. Augustine, Florida 32085-1002 Phone (904) 824-5178 Fax (904) 824-4880 July, 2009 TABLE OF CONTENTS Illustrations...............….........................................................................................3 Introduction ..........................................................................................................5 Methodology and Sources.....................................................................................6 Chapter 1: History and Development of King’s Road.........................................14 Chapter 2: History and Development of Pablo Road..........................................81 Conclusions and Recommendations…………………………………………….146 Bibliography.........................................................................................................148 Appendices/Attachments Tables of Course of Roads through Government Land Office Plats and Field Notes Course of Roads on Topographic Maps Course of Roads on 1950 St. Johns County Township Plats Course of Roads on Topographic Maps and Aerials in Power Point Preservation 2 ILLUSTRATIONS Illustration 1 -

Connecting the Blocks

CONTENTS EXECUTIVE SUMMARY 4 INTRODUCTION 6 UNDERSTANDING THE CONTEXT 7 Review of Existing Plans and Studies 7 The Study Area 10 Multimodal Districts 10 Who Lives There? 12 How Do They Live? 18 Where Are They Going? 26 How Are They Getting There? 30 What Does the Future Look Like? 45 Summary 51 NEEDS ASSESSMENT METHODOLOGY 53 COMPLETE STREETS STANDARDS 53 Connectivity and Quality 53 Streets Typology 54 Complete Streets Network 63 Level of Service Standards 63 IDENTIFICATION OF MULTI-MODAL NEEDS 69 PRIORITIZATION OF MULTI-MODAL NEEDS 69 COST ESTIMATES 73 APPENDIX A: MAPS 74 APPENDIX B: PROJECT NEEDS LIST WITH COST ESTIMATES 79 APPENDIX C: PRIORITIZATION CRITERIA 125 TABLES FIGURES Table 1. People Per Acre 12 Figure 1. Multimodal Connectivity Districts 11 Table 2. Broward County Transit Routes 32 Figure 2. People Per Acre 13 Table 3. Sun Trolley Routes 33 Figure 3. Population that is 18 and Under Per Acre 15 Table 4. Limited-Access Highways in Fort Lauderdale 40 Figure 4. Population that is 65 and Older Per Acre 17 Table 5. Major East-West Corridors (Non-Interstates) 40 Figure 5. Downtown Riverfront Development 18 Table 6. Major North-South Corridors Figure 6. Existing Land Use 19 (Non-Interstates) 40 Figure 7. Single-Family Home 20 Table 7. Pedestrian Connectivity 42 Figure 8. Multi-Family Residences 20 Table 8. Bicycle Connectivity (Arterials and Collectors) 43 Figure 9. Residential Land Use 21 Table 9. Transit Connectivity 44 Figure 10. Land Use Related to Employment 23 Table 10. 2035 LRTP Cost Feasible Figure 11. Income and Car Ownership 25 Roadway Projects within Fort Lauderdale 47 Figure 12. -

Metrorail Map (Pdf)

METRORAIL NOVEMBER 2018 to West Palm Beach to West West to Palm Beach METRORAIL 27 TRANSFER PALMETTO OKEECHOBEE NORTHSIDE NW 79 ST 79 ST CAUSEWAY MEDLEY DR. MARTIN WESTGATE LUTHER KING, JR. 826 HIALEAH TRI-RAIL BROWNSVILLE HIALEAH MARKET EARLINGTON HEIGHTS MIAMI TRANSFER BETWEEN ORANGE AND GREEN LINES SPRINGS BLVD BISCAYNE JULIA TUTTLE CAUSEWAY RENTAL CAR MIA TERMINAL 112 195 CENTER ALLAPATTAH MIAMI AIRPORT WYNWOOD NW 27 AVE NW 27 SANTA MIAMI CLARA 95 1 INTERNATIONAL CIVIC AIRPORT CENTER CULMER MACARTHUR CAUSEWAYMIAMI 836 395 BEACH MIAMICENTRAL HISTORIC OVERTOWN / LYRIC THEATRE DOWN- TOWN PORT GOVERNMENT CENTER MIAMI LITTLE HAVANA SW 8 ST / TAMIAMI TRAIL 41 BRICKELL THE ROADS CORAL WAY VIZCAYA SW 27 AVE SW 27 S DIXIE HWY COCONUT GROVE CORAL GABLES DOUGLAS ROAD UNIVERSITY SOUTH MIAMI 826 SW 88 ST / DADELAND NORTH KENDALL DR to DADELAND SOUTH City TRANSFER TO SOUTH DADE TRANSITWAY Homestead& Florida NORTH 1 PINECREST METRORAIL METRORAIL CONNECTING SERVICES CONNECTING SERVICES Orange Line / StationOrange Line / Station Metromover Metromover Green Line / Station Tri-Rail (tri-rail.com) Green Line / Station Tri-Rail (tri-rail.com) Station Serving Both Lines Brightline (gobrightline.com) Brightline (gobrightline.com) Station Serving Both Lines MIA Mover (miami-airport.com) Recommended Transfer Station MIA Mover (miami-airport.com) Recommended Transfer Station South Dade Transitway Station Connects with Metromover South Dade Transitway Station ConnectsStation with Tri-Rail Connects with Metromover Station ConnectsStation with Airport Connects with Tri-Rail Station Connects with Brightline Station Connects with Airport Station Connects with Brightline www.miamidade.gov/transit INFORMATION : INFORMACION : ENFOMASYON 311 OR 305.468.5900 TTY/FLA RELAY: 711 @GOMIAMIDADE MDT TRACKER • EASY PAY MIAMI. -

Final Alternatives Analysis Report

South Florida East Coast Corridor FINAL ALTERNATIVES ANALYSIS REPORT October 2011 Federal Aid No. FTAX004 FTA Grant No. FL-90-X372-07 FM No. 417031-1-22-01 Miami-Dade, Broward, and Palm Beach Counties, Florida Contract: C-8F66 2 SFECCTA Alternatives Analysis Report SOUTH FLORIDA EAST COAST CORRIDOR TRANSIT ANALYSIS Lead Agencies: Florida Department of Transportation, Federal Transit Administration Title of the Proposed Action: South Florida East Coast Corridor Transit Analysis ABSTRACT: This report documents the development and analysis of alternatives for implementing reliable, high quality transit in the 85-mile Florida East Coast corridor located in southeast Florida. The purpose of the project is to increase transit options for travel in southeast Florida, support the Eastward Ho! Initiative of the counties in the region, encourage redevelopment and economic growth in the coastal cities, and supplement the existing highway network. These goals were developed in cooperation with the counties, cities, metropolitan planning organizations, regional planning organizations, civic and business organizations, and the general public. The study has proceeded in two phases. The first phase led to the development of modally generic alternatives that were refined into four, specific modal alternatives in Phase 2, which is the subject of this report. These four alternatives: TSM, BRT, Integrated Rail “DMU”, and Integrated Rail “Push- Pull,” were defined and compared against both a No Build alternative and against each other. Each of these alternatives incorporates new transit service along the Florida East Coast Railway (FEC) cor- ridor with existing transit service operated by each of the three counties in the region (Palm Beach, Broward, and Miami-Dade) and Tri-Rail.