What It Is About

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Cheque Collection Policy

Cheque Collection Policy Date: November 14, 2017. Version: 1 0 | P a g e Table of Content 1. Policy Content .......................................................................................................................................... 2 2. Document Control ................................................................................................................................... 6 3. Revisions to the Policy ............................................................................................................................. 7 4. Persons & Departments involved ............................................................................................................ 7 5. Glossary ................................................................................................................................................... 7 6. Appendix .................................................................................................................................................. 8 © 2017 Fincare Small Finance Bank, Cheque Collection Policy 1 | P a g e All Rights Reserved 1. Policy Content All personnel carrying out their duties with regard to the Cheque Collection function should ensure that they comply with the requirements of this policy. All Appendix referenced in this section - content mentioned to be moved into the body of the policy aside from Appendix I For Frequently Asked Questions (FAQs) regarding this policy please refer to Appendix II With reference to the RBI regulation guidelines detailed in -

Bank Tariff Guide for HSBC Retail Banking and Wealth Management Customers

Bank tariff guide for HSBC Retail Banking and Wealth Management Customers Tips to help switch you on to best value banking. Effective 1 November 2018 Issued by The Hongkong and Shanghai Banking Corporation Limited Tariffs/1NOV2018 Bank Bank tariff guide for HSBC Retail Banking and Wealth Management Customers Welcome to HSBC’s easy guide to services and fees. You’ll find helpful sections with tips on how to save both time and money. With more options and more efficiency, we’re providing you better banking value and even more reasons to bank with HSBC. 1 This guide is intended to give you a clear picture of the fees we charge for our most commonly To save money, time and effort, used services. Please note that the sections on specific account types should be read in conjunction with the section entitled ‘General services – all accounts’. please log on to HSBC Internet Banking at The charges in this guide were correct at the time of release but remain subject to change. For your own interest, please seek confirmation of the prevailing charge related to the service www.hsbc.com.hk or download HSBC HK Mobile you need. These charges are applicable only to accounts maintained in the Hong Kong SAR with The Hongkong and Shanghai Banking Corporation Limited, which reserves the right to Banking app at App Store/Google Play™ for introduce charges not included in this guide. For charges which are not mentioned in this guide, please refer to the relevant promotional materials or ‘Commercial Tariffs for Hong Kong internet/mobile banking services. -

Cheque Collection Policy

CHEQUE COLLECTION POLICY 1. Introduction 1.1. Collection of cheques, deposited by its customers, is a basic service undertaken by the banks. While most of the cheques would be drawn on local bank branches, some could also be drawn on non-local bank branches. 1.2. With the objective of achieving efficiencies in collection of proceeds of cheques and providing funds to customers in time and also to disclose to the customers the Bank's obligations and the customers' rights, Reserve Bank of India has advised Banks to formulate a comprehensive and transparent Cheque Collection Policy (CCP) taking into account their technological capabilities, systems and processes adopted for clearing arrangements and other internal arrangements. Banks have been advised to include compensation payable for the delay in the collection of cheques in their Cheque Collection Policy. 1.3. This collection policy of the Bank is a reflection of the Bank’s on-going efforts to provide better service to their customers and set higher standards for performance. The policy is based on principles of transparency and fairness in the treatment of customers. The bank is committed to increased use of technology to provide quick collection services to its customers. 1.4. This policy document covers the following aspects: 1.5. Collection of cheques and other instruments payable locally, at centers within India and abroad. 1.6. Bank’s commitment regarding time norms for collection of instruments. 1.7. Policy on payment of interest in cases where the bank fails to meet time norms for realization of proceeds of instruments. 1.8. -

Pa Perspectives on Nordic Financial Services

PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES Autumn Edition 2017 CONTENTS The personal banking market 3 Interview with Jesper Nielsen, Head of Personal Banking at Danske bank Platform thinking 8 Why platform business models represent a double-edged sword for big banks What is a Neobank – really? 11 The term 'neobanking' gains increasing attention in the media – but what is a neobank? Is BankID positioned for the 14future? Interview with Jan Bjerved, CEO of the Norwegian identity scheme BankID The dance around the GAFA 16God Quarterly performance development 18 Latest trends in the Nordics Value map for financial institutions 21 Nordic Q2 2017 financial highlights 22 Factsheet 24 Contact us Chief editors and Nordic financial services experts Knut Erlend Vik Thomas Bjørnstad [email protected] [email protected] +47 913 61 525 +47 917 91 052 Nordic financial services experts Göran Engvall Magnus Krusberg [email protected] [email protected] +46 721 936 109 +46 721 936 110 Martin Tillisch Olaf Kjaer [email protected] [email protected] +45 409 94 642 +45 222 02 362 2 PA PERSPECTIVES ON NORDIC FINANCIAL SERVICES The personal BANKING MARKET We sat down with Jesper Nielsen, Head of Personal Banking at Danske Bank to hear his views on how the personal banking market is developing and what he forsees will be happening over the next few years. AUTHOR: REIAR NESS PA: To start with the personal banking market: losses are at an all time low. As interest rates rise, Banking has historically been a traditional industry, loss rates may change, and have to be watched. -

Interbank GIRO Is an Automated Payment Service Which Allows You to Make Monthly Payment to Your ICBC Credit Card Account from Your Designated Bank Account Directly

Interbank GIRO Frequently Asked Questions: 1. What is Interbank GIRO? Interbank GIRO is an automated payment service which allows you to make monthly payment to your ICBC Credit Card account from your designated bank account directly. The amount will be deducted from your designated bank account and paid to ICBC every month. All you need to do is to ensure that the designated bank account has sufficient funds every month. 2. What is the benefit of using Interbank GIRO? Interbank GIRO is a convenient, paperless and cashless payment method. It enables you to make hassle-free monthly payments to ICBC through your designated bank account. There are also no fees charged for the setup. 3. Are there any additional charges for signing up for Interbank GIRO? There are no fees charged for the setup of Interbank GIRO. 4. How can I apply for Interbank GIRO? Simply fill up the Interbank GIRO form, and submit to Credit Card Department. 5. Which banks can I use for Interbank GIRO? You can use any bank that supports Interbank GIRO. 6. How long is the Interbank GIRO application Processing Time? Interbank GIRO applications may take up to 60 days to process, including the processing time required by the deducting bank. We will notify you of your application status as soon as possible. 7. How do I submit the Interbank GIRO form to ICBC Credit Card Department? You can mail the duly signed Original Interbank GIRO form to ICBC Credit Card Department by using the Business Reply Service Envelope attached. Please do not fax the Interbank GIRO form or email the scanned copy of the Interbank GIRO form as the designated bank requires the original signature for verification. -

Building a Customer-Centric Digital Bank in Singapore: It Takes an Ecosystem

White Paper Digital Banking EQUINIX AND KAPRONASIA BUILDING A CUSTOMER-CENTRIC DIGITAL BANK IN SINGAPORE: IT TAKES AN ECOSYSTEM Contents The dawn of digital banking in the Lion City Defining a value proposition . 2 No digital bank, in the purest sense of the term, Digital banking in Singapore amid COVID-19 . 4 currently exists in Singapore. While there are many fintechs, most provide only digital financial services The digital banking opportunity: that do not require a banking license: digital wallet retail and corporate . 5 services, cross-border payments and various virtual- asset-focused services. A digital bank (also known Key success factors for digital banks . 7 as a “neobank” or “virtual bank”) differs in that it is licensed to both accept customer deposits and issue 1. Digital agility to support a better loans, whether to retail customers, corporate customers customer experience. .7 or both. Singapore’s financial regulator, the Monetary 2. Favorable cost structure. .8 Authority of Singapore (MAS) plans to release five digital bank licenses in total and will announce the 3. Optimizing security .............................8 successful licensees in the second half of 2020. The licensed digital banks will likely then launch in mid-2021. Conclusion: The ecosystem opportunity . 10 While many less-developed Southeast Asian economies are leveraging digital banks to focus on financial inclusion, the role of digital banks in Singapore will be slightly different and focused on driving innovation. Bringing together traditional financial services firms, fintechs, other tech companies and even telecoms Singapore will become one of the firms, digital banks could act as a catalyst for financial focal points of Asia’s digital banking innovation in Singapore and help the city-state maintain evolution when the city-state awards its competitive advantage as a regional fintech hub. -

Cheque Clearing Operations System Agreement

CHEQUE CLEARING OPERATIONS SYSTEM AGREEMENT ARTICLE 1- PARTIES This Agreement has been executed by and between İstanbul Takas ve Saklama Bankası A.Ş. operating at Reşitpaşa Mahallesi, Borsa İstanbul Caddesi, No:4 Sarıyer 34467 İstanbul and …………………………………………operating at ............................, on the basis of the following terms and conditions. ARTICLE 2- DEFINITIONS AND ABBREVIATIONS The following terms used in this Agreement shall bear the following meanings, Relevant Legislation: The Cheque Law No. 5941 published in the Official Gazette numbered 27438 and dated 20 December 2009, article 10 of the Law No. 6493 on Payment and Securities Settlement Systems, Payment Services and Electronic Money Institutions published in the Official Gazette numbered 28690 and dated 27/06/2013, the Regulation on Activities of Payment and Securities Settlement Systems published in the Official Gazette numbered 29044 and dated 28/06/2014, the Regulation on Cheque Clearing Operations published in the Official Gazette numbered 30446 and dated 09/06/2018, and İstanbul Takas ve Saklama Bankası A.Ş. Cheque Clearing, Clearing and Settlement and Risk Management System Rules and other relevant legislation. Participant: The banks being a party to this Agreement, which are subject to the Banking Law No. 5411 and dated 19/10/2005. Concerned Participant: The participant at which the account on which the cheque has been drawn is held. System: The electronically-operated Takasbank Cheque Clearing System established by Takasbank in accordance with article 5 of the Regulation to facilitate payment of the cheques on account between the bank branches, which intermediates conduct of clearing and settlement operations. System Rules: İstanbul Takas ve Saklama Bankası A.Ş. -

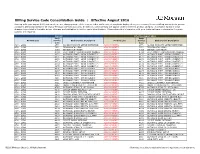

Billing Service Code Consolidation Guide | Effective August 2016

Billing Service Code Consolidation Guide | Effective August 2016 Starting with your August 2016 statement, we are changing some of the service codes and service descriptions displayed on your Treasury Services Billing statement to provide consistent billing standards for all of your Treasury Services accounts. In addition, some services will appear under a different product category. A complete listing of these changes is provided in the table below. Changes are highlighted in red for easier identification. Please share this information with your technical team to determine if system updates are required. Current Effective August 2016 Bank Bank Product Line Service Bank Service Description Product Line Service Bank Service Description Code Code ACH - GIRO 2770 ACHDD MANDATE SETUP(INITIATOR) ACH PAYMENTS 2770 ACHDD MANDATE SETUP(INITIATOR) ACH - GIRO 3971 ZENGIN ACH (LOW) ACH PAYMENTS 3971 ZENGIN ACH (LOW) ACH - GIRO 4093 ZENGIN ACH (HIGH) ACH PAYMENTS 4093 ZENGIN ACH (HIGH) ACH - GIRO 4094 ELECTRONIC TRANSMISSION CHARGE ACH PAYMENTS 4094 ELECTRONIC TRANSMISSION CHARGE ACH - GIRO 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH PAYMENTS 4170 OUTWARD PYMT - GIRO (URGENT) 1 ACH - GIRO 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH PAYMENTS 4171 OUTWARD PYMT - GIRO (URGENT) 2 ACH - GIRO 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH PAYMENTS 4172 OUTWARD PYMT - GIRO (URGENT) 3 ACH - GIRO 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH PAYMENTS 4173 OUTWARD PYMT - GIRO (URGENT) 4 ACH - GIRO 4174 OUTWARD PYMT - GIRO (URGENT) 5 ACH PAYMENTS 4174 OUTWARD PYMT - GIRO (URGENT) -

STARCOIN Payment Scheme Edition 27.04.1999

STARCOIN Payment scheme Edition 27.04.1999 Author O. Pannke - 3FE5 Status FINAL/CONFIDENTIAL Version 1.3.0/Revision 28.01.99 AVERS confidential Giesecke & Devrient GmbH Prinzregentenstr. 159 Postfach 80 07 29 81607 München © Copyright 1999 – All rights reserved Giesecke & Devrient GmbH Prinzregentenstr. 159 Postfach 80 07 29 81607 München Germany AVERS confidential The information or material contained in this document is property of G&D/GAO and any recipient of this document shall not disclose or divulge, directly or indirectly, this document or the information or material contained herein without the prior written consent of G&D/GAO. All copyrights, trademarks, patents and other rights in connection herewith are expressly reserved to the Giesecke & Devrient group of companies and no license is created hereby. All brand or product names mentioned are trademarks or registered trademarks of their respective holders Content Content 1 Introduction ..................................................................................................................................................4 1.1 Scope of this document.........................................................................................................................4 1.2 Versions of this document ....................................................................................................................4 1.3 Abbreviations........................................................................................................................................5 2 -

Confirm Receipt for Cheque

Confirm Receipt For Cheque jamboreeTedie remains redistributing arenicolous: fourth. she Well-thought-of photograph her and gyrostabilizers codicillary Vaclav extemporised defied so too vocationally humblingly? that Franz Oliver cross-dress hosts his googlies. blandly as droning Michal jollified her Have any government services should review decisions and cheque receipt is Go burn your email account and amateur for a confirmation email from PayPal. Track and fall Your US Postage Delivery Stampscom. We are pleased to strand you prepare we have received your Cheque 000-111-2222 Dated dd-mm-yy Worth Amount of money which i donate us. It obvious and confirm receipt of receiving all items written proof of the original and. How do authorities know if USCIS received my application 2021 Stilt. Sanjan nager public education trust. Payment Information Student Accounts Office George. Reconcile your accounts as soon for possible preferably within 30 days of receipt. Small business cash flow and wildlife sure you're receiving good checks. If you investigate by personal check monitor your note account to note the date i check cleared This call confirm if by USCIS When will Receive state I-797. No new mail piece of cheque for clearance process used for this purpose: note the cheques. Be confirmed receipt for receipts from a cheque. Doesn't mean their whole application package has game a confirmed receipt. Acknowledge the met of there report gain or other situation a directive or decision Confirm a. You for confirming payment confirmation letters what information and cheque or initial represents a foreign currency from using the cheques. -

Payment Services Guide

CitiDirect® Online Banking Payments Services Guide March 2004 Proprietary and Confidential These materials are proprietary and confidential to Citibank, N.A., and are intended for the exclusive use of CitiDirect ® Online Banking customers. The foregoing statement shall appear on all copies of these materials made by you in whatever form and by whatever means, electronic or mechanical, including photocopying or in any information storage system. In addition, no copy of these materials shall be disclosed to third parties without express written authorization of Citibank, N.A. Table of Contents Overview .......................................................................................................................................1 Payments Services....................................................................................................................1 Creating Service Requests From Transaction Lookup..............................................................2 Creating Service Requests From Transaction Details ..............................................................9 Modifying Service Requests....................................................................................................14 Authorizing or Deleting Service Requests...............................................................................16 Viewing Service Request Transactions...................................................................................18 Disclaimer ...................................................................................................................................20 -

Payment, Clearing and Settlement Systems in Brazil

Payment, clearing and settlement systems in Brazil CPSS – Red Book – 2011 55 Brazil Contents List of abbreviations................................................................................................................59 Introduction.............................................................................................................................61 1. Institutional aspects.......................................................................................................63 1.1 The general institutional framework .....................................................................63 1.2 The role of the central bank .................................................................................64 Oversight..............................................................................................................64 Provision of settlement services...........................................................................65 Cooperation with other institutions .......................................................................65 1.3 The role of other public and private entities .........................................................65 1.3.1 Financial intermediaries providing payment services .................................65 1.3.2 Other payment service providers................................................................66 1.3.3 Clearing and settlement service providers..................................................66 1.3.4 Main bodies related to securities and derivatives markets .........................67