Excelligence Learning Corp

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Annual Report

Building Long-term Wealth by Investing in Private Companies Annual Report and Accounts 12 Months to 31 January 2021 Our Purpose HarbourVest Global Private Equity (“HVPE” or the “Company”) exists to provide easy access to a diversified global portfolio of high-quality private companies by investing in HarbourVest-managed funds, through which we help support innovation and growth in a responsible manner, creating value for all our stakeholders. Investment Objective The Company’s investment objective is to generate superior shareholder returns through long-term capital appreciation by investing primarily in a diversified portfolio of private markets investments. Our Purpose in Detail Focus and Approach Investment Manager Investment into private companies requires Our Investment Manager, HarbourVest Partners,1 experience, skill, and expertise. Our focus is on is an experienced and trusted global private building a comprehensive global portfolio of the markets asset manager. HVPE, through its highest-quality investments, in a proactive yet investments in HarbourVest funds, helps to measured way, with the strength of our balance support innovation and growth in the global sheet underpinning everything we do. economy whilst seeking to promote improvement in environmental, social, Our multi-layered investment approach creates and governance (“ESG”) standards. diversification, helping to spread risk, and is fundamental to our aim of creating a portfolio that no individual investor can replicate. The Result Company Overview We connect the everyday investor with a broad HarbourVest Global Private Equity is a Guernsey base of private markets experts. The result is incorporated, London listed, FTSE 250 Investment a distinct single access point to HarbourVest Company with assets of $2.9 billion and a market Partners, and a prudently managed global private capitalisation of £1.5 billion as at 31 January 2021 companies portfolio designed to navigate (tickers: HVPE (£)/HVPD ($)). -

Private Equity Spotlight January 2007 / Volume 3 - Issue 1

Private Equity Spotlight January 2007 / Volume 3 - Issue 1 Welcome to the latest edition of Private Equity Spotlight, the monthly newsletter from Private Equity Intelligence, providing insights into private equity performance, investors and fundraising. Private Equity Spotlight combines information from our online products Performance Analyst, Investor Intelligence and Funds in Market. FEATURE ARTICLE page 01 INVESTOR SPOTLIGHT page 10 Overhang, what overhang? The favourable market and difficulty of getting allocations to With 2006’s $404 billion smashing all previous records for top quartile funds has led to increased LP interest in Asian private equity fund raising, some commentators are suggesting focused funds. We look at LPs investing in these funds. that there is now an ‘overhang’ of committed capital that the industry may struggle to invest. The facts suggest otherwise. • How do LPs perceive Asian focused funds? PERFORMANCE SPOTLIGHT page 05 • Who is making the most Growth in distributions to LPs and the rate of call-ups are significant investments? driving the fundraising market. Performance Spotlight looks at the trends. • Which types of investor are the most active? FUND RAISING page 06 After a record breaking year for fundraising in 2006, we • How much is being committed examine the latest news for venture and buyout funds, as well to the region? as examining the market for first-time fund vehicles. No. of Funds on INVESTOR NEWS page 12 US Europe ROW Road All the latest news on investors in private equity: Venture 202 97 83 382 • State of Wisconsin Investment Board posts high returns Buyout 100 48 36 184 boosted by its private equity portfolio Funds of Funds 65 47 12 124 • Somerset County Council Pension Fund seeks new fund of Other 129 31 42 202 funds manager • LACERA looks for new advisor Total 496 223 173 892 • Indiana PERF is set to issue real estate RFPs SUBSCRIPTIONS If you would like to receive Private Equity Spotlight each month • COPERA close to appointing new alternatives chief. -

Advancing the Role of the Finance Executive

Advancing the role of the finance executive Built on the back of in-depth conversations with private equity CFOs, a 20-year heritage of our CFO community and the annual conference Contents » Connect. Evolve. Advance. » Past attendees list » Testimonials » Product offering » Messaging platform functionality » Unlock your networking opportunities with our virtual platform » Events 2 of 13 Advance your career Get direct access to industry peers and specialists who are tackling the same problems and obstacles you face. Benchmark your strategies and solutions to progress Connect. with confidence. Evolve. Advance your team Successful CFOs have a strong support team. Give Advance. your COO, CIO CCO, Finance Director and Controller The industry defining CFO & COO Forum All Access. Dive into a wide range of operational hot is now just one of the many essential topics from tax and compliance to recruitment, data updates we’ll give you throughout the year security management and cyber risk. with your CFO All Access subscription, designed around you to unlock: » Insider know-how – from CFO leaders at the top firms, to the innovators in the mid and lower market Advance your firm » Sector specific xpertisee – from technology to human capital to ESG The world is changing faster than ever – driven by macro issues such as climate change, a pandemic » Regulatory insight – direct from SEC global recession and political uncertainty. Progressive executives and directors strategies on ESG and diversity are no longer nice to » Authoritative market commentary – haves. LPs are directing capital to firms that take these from our acclaimed editorial team topics seriously and can show it. -

Private Equity in Healthcare – an Updated Review of Selected Niche Investment Areas

Private Equity in Healthcare – An Updated Review of Selected Niche Investment Areas SCOTT BECKER, PARTNER HOLLY BUCKLEY, PARTNER 312-750-6016 | [email protected] 312-849-3687 | [email protected] 77 West Wacker Drive, Suite 4100 77 West Wacker Drive, Suite 4100 Chicago, IL 60601-1818 Chicago, IL 60601-1818 ALYSSA C. CAMPBELL, ASSOCIATE GEOFFREY C. COCKRELL, PARTNER 312-750-3510 | [email protected] 312-849-8272 | [email protected] 77 West Wacker Drive, Suite 4100 77 West Wacker Drive, Suite 4100 Chicago, IL 60601-1818 Chicago, IL 60601-1818 ERIN E. DINE, ASSOCIATE TIMOTHY J. FRY, ASSOCIATE 312-750-3524 | [email protected] 312-750-8659 | [email protected] 77 West Wacker Drive, Suite 4100 77 West Wacker Drive, Suite 4100 Chicago, IL 60601-1818 Chicago, IL 60601-1818 JULIE K. LETWAT, COUNSEL AMANDA K. ROENIUS, ASSOCIATE 312-750-2777 | [email protected] 312-849-8157 | [email protected] 77 West Wacker Drive, Suite 4100 77 West Wacker Drive, Suite 4100 Chicago, IL 60601-1818 Chicago, IL 60601-1818 AMBER MCGRAW WALSH, PARTNER BART WALKER, PARTNER 312-750-3596 | [email protected] 704-343-8923 | [email protected] 77 West Wacker Drive, Suite 4100 201 North Tryon Street, Suite 3000 Chicago, IL 60601-1818 Charlotte, NC 28202 October 7, 2019 www.mcguirewoods.com McGuireWoods marketing communications are intended to provide information of general interest to the public. Marketing communications are not intended to offer legal advice about specific situations or problems. McGuireWoods does not intend to create an attorney-client relationship by offering general interest information, and reliance on information presented in marketing communications does not create such a relationship. -

Tygris Commercial Finance Group, Inc. Launched with Over $1.75 Billion in Equity Commitments 5/20/08 8:41 PM

Tygris Commercial Finance Group, Inc. Launched With Over $1.75 Billion in Equity Commitments 5/20/08 8:41 PM Tygris Commercial Finance Group, Inc. Launched With Over $1.75 Billion in Equity Commitments Newly Formed Commercial Finance Company Created to Support the Financing Needs of Middle Market Companies Largest Initial Capital Raise Ever in the U.S. Commercial Finance Sector Tygris to Acquire US Express Leasing, Inc. and MarCap LLC NEW YORK, May 20 /PRNewswire/ -- Tygris Commercial Finance Group, Inc. ("Tygris"), a commercial finance company, today announced its formation and funding with over $1.75 billion in equity commitments -- the largest initial capital raise ever in the U.S. commercial finance sector. Tygris has assembled a team of commercial finance industry executives with significant experience leading large commercial finance businesses. Frederick E. "Rick" Wolfert, formerly Vice Chairman of Commercial Finance of the CIT Group and President of Heller Financial Inc., is the Company's CEO. Tygris will initially have offices in Chicago, Stamford, CT and Parsippany, NJ. Tygris was founded by Aquiline Capital Partners LLC ("Aquiline"), a New York based private equity firm specializing in financial services, with New Mountain Capital, L.L.C. and TPG Capital joining as lead investors. Tygris' key investors also include Diamond Castle Holdings, LLC and Hamilton Lane. Tygris has established significant relationships with financial institutions including Deutsche Bank, Credit Suisse, SunTrust Robinson Humphrey, Barclays, Wachovia and Wells Fargo Foothill. Tygris was created to provide liquidity and growth capital to middle market companies throughout North America in response to the current credit market dislocation that has constrained the availability of such capital. -

Financial Technology Sector Summary

Financial Technology Sector Summary July 30, 2014 Financial Technology Sector Summary Table of Contents I. GCA Savvian Overview II. Market Summary III. Payments / Banking IV. Securities / Capital Markets / Data & Analytics V. Healthcare / Insurance I. GCA Savvian Overview GCA Savvian Overview Highlights Firm Statistics GCA Savvian Focus . Over 225 professionals today Mergers & Acquisitions Private Capital Markets . Full spectrum of buy-side, sell- . Agented private capital raiser . Headquarters in San Francisco and Tokyo; offices in New side and strategic advisory York, London, Shanghai, Mumbai, and Osaka . Equity and debt capital markets . Public and private company advisory services experience . Provides mergers and acquisitions advisory services, private . Core competency, with important capital & capital markets advisory services, and principal . Strategic early-stage growth relationships among the venture investing companies through industry capital and private equity defining, multi-billion dollar community transactions . Over 500 transactions completed . Publicly traded on the Tokyo Stock Exchange (2174) Senior level attention and focus, Relationships and market extensive transaction intelligence; a highly experienced team in experience and deep domain insight the industry Global Advisory Firm Market Positioning Bulge Bracket Growth Sector Focus Transaction Expertise . Senior Team with . Growth Company Focus Unparalleled Transaction . Sector Expertise / Domain Experience Knowledge . Highest Quality Client . Private Capital Access -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Form

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 Form 10-K (Mark One) ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year ended December 31, 2016 or TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the transition period from to Commission File No. 001-35537 COMMUNITY CHOICE FINANCIAL INC. (Exact name of registrant as specified in its charter) Ohio 45-1536453 (State or other jurisdiction of (IRS Employer Identification No.) incorporation or organization) 6785 Bobcat Way, Suite 200, Dublin, Ohio 43016 (Address of principal executive offices) (Zip Code) Registrant’s telephone number, including area code (614) 798-5900 Securities registered pursuant to Section 12(b) of the Act: None Securities registered pursuant to Section 12(g) of the Act: None Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes No Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes No Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes No Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). -

Directory National Association of Therapeutic Schools and Programs

NATSAP 2009 Directory National Association of Therapeutic Schools and Programs NATSAP 2009 DIRECTORY e only bee, th s th at e i m op ak H es “ h o n e y w i t h o u t f l o w e r s , ” - R o b e r t G r e e n I n g e r s o l l Schools and Programs for Young People Experiencing Behavioral, Psychiatric and Learning Diffi culties NATSAP • www.natsap.org • (301) 986-8770 1 NATSAP 2009 Directory NATSAP 2009 Directory TABLE OF CONTENTS Page About NATSAP ............................................................................................3 NATSAP Ethical Principles ..........................................................................4 Program Definitions ......................................................................................5-6 NATSAP Alumni Advisory Council ............................................................10 Questions to Ask Before Making a Final Placement ....................................11-14 Program Listing By Name ............................................................................11-14 Program Directory Listings ...........................................................................16-187 Program Listing By State ...............................................................................................188-192 By Gender ...........................................................................................193-195 By Age ................................................................................................195-199 By Program Type ................................................................................200-202 -

Therapeutic Boarding Schools, Wilderness Camps, Boot Camps and Behavior Modification Facilities, Have Sprung up in Greater Numbers Since the 1990S

CHILD ABUSE AND DECEPTIVE MARKETING BY RESIDENTIAL PROGRAMS FOR TEENS HEARING BEFORE THE COMMITTEE ON EDUCATION AND LABOR U.S. HOUSE OF REPRESENTATIVES ONE HUNDRED TENTH CONGRESS SECOND SESSION HEARING HELD IN WASHINGTON, DC, APRIL 24, 2008 Serial No. 110–89 Printed for the use of the Committee on Education and Labor ( Available on the Internet: http://www.gpoaccess.gov/congress/house/education/index.html U.S. GOVERNMENT PRINTING OFFICE 41–839 PDF WASHINGTON : 2008 For sale by the Superintendent of Documents, U.S. Government Printing Office Internet: bookstore.gpo.gov Phone: toll free (866) 512–1800; DC area (202) 512–1800 Fax: (202) 512–2104 Mail: Stop IDCC, Washington, DC 20402–0001 VerDate 0ct 09 2002 15:49 Jul 16, 2008 Jkt 000000 PO 00000 Frm 00001 Fmt 5011 Sfmt 5011 G:\DOCS\110TH\FC\110-89\41839.TXT HBUD1 PsN: DICK COMMITTEE ON EDUCATION AND LABOR GEORGE MILLER, California, Chairman Dale E. Kildee, Michigan, Vice Chairman Howard P. ‘‘Buck’’ McKeon, California, Donald M. Payne, New Jersey Senior Republican Member Robert E. Andrews, New Jersey Thomas E. Petri, Wisconsin Robert C. ‘‘Bobby’’ Scott, Virginia Peter Hoekstra, Michigan Lynn C. Woolsey, California Michael N. Castle, Delaware Rube´n Hinojosa, Texas Mark E. Souder, Indiana Carolyn McCarthy, New York Vernon J. Ehlers, Michigan John F. Tierney, Massachusetts Judy Biggert, Illinois Dennis J. Kucinich, Ohio Todd Russell Platts, Pennsylvania David Wu, Oregon Ric Keller, Florida Rush D. Holt, New Jersey Joe Wilson, South Carolina Susan A. Davis, California John Kline, Minnesota Danny K. Davis, Illinois Cathy McMorris Rodgers, Washington Rau´ l M. -

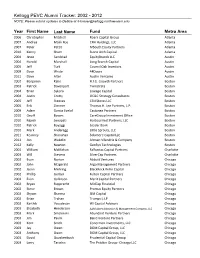

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please Submit Updates to Debbie at [email protected]

Kellogg PEVC Alumni Tracker: 2002 - 2012 NOTE: Please submit updates to Debbie at [email protected] Year First Name Last Name Fund Metro Area 2006 Christopher Mitchell Roark Capital Group Atlanta 2007 Andrea Malik Roe CRH Holdings, LLC Atlanta 2007 Peter Pettit MSouth Equity Partners Atlanta 2010 Kenny Shum Stone Arch Capital Atlanta 2004 Jesse Sandstad EquityBrands LLC Austin 2004 Harold Marshall Long Branch Capital Austin 2005 Jeff Turk Council Oak Investors Austin 2009 Dave Wride 44Doors Austin 2011 Dave Alter Austin Ventures Austin 2002 Benjamin Kahn H.I.G. Growth Partners Boston 2003 Patrick Davenport Twinstrata Boston 2004 Brian Sykora Lineage Capital Boston 2004 Justin Crotty OC&C Strategy Consultants Boston 2005 Jeff Steeves CSN Stores LLC Boston 2005 Erik Zimmer Thomas H. Lee Partners, L.P. Boston 2009 Adam Garcia Evelof Castanea Partners Boston 2010 Geoff Bowes CareGroup Investment Office Boston 2010 Rajesh Senapati HarbourVest Partners, LLC Boston 2010 Patrick Boyaggi Leader Bank Boston 2010 Mark Anderegg Little Sprouts, LLC Boston 2011 Kearney Shanahan Solamere Capital LLC Boston 2012 Jon Wakelin Altman Vilandrie & Company Boston 2012 Kelly Newton GenSyn Technologies Boston 2003 William McMahan Falfurrias Capital Partners Charlotte 2003 Will Stevens SilverCap Partners Charlotte 2002 Evan Norton Abbott Ventures Chicago 2002 John Fitzgerald Argo Management Partners Chicago 2002 Jason Mehring BlackRock Kelso Capital Chicago 2002 Phillip Gerber Fulton Capital Partners Chicago 2002 Evan Gallinson Merit Capital Partners -

Aspen Education Group

ASPEN ACHIEVEMENT ACADEMY A division of Aspen Education Group SUPPLEMENTAL DOCUMENTS for admission Please note: The initial application needs to be completed & submitted on line at www.aspenacademy.com Please complete these supplemental documents in addition to the application and fax to 435.836.2477 If you have questions contact your admissions counselor at 435.836.2472 ASPEN ACHIEVEMENT ACADEMY PO Box 400 / 98 South Main Street Loa, UT 84747 800.283.8334 Admissions Office 435.836.2472 Main Office 435.836.2477 FAX www.aspenacademy.com A Aspen Education Group AUTHORIZATION FOR USE OR DISCLOSURE OF HEALTH INFORMATION This form is a RELEASE OF INFORMATION FORM. Completion of this document authorizes the disclosure and/or use of individually identifiable health information, as set forth below, consistent with State and Federal law concerning the privacy of such information. Failure to provide all information requested may invalidate this Authorization. USE AND DISCLOSURE OF HEALTH INFORMATION I hereby authorize the use or disclosure of my health information as follows: Patient Name: Persons/Organizations authorized to use or disclose the information: 1 Aspen Achievement Academy Persons/Organizations authorized to receive the information: Aspen Achievement Academy Name/Title: Name/Title: Address: Address: City: City: State: Zip: State: Zip: E-mail address: E-mail address: Phone ( ) Phone ( ) Purpose of requested use or disclosure: 2 This Authorization applies to the following information (select only one of the following):3 All health information pertaining to any medical history, mental or physical condition and treatment received. [Optional] Except: Only the following records or types of health information (including any dates): EXPIRATION This Authorization expires [insert date or event]:4 NOTICE OF RIGHTS AND OTHER INFORMATION I may refuse to sign this Authorization. -

Private Equity Benchmark Report

Preqin Private Equity Benchmarks: All Private Equity Benchmark Report As of 31st March 2014 alternative assets. intelligent data. Preqin Private Equity Benchmarks: All Private Equity Benchmark Report As of 31st March 2014 Report Produced on 9th October 2014 This publication is not included in the CLA Licence so you must not copy any portion of it without the permission of the publisher. All rights reserved. The entire contents of the report are the Copyright of Preqin Ltd. No part of this publication or any information contained in it may be copied, transmitted by any electronic means, or stored in any electronic or other data storage medium, or printed or published in any document, report or publication, without the express prior written approval of Preqin Ltd. The information presented in the report is for information purposes only and does not constitute and should not be construed as a solicitation or other offer, or recommendation to acquire or dispose of any investment or to engage in any other transaction, or as advice of any nature whatsoever. If the reader seeks advice rather than information then he should seek an independent fi nancial advisor and hereby agrees that he will not hold Preqin Ltd. responsible in law or equity for any decisions of whatever nature the reader makes or refrains from making following its use of the report. While reasonable efforts have been used to obtain information from sources that are believed to be accurate, and to confi rm the accuracy of such information wherever possible, Preqin Ltd. Does not make any representation or warranty that the information or opinions contained in the report are accurate, reliable, up-to-date or complete.