A Tale of Three Telcos Decline and Fall by Nigel Hawkins , Hardman & Co Infrastructure and Renewables Specialist

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Costs and Benefits of Relaxing International Frequency Harmonisation and Radio Standards

COSTS AND BENEFITS OF RELAXING INTERNATIONAL FREQUENCY HARMONISATION AND RADIO STANDARDS FINAL REPORT INDEPEN AND AEGIS SYSTEMS March 2004 Indepen Diespeker Wharf 38 Graham Street London N1 8JX Telephone +44 (0) 20 7324 1800 Facsimile +44 (0) 20 7704 0872 http://www.indepen.co.uk Indepen Consulting Ltd is a management consultancy providing advice and assistance to organisations addressing the challenges of regulation, competition and restructuring in telecommunications and utility sectors. Further information can be found at www.indepen.co.uk Aegis Systems Ltd provides expertise in the market use, regulation and licensing of radio frequency spectrum. Further information can be found at www.aegis-systems.co.uk Project Team: Phillipa Marks (Director, Indepen) Brian Williamson (Principal Consultant, Indepen) Helen Lay (Consultant, Indepen) Val Jervis (Aegis Systems) John Horrocks (Horrocks Technology) Contents Summary..........................................................................................................1 1 Introduction ..........................................................................................15 2 Costs and Benefits of Standards and Harmonisation Measures..19 3 Case studies .........................................................................................39 4 Conclusions and Recommendations................................................75 Glossary.........................................................................................................84 Annex 1 GSM 900 and 1800 MHz........................................................87 -

List of Marginable OTC Stocks

List of Marginable OTC Stocks @ENTERTAINMENT, INC. ABACAN RESOURCE CORPORATION ACE CASH EXPRESS, INC. $.01 par common No par common $.01 par common 1ST BANCORP (Indiana) ABACUS DIRECT CORPORATION ACE*COMM CORPORATION $1.00 par common $.001 par common $.01 par common 1ST BERGEN BANCORP ABAXIS, INC. ACETO CORPORATION No par common No par common $.01 par common 1ST SOURCE CORPORATION ABC BANCORP (Georgia) ACMAT CORPORATION $1.00 par common $1.00 par common Class A, no par common Fixed rate cumulative trust preferred securities of 1st Source Capital ABC DISPENSING TECHNOLOGIES, INC. ACORN PRODUCTS, INC. Floating rate cumulative trust preferred $.01 par common $.001 par common securities of 1st Source ABC RAIL PRODUCTS CORPORATION ACRES GAMING INCORPORATED 3-D GEOPHYSICAL, INC. $.01 par common $.01 par common $.01 par common ABER RESOURCES LTD. ACRODYNE COMMUNICATIONS, INC. 3-D SYSTEMS CORPORATION No par common $.01 par common $.001 par common ABIGAIL ADAMS NATIONAL BANCORP, INC. †ACSYS, INC. 3COM CORPORATION $.01 par common No par common No par common ABINGTON BANCORP, INC. (Massachusetts) ACT MANUFACTURING, INC. 3D LABS INC. LIMITED $.10 par common $.01 par common $.01 par common ABIOMED, INC. ACT NETWORKS, INC. 3DFX INTERACTIVE, INC. $.01 par common $.01 par common No par common ABLE TELCOM HOLDING CORPORATION ACT TELECONFERENCING, INC. 3DO COMPANY, THE $.001 par common No par common $.01 par common ABR INFORMATION SERVICES INC. ACTEL CORPORATION 3DX TECHNOLOGIES, INC. $.01 par common $.001 par common $.01 par common ABRAMS INDUSTRIES, INC. ACTION PERFORMANCE COMPANIES, INC. 4 KIDS ENTERTAINMENT, INC. $1.00 par common $.01 par common $.01 par common 4FRONT TECHNOLOGIES, INC. -

Issue 23 November 2005 1 Submarine Telecoms Forum Is Published Bi-Monthly by WFN Strategies, L.L.C

DDefenseefense & Non-traditionaNon-traditional CableCable SystemsSystems – 4th4th AnnAnniiversaryversary IssueIssue November 2005 Issue 23 1 Submarine Telecoms Forum is published bi-monthly by WFN Strategies, L.L.C. The publication may not be reproduced or transmitted in any form, in whole or in part, without the Exordium permission of the publishers. NNovember’sovember’s iissuessue mmarksarks ourour ffourthourth aanniversarynniversary inin publishingpublishing SubmarineSubmarine TelecomsTelecoms Forum,Forum, andand thoughthough tthngshngs sstilltill aaren’tren’t aass rrosyosy aass theythey werewere inin thethe “build“build itit andand theythey willwill come”come” era,era, nornor willwill theythey probablyprobably everever Submarine Telecoms Forum is an independent com- bbee – tthingshings aarere stillstill ccertainlyertainly mmuchuch improved.improved. mercial publication, serving as a freely accessible forum for professionals in industries connected with submarine optical TThehe ffewew pprinciplesrinciples wwee establishedestablished inin thethe beginning,beginning, wewe continuecontinue toto holdhold dear.dear. WeWe promisedpromised then,then, andand fi bre technologies and techniques. ccontinueontinue ttoo ppromiseromise yyou,ou, oourur rreaders:eaders: Liability: while every care is taken in preparation of this 11.. TThathat wwee wwillill pproviderovide a wwideide rrangeange ooff iideasdeas aandnd iissues;ssues; publication, the publishers cannot be held responsible for the 22.That.That wwee wwillill sseekeek ttoo iincite,ncite, eentertainntertain -

Telecom in the Time of Crash

INCIDENTAL PAPER Telecom in the Time of Crash Kas Kalba November 2002 Program on Information Resources Policy Center for Information Policy Research Harvard University The Program on Information Resources Policy is jointly sponsored by Harvard University and the Center for Information Policy Research. Chairman Managing Director Anthony G. Oettinger John C. B. LeGates Kas Kalba is President of Kalba International, Inc., a management consulting and research firm. He is writing a book on the telecom crash, from which this paper is derived, and has been a longstanding participant in PIRP activities. Copyright © 2002 by Kas Kalba. Not to be reproduced in any form without written consent from Kas Kalba, Kalba International. Inc., 23 Sandy Pond Road, Lincoln, 01773, USA. +1 (781) 259-9589. E-mail: [email protected] URL: http://www.kalbainternational.com ISBN 1-879716-85-2 I-02-2 November 2002 PROGRAM ON INFORMATION RESOURCES POLICY Harvard University Center for Information Policy Research Affiliates AT&T Corp. Nippon Telegraph & Telephone Corp Australian Telecommunications Users (Japan) Group PDS Consulting BellSouth Corp. PetaData Holdings, Inc. The Boeing Company Samara Associates Booz Allen Hamilton Skadden, Arps, Slate, Meagher & Flom Center for Excellence in Education LLP Commission of the European Sonexis Communities Strategy Assistance Services Critical Path TOR LLC CyraCom International United States Government: Ellacoya Networks, Inc. Department of Commerce Hanaro Telecom Corp. (Korea) National Telecommunications and Hearst Newspapers Information Administration Hitachi Research Institute (Japan) Department of Defense IBM Corp. National Defense University Korea Telecom Department of Health and Human Lee Enterprises, Inc. Services Lexis–Nexis National Library of Medicine John and Mary R. -

Download Date 30/09/2021 09:11:11

Index revisions, market quality and the cost of equity capital. Item Type Thesis Authors Aldaya, Wael H. Rights <a rel="license" href="http://creativecommons.org/licenses/ by-nc-nd/3.0/"><img alt="Creative Commons License" style="border-width:0" src="http://i.creativecommons.org/l/by- nc-nd/3.0/88x31.png" /></a><br />The University of Bradford theses are licenced under a <a rel="license" href="http:// creativecommons.org/licenses/by-nc-nd/3.0/">Creative Commons Licence</a>. Download date 30/09/2021 09:11:11 Link to Item http://hdl.handle.net/10454/5687 University of Bradford eThesis This thesis is hosted in Bradford Scholars – The University of Bradford Open Access repository. Visit the repository for full metadata or to contact the repository team © University of Bradford. This work is licenced for reuse under a Creative Commons Licence. Index revisions, market quality and the cost of equity capital Wael Hamdi Aldaya Submitted for the degree of Doctor of Philosophy School of Management University of Bradford 2012 i ABSTRACT Wael Hamdi AlDAYA Index revisions, market quality and the cost of equity capital Keywords: Index revisions, stock liquidity, cost of capital, market quality, price efficiency. This thesis examines the impact of FTSE 100 index revisions on the various aspects of stock market quality and the cost of equity capital. Our study spans over the period 1986–2009. Our analyses indicate that the index membership enhances all aspects of liquidity, including trading continuity, trading cost and price impact. We also show that the liquidity premium and the cost of equity capital decrease significantly after additions, but do not exhibit any significant change following deletions. -

The Great Telecom Meltdown for a Listing of Recent Titles in the Artech House Telecommunications Library, Turn to the Back of This Book

The Great Telecom Meltdown For a listing of recent titles in the Artech House Telecommunications Library, turn to the back of this book. The Great Telecom Meltdown Fred R. Goldstein a r techhouse. com Library of Congress Cataloging-in-Publication Data A catalog record for this book is available from the U.S. Library of Congress. British Library Cataloguing in Publication Data Goldstein, Fred R. The great telecom meltdown.—(Artech House telecommunications Library) 1. Telecommunication—History 2. Telecommunciation—Technological innovations— History 3. Telecommunication—Finance—History I. Title 384’.09 ISBN 1-58053-939-4 Cover design by Leslie Genser © 2005 ARTECH HOUSE, INC. 685 Canton Street Norwood, MA 02062 All rights reserved. Printed and bound in the United States of America. No part of this book may be reproduced or utilized in any form or by any means, electronic or mechanical, including photocopying, recording, or by any information storage and retrieval system, without permission in writing from the publisher. All terms mentioned in this book that are known to be trademarks or service marks have been appropriately capitalized. Artech House cannot attest to the accuracy of this information. Use of a term in this book should not be regarded as affecting the validity of any trademark or service mark. International Standard Book Number: 1-58053-939-4 10987654321 Contents ix Hybrid Fiber-Coax (HFC) Gave Cable Providers an Advantage on “Triple Play” 122 RBOCs Took the Threat Seriously 123 Hybrid Fiber-Coax Is Developed 123 Cable Modems -

General Distribution OCDE/GD(96)179

General Distribution OCDE/GD(96)179 LOCAL TELECOMMUNICATION COMPETITION: DEVELOPMENTS AND POLICY ISSUES ORGANISATION FOR ECONOMIC CO-OPERATION AND DEVELOPMENT Paris 46204 Document complet disponible sur OLIS dans son format d'origine Complete document available on OLIS in its original format Copyright OECD, 1996 Applications for permission to reproduce or translate all or part of this material should be made to: Head of Publications Service, OECD, 2 rue André-Pascal, 75775 Paris Cedex 16, France. 2 TABLE OF CONTENTS MAIN POINTS......................................................................................................................................... 6 LOCAL TELECOMMUNICATION COMPETITION.............................................................................. 8 Defining Local Markets......................................................................................................................... 8 Redefining Local Markets ..................................................................................................................... 9 Importance of Local Telecommunication Competition for Traditional and New Services .....................19 MARKET SHARE AND BOTTLENECK CONTROL OF CUSTOMER ACCESS NETWORKS ..........23 Merging Regulatory Streams................................................................................................................23 National Markets..................................................................................................................................26 International -

Vitruvius on Architecture

107390 THE LOEB CLASSICAL LIBRARY FOUNDED BY JAMES LOEB, LL.D. EDITED BY fT. E. PAGE, C.H., LITT.D. LL.D. H. D. LITT.D. j-E. CAPPS, PH.D., fW. KOUSE, L. A. POST, M.A. E. H. WARMINGTON, M.A.. F.E.HIST.SOC. VITRUVIUS ON ARCHITECTURE I uzaJt yiTKUVIUS ON ARCHITECTURE EDITED FROM THE HARLEIAN MANUSCRIPT 2767 AI TRANSLATED INTO ENGLISH BY FRANK GRANGER, D.Lrr., AJLLB.A. PROFESSOR IN UNIVERSITY COLLEGE, NOTTINGHAM IN TWO VOLUMES I CAMBRIDGE, MASSACHUSETTS HARVARD UNIVERSITY PRESS LONDON WILLIAM HEINEMANN LTD MCMLV First printed 1931 Reprinted 1944,1955 To JESSB LORD TRBXT Printed in Great Britain CONTENTS PAQK PREFACE vii INTRODUCTION : VITRUVIUS AND THE ARCHITECTURE OF THE WEST ...... ix HISTORY OF THE MSS. OF VITRUVIUS . X\'i THE EARLIEST EDITIONS OF VITRUVIUS . XXi THE SCHOLIA OF THE MSS. XXV - THE ILLUSTRATIONS OF THE MSS. XXVli THE LANGUAGE OF VITRUVIUS . XXViii BIBLIOGRAPHY: THE MSS. XXXli EDITIONS ...... xxxiii TRANSLATIONS XXXiii THE CHIEF CONTRIBUTIONS TO THE STUDY OF VITRUVIUS ..... xxxiv BOOKS OF GENERAL REFERENCE . XXXVi TEXT AND ENGLISH TRANSLATION: BOOK I. ARCHITECTURAL PRINCIPLES . 1 BOOK II. EVOLUTION OF BUILDING : USE OF MATERIALS . 71 BOOK III. IONIC TEMPLES . 151 BOOK IV. DORIC AND CORINTHIAN TEMPLES 199 BOOK V. PUBLIC BUILDINGS I THEATRES (AND MUSIC), BATHS, HARBOURS . 249 INDEX OF ARCHITECTURAL TERMS 319 CONTENTS ILLUSTRATIONS: THE CAPITOL DOUGGA . (Frontispiece) PLATE A. WINDS AND DIRECTION OF STREETS (at end) PLATE B. PLANS OF TEMPLES . PLATE C. IONIC ORDER . PLATE 0. CORINTHIAN ORDER (see Frontispiece) PLATE E. DORIC ORDER . (at end] PLATE F. MUSICAL SCALES . , . , PLATE O. THEATRE . -

Admission Document Prepared in Accordance with the AIM Rules

233582 Gold Cover Spread 8mm Spine 07/10/2014 14:06 Page 1 Placing and Admission to AIM Gamma Communications plc Nominated AdviserAdviser,, Broker & Sole Bookrunner Perivan Financial Print 233582 233582 Gold pp001-pp004 07/10/2014 14:06 Page 1 THIS DOCUMENT IS IMPORTANT AND REQUIRES YOUR IMMEDIATE ATTENTION If you are in any doubt as to the contents of this document or as to what action you should take you should consult your stockbroker, bank manager, solicitor, accountant or other independent financial adviser authorised under the Financial Services and Markets Act 2000 (“FSMA”) who specialises in advising on the acquisition of shares and other securities. This document comprises an admission document prepared in accordance with the AIM Rules. Application will be made for the Ordinary Shares to be admitted to trading on AIM. It is expected that Admission will become effective and that trading in the Ordinary Shares on AIM will commence at 8.00 a.m. on 10 October 2014. The Ordinary Shares are not dealt on any other recognised investment exchange and it is emphasised that no application has been, or is being, made for the Ordinary Shares to be admitted to any such exchange. This document is not an approved prospectus for the purposes of section 85 of FSMA, has not been prepared in accordance with the Prospectus Rules published by the Financial Conduct Authority (“FCA”) and a copy of it has not been, and will not be, delivered to the UK Listing Authority in accordance with the Prospectus Rules or delivered to or approved by any other authority which could be a competent authority for the purposes of the Prospectus Directive. -

Expmlanatory Memorandum for the Quarterly Report

Irish Communications Market Quarterly Key Data Explanatory Memorandum Document No: 05/92a Date: 20th December 2005 An Coimisiún um Rialáil Cumarsáide Commission for Communications Regulation Abbey Court Irish Life Centre Lower Abbey Street Dublin 1 Ireland Telephone +353 1 804 9600 Fax +353 1 804 9680 Email [email protected] Web www.comreg.ie Contents Contents ..............................................................................................1 1 Executive Summary..........................................................................2 2 Questionnaire Issue ..........................................................................3 3 Primary Data ...................................................................................1 4 Secondary data ................................................................................5 4.1 PRICING DATA..........................................................................................5 4.2 COMPARATIVE DATA ...................................................................................6 5 Glossary..........................................................................................7 6 PPP Conversion Rates data ................................................................0 1 ComReg 05/92a 1 Executive Summary Following the publication of an annual market review in November 1999, ComReg’s predecessor- the ODTR- published its first Quarterly Review on 22nd March 2000. Since that date, ComReg has continued to collect primary statistical data from authorised operators on a quarterly -

Relazione Annuale 2018 Sull’Attività Svolta E Sui Programmi Di Lavoro

Relazione annuale 2018 sull’attività svolta e sui programmi di lavoro www.agcom.it www.agcom.it RELAZIONE ANNUALE 2018 sull’attività svolta e sui programmi di lavoro Autorità per le garanzie nelle comunicazioni Presidente ANGELO MARCELLO CARDANI Componenti ANTONIO MARTUSCIELLO MARIO MORCELLINI ANTONIO NICITA FRANCESCO POSTERARO Segretario generale RICCARDO CAPECCHI Vice segretari generali LAURA ARÌA ANTONIO PERRUCCI Capo di gabinetto del Presidente ANNALISA D’ORAZIO Indice Prefazione del Presidente: 20 anni di AGCOM. 7 Premessa alla lettura . 9 CAPITOLO I CAPITOLO III Il contesto istituzionale dell’Autorità . 11 Il contesto economico e concorrenziale: assetti e prospettive dei mercati regolati 73 1.1 L’Autorità nel contesto europeo . 14 3.1 Gli scenari nei mercati delle telecomuni- 1.2 Il ruolo e le relazioni istituzionali cazioni . 77 dell’Autorità nel contesto italiano . 18 3.2 Il contesto di mercato nel settore dei servizi postali . 98 1.3 Le sinergie e la nuova regolamentazione . 24 3.3 L’evoluzione dei media e la rivoluzione digitale . 105 CAPITOLO II CAPITOLO IV L’attività dell’Autorità . 31 L’organizzazione dell’Autorità 141 2.1 Le attività regolamentari e di vigilanza nei 4.1 L’assetto organizzativo e la politica delle mercati delle telecomunicazioni . 33 risorse umane . 143 4.2 Gli organismi strumentali e ausiliari . 150 2.2 I servizi “media”: analisi, regole e controlli 37 4.3 La tutela giurisdizionale in ambito 2.3 Tutela e garanzia dei diritti nel sistema nazionale . 154 digitale . 42 2.4 La regolamentazione e la vigilanza nel settore postale . 53 CAPITOLO V I risultati conseguiti e i programmi di lavoro 157 2.5 I rapporti con i consumatori e gli utenti. -

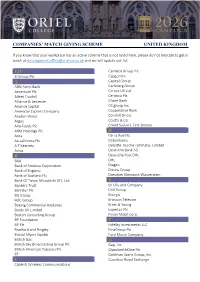

Matched Giving Company List

COMPANIES’ MATCH GIVING SCHEME UNITED KINGDOM If you know that your workplace has an active scheme that is not listed here, please do not hesitate to get in touch at [email protected] and we will update our list. 123 Camelot Group Plc 3i Group Plc Capgemini A Capital Group ABN Amro Bank Carlsberg Group Accenture Plc Cemex UK Ltd Alfred Dunhill Centrica Plc Alliance & Leicester Chase Bank Alliance Capital Citigroup Inc. American Express Company Cooperative Bank Anglian Water Cornhill Direct Argos Coutts & Co. Arla Foods Plc Credit Suisse | First Boston ARM Holdings Plc D Asda De La Rue Plc AstraZeneca Plc Debenhams A.T Kearney Deloitte Touche Tohmatsu Limited Aviva Deutsche Bank AG B Deutsche Post DHL BAA DHL Bank of America Corporation Diageo Bank of England Dixons Group Bank of Scotland Plc Dresdner Kleinwort Wasserstein Bank Of Tokyo-Mitsubishi UFJ, Ltd E Bankers Trust Eli Lilly and Company Barclays Plc EMI Group BG Group Energis BOC Group Ericsson Telecom Boeing Commercial Airplanes Ernst & Young Boots UK Limited Experian Plc Boston Consulting Group Exxon Mobil Corp. BP Foundation F BP Plc Fidelity Investments LLC Bradford and Bingley FirstGroup Plc Bristol-Myers Squibb Ford Motor Company British Gas G British Sky Broadcasting Group Plc Gap, Inc. British American Tobacco Plc GlaxoSmithKline Plc BT Goldman Sachs Group, Inc. C Guardian Royal Exchange Cable & Wireless Communications H Philips Halifax Phoenix Group Home Retail Group PPG Industries HSBC Bank Plc PricewaterhouseCoopers HSBC Holdings Plc Proctor & Gamble Co. I R IBM Reuters IDEO Robert Fleming & Co. Industrial Bank of Japan Rolls Royce J Royal Bank of Scotland Group Plc J P Morgan & Co Royal Dutch Shell Plc J Sainsbury Plc Royal London Mutual Insurance Society Limited Johnson & Johnson RSA Insurance Group Plc JPMorgan Chase Bank RWE npower Plc K S Kellogg’s Santander Group Kingfisher Plc Santander UK Plc KPMG LLP Schneider Electric L Schroders Plc Legal & General Group Plc Seaboard Corp.