Index Guideline

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

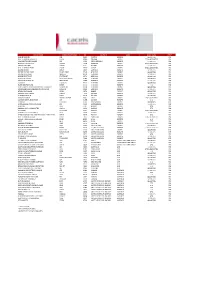

Execution Venues List

Execution Venues List This list should be read in conjunction with the Best Execution policy for Credit Suisse AG (excluding branches and subsidiaries), Credit Suisse (Switzerland) Ltd, Credit Suisse (Luxembourg) S.A, Credit Suisse (Luxembourg) S.A. Zweigniederlassung Österreichand, Neue Aargauer Bank AG published at www.credit-suisse.com/MiFID and https://www.credit-suisse.com/lu/en/private-banking/best-execution.html The Execution Venues1) shown enable the in scope legal entities to obtain on a consistent basis the best possible result for the execution of client orders. Accordingly, where the in scope legal entities may place significant reliance on these Execution Venues. Equity Cash & Exchange Traded Funds Country/Liquidity Pool Execution Venue1) Name MIC Code2) Regulated Markets & 3rd party exchanges Europe Austria Wiener Börse – Official Market WBAH Austria Wiener Börse – Securities Exchange XVIE Austria Wiener Börse XWBO Austria Wiener Börse Dritter Markt WBDM Belgium Euronext Brussels XBRU Belgium Euronext Growth Brussels ALXB Czech Republic Prague Stock Exchange XPRA Cyprus Cyprus Stock Exchange XCYS Denmark NASDAQ Copenhagen XCSE Estonia NASDAQ Tallinn XTAL Finland NASDAQ Helsinki XHEL France EURONEXT Paris XPAR France EURONEXT Growth Paris ALXP Germany Börse Berlin XBER Germany Börse Berlin – Equiduct Trading XEQT Germany Deutsche Börse XFRA Germany Börse Frankfurt Warrants XSCO Germany Börse Hamburg XHAM Germany Börse Düsseldorf XDUS Germany Börse München XMUN Germany Börse Stuttgart XSTU Germany Hannover Stock Exchange XHAN -

Representation Letter from Nasdaq Stockholm

Katten Paternoster House 65 St Paul's Churchyard London, EC4M SAB +44 (0) 20 7776 7620 tel +44 (0) 20 7776 7621 fax www.katten.co.uk [email protected] +44 (0) 20 7776 7625 direct January 15, 2020 Ref No. 385248 00020 CHJ:sh VIA E-MAIL AND FEDERAL EXPRESS Mr. Brett Redfeam Director U.S. Securities and Exchange Commission 100 F Street, NE Washington, D.C. 20549-7010 United States of America Re: Intent of Nasdaq Stockholm AB to Rely on No-Action Relief for Foreign Options Markets and Their Members That Engage in Familiarization Activities Dear Mr. Redfeam: At the request of our client, Nasdaq Stockholm AB ("Nasdaq"), we are writing to provide you with a notification of Nasdaq's intent to rely on the class no-action relief issued by the Securities and Exchange Commission's ("SEC" or "Commission") Division of Trading and Markets ("Division") for foreign options markets and their members that engage in familiarization activities with certain U.S.-based persons.1 BACKGROUND In the Class Relief, the Division took a no-action position under which a Foreign Options Market2, its Representatives3 and the Foreign Options Market's members, could engage in 1 See LIFFE A&M and Class Relief, SEC No-Action Letter (Jul. 1, 2013) ("Class Relief'). Capitalized terms used herein and not otherwise defined have the meanings given in the Class Relief. Pursuant to the Class Relief, a Foreign Options Market is not required to apply de novo for similar no-action or other relief; it can file with the Division a notice of intent to rely on the Class Relief. -

Zealand Pharma Increases Its Share Capital As a Consequence of Exercise of Employee Warrants

Company announcement – No. 26 / 2019 Zealand Pharma increases its share capital as a consequence of exercise of employee warrants Copenhagen, August 23, 2019 – Zealand Pharma A/S (“Zealand”) (NASDAQ: ZEAL) (CVR-no. 20 04 50 78), a Copenhagen-based biotechnology company focused on the discovery and development of innovative peptide-based medicines, has increased its share capital by a nominal amount of DKK 16,500 divided into 16,500 new shares with a nominal value of DKK 1 each. The increase is a consequence of the exercise of warrants granted under one of Zealand's employee warrant programs. Employee warrant programs are part of Zealand’s incentive scheme, and each warrant gives the owner the right to subscribe for one new Zealand share at a pre specified price, the exercise price, in specific predefined time periods before expiration. For a more detailed description of Zealand’s warrant programs, see the company’s Articles of Association, which are available on the website: www.zealandpharma.com. The exercise price was DKK 101.20 per share and the total proceeds to Zealand from the capital increase amount to DKK 1,669,800.00. The new shares give rights to dividend and other rights from the time of the warrant holder's exercise notice. Each new share carries one vote at Zealand’s general meetings. Zealand has only one class of shares. The new shares will be listed on Nasdaq Copenhagen after registration of the capital increase with the Danish Business Authority. Following registration of the new shares, the share capital of Zealand will be nominal DKK 31,831,290 divided into 31,831,290 shares with a nominal value of DKK 1 each. -

Final Report Amending ITS on Main Indices and Recognised Exchanges

Final Report Amendment to Commission Implementing Regulation (EU) 2016/1646 11 December 2019 | ESMA70-156-1535 Table of Contents 1 Executive Summary ....................................................................................................... 4 2 Introduction .................................................................................................................... 5 3 Main indices ................................................................................................................... 6 3.1 General approach ................................................................................................... 6 3.2 Analysis ................................................................................................................... 7 3.3 Conclusions............................................................................................................. 8 4 Recognised exchanges .................................................................................................. 9 4.1 General approach ................................................................................................... 9 4.2 Conclusions............................................................................................................. 9 4.2.1 Treatment of third-country exchanges .............................................................. 9 4.2.2 Impact of Brexit ...............................................................................................10 5 Annexes ........................................................................................................................12 -

Trifork Holding AG Listing on SIX Swiss Exchange Postponed

Company announcement no. 23 / 2021 Schindellegi, Switzerland – 23 June 2021 Trifork Holding AG Listing on SIX Swiss Exchange postponed On June 15, 2021, SIX Swiss Exchange granted Trifork approval to list the Trifork shares in accordance with the International Reporting Standard of SIX Swiss Exchange. As a consequence, Trifork after consulting our advisors and approval of our board on June 17 decided and announced the decision to list its shares on SIX Swiss Exchange as a dual listing following the successful IPO and listing on Nasdaq Copenhagen. The intention was to start trading as of 28 June 2021. Trifork has been informed by SIX Swiss Exchange that FINMA (Swiss Financial Market Supervisory Authority) considers applying the Ordinance on Trading of Swiss Equity Securities on Foreign Exchanges (Verordnung über die Anerkennung ausländischer Handelsplätze für den Handel mit Beteiligungspapieren von Gesellschaften mit Sitz in der Schweiz) issued in November 2018 which creates legal uncertainty. Trifork will seek to clarify the situation with the Swiss authorities before proceeding with a potential Swiss listing as Trifork remains fully committed to the existing listing and trading of its shares on Nasdaq Copenhagen. There will be no impact on the listing and trading of Trifork’s shares on Nasdaq Copenhagen. The Board of Directors will provide an update on the potential listing on SIX Swiss Exchange in due course. For further information, please contact: Investors Dan Dysli, Head of Investor Relations [email protected], +41 79 421 6299 Swiss Media Dynamics Group AG Philippe Blangey, Partner [email protected], +41 79 785 46 32 Danish Media Peter Rørsgaard, Trifork CMO [email protected], +45 2042 2494 About Trifork Trifork Group, headquartered in Schindellegi, Switzerland, with offices in 11 countries in Europe and North America, is an international IT group focusing on the development of innovative software solutions. -

Lieux Exécution 201904

VENUE NAME VENUE SHORTNAME MIC COUNTRY ZONE ASSET CLASS TYPE * WIENER BOERSE WB XWBO AUSTRIA EUROPE SECURITIES RM NYSE EURONEXT BRUSSELS ENXBE XBRU BELGIUM EUROPE ETD & SECURITIES RM PRAGUE STOCK EXCHANGE PSE XPRA CZECH REPUBLIC EUROPE SECURITIES RM NASDAQ COPENHAGEN OMX DK XCSE DENMARK EUROPE ETD & SECURITIES RM NASDAQ HELSINKI OMX FI XHEL FINLAND EUROPE SECURITIES RM NYSE EURONEXT PARIS ENXFR XPAR FRANCE EUROPE ETD & SECURITIES RM BOERSE BERLIN BERLIN XBER GERMANY EUROPE SECURITIES RM BOERSE DUESSELDORF DUSSELDORF XDUS GERMANY EUROPE SECURITIES RM BOERSE MUENCHEN MUNICH XMUN GERMANY EUROPE SECURITIES RM BOERSE STUTTGART STUTTGART XSTU GERMANY EUROPE SECURITIES RM DEUTSCHE BOERSE DEUTSCHE BOERSE XFRA GERMANY EUROPE SECURITIES RM DEUTSCHE BOERSE AG FRANCFORT XFRA GERMANY EUROPE SECURITIES RM EQUIDUCT EQUIDUCT XBER GERMANY EUROPE SECURITIES RM EUREX DEUTSCHLAND EUREX XEUR GERMANY EUROPE ETD RM HANSEATISCHE WERTPAPIERBOERSE HAMBURG HAMBOURG XHAM GERMANY EUROPE SECURITIES RM NIEDERSAECHSISCHE BOERSE ZU HANNOVER HANOVRE XHAN GERMANY EUROPE SECURITIES RM ATHENS EXCHANGE ATHEX XATH GREECE EUROPE SECURITIES RM NASDAQ OMX ICELAND OMX IC XICE ICELAND EUROPE SECURITIES RM EURONEXT DUBLIN ENXIE XDUB IRELAND EUROPE SECURITIES RM BORSA ITALIANA BORSA ITALIANA XMIL ITALY EUROPE ETD & SECURITIES RM LONDON METAL EXCHANGE LME XLME LONDON EUROPE ETD RM EURO MTF EURO MTF XLUX LUXEMBOURG EUROPE SECURITIES MTF LUXEMBOURG STOCK EXCHANGE BDL XLUX LUXEMBOURG EUROPE SECURITIES RM FISH POOL FISH FISH NORWAY EUROPE ETD RM NASDAQ OMX COMMODITIES OMX CO NORX NORWAY -

COVID-19 Could Push Another 100 Million People Into Extreme

WORLD MSCI WORLD INDEX MARKET S 0.33% ▲ Vikram Limaye CEO at Radical Uncertainty: Decision Black Sea & Eurasia Coun - India’s NSE Making Beyond the Numbers tries in the Spotlight “The markets don’t seem to be con - An informative, profound yet practical Politics, Economy, Capital Markets, nected with the ground reality and the book by leading economists John Central Bank Interest Rates, News uncertainty” (p.3) Kay and Marvyn King (p.5) & Data (p. 10-11) USA : The US election news cycle kicked into full gear MALI: The Malian president resigned on with the Democratic National Convention. Next week, Wednesday following a military coup. This is the Republican National Convention will take center stage. the country's second coup in less than 10 years. BELARUS: President Alexan - Oxfam report Dignity Not Destitution der Lukashenko won Belarus' presidential election two weeks ago as protests continue to E.Asia & Pacific 239.8m sweep the country. South Asia 128.8m M Latin America Carib. 54. 3m A F .6m X 47 O 5 : Meadle East & N.Africa 44.9m e c r u o Sub Saharan Africa 44.6m S Europe & C.Asia 30. 5m LYBIA: GNA Chief Fayez al-Sar - Other High Income 4. 7m raj ordered on Friday a ceasefire in Libya.The Eastern-based par - liament also called for an imme - “Economic stimulus packages must support ordinary workers and small businesses, and bail outs OXFAM: diate ceasefire. for big corporations must be conditional on action to build fairer, more sustainable economies” Jose Maria Vera, Oxfam International Interim Executive Director COVID-19 could push another 100 Million People into Extreme POVERTY p to 100 million people will be pushed into "ex - poverty, but the new estimate puts the deterioration at 70 treme poverty" by the coronavirus crisis, World to 100 million. -

Doing Data Differently

General Company Overview Doing data differently V.14.9. Company Overview Helping the global financial community make informed decisions through the provision of fast, accurate, timely and affordable reference data services With more than 20 years of experience, we offer comprehensive and complete securities reference and pricing data for equities, fixed income and derivative instruments around the globe. Our customers can rely on our successful track record to efficiently deliver high quality data sets including: § Worldwide Corporate Actions § Worldwide Fixed Income § Security Reference File § Worldwide End-of-Day Prices Exchange Data International has recently expanded its data coverage to include economic data. Currently it has three products: § African Economic Data www.africadata.com § Economic Indicator Service (EIS) § Global Economic Data Our professional sales, support and data/research teams deliver the lowest cost of ownership whilst at the same time being the most responsive to client requests. As a result of our on-going commitment to providing cost effective and innovative data solutions, whilst at the same time ensuring the highest standards, we have been awarded the internationally recognized symbol of quality ISO 9001. Headquartered in United Kingdom, we have staff in Canada, India, Morocco, South Africa and United States. www.exchange-data.com 2 Company Overview Contents Reference Data ............................................................................................................................................ -

Over 100 Exchanges Worldwide 'Ring the Bell for Gender Equality in 2021' with Women in Etfs and Five Partner Organizations

OVER 100 EXCHANGES WORLDWIDE 'RING THE BELL FOR GENDER EQUALITY IN 2021’ WITH WOMEN IN ETFS AND FIVE PARTNER ORGANIZATIONS Wednesday March 3, 2021, London – For the seventh consecutive year, a global collaboration across over 100 exchanges around the world plan to hold a bell ringing event to celebrate International Women’s Day 2021 (8 March 2020). The events - which start on Monday 1 March, and will last for two weeks - are a partnership between IFC, Sustainable Stock Exchanges (SSE) Initiative, UN Global Compact, UN Women, the World Federation of Exchanges and Women in ETFs, The UN Women’s theme for International Women’s Day 2021 - “Women in leadership: Achieving an equal future in a COVID-19 world ” celebrates the tremendous efforts by women and girls around the world in shaping a more equal future and recovery from the COVID-19 pandemic. Women leaders and women’s organizations have demonstrated their skills, knowledge and networks to effectively lead in COVID-19 response and recovery efforts. Today there is more recognition than ever before that women bring different experiences, perspectives and skills to the table, and make irreplaceable contributions to decisions, policies and laws that work better for all. Women in ETFs leadership globally are united in the view that “There is a natural synergy for Women in ETFs to celebrate International Women’s Day with bell ringings. Gender equality is central to driving the global economy and the private sector has an important role to play. Our mission is to create opportunities for professional development and advancement of women by expanding connections among women and men in the financial industry.” The list of exchanges and organisations that have registered to hold an in person or virtual bell ringing event are shown on the following pages. -

Execution Venues Equities and Fixed Income

UBS AG London Branch 5 Broadgate London EC2M 2QS United Kingdom UBS Europe SE OpernTurm Bockenheimer Landstraße 2-4 60306 Frankfurt am Main Germany www.ubs.com/ibterms Execution venues Equities and fixed income Version: December 2020 For information about our investment bank entities, visit www.ubs.com/ibterms Execution venues This is a non-exhaustive list of the main execution venues that we use outside UBS and our own systematic internalisers. We will review and update it from time to time in accordance with our UK and EEA MiFID Order Handling & Execution Policy. We may use other execution venues where appropriate. Equities Cash Equities Direct access Aquis Exchange Europe Aquis Exchange PlcAthens Stock Exchange BATS Europe, a CBOE Company Borsa Italiana CBOE NL CBOE UK Citadel Securities (Europe) Limited SI Deutsche Börse Group - Xetra Euronext Amsterdam Stock Exchange Euronext Brussels Stock Exchange Euronext Lisbon Stock Exchange Euronext Paris Stock Exchange Instinet Blockmatch Euronext DublinITG Posit London Stock Exchange Madrid Stock Exchange Nasdaq Copenhagen Nasdaq Helsinki Nasdaq Stockholm Oslo Bors Sigma X Europe Sigma X MTFTower Research Capital Europe Limited SI Turquoise Europe TurquoiseUBS Investment Bank UBS MTF Vienna Stock Exchange Virtu Financial Ireland Limited Warsaw Stock Exchange Via intermediate broker Budapest Stock Exchange Cairo & Alexandria Stock Exchange Deutsche Börse - Frankfurt Stock Exchange Istanbul Stock Exchange Johannesburg Stock Exchange Moscow Exchange Prague Stock Exchange SIX Swiss Exchange Tel Aviv Stock Exchange Structured Products Direct access Börse Frankfurt (Zertifikate Premium) Börse Stuttgart (EUWAX) Xetra SIX Swiss Exchange SeDeX Milan Euronext Amsterdam London Stock Exchange Madrid Stock Exchange NASDAQ OMX Stockholm JSE Johannesburg Stock Exchange OTC matching CATS-OS Fixed Income Cash bonds Via Bond Port Bloomberg EuroTLX Euronext ICE (KCG) BondPoint Market Axess MOT MTS BondsPro 1 © UBS 2020. -

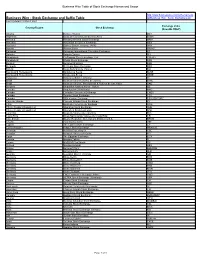

Stock Exchange and Suffix Table Ml/Business Wire Stock Exchanges.Pdf Last Updated 12 March 2021

Business Wire Table of Stock Exchange Names and Usage http://www.businesswire.com/schema/news Business Wire - Stock Exchange and Suffix Table ml/Business_Wire_Stock_Exchanges.pdf Last Updated 12 March 2021 Exchange Value Country/Region Stock Exchange (NewsML ONLY) Albania Bursa e Tiranës BET Argentina Bolsa de Comercio de Buenos Aires BCBA Armenia Nasdaq Armenia Stock Exchange ARM Australia Australian Securities Exchange ASX Australia Sydney Stock Exchange (APX) APX Austria Wiener Börse WBAG Bahamas Bahamas International Securities Exchange BS Bahrain Bahrain Bourse BH Bangladesh Chittagong Stock Exchange, Ltd. CSEBD Bangladesh Dhaka Stock Exchange DSE Belgium Euronext Brussels BSE Bermuda Bermuda Stock Exchange BSX Bolivia Bolsa Boliviana de Valores BO Bosnia and Herzegovina Banjalucka Berza BLSE Bosnia and Herzegovina Sarajevska Berza SASE Botswana Botswana Stock Exchange BT Brazil Bolsa de Valores do Rio de Janeiro BVRJ Brazil Bolsa de Valores, Mercadorias & Futuros de Sao Paulo SAO Bulgaria Balgarska fondova borsa - Sofiya BB Canada Aequitas NEO Exchange NEO Canada Canadian Securities Exchange CNSX Canada Toronto Stock Exchange TSX Canada TSX Venture Exchange TSX VENTURE Cayman Islands Cayman Islands Stock Exchange KY Chile Bolsa de Comercio de Santiago SGO China, People's Republic of Shanghai Stock Exchange SHH China, People's Republic of Shenzhen Stock Exchange SHZ Colombia Bolsa de Valores de Colombia BVC Costa Rica Bolsa Nacional de Valores de Costa Rica CR Cote d'Ivoire Bourse Regionale Des Valeurs Mobilieres S.A. BRVM Croatia -

Northern Trust Emea Order Execution Policy

NORTHERN TRUST EMEA ORDER EXECUTION POLICY For Professional Clients of the following Northern Trust entities: • Northern Trust Global Services SE, and its branches • Northern Trust Securities LLP, and its branches • The Northern Trust Company, London branch Publication date: 1 January 2021 Contents INTRODUCTION .................................................................................................................................................................... 3 A. Purpose of this policy .................................................................................................................................................................................... 3 B. What is Best Execution? ............................................................................................................................................................................... 3 POLICY SCOPE ..................................................................................................................................................................... 4 A. Northern Trust entities subject to this Policy ................................................................................................................................................. 4 B. Types of Clients ............................................................................................................................................................................................. 4 C. Activities .......................................................................................................................................................................................................