Oshkosh Corporation

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

OSB Representative Participant List by Industry

OSB Representative Participant List by Industry Aerospace • KAWASAKI • VOLVO • CATERPILLAR • ADVANCED COATING • KEDDEG COMPANY • XI'AN AIRCRAFT INDUSTRY • CHINA FAW GROUP TECHNOLOGIES GROUP • KOREAN AIRLINES • CHINA INTERNATIONAL Agriculture • AIRBUS MARINE CONTAINERS • L3 COMMUNICATIONS • AIRCELLE • AGRICOLA FORNACE • CHRYSLER • LOCKHEED MARTIN • ALLIANT TECHSYSTEMS • CARGILL • COMMERCIAL VEHICLE • M7 AEROSPACE GROUP • AVICHINA • E. RITTER & COMPANY • • MESSIER-BUGATTI- CONTINENTAL AIRLINES • BAE SYSTEMS • EXOPLAST DOWTY • CONTINENTAL • BE AEROSPACE • MITSUBISHI HEAVY • JOHN DEERE AUTOMOTIVE INDUSTRIES • • BELL HELICOPTER • MAUI PINEAPPLE CONTINENTAL • NASA COMPANY AUTOMOTIVE SYSTEMS • BOMBARDIER • • NGC INTEGRATED • USDA COOPER-STANDARD • CAE SYSTEMS AUTOMOTIVE Automotive • • CORNING • CESSNA AIRCRAFT NORTHROP GRUMMAN • AGCO • COMPANY • PRECISION CASTPARTS COSMA INDUSTRIAL DO • COBHAM CORP. • ALLIED SPECIALTY BRASIL • VEHICLES • CRP INDUSTRIES • COMAC RAYTHEON • AMSTED INDUSTRIES • • CUMMINS • DANAHER RAYTHEON E-SYSTEMS • ANHUI JIANGHUAI • • DAF TRUCKS • DASSAULT AVIATION RAYTHEON MISSLE AUTOMOBILE SYSTEMS COMPANY • • ARVINMERITOR DAIHATSU MOTOR • EATON • RAYTHEON NCS • • ASHOK LEYLAND DAIMLER • EMBRAER • RAYTHEON RMS • • ATC LOGISTICS & DALPHI METAL ESPANA • EUROPEAN AERONAUTIC • ROLLS-ROYCE DEFENCE AND SPACE ELECTRONICS • DANA HOLDING COMPANY • ROTORCRAFT • AUDI CORPORATION • FINMECCANICA ENTERPRISES • • AUTOZONE DANA INDÚSTRIAS • SAAB • FLIR SYSTEMS • • BAE SYSTEMS DELPHI • SMITH'S DETECTION • FUJI • • BECK/ARNLEY DENSO CORPORATION -

JLG 10 MSP.Qxd:Layout 1 27/3/08 10:55 Page 1

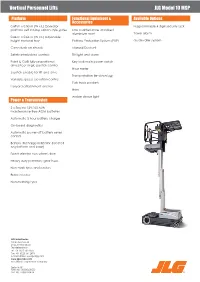

JLG 10 MSP.qxd:Layout 1 27/3/08 10:55 Page 1 Vertical Personnel Lifts JLG Model 10 MSP Platform Functional Equipment & Available Options Accessories 0.69 m x 0.50 m (W x L) Operator Programmable 4 digit security lock platform self closing saloon style gates Low maintenance anodised aluminium mast Travel alarm 0.66 m x 0.66 m (W x L) Adjustable height material tray Pothole Protection System (PHP) Guide roller system Carry deck on chassis Manual Descent Safety interlocked controls Tilt light and alarm Point & Go® fully proportional Key lock main power switch drive/steer single joystick control Hour meter Joystick enable for lift and drive Transportation tie-down lugs Variable speed elevation control Fork truck pockets Lanyard attachment anchor Horn Amber strobe light Power & Transmission 2 x Sealed 12V,100 A/Hr maintenance-free AGM batteries Automatic 5 hour battery charger On-board diagnostics Automatic power-off battery saver control Battery discharge indicator (located on platform and base) Direct electric two wheel drive Heavy duty planetary gear hubs Non mark tyres and casters Brake release Non-marking tyres JLG Industries Inc. Polaris Avenue 63 2132 JH Hoofddorp The Netherlands Tel: +31 (0)23 565 5665 Fax: +31 (0)23 557 2493 e-mail address: [email protected] www.jlgeurope.com An Oshkosh Corporation Company Printed in UK FORM No.: DS003-0208-500 PART NO.: DS003-ENGLISH JLG 10 MSP.qxd:Layout 1 27/3/08 10:55 Page 2 Vertical Personnel Lifts JLG Model 10 MSP 10MSP Working height 5.05 m Platform height 3.05 m Operator platform capacity 160 -

Page 1 of 32 VEHICLE RECALLS by MANUFACTURER, 2000 Report Prepared 1/16/2008

Page 1 of 32 VEHICLE RECALLS BY MANUFACTURER, 2000 Report Prepared 1/16/2008 MANUFACTURER RECALLS VEHICLES ACCUBUIL T, INC 1 8 AM GENERAL CORPORATION 1 980 AMERICAN EAGLE MOTORCYCLE CO 1 14 AMERICAN HONDA MOTOR CO 8 212,212 AMERICAN SUNDIRO MOTORCYCLE 1 2,183 AMERICAN SUZUKI MOTOR CORP. 4 25,023 AMERICAN TRANSPORTATION CORP. 5 1,441 APRILIA USA INC. 2 409 ASTON MARTIN 2 666 ATHEY PRODUCTS CORP. 3 304 B. FOSTER & COMPANY, INC. 1 422 BAYERISCHE MOTOREN WERKE 11 28,738 BLUE BIRD BODY COMPANY 12 62,692 BUELL MOTORCYCLE CO 4 12,230 CABOT COACH BUILDERS, INC. 1 818 CARPENTER INDUSTRIES, INC. 2 6,838 CLASSIC LIMOUSINE 1 492 CLASSIC MANUFACTURING, INC. 1 8 COACHMEN INDUSTRIES, INC. 8 5,271 COACHMEN RV COMPANY 1 576 COLLINS BUS CORPORATION 1 286 COUNTRY COACH INC 6 519 CRANE CARRIER COMPANY 1 138 DABRYAN COACH BUILDERS 1 723 DAIMLERCHRYSLER CORPORATION 30 6,700,752 DAMON CORPORATION 3 824 DAVINCI COACHWORKS, INC 1 144 D'ELEGANT CONVERSIONS, INC. 1 34 DORSEY TRAILERS, INC. 1 210 DUTCHMEN MANUFACTURING, INC 1 105 ELDORADO NATIONAL 1 173 ELECTRIC TRANSIT, INC. 1 54 ELGIN SWEEPER COMPANY 1 40 E-ONE, INC. 1 3 EUROPA INTERNATIONAL, INC. 2 242 EXECUTIVE COACH BUILDERS 1 702 FEATHERLITE LUXURY COACHES 1 83 FEATHERLITE, INC. 2 3,235 FEDERAL COACH, LLC 1 230 FERRARI NORTH AMERICA 8 1,601 FLEETWOOD ENT., INC. 5 12, 119 FORD MOTOR COMPANY 60 7,485,466 FOREST RIVER, INC. 1 115 FORETRAVEL, INC. 3 478 FOURWINNS 2 2,276 FREIGHTLINER CORPORATION 27 233,032 FREIGHTLINER LLC 1 803 GENERAL MOTORS CORP. -

Oshkosh Corporation

AT-A-GLANCE Oshkosh Corporation is a leading designer, The top priorities of our 13,800 team members manufacturer and marketer of a broad range are to serve and delight our customers as well of access equipment, specialty military, fire & as drive superior operating performance to emergency and commercial vehicles and vehicle benefit our shareholders. We do this through bodies. Our products are valued worldwide by rental execution of our MOVE strategy and by leveraging companies, defense forces, concrete placement our strengths and resources in engineering, and refuse businesses, fire & emergency departments manufacturing, purchasing and distribution and municipal and airport services, where high across our four business segments. quality, superior performance, rugged reliability and long-term value are paramount. Approximately 24% of our revenues came from outside the United States in fiscal 2016 and we We partner with our customers to deliver superior have manufacturing operations in eight U.S. states solutions that safely and efficiently move people and in Australia, Belgium, Canada, China, France, and materials at work, around the globe and around Mexico, Romania and the United Kingdom as well the clock. as operations to support sales or deliver service in over 150 countries. We believe our business model makes us a different integrated global industrial and supports our Our company was founded in 1917 and we look goals of driving superior value for both customers forward to celebrating our 100th anniversary in and shareholders. Our business model brings 2017. We are proud of our strong culture and together a unique set of integrated capabilities and operating performance that contribute to our diverse end markets to position our company to be positive outlook as we prepare to celebrate 100 successful in a variety of economic environments. -

2016–2017 First Destination Study

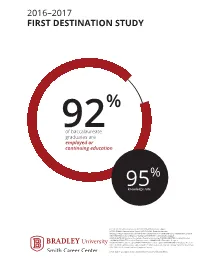

2016–2017 FIRST DESTINATION STUDY % 92of baccalaureate graduates are employed or continuing education % 95knowledge rate JOE BATTELLINE–Associate Director JUDY BROWN–Administrative Support JESSICA CURRAN–Administrative Support JESSICA DEPKE–Graduate Assistant KRYSTLE DORSEY–Assistant Director KIM DUNN–Assistant Director HANNAH GODSIL–Administrative Support KEN HARDING–Director of Employer Testing LISA HINTHORN–Administrative Support DAWN KOELTZOW–Director of the Springer Center for Internships CARMEN KREMITZKI–Assistant Director SANDRA MCDERMOTT–Director of Employer Services AMANDA MELLEY–Graphic Designer DYLAN PASHKE–Graphic Designer JANET PESEK–Administrative Support HANNAH RAMLO–Graduate Assistant KIRSTEN RINGEL–Administrative Support DAVID SCHWARTZ–Assistant Director, Springer Center for Internships RICK SMITH, PH.D.–Senior Director of Employer Services JON C. NEIDY - Executive Director, Assistant Vice President of Student Affairs 2016–2017 BACCALAUREATE GRADUATES FIRST DESTINATION STUDY EXECUTIVE SUMMARY 13% 78% continuing education employed 9% still seeking baccalaureate graduates participated used the services knowledge in experiential of Smith Career 1,117 of 1,065 96% learning 96% Center 576 EMPLOYERS hired our ‘16–’17 across 30 states and 5 countries baccalaureate graduates 2016–2017 BACCALAUREATE GRADUATES 85% 7% 8% 20 40 60 80 $29,120–$110,000 FOSTER % salary offers range COLLEGE 45% OF BUSINESS 92 salaries reported career outcomes 96% 72% 11% 17% $20,000–$58,600 SLANE salary offers range COLLEGE OF 25% COMMUNICATIONS % salaries -

UNITED STATES SECURITIES and EXCHANGE COMMISSION Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION Washington, D.C. 20549 SCHEDULE 14A Proxy Statement Pursuant to Section 14(a) of the Securities Exchange Act of 1934 (Amendment No. ) Filed by the Registrant x Filed by a Party other than the Registrant o Check the appropriate box: o Preliminary Proxy Statement o Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) x Definitive Proxy Statement o Definitive Additional Materials o Soliciting Material under §240.14a-12 Oshkosh Corporation (Name of Registrant as Specified In Its Charter) (Name of Person(s) Filing Proxy Statement, if other than the Registrant) Payment of Filing Fee (Check the appropriate box): x No fee required. o Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. (1) Title of each class of securities to which transaction applies: (2) Aggregate number of securities to which transaction applies: (3) Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): (4) Proposed maximum aggregate value of transaction: (5) Total fee paid: o Fee paid previously with preliminary materials. o Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. (1) Amount Previously Paid: (2) Form, Schedule -

Oshkosh Corporation Incoming Letter Dated September 20, 2016

November 4, 2016 Marc S. Gerber Skadden, Arps, Slate, Meagher & Flom LLP [email protected] Re: Oshkosh Corporation Incoming letter dated September 20, 2016 Dear Mr. Gerber: This is in response to your letter dated September 20, 2016 concerning the shareholder proposal submitted to Oshkosh by John Chevedden. Copies of all of the correspondence on which this response is based will be made available on our website at http://www.sec.gov/divisions/corpfin/cf-noaction/14a-8.shtml. For your reference, a brief discussion of the Division’s informal procedures regarding shareholder proposals is also available at the same website address. Sincerely, Matt S. McNair Senior Special Counsel Enclosure cc: John Chevedden ***FISMA & OMB Memorandum M-07-16*** November 4, 2016 Response of the Office of Chief Counsel Division of Corporation Finance Re: Oshkosh Corporation Incoming letter dated September 20, 2016 The proposal asks the board to amend certain provisions of the company’s proxy access bylaw in the manner specified in the proposal. There appears to be some basis for your view that Oshkosh may exclude the proposal under rule 14a-8(i)(10). Based on the information you have presented, it appears that Oshkosh’s policies, practices and procedures compare favorably with the guidelines of the proposal and that Oshkosh has, therefore, substantially implemented the proposal. Accordingly, we will not recommend enforcement action to the Commission if Oshkosh omits the proposal from its proxy materials in reliance on rule 14a-8(i)(10). Sincerely, Evan S. Jacobson Special Counsel DIVISION OF CORPORATION FINANCE INFORMAL PROCEDURES REGARDING SHAREHOLDER PROPOSALS The Division of Corporation Finance believes that its responsibility with respect to matters arising under Rule 14a-8 [17 CFR 240.14a-8], as with other matters under the proxy rules, is to aid those who must comply with the rule by offering informal advice and suggestions and to determine, initially, whether or not it may be appropriate in a particular matter to recommend enforcement action to the Commission. -

Oshkosh Defense Overview

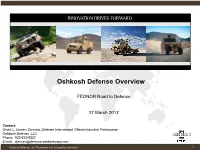

INNOVATION DRIVES FORWARD Oshkosh Defense Overview FEDNOR Road to Defence 27 March 2017 Contact: David L. Jensen, Director, Defense International Offsets/Industrial Participation Oshkosh Defense, LLC Phone: 920-233-9227 E-mail:Company [email protected] Confidential Oshkosh Defense, LLC Proprietary and Competition Sensitive 1 Oshkosh Corporation Today Established: 1917 FY15 Sales: $6.1 billion Fortune Ranking: 394 Headquarters: Oshkosh, Wisconsin Operations: Our Mission: To partner with customers to Manufacturing in seven countries deliver superior solutions that safely and Service centers in 23 countries efficiently move people and materials at work, around the globe and around the clock Six new product development facilities Employees: 12,000+ Customer Reach: 130 countries NYSE: OSK Company Confidential Oshkosh Defense, LLC Proprietary and Competition Sensitive 2 A Family of Industry Leading Brands Pierce Manufacturing (1996) Jerr-Dan Corporation (2004) Nova Quintech (1997) CON-E-CO (2005) McNeilus Companies (1998) London Machinery Inc. (2005) Kewaunee Fabrications (1999) AK Specialty Vehicles (2006) Viking Truck & Equipment (1999) Iowa Mold Tooling (IMT) (2006) TEMCO (2001) JLG Industries (2006) TRANSFORMING OSHKOSH INTO A GLOBAL INDUSTRIAL 3 Company Confidential Oshkosh Defense, LLC Proprietary and Competition Sensitive 3 Working Together to Move the World at Work Values, Mission, MOVE Strategy Oshkosh Operating System Company Confidential Oshkosh Defense, LLC Proprietary and Competition Sensitive 4 Oshkosh Corporation -

Pierce Saber/Enforcer Operator's Manual

Saber®/Enforcer™ Operator’s Manual Operator’s © 2018 Pierce Manufacturing Inc. Part No. PM-C-OM014-SEN-0718 TABLE OF CONTENTS CHAPTER 1. FOREWORD To the Owner and Operator 1-1 WHO SHOULD USE, SERVICE, AND MAINTAIN THIS VEHICLE .......................................................................... 1-1 1-2 VEHICLE IDENTIFICATION .............................................................................................................................. 1-3 1-3 CUSTOMER ASSISTANCE INFORMATION ......................................................................................................... 1-4 1-4 RESPONSIBILITY ........................................................................................................................................... 1-4 1-5 PROFESSIONAL, TRAINING, AND STANDARDS ORGANIZATIONS ....................................................................... 1-5 CHAPTER 2. SAFETY Safety and Responsibility 2-1 WARNINGS AND CAUTIONS ........................................................................................................................... 2-1 2-1.1 WARNING AND CAUTION STATEMENTS ............................................................................................. 2-1 2-1.2 GENERAL WARNINGS AND CAUTIONS .............................................................................................. 2-2 2-1.3 SAFETY WARNING LABELS ............................................................................................................... 2-2 2-2 BACKING THE VEHICLE ................................................................................................................................ -

2009 Annual Report

2009 Annual Report National Fallen Firefighters F o u n d a t i o n Who We Are The U. S. Congress created the non- profit National Fallen Firefighters Foundation in 1992 with the mission to honor fallen firefighters and to assist their survivors in the rebuilding of their lives. Since its inception, the Foundation has de- veloped many programs to fulfill this Table of Contents mandate. Who We Are 1 The Foundation is a 501(c)(3) nonprofit What We Do 1 organization, located in Emmitsburg, Mary- How We Do it 2 land, and registered as a corporation in the Board of Directors 10 State of Maryland. Grants and donations from Who Helps Us 11 individuals, organizations, corporations, and Appendix foundations fund many of the Foun- NFFF Financial Position 13 NFFF Statement of Activity 14 dation’s programs. What We Do The United States Congress chartered the Foundation and a website; in 1992 and established a number of objectives deemed necessary for the Foundation to carry out its mission. • Plan, direct, and manage the National Fallen Firefight- In subsequent years, Congress has added to those ini- ers Memorial Service and related activities in coor- tial objectives. dination with the Federal Government, fire service organizations, and survivors of fallen firefighters; During 2009, the Foundation worked to fulfill the pur- poses set forth in Public Law 102-522, as amended • Provide financial assistance to families of fallen fire- and codified into United States Code Title 36, Section fighters for transportation, lodging, and meals during 151302. -

Opportunities Targeted to the People You Want to Meet and the Visibility to Grow Your Brand

Opportunities targeted to the people you want to meet and the visibility to grow your brand. • • • • • • • • • • 3M Company Electromed Inc. MGC Diagnostics Corporation Spectrum Brands Holdings, Inc. ASK LLP A. O. Smith Corporation EMC Insurance Group Inc. MOCON, Inc. SS&C Technologies Holdings, Inc. Ballard Spahr, LLP (Lindquist & Vennum) Allete Inc. EnteroMedics Inc. Moody's (formerly Advent Software) BlackRock, Inc. Alliant Energy Corporation Evolving Systems, Inc. Mosaic Co. St. Jude Medical, Inc. Bloomberg L.P. Ameriprise Financial, Inc. Famous Dave’s of America MTS Systems Corporation Stamps.com Inc. BNY Mellon Brand Advantage Group Apogee Enterprises, Inc. Fastenal Company Multiband Corp. Steelcase Broadridge Financial Solutions, Inc. Arctic Cat Inc. FBL Financial Group, Inc. Navarre Stratasys, Ltd. Business Wire Sunshine Heart Inc Associated Bank FHLBanks Office of Finance New Jersey Resources Corporation CFA Institute SUPERVALU Inc. AstraZeneca plc FICO Northern Oil & Gas, Inc. Curran & Connors AxoGen, Inc. First Business NorthWestern Energy Corp SurModics, Inc. Deluxe Corporation Bemis Company, Inc. Financial Services, Inc. NVE Corporation Target Corporation Drexel Hamilton, LLC Best Buy, Co., Inc. FLUX Power Holdings, Inc. OneBeacon Insurance Group TCF Financial Corporation EQS Group Bio-Techne Corporation G&K Services, Inc. Orion Engineered Carbons S.A. Tennant Company FactSet Research Systems Inc. Black Hills Corp. General Mills, Inc. Oshkosh Corporation Tetraphase Pharmaceuticals, Inc. Federal Reserve Bank of Minneapolis Boston Scientific Corporation Graco, Inc. OSI Systems, Inc. The Toro Company Inspired Investment Leadership: Objective Measure Conference Buffalo Wild Wings, Inc. H.B. Fuller Company Otter Tail Corporation Tile Shop Holdings Inc Intrinsic Research Systems Inc. C.H. Robinson Worldwide, Inc. Heartland Financial USA, Inc. -

2019 Annual Report Statement of Company Business Stockholders’ Information

2019 ANNUAL REPORT STATEMENT OF COMPANY BUSINESS STOCKHOLDERS’ INFORMATION PACCAR is a global technology company that designs and manufactures premium quality light, medium and heavy duty commercial vehicles sold worldwide under Corporate Offices Stock Transfer Trademarks Owned by PACCAR Building and Dividend PACCAR Inc and its 777 106th Avenue N.E. Dispersing Agent Subsidiaries the Kenworth, Peterbilt and DAF nameplates. PACCAR designs and manufactures Bellevue, Washington Equiniti Trust Company DAF, EPIQ, Kenmex, 98004 Shareowner Services Kenworth, Leyland, diesel engines and other powertrain components for use in its own products and for P.O. Box 64854 PACCAR, PACCAR MX-11, Mailing Address St. Paul, Minnesota PACCAR MX-13, PACCAR P.O. Box 1518 55164-0854 PX, PacFuel, PacLease, sale to third party manufacturers of trucks and buses. PACCAR distributes Bellevue, Washington 800.468.9716 PacLink, PacTax, PacTrac, 98009 www.shareowneronline.com PacTrainer, Peterbilt, aftermarket truck parts to its dealers through a worldwide network of Parts The World’s Best, TRP, Telephone PACCAR’s transfer agent TruckTech+, SmartNav, and 425.468.7400 maintains the company’s SmartLINQ Distribution Centers. Finance and leasing subsidiaries facilitate the sale of shareholder records, issues Facsimile stock certificates and Independent Auditors PACCAR products in many countries worldwide. PACCAR manufactures and 425.468.8216 distributes dividends and Ernst & Young LLP IRS Forms 1099. Requests Seattle, Washington Website concerning these matters markets industrial