Regulatory Competition and the E Ciency of Alternative Derivative Product Margining Systems

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Here We Go Again

2015, 2016 MDDC News Organization of the Year! Celebrating 161 years of service! Vol. 163, No. 3 • 50¢ SINCE 1855 July 13 - July 19, 2017 TODAY’S GAS Here we go again . PRICE Rockville political differences rise to the surface in routine commission appointment $2.28 per gallon Last Week pointee to the City’s Historic District the three members of “Team him from serving on the HDC. $2.26 per gallon By Neal Earley @neal_earley Commission turned into a heated de- Rockville,” a Rockville political- The HDC is responsible for re- bate highlighting the City’s main po- block made up of Council members viewing applications for modification A month ago ROCKVILLE – In most jurisdic- litical division. Julie Palakovich Carr, Mark Pierzcha- to the exteriors of historic buildings, $2.36 per gallon tions, board and commission appoint- Mayor Bridget Donnell Newton la and Virginia Onley who ran on the as well as recommending boundaries A year ago ments are usually toward the bottom called the City Council’s rejection of same platform with mayoral candi- for the City’s historic districts. If ap- $2.28 per gallon of the list in terms of public interest her pick for Historic District Commis- date Sima Osdoby and city council proved Giammo, would have re- and controversy -- but not in sion – former three-term Rockville candidate Clark Reed. placed Matthew Goguen, whose term AVERAGE PRICE PER GALLON OF Rockville. UNLEADED REGULAR GAS IN Mayor Larry Giammo – political. While Onley and Palakovich expired in May. MARYLAND/D.C. METRO AREA For many municipalities, may- “I find it absolutely disappoint- Carr said they opposed Giammo’s ap- Giammo previously endorsed ACCORDING TO AAA oral appointments are a formality of- ing that politics has entered into the pointment based on his lack of qualifi- Newton in her campaign against ten given rubberstamped approval by boards and commission nomination cations, Giammo said it was his polit- INSIDE the city council, but in Rockville what process once again,” Newton said. -

Up to EUR 3,500,000.00 7% Fixed Rate Bonds Due 6 April 2026 ISIN

Up to EUR 3,500,000.00 7% Fixed Rate Bonds due 6 April 2026 ISIN IT0005440976 Terms and Conditions Executed by EPizza S.p.A. 4126-6190-7500.7 This Terms and Conditions are dated 6 April 2021. EPizza S.p.A., a company limited by shares incorporated in Italy as a società per azioni, whose registered office is at Piazza Castello n. 19, 20123 Milan, Italy, enrolled with the companies’ register of Milan-Monza-Brianza- Lodi under No. and fiscal code No. 08950850969, VAT No. 08950850969 (the “Issuer”). *** The issue of up to EUR 3,500,000.00 (three million and five hundred thousand /00) 7% (seven per cent.) fixed rate bonds due 6 April 2026 (the “Bonds”) was authorised by the Board of Directors of the Issuer, by exercising the powers conferred to it by the Articles (as defined below), through a resolution passed on 26 March 2021. The Bonds shall be issued and held subject to and with the benefit of the provisions of this Terms and Conditions. All such provisions shall be binding on the Issuer, the Bondholders (and their successors in title) and all Persons claiming through or under them and shall endure for the benefit of the Bondholders (and their successors in title). The Bondholders (and their successors in title) are deemed to have notice of all the provisions of this Terms and Conditions and the Articles. Copies of each of the Articles and this Terms and Conditions are available for inspection during normal business hours at the registered office for the time being of the Issuer being, as at the date of this Terms and Conditions, at Piazza Castello n. -

Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field?

Fortune pgs 31-50 1/6/04 8:21 PM Page 31 Margin Requirements Across Equity-Related Instruments: How Level Is the Playing Field? hen interest rates rose sharply in 1994, a number of derivatives- related failures occurred, prominent among them the bankrupt- cy of Orange County, California, which had invested heavily in W 1 structured notes called “inverse floaters.” These events led to vigorous public discussion about the links between derivative securities and finan- cial stability, as well as about the potential role of new regulation. In an effort to clarify the issues, the Federal Reserve Bank of Boston sponsored an educational forum in which the risks and risk management of deriva- tive securities were discussed by a range of interested parties: academics; lawmakers and regulators; experts from nonfinancial corporations, investment and commercial banks, and pension funds; and issuers of securities. The Bank published a summary of the presentations in Minehan and Simons (1995). In the keynote address, Harvard Business School Professor Jay Light noted that there are at least 11 ways that investors can participate in the returns on the Standard and Poor’s 500 composite index (see Box 1). Professor Light pointed out that these alternatives exist because they dif- Peter Fortune fer in a variety of important respects: Some carry higher transaction costs; others might have higher margin requirements; still others might differ in tax treatment or in regulatory restraints. The author is Senior Economist and The purpose of the present study is to assess one dimension of those Advisor to the Director of Research at differences—margin requirements. -

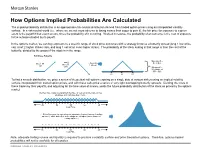

How Options Implied Probabilities Are Calculated

No content left No content right of this line of this line How Options Implied Probabilities Are Calculated The implied probability distribution is an approximate risk-neutral distribution derived from traded option prices using an interpolated volatility surface. In a risk-neutral world (i.e., where we are not more adverse to losing money than eager to gain it), the fair price for exposure to a given event is the payoff if that event occurs, times the probability of it occurring. Worked in reverse, the probability of an outcome is the cost of exposure Place content to the outcome divided by its payoff. Place content below this line below this line In the options market, we can buy exposure to a specific range of stock price outcomes with a strategy know as a butterfly spread (long 1 low strike call, short 2 higher strikes calls, and long 1 call at an even higher strike). The probability of the stock ending in that range is then the cost of the butterfly, divided by the payout if the stock is in the range. Building a Butterfly: Max payoff = …add 2 …then Buy $5 at $55 Buy 1 50 short 55 call 1 60 call calls Min payoff = $0 outside of $50 - $60 50 55 60 To find a smooth distribution, we price a series of theoretical call options expiring on a single date at various strikes using an implied volatility surface interpolated from traded option prices, and with these calls price a series of very tight overlapping butterfly spreads. Dividing the costs of these trades by their payoffs, and adjusting for the time value of money, yields the future probability distribution of the stock as priced by the options market. -

Margin Requirements and Equity Option Returns∗

Margin Requirements and Equity Option Returns∗ Steffen Hitzemann† Michael Hofmann‡ Marliese Uhrig-Homburg§ Christian Wagner¶ December 2017 Abstract In equity option markets, traders face margin requirements both for the options them- selves and for hedging-related positions in the underlying stock market. We show that these requirements carry a significant margin premium in the cross-section of equity option returns. The sign of the margin premium depends on demand pressure: If end-users are on the long side of the market, option returns decrease with margins, while they increase otherwise. Our results are statistically and economically significant and robust to different margin specifications and various control variables. We explain our findings by a model of funding-constrained derivatives dealers that require compensation for satisfying end-users’ option demand. Keywords: equity options, margins, funding liquidity, cross-section of option returns JEL Classification: G12, G13 ∗We thank Hameed Allaudeen, Mario Bellia, Jie Cao, Zhi Da, Matt Darst, Maxym Dedov, Bjørn Eraker, Andrea Frazzini, Ruslan Goyenko, Guanglian Hu, Hendrik Hülsbusch, Kris Jacobs, Stefan Kanne, Olaf Korn, Dmitriy Muravyev, Lasse Pedersen, Matthias Pelster, Oleg Rytchkov, Ivan Shaliastovich, as well as participants of the 2017 EFA Annual Meeting, the SFS Cavalcade North America 2017, the 2017 MFA Annual Meeting, the SGF Conference 2017, the Conference on the Econometrics of Financial Markets, the 2016 Annual Meeting of the German Finance Association, the Paris December 2016 Finance Meeting, and seminar participants at the Center for Financial Frictions at Copenhagen Business School, the CUHK Business School, the University of Gothenburg, and the University of Wisconsin-Madison for valuable discussions and helpful comments and suggestions. -

A Practitioner's Guide to Structuring Listed Equity Derivative Securities

21 A Practitioner’s Guide to Structuring Listed Equity Derivative Securities JOHN C. BRADDOCK, MBA Executive Director–Investments CIBC Oppenheimer A Division of CIBC World Markets Corp., New York BENJAMIN D. KRAUSE, LLB Senior Vice President Capital Markets Division Chicago Board Options Exchange, New York Office INTRODUCTION Since the mid-1980s, “financial engineers” have created a wide array of instru- ments for use by professional investors in their search for higher returns and lower risks. Institutional investors are typically the most voracious consumers of structured derivative financial products, however, retail investors are increasingly availing themselves of such products through public, exchange- listed offerings. Design and engineering lie at the heart of the market for equity derivative securities. Through the use of computerized pricing and val- uation technology and instantaneous worldwide communications, today’s financial engineers are able to create new and varied instruments that address day-to-day client needs. This in turn has encouraged the development of new financial products that have broad investor appeal, many of which qualify for listing and trading on the principal securities markets. Commonly referred to as listed equity derivatives because they are listed on stock exchanges and trade under equity rules, these new financial products fuse disparate invest- ment features into single instruments that enable retail investors to replicate both speculative and risk management strategies employed by investment pro- fessionals. Options on individual common stocks are the forerunners of many of today’s publicly traded equity derivative products. They have been part of the 434 GUIDE TO STRUCTURING LISTED EQUITY DERIVATIVE SECURITIES securities landscape since the early 1970s.1 The notion of equity derivatives as a distinct class of securities, however, did not begin to solidify until the late 1980s. -

Tax Treatment of Derivatives

United States Viva Hammer* Tax Treatment of Derivatives 1. Introduction instruments, as well as principles of general applicability. Often, the nature of the derivative instrument will dictate The US federal income taxation of derivative instruments whether it is taxed as a capital asset or an ordinary asset is determined under numerous tax rules set forth in the US (see discussion of section 1256 contracts, below). In other tax code, the regulations thereunder (and supplemented instances, the nature of the taxpayer will dictate whether it by various forms of published and unpublished guidance is taxed as a capital asset or an ordinary asset (see discus- from the US tax authorities and by the case law).1 These tax sion of dealers versus traders, below). rules dictate the US federal income taxation of derivative instruments without regard to applicable accounting rules. Generally, the starting point will be to determine whether the instrument is a “capital asset” or an “ordinary asset” The tax rules applicable to derivative instruments have in the hands of the taxpayer. Section 1221 defines “capital developed over time in piecemeal fashion. There are no assets” by exclusion – unless an asset falls within one of general principles governing the taxation of derivatives eight enumerated exceptions, it is viewed as a capital asset. in the United States. Every transaction must be examined Exceptions to capital asset treatment relevant to taxpayers in light of these piecemeal rules. Key considerations for transacting in derivative instruments include the excep- issuers and holders of derivative instruments under US tions for (1) hedging transactions3 and (2) “commodities tax principles will include the character of income, gain, derivative financial instruments” held by a “commodities loss and deduction related to the instrument (ordinary derivatives dealer”.4 vs. -

Bond Futures Calendar Spread Trading

Black Algo Technologies Bond Futures Calendar Spread Trading Part 2 – Understanding the Fundamentals Strategy Overview Asset to be traded: Three-month Canadian Bankers' Acceptance Futures (BAX) Price chart of BAXH20 Strategy idea: Create a duration neutral (i.e. market neutral) synthetic asset and trade the mean reversion The general idea is straightforward to most professional futures traders. This is not some market secret. The success of this strategy lies in the execution. Understanding Our Asset and Synthetic Asset These are the prices and volume data of BAX as seen in the Interactive Brokers platform. blackalgotechnologies.com Black Algo Technologies Notice that the volume decreases as we move to the far month contracts What is BAX BAX is a future whose underlying asset is a group of short-term (30, 60, 90 days, 6 months or 1 year) loans that major Canadian banks make to each other. BAX futures reflect the Canadian Dollar Offered Rate (CDOR) (the overnight interest rate that Canadian banks charge each other) for a three-month loan period. Settlement: It is cash-settled. This means that no physical products are transferred at the futures’ expiry. Minimum price fluctuation: 0.005, which equates to C$12.50 per contract. This means that for every 0.005 move in price, you make or lose $12.50 Canadian dollar. Link to full specification details: • https://m-x.ca/produits_taux_int_bax_en.php (Note that the minimum price fluctuation is 0.01 for contracts further out from the first 10 expiries. Not too important as we won’t trade contracts that are that far out.) • https://www.m-x.ca/f_publications_en/bax_en.pdf Other STIR Futures BAX are just one type of short-term interest rate (STIR) future. -

Margin-Based Asset Pricing and Deviations from the Law of One Price∗

Margin-Based Asset Pricing and Deviations from the Law of One Price∗ Nicolae Gˆarleanu and Lasse Heje Pedersen† Current Version: September 2009 Abstract In a model with heterogeneous-risk-aversion agents facing margin constraints, we show how securities’ required returns are characterized both by their betas and their margins. Negative shocks to fundamentals make margin constraints bind, lowering risk-free rates and raising Sharpe ratios of risky securities, especially for high-margin securities. Such a funding liquidity crisis gives rise to “bases,” that is, price gaps between securities with identical cash-flows but different margins. In the time series, bases depend on the shadow cost of capital, which can be captured through the interest- rate spread between collateralized and uncollateralized loans, and, in the cross section, they depend on relative margins. We apply the model empirically to CDS-bond bases and other deviations from the Law of One Price, and to evaluate the Fed lending facilities. ∗We are grateful for helpful comments from Markus Brunnermeier, Xavier Gabaix, Andrei Shleifer, and Wei Xiong, as well as from seminar participants at the Bank of Canada, Columbia GSB, London School of Economics, MIT Sloan, McGill University, Northwestern University Kellog, UT Austin McCombs, UC Berkeley Haas, the Yale Financial Crisis Conference, and Yale SOM. †Gˆarleanu (corresponding author) is at Haas School of Business, University of California, Berkeley, NBER, and CEPR; e-mail: [email protected]. Pedersen is at New York University, NBER, and CEPR, 44 West Fourth Street, NY 10012-1126; e-mail: [email protected], http://www.stern.nyu.edu/∼lpederse/. -

Guide for Margin Finance

Guide for Margin Finance Guide for Margin Finance Contents Margin Finance What is margin finance? How does margin finance take place? Risks of margin finance Acknowledgement 1 / 6 Guide for Margin Finance Margin Finance Investors should request copies from their financial brokers and familiarize themselves with the following: The guide issued by the Jordan Securities Commission, Margin Finance Instructions, the list of securities allowed to be margin financed, and the margin finance agreement. Investors should also sign an acknowledgement that they have familiarized themselves with the above in order to protect their rights. This guide aims to familiarize investors with the concept of margin finance and the risks related to it. It should be read thoroughly. 2 / 6 Guide for Margin Finance What is margin finance? The term “Margin Finance” shall mean the financing by a Financial Broker of a part of the value of the securities in the margin finance account by guaranteeing the securities in that account. How does margin finance take place? Say you are an investor and you buy shares worth JD 5,000 with your own money, then the value of these shares rises to JD 7,500, your profit would be 50%. But if you finance your purchase of these shares through margin finance the shares, you would pay JD 2,500 of your own money and your broker would pay JD 2,500, so your profit would be 100%. In other words, your profit is greater when you margin finance. If, on the other hand, the value of the shares drops to JD 2,500 after you had bought them with your own money, your loss would be 50%; but if you had bought them from the margin finance account, your loss would be 100% plus any interest payments and fees. -

EQUITY EQUITY DER- PARAMETERS METHODOLOGIES USED in MARGIN CALCULATIONS Manual

EQUITY EQUITY DER- PARAMETERS METHODOLOGIES USED IN MARGIN CALCULATIONS Manual APRIL 2021 V02.0 1 TABLE OF CONTENTS Executive summary ...................................................................................... 3 Methodologies for determining Margin Parameters used in Margin Calculations ...................................................................................................... 5 2.1 Main parameters...................................................................................... 6 2.2 Margin Interval calculation ...................................................................... 7 2.2.1 Defining Coverage Level......................................................................... 7 2.2.2 Determining the Margin Interval for Equity cash ........................................ 7 2.2.3 Determining the Margin Interval for Equity derivatives .............................. 10 2.3 Product Group Offset Factor .................................................................. 10 2.4 Futures Straddle Margin ........................................................................ 10 2.4.1 Straddle Interest Rate Methodology ........................................................ 11 2.4.2 Straddle Correlation Methodology ........................................................... 13 2.5 Minimum Initial Margin ......................................................................... 13 2.6 Margin Intervals and Additional Margin changes ................................... 14 2 EXECUTIVE SUMMARY 3 EXECUTIVE SUMMARY This -

Investors Or Traders Perception on Equity Derivatives

European Journal of Molecular & Clinical Medicine ISSN 2515-8260 Volume 07, Issue 06, 2020 INVESTORS OR TRADERS PERCEPTION ON EQUITY DERIVATIVES Sreelekha Upputuri1, Dr. M. S. V Prasad2, Mrs. Sandhya Sri3 1Research Scholar GITAM institute of Management, Visakhapatnam, Andhra Pradesh. 2Professor and Head of the Finance Department, GITAM Institute of Management, Visakhapatnam, Andhra Pradesh. 3Associate Professor, A.V. N College, Visakhapatnam, Andhra Pradesh. Abstract Equity derivatives are a type of derivatives where its values are derived from equities like securities. Equity derivatives are derived from its one or more underlying equity security. The most commonly used equity derivatives in the market are futures and options. Futures can be stated as contracts which are standard in nature and can be transferred between the two parties with a purpose of buying or selling an underlying asset in future at particular time and price. Options can be described as contracts which give the buyer the right to buy or sell underlying asset at a particular price and time. In call option, the right to buy is applicable and in put option, the right to sell is applicable. This paper objective is to measure the perception of the investors towards Equity derivative. The derivative market seems to be new segment in secondary market operations in India. Usually this trade measures are sophisticated, making it difficult for an Indian investor to digest and also to make profits in trading the derivative. This study aims to measure the investors’ perception towards Derivatives market. This research is of descriptive nature, in which, systematic sampling technique is used.