MCB Bank Limited Financial Statements for the Year Ended

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GOVT-PUNJAB Waitinglist Nphs.Pdf

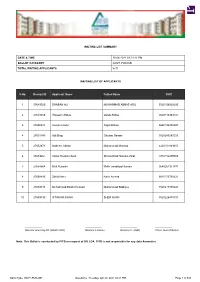

WAITING LIST SUMMARY DATE & TIME 20-04-2021 02:21:11 PM BALLOT CATEGORY GOVT-PUNJAB TOTAL WAITING APPLICANTS 8711 WAITING LIST OF APPLICANTS S No. Receipt ID Applicant Name Father Name CNIC 1 27649520 SHABAN ALI MUHAMMAD ABBAS ADIL 3520106922295 2 27649658 Waseem Abbas Qalab Abbas 3520113383737 3 27650644 Usman Hiader Sajid Abbasi 3650156358657 4 27651140 Adil Baig Ghulam Sarwar 3520240247205 5 27652673 Nadeem Akhtar Muhammad Mumtaz 4220101849351 6 27653461 Imtiaz Hussain Zaidi Shasmshad Hussain Zaidi 3110116479593 7 27654564 Bilal Hussain Malik tasadduq Hussain 3640261377911 8 27658485 Zahid Nazir Nazir Ahmed 3540173750321 9 27659188 Muhammad Bashir Hussain Muhammad Siddique 3520219305241 10 27659190 IFTIKHAR KHAN SHER KHAN 3520226475101 ------------------- ------------------- ------------------- ------------------- Director Housing-XII (LDAC NPA) Director Finance Director IT (I&O) Chief Town Planner Note: This Ballot is conducted by PITB on request of DG LDA. PITB is not responsible for any data Anomalies. Ballot Type: GOVT-PUNJAB Date&time : Tuesday, Apr 20, 2021 02:21 PM Page 1 of 545 WAITING LIST OF APPLICANTS S No. Receipt ID Applicant Name Father Name CNIC 11 27659898 Maqbool Ahmad Muhammad Anar Khan 3440105267405 12 27660478 Imran Yasin Muhammad Yasin 3540219620181 13 27661528 MIAN AZIZ UR REHMAN MUHAMMAD ANWAR 3520225181377 14 27664375 HINA SHAHZAD MUHAMMAD SHAHZAD ARIF 3520240001944 15 27664446 SAIRA JABEEN RAZA ALI 3110205697908 16 27664597 Maded Ali Muhammad Boota 3530223352053 17 27664664 Muhammad Imran MUHAMMAD ANWAR 3520223937489 -

SUMMARY of TAX EXPENDITURE 2021 Income Tax Estimates

SUMMARY OF TAX EXPENDITURE 2021 Tax Expenditure Report 2021 for federal taxes, based on data pertaining to FY 2019-20, amounted to an estimated Rs. 1,314.27 billion. Tax expenditure in sales tax amounted highest at Rs. 578.46 billion (44% of the total), while in income tax amounted to Rs. 448.05 billion (34%), and in Customs, to Rs. 287.77 billion (22%). In last fiscal year 2019-20, FBR’s tax collection was Rs. 3,997.4 billion. Hence, tax expenditure to total collection ratio comes to about 33%, and tax expenditure to GDP ratio stands at around 3.2%. The tax expenditure estimates are unadjusted amounts, meaning that elimination or repeal of a specific exemption would not necessarily produce the rupee amounts cited in this report. Actual receipts would depend on enforcement, taxpayer compliance, effective dates of legislation repealing the exemption, exact wording of any legislation, taxpayer’s behavior, and some other economic factors. This report briefly outlines federal tax exemptions and concessions. These descriptions do not grant rights or impose obligations; rather, the tax laws and rules made thereunder determine actual tax liability. Each estimate is based on the best information available from public and private sources, including FBR’s database. It would be exceptionally burdensome on taxpayers to require detailed reporting of transactions corresponding to each of the exemption sections and clauses. No such detailed reporting is imposed by statute or rules. Consequently, tax returns do not contain data sufficient to estimate the value of all exemptions and exclusions. Estimation requires identification of pertinent, useful data available from various external sources. -

SSR JUNE__2016 Reduced.Pdf

Central University of Kashmir SELF STUDY REPORT Submitted to NATIONAL ASSESSMENT AND ACCREDITATION COUNCIL (NAAC) Bangalore, India Table of Contents Content Page No. Executive Summary 1 Profile of the University 15 Criteria wise Inputs 25 Departmental Profiles 95 Appendices 281 Publications 282 Diversity in Faculty Recruitment 312 List of Court Cases 313 Executive Council 314 Academic Council 315 Finance Committee 317 Progression in Student Enrollment 318 Deans of various Schools 319 Members of IQAC 320 Administration 321 List of Students who qualified NET/JRF 322 Major Events 2010-15 323 Meetings of Various Academic/Administrative Boards 328 List showing students and other outreach activities during 2010-15 330 List Showing the awards received by the faculty during 2010-15 332 Central Universities Act 2009 333 Income and Expenditure 366 Central University of Kashmir Master Plan 371 Organizational Chart 372 Self Assessment Proforma 376 Executive Summary The University is presently operating through a number of campuses acquired on rent basis, owing to the fact that the construction of multi-storeyed buildings at the original site of the University Campus at Tulmulla (Ganderbal) has not yet been completed. Presently, the construction work is going on for pre-engineered 2-storeyed buildings which are expected to be completed within next six months. Hopefully, in the month of June-2016 some teaching departments may be shifted to Tulmulla (Ganderbal). At present, the three rented EXECUTIVE SUMMARY campuses are housing various teaching departments, the details of which are given as under: S. NO. NAME OF THE CAMPUS TOTAL BUILT-UP AREA DEPARTMENTS OPERATING IN THE CAMPUS. -

UBL Employee Pension Fund Trust

UBL Employee Pension Fund Trust Employees Retrenched in 1997 on Pension Fund Scheme List of complete retrenched employees in terms of Supreme Court Orders; Column1 EMPNO EMPLOYEE_NAME 1 113148 SYED ZAFAR ALI 2 113290 IQBAL PERVEZ MIRZA 3 113333 MIAN AHSAN HABIB 4 113388 MUHAMMAD LATIF KHAN 5 113397 S M PARWEZ AKHTAR 6 113449 MUHAMMAD QAYYUM MIRZA 7 113689 MUHAMMAD YUNUS 8 113865 SAADAT ALI 9 113883 SHAH BEHRAM QURESHI 10 113908 CH NAZIR AHMED 11 114361 MUHAMMAD AFZAL 12 114662 MOHAMMAD ASLAM 13 114811 JAMIL UR REHMAN 14 114884 MOHAMMAD ASHRAF JANJUA 15 114909 ANWAR HUSSAIN 16 114945 ZAMIR AHMED 17 114963 MUHAMMAD QUDDUS HASAN SIDDIQUI 18 115016 NASIM AHMED 19 115131 MUHAMMAD HANIF 20 115326 ABDUL QADIR AWAN 21 115423 MUHAMMAD ASHFAQUE 22 115654 ANSAR AHMED 23 115779 MUHAMMED SIDDIQUE ABA ALI 24 115788 WASIM AKHTAR GHANI 25 115867 ABOOBAKER 26 115919 MIRZA AFLAQ BEG 27 116211 SALEEM A BANA 28 116239 MUHAMMAD ISMAIL KHAN AFRIDI 29 116372 GHULAM HUSSAIN 30 116789 TURAB ALI A FRAMEWALA 31 116798 GHULAM AKBAR 32 116804 MUHAMMAD AMIN 33 116877 MUHAMMAD AMIN KHAN 34 117009 MUHAMMAD YOUSUF BAKKER 35 117188 MUHAMMAD IQBAL 36 117197 ALEXANDER MATHEWS 37 117452 KAMALUDDIN 38 117513 S SHAH NAWAZ ZIA 39 117586 ABDUL RAZZAQ TAI 40 117896 BADRUDDIN 41 117984 GUL ALAM KHAN Column1 EMPNO EMPLOYEE_NAME 42 118037 NASEER AHMED 43 118426 MANNAN AHMED 44 118648 S ANJUM HUSSAIN NAQVI 45 119010 MUHAMMAD YAQOOB 46 119199 ZAFAR IQBAL BHATTI 47 119223 RAIS AKHTAR 48 119375 QADRI MUHAMMAD SHAFI 49 119481 MUHAMMED IQBAL 50 119746 ABDUL QAYYUM 51 119807 IQBAL DAYALA -

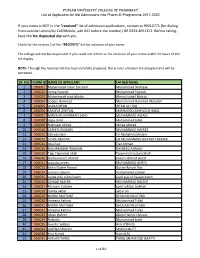

List of Admission Applications, Contact at 99212775 (For Dialing from Outside Lahore/By Cell/Mobile, Add 042 Before the Number) OR 0333-4051352

Punjab Univeristy College of Pharmacy List of Applicants for the Admissions into Pharm-D Programme 2017-2022 If your name is NOT in the “received” list of admission applications, contact at 99212775 (for dialing from outside Lahore/by Cell/Mobile, add 042 before the number) OR 0333-4051352. Before calling, have the fee deposited slip with you. Check for the version 2 of the “RECEIVED” list for inclusion of your name. The college will not be responsible if you could not inform us for omission of your name within 24 hours of the list display NOTE: Through the received list has been carefully prepared, the errors/ omission are accepted and will be corrected. SR. NO. FORM ID NAME OF APPLICANT FATHER NAME 1 DB0001 Muhammad Umar Eatsham Muhammad Shafique 2 DB0002 Amna Yaqoob Muhammad Yaqoob 3 DB0003 Muhammad saad bhutta Ahmad sohail bhutta 4 DB0004 Zoobia Hammad Muhammad Hammad Abdullah 5 DB0005 AMNA IRFAN IRFAN UL HAQ 6 DB0006 SAMEYA ASHFAQ MAHMOOD ASHFAQ AHMAQ 7 DB0007 MIRZA MUHAMMAD SAJID MUHAMMAD ASLAM 8 DB0008 Aqsa Jamil Muhammad Jamil 9 DB0009 Rukhsaar Ishfaq Ishfaq Ahmad 10 DB0010 SAFEER HUSSAIN MUHAMMAD HAFEEZ 11 DB0012 Zainab islam Ch Muhammad islam 12 DB0013 SIDRA AKHTAR CH MUHAMMAD AKHTAR CHEEMA 13 DB0014 Iqra Ejaz Ejaz Ahmad 14 DB0016 MUHAMMAD RAMZAN RASHEED AHMAD 15 DB0019 Taqi Tajammal Shah Tajammal Hussain Shah 16 DB0020 bisma naseer ahmed naseer ahmed javed 17 DB0021 tayyaba anees MUHAMMAD ANEES 18 DB0023 Sadia Gulam Rasool Gulam Rasool Naz 19 DB0024 zunaira saleem muhammad saleem 20 DB0025 syeda rida zahra kazmi syed ejaz ul -

From April 23 to 29, 2018)

STATEMENT OF ADVERTISEMENT RELEASED TO PRINT MEDIA (From April 23 to 29, 2018) S # Newspaper Station Insertions CMs 1. 92-News Lahore 3 102 2. Aaina Quetta 1 60 3. Aaj Peshawar 7 352 4. Aaj Subh Peshawar 1 30 5. Aajir Rawalpindi 1 40 6. Ab Tak Lahore 1 32 7. Ace News Faisalabad 1 34 8. Aeen Peshawar 2 120 9. Aftab Multan 2 80 10. Aftab Lahore 1 60 11. Aina-e-Jehan Islamabad 1 36 12. Akhbar-e-Haq Islamabad 1 21 13. Al-Akhbar Islamabad 1 60 14. Al-Akhbar Peshawar 1 108 15. Al-Jalal Sargodha 1 20 16. Al-Jazeera Quetta 2 38 17. Aman (F) Faisalabad 1 76 18. Amn Karachi 1 80 19. Asas Rawalpindi 3 104 20. Ash Sharq Rawalpindi 1 36 21. Asro Hyderabad 1 40 22. Ausaf (C) 2 170 23. Ausaf Islamabad 5 223 24. Ausaf Muzaffarabad 4 196 25. Ausaf Lahore 2 92 26. Ausaf Gilgit Baltistan 1 81 27. Ausaf Karachi 1 60 28. Autan Rawalpindi 1 48 29. Awam Quetta 1 80 30. Awam Islamabad 1 52 31. Awami Awaz Karachi 5 262 32. Awami Forum Karachi 1 20 33. Awami Mahaz Karachi 1 14 34. Azadi Swat 1 88 35. Azadi (Q) Quetta 1 60 36. Azan Gilgit Baltistan 3 206 37. Azkar Rawalpindi 2 80 38. Baakhabar Quetta 1 88 39. Bad-e-Shamal Skardu 1 40 40. Baghi Lahore 1 30 41. Baitab Lahore 1 30 42. Balochistan Express Quetta 2 140 43. Balochistan News Quetta 1 80 44. Barwaqt Khabar Bahawalpur 1 45 45. -

Resultcafexaminationsp2021.Pdf

THE INSTITUTE OF CHARTERED ACCOUNTANTS OF PAKISTAN PRESS RELEASE April 29, 2021 Spring 2021 Result of Certificate in Accounting and Finance (CAF) The Council of the Institute of Chartered Accountants of Pakistan is pleased to declare the result of the above examination held in March 2021: Candidates Passed-CAF Candidates Passed-CAF CRN Name Credited CRN Name Credited Paper(s) Paper(s) 046836 MUHAMMAD IRFAN ASIF KHOKHAR 078174 HAMZA SALEEM S/o MUHAMMAD ASIF KHOKHAR S/o MUHAMMAD SALEEM KHAN 056117 ALI AHMED ABBASI 078190 SYED IMRAN HAIDER S/o WAKEEL AHMED ABBASI S/o SYED ABID HUSSAIN 063526 UZAIR JAVEED 078759 MUHAMMAD BILAL PATHAN S/o JAVEED SALEEM S/o GHUFRAN AHMED PATHAN 066420 FARAZ NAEEM AHMED 079271 MUHAMMAD UBAID ASHRAF S/o NAEEM AHMED CHAUDHARY S/o RANA MUHAMMAD ASHRAF 068288 USMAN ALI 079584 CH. HAMDI TAHIR S/o PERVAIZ AHMAD S/o CHAUDHRY TAHIR AMIN 068343 FAIZA ASHIQ 079889 MOHSIN KHAN D/o ASHIQ ALI S/o ZULFIQAR ALI KHAN 069546 MUHAMMAD ASAD ULLAH FAROOQ 080002 MAHRUKH ALI S/o MUHAMMAD FAROOQ D/o ZULFQAR ALI 070000 ABUZAR SUBHANI 080328 ANAS TANVEER S/o MUNIR AHMAD S/o TANVEER HUSSAIN 071130 AMIR KHAN 080580 MUHAMMAD ADNAN ARSHAD S/o TILAWAT KHAN S/o MUHAMMAD ARSHAD 071198 FAHAD BIN TARIQ 080632 AHSAN SALMAN S/o TARIQ MEHMOOD S/o MUHAMMAD SALMAN 072264 GHULAM FATIMA 081229 AMMARA ASLAM D/o YAQOOB AHMAD FAROOQI D/o MUHAMMAD ASLAM 072552 IQRA GUL AFSHA 081460 JALAL KHAN D/o GUL SHER KHAN S/o SHAHEEN ULLAH 074194 HAROON KHAN 081473 SARAH ARSHAD S/o ILYAS KHAN D/o ARSHAD SALEEM 074332 SABA IFTIKHAR 082093 MUHAMMAD ARSALAN D/o IFTIKHAR -

NBP Islamic Sarmaya Izafa Fund Download

NBP ISLAMIC SARMAYA IZAFA FUND NBP Islamic Sarmaya Izafa Fund MISSION STATEMENT To rank in the top quartile in performance of NBP FUNDS relative to the competition, and to consistently offer Superior risk-adjusted returns to investors. 01 NBP Islamic Sarmaya Izafa Fund FUND'S INFORMATION 03 DIRECTORS' REPORT 05 REPORT OF THE TRUSTEE TO THE UNITHOLDERS 09 INDEPENDENT AUDITORS' REVIEW REPORT TO THE UNITHOLDERS 10 Contents CONDENSED INTERIM STATEMENT OF ASSETS AND LIABILITIES 11 CONDENSED INTERIM INCOME STATEMENT 12 CONDENSED INTERIM STATEMENT OF COMPREHENSIVE INCOME 13 CONDENSED INTERIM STATEMENT OF MOVEMENT IN UNIT HOLDERS' FUND 14 CONDENSED INTERIM CASH FLOW STATEMENT 15 NOTES TO AND FORMING PART OF THESE CONDENSED INTERIM FINANCIAL INFORMATION 16 02 NBP Islamic Sarmaya Izafa Fund FUNDS INFORMATION Management Company NBP Fund Management Limited - Management Company Board of Directors of Management Company Shaikh Muhammad Abdul Wahid Sethi Chairman Dr. Amjad Waheed Chief Executive Officer Ms. Mehnaz Salar Director Syed Hasan Irtiza Kazmi Director Mr. Ali Saigol Director Mr. Imran Zaffar Director Mr. Khalid Mansoor Director Mr. Humayun Bashir Director Mr. Saad Amanullah Khan Director Company Secretary & COO Mr. Muhammad Murtaza Ali Chief Financial Officer Mr. Khalid Mehmood Audit & Risk Committee Mr. Saad Amanullah Khan Chairman Syed Hasan Irtiza Kazmi Member Mr. Imran Zaffar Member Mr. Humayun Bashir Member Human Resource Committee Mr. Khalid Mansoor Chairman Shaikh Muhammad Abdul Wahid Sethi Member Mr. Ali Saigol Member Mr. Humayun Bashir Member Strategy & Business Planning Committee Mr. Humayun Bashir Chairman Ms. Mehnaz Salar Member Mr. Ali Saigol Member Mr. Imran Zaffar Member Mr. Saad Amanullah Khan Member Trustee Central Depository Company of Pakistan Limited CDC House, 99-B, Block "B" S.M.C.H.S., Main Shahra-e-Faisal, Karachi. -

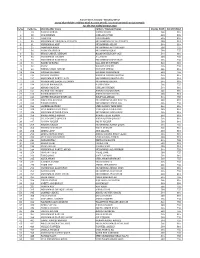

S.No Folio No. Shareholder Name Father / Husband

Amreli Steels Limited - Dividend (D-3) List of Shareholders without Bank Account Details / In-Accurate Bank Account Details For the year ended 30 June 2018 S.No Folio No. Shareholder Name Father / Husband Name Shares Held Net Dividend 1 13 BASSAM ZUBAIR ZUBAIR FEROZ 500 810 2 28 GUL HUSSAIN GHULAM QUTAB 500 809 3 29 IRAM GUL GUL HUSSAIN 500 809 4 30 MUHAMMAD FURQAN ALI CHISHTI MUHAMMAD RIAZ ALI CHISHTI 500 810 5 31 MUHAMMAD ARIF MUHAMMAD ASLAM 500 810 6 35 SHAHZADA KHAN MUHAMMAD AYYUAB KHAN 500 755 7 36 NASREEN AKHTAR MUHAMMAD IQBAL 500 755 8 53 HUSAIN ABDUL REHMAN HASAN MUIZUDDIN QAZI 500 810 9 55 MUHAMMAD IBRAHIM ALLAUDIN 500 755 10 68 MOHAMMAD NAIM KHAN MOHAMMAD HAFIZ KHAN 500 755 11 69 HAMID UZ ZAFAR RAO AZIZ UR REHMAN 500 810 12 92 SADAF WAJAHAT NAEEM 500 755 13 94 ZUBAIR FAISAL ABBASI M. HANIF ABBASI 500 810 14 105 NAVEED GULSHER GULSHER MUHAMMAD 500 755 15 116 AYESHA SHAMIM KANWAR SHAMIM AKHTAR 500 810 16 117 MOHAMMAD NABEEL RAZA MOHAMMAD JAWAID RAZA 500 810 17 118 MUHAMAMD QAMAR UZ ZAMAN MUHAMMAD BASHIR 500 810 18 119 ARSLAN BIN NASEER NASIR UDDIN 500 755 19 126 AHMAD NADEEM GHULAM HUSSAIN 500 810 20 127 ASFAND YAR FAROOQ AHMAD FAROOQ KHAN 500 810 21 145 KHURRAM WAHEED ABDUL WAHEED ILYAS 500 810 22 146 SAYYED HUSSNAIN ZULFIQAR ZULIFQAR AHMAD 500 755 23 148 SHOAIB UR REHMAN MUHAMMAD SHARIF BHUTTA 500 810 24 165 ZISHAN USMAN MOHAMMAD USMAN ALI\ 500 755 25 182 SABEEKA ALI ZAIDI SYED KOMAIL TAZA ZAIDI 500 810 26 183 SYED KOMAIL RAZA ZAIDI SYED IQBAL AHMED ZADI. -

Channel-7 Quarter Page Color PID No. 4871 /20 1. the News (C) 2

M/o Information & Broadcasting (Women day) Channel-7 Quarter page color PID No. 4871 /20 1. The News (C) 2. Nawa-e-Waqt Ibd/Lhr/Mul 3. Khabrain Ibd/Mul 4. Ausaf Ibd/Mzb/glt/Mul 5. Aaj Peshawar 6. Dunya Ibd/Lhr/Qta/Guj Quarter page B&W 7. Bhasha News Besham 8. Voice of Pakistan Islamabad 9. Nawa-e-Islamabad Rawalpindi 10. Multan Nama Multan 11. Lokai Lahore 12. Gul Zameen Gawadar Quetta 13. Minority Times Islamabad 14. Parwaz (F) Faisalabad 15. Capital World Islamabad 16. Times Peshawar 17. Awaz-e-Shehr Peshawar 18. Barwaqt Khabar Bahawalpur 19. Wateen Vehari 20. Kashmir Times Rawalpindi 21. Saba Quetta 22. Parliament Times Muzaffarabad 23. Jammu & Kashmir Times Muzaffarabad 24. Asian Sun Rawalpindi 25. Panah Gilgit Baltistan 26. Waas Islamabad 27. Awaz-e-Subh Peshawar 28. Nai Subh Faisalabad 29. Bayan Peshawar 30. Capital Report Islamabad 31. Qul Peshawar 32. Pindi Post Rawalpindi 33. Eagle Karachi 34. Janch Islamabad 35. Payam-e-Khybar Peshawar 36. Baghi Lahore 37. Manind-e-Aina Peshawar 38. Bolta Pakistan Islamabad 39. Date Line Islamabad 40. Eman Karachi 41. Labour News Islamabad 42. Aham Khabar Quetta 43. Frontier News Peshawar 44. Kashmir Post Mzfd 45. Jammu & Kashmir Mzfd 46. Information Times Harripur 47. Cholistan Times RYK 48. Eagle Hub 49. Frontier star Peshawar 50. Koshish Hyderabad 51. Kashmir Express Mzb 52. Universal Recorder Rawalpindi 53. Press conference Gujranwala 54. Aflaak Lahore 55. Geo Hazara Haripur 56. News Lark Karachi 57. Capital Today Islamabad 58. Sargaram Abbottabad 59. Work News Islamabad 60. Mashriq Lahore 61. Big Digit Islamabad 62. -

August 2021 As Against the Target of Rs

Smart & Easy Savings! WE ARE LIVE ON WHATSAPP send us “NBP Funds” on to get started 021 111 111 632 Fund Manager Report of Conventional Schemes August - 2021 AM1 NBP Fund Management Limited For More Information & Investment Rated by PACRA Disclaimer: All investments in mutual funds are subject to market risk. Past performance is not necessarily indicative of future results. Please read the Offering Documents to understand the investment policies and the risks involved. NBP Funds or any of its sales representative cannot guarantee preservation / protection of capital and / or expected returns / profit on investments. Note: Detailed monthly reports of NBP Funds are also available on our website www.nbpfunds.com NBP FUNDS Table of Contents Managing Your Savings Table of Contents Table 1-2 CEO’s Write-up 03 Capital Market Review NBP Government Securities 04 05 NBP Money Market Fund Liquid Fund NGSLF NMMF NBP Government Securities 06 Savings Fund 07 NBP Mahana Amdani Fund NGSSF NMAF 08 NBP Financial Sector Income Fund 09 NBP Income Opportunity Fund NFSIF NIOF 10 NBP Savings Fund 11 NBP Sarmaya Izafa Fund NBP-SF NSIF 12 NBP Balanced Fund 13 NBP Stock Fund NBF NSF 14 NBP Financial Sector Fund 15 NBP Pakistan Growth Exchange NFSF NBP-GETF Traded Fund 16 NAFA Pension Fund NPF NBP FUNDS Managing Your Savings Promising Economic and Stock Market prospects Economy: After Coronavirus-induced contraction in FY20, Pakistan’s economy staged a V-shaped recovery as reflected by an estimated 3.94% GDP growth for FY21. We expect continuation of this growth momentum and anticipate GDP growth of 4.3% in FY22. -

List of Graduate Students 08

2008 FACULTY OF ARTS/ISLAMIC STUDIES/MANAGEMENT SCIENCES FACULTY OF SCIENCE / PHARMACY ARABIC FACULTY OF SCIENCE B.A.(HONS.) APPLIED CHEMISTRY MARIA MALIK B.Sc (H) MUHAMMAD RAMZAN MUHAMMAD ANWAR ADEEL SARWER / GHULAM SARWER MUHAMMAD ISHAQ MUHAMMAD ANWAR AFSHAN ISHAQUE RIAZ AHMED M. ISHAQUE AHMED AHSAN SAFDER ALI ALI FARAZ ARABIC SARFARAZ AHMAD KHAN AMMARAH MASOOD M.A.(FINAL) MASOOD HASAN FARJAD ALI ARSALAN ELAHI ABDUL REHMAN SHAN ELAHI HAFIZA SUMERA BUSHRA ABIDI M. HAMID KHAN SYED ZULFIQAR HADER ABIDI MUHAMMAD SHAKEEL FARAH MUNAWAR MUHAMMAD ASLAM MUHAMMAD MUNAWAR HUSSAIN MUHAMMAD YOUNAS HAFIZ MUHAMMAD KAWISH HAJI ALI ABDUL QAYYUM ANSARI SABA NOOR UZ ZAMAN HINA BATOOL NOOR UZ ZAMAN SYED MUJAHID ABBAS SANA ABDUL SHAKOOR HUMNA WAHID ABDUL SHAKOOR LASI SYED WAHID ALI SARA NASIM M. HABIB UDDIN SIDDIQUI XXX M. QAMAR UDDIN SIDDIQUI HUMERA SHARIF MAHEEN ILYAS SHARIF UDDIN MUHAMMAD ILYAS FAROOQUI BANEEN ABBAS MAIMOONA SAFDAR SHEIKH QAISER ABBAS SAFDAR ALI NOREEN MANSOOR TALAT JAMEEL AHMED MASOOD TALAT MEHWISH LATIF ABDUL LATIF MUDASSIR FAROOQ BENGALI FAROOQ AZAM MUHAMMAD FARHAN M.A.(FINAL) MUHAMMED RIZWAN JAHENGIR AHMED MUHAMMAD NAVEED AKBAR ALI AHMED MUHAMMAD AKBAR MUHAMMAD TUAHA AKHTER ABDUL KARIM AKHTER MUHAMMAD UMAIR HABIB BUSINESS ADMINISTRATION MUHAMMAD HABIB 1 / 86 2008 NAUSHIN MUBASHIR B.B.A.(HONS.) MUBASHIR AHMED AAMIR NIDA IQBAL ROSHAN ALI IQBAL HUSSAIN AHAD HUSSAIN NIDA NOOR SYED WAJAHAT HUSSAIN NOOR UL HAQUE AISHA RAZI HAIDER OVAIS AHMED ANSARI RAZI UDDIN HAIDER AQEEL AHMED ALI ASIM JAFRI SABAH TAHFOOR ALI ZAMIN SYED TAHFOOR UL ISLAM