(“Mah Sing” Or “Company”) Proposed Joint

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

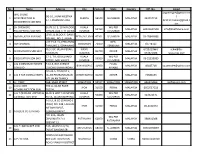

No. Name Address City Postcod State Country Off. No. Email 1 JING

No. Name Address City Postcod State Country Off. No. Email [email protected] JING SHENG BG-16, JALAN MESTIKA / 1 CONSTRUCTION & CHERAS 56100 SELANGOR MALAYSIA 342957713 17, TAMAN MESTIKA [email protected] ENGINEERING SDN BHD om 2H OFFSHORE SUITE 16-3, 16TH FLOOR, KUALA WIL PER 2 50450 MALAYSIA 60321627500 [email protected] ENGINEERING SDN BHD WISMA UOA II, 21 JALAN LUMPUR K.LUMPUR LEVEL 8, BLOCK F, OASIS 3 3M MALAYSIA SDN BHD PETALING JAYA 47301 SELANGOR MALAYSIA 03-78842888 SQUARE, NO. 2, JALAN LOT 15 & 19, PERSIARAN NEG. 4 3M SEREMBA SEREMBAN 70450 MALAYSIA 66778111 TANJUNG 2, SENAWANG SEMBILAN PLO 317, JALAN PERAK, PASIR 072521288 / schw@5e- 5 5E RESOURCES SDN BHD 81700 JOHOR MALAYSIA KAWASAN GUDANG 072521388 resources.com 17-6, THE BOULEVARD KUALA WIL PER 6 8 EDUCATION SDN BHD 59200 MALAYSIA 03-22018089 OFFICE, MID VALLEY LUMPUR K.LUMPUR A & D DESIGN NETWORK F-10-3, BAY AVENUE PULAU 7 BAYAN LEPAS 11900 MALAYSIA 46447718 [email protected] SDN BHD LORONG BAYAN INDAH 1 PINANG NO 23-A, TINGKAT 1, 8 A & K TAX CONSULTANTS JALAN PEMBANGUNAN JOHOR BAHRU 81200 JOHOR MALAYSIA 72385635 OFF JALAN TAMPOI 9 A + PGRP 36B, SAGO STREET SINGAPORE 50927 SINGAPORE SINGAPORE 656325866 [email protected] A A DESIGN 390-A, JALAN PASIR 10 IPOH 31650 PERAK MALAYSIA 6052537518 COMMUNICATION SDN PUTEH, A H T (NORLAN UNITED) & BLOK B UNIT 4-8 IMPIAN KUALA WIL PER 11 50460 MALAYSIA 322722171 CARRIAGE SDN BHD KOTA, JALAN KAMPUNG LUMPUR K.LUMPUR A JALIL & CO SDN BHD ( IPOH ) NO. 14B, LALUAN IPOH 31350 PERAK MALAYSIA 05-3132072 MEDAH RAPAT, 12 A JALIL & CO SDN BHD GUNUNG RAPAT, NO. -

Property Launches Major News

ECONOMIC OVERVIEW Property launches Key statistics Latest release Previous rate Apartments / Condos / Townhouses Two storey terraced houses Quarterly GDP growth 4.5% (4Q2009) -1.2% (3Q2009) Two & half storey terraced houses Annual GDP growth -1.7% (2009) 4.6% (2008) Two storey semi-d cluster houses Consumer Price Index (CPI) 1.2% (Feb-10) 1.3% (Jan-10) Two storey semi-d houses Two & half storey semi-d houses Industrial Production Index (IPI) 107.2 (Jan-10) 104.2 (Dec-09) Two storey detached houses Base Lending Rate (BLR) 5.80% (Mac-10) 5.51% (Feb-10) Two & half storey detached houses Exchange rate: RM to US dollar RM3.258 (30/03) RM3.390 (01/03) Major News Source: Department of Statistics Malaysia & Bank Negara Malaysia IOI expects brisk sales of Adenia phase … First quarter of 2010 (1Q2010) has shown significant improvement as compared Magna Prima to launch 5 projects in … with the precesdent quarter in 2009, where at the height of the global financial SP Setia in growth mode in southern Johor crisis, the government was forced to introduce two (2) economic stimulus Development of i-City enters 2nd phase… packages worth RM67 billion. Ivory seeks investor for planned hotel Sime Darby Property, Sunrise in RM1 bil.. During 1Q2010, it was announced that the country’s economic slump has ended New hotel to open soon in KL when it was announced that the country’s Gross Domestic Products (GDP) grew RM40 million swiftlet farm for Sarawak… by 4.5% in 4Q2009 after recording negative growths of -6.2%, -3.9% and -1.2% during the 1Q2009, 2Q2009 and 3Q2009, respectively. -

WTW Property Market 2011 C H Williams Talhar & Wong

C H Williams Talhar & Wong WTW Property Market 2011 C H WILLIAMS TALHAR & WONG Established in 1960, C H Williams Talhar & Wong (WTW) is a leading real estate services company in Malaysia and Brunei (headquartered in Kuala Lumpur) operating with 25 branches and associated offices. WTW provides Valuation & Advisory Services, Agency & Transactional Services and Management Services. HISTORY Colin Harold Williams established “C H Williams & Co, Valuer & Estate Agent” when he set up office in Kuala Lumpur in 1960. Messrs C H Williams Talhar & Wong was formed in 1973 following the merger with Johor based Talhar & Co (Valuer & Estate Agent) and the inclusion of Dato Wong Choon Kee. PRESENT MANAGEMENT The Group is headed by Chairman, Mohd Talhar Abdul Rahman who guides the group on policy developments and identifies key marketing strategies which have been instrumental in maintaining the strong competitive edge of WTW. The current Managing Directors of the WTW Group operations are: ► C H Williams Talhar & Wong Sdn Bhd Foo Gee Jen ► C H Williams Talhar & Wong (Sabah) Sdn Bhd Chong Choon Kim C H Williams Talhar & Wong ► C H Williams Talhar & Wong & Yeo Sdn Bhd (operating in Sarawak) Robert Ting ► WTW Bovis Sdn Bhd Dinesh Nambiar 2 Chairman’s Foreword resuscitated space, can generate their trades and on how much was spent to refit the buildings on top of the acquiring cost of the landed assets in the first instance. There are still nonetheless many buildings in major towns and cities which remain unproductive. These bear witness to the excesses of our past euphoric boom periods. Renewed awareness and urgent re-thinking in solving urban blight is as much a priority if the well- being of our urban environment is to rise in tandem with the country’s expected economic transformation. -

Light Rail Transit Stations

Light Rail Transit Stations Kuala Lumpur, Malaysia Architect: Arkitek Kitas Sendirian / Tay Kiam Seng Client: Sistem Transit Aliran Ringan Built Area: 60’190 m² Cost: n.a. Kuala Lumpur’s first two light rail transit (LRT) lines were built on a limited budget. The c 27 miles of track serve 25 stations, many of them in challenging situations spanning over the river or existing roads. The design concept is based on the traditional Malay ‘wakaf’, or wayside rest-stop - a simple exposed timber structure with open sides and a layered roof. In the LRT stations this is translated into an exposed structure with minimal brick or concrete masonry walls and a layered roof consisting of metal decks supported by large-span tubular steel members. 3198.MAL 2007 Award Cycle 2007 On Site Review Report 3198.MAL by Hanif Kara Light Rail Transit Stations Kuala Lumpur, Malaysia Architect Arkitek Kitas Sendirian / Tay Kiam Seng Client Sistem Transit Aliran Ringan Design 1994 - 1996 Completed 1998 Kuala Lumpur Light Rail Transit System Kuala Lumpur, Malaysia I. Introduction Sistem Transit Aliran Ringin (STAR) is the operator of System 1 of the Kuala Lumpur Light Rail Transit System (KLLRT). This was built in two phases. Phase I is approximately 12 kilometres long and runs from Ampang to Jalan Sultan Ismail. The first 9.5 kilometre-stretch is at-grade, utilising the existing but disused Malayan Railways corridor; the remainder of the route is elevated. Thirteen stations were built for Phase 1, including an administration building and depot and stabling yard at Ampang. Phase II is approximately 15 kilometres long and extends the Phase 1 line in both directions: 3.2 kilometres northwards (along the elevated portion) to Sentul Timur, and 11.8 kilometres southwards to the Commonwealth Games Village and Bukit Jalil Station, which serves the national sports complex. -

Major News Property Launches

Property launches ECONOMIC OVERVIEW Apartments / Condos / Townhouses Key statistics Latest release Previous rate Single storey terraced houses Two storey terraced houses Quarterly GDP growth 4.0% (2Q2011) 4.6% (1Q2011) Three storey terraced houses Annual GDP growth 7.2% (2010) -1.7%(2009) Three storey semi-d houses Two storey detached houses Consumer Price Index (CPI) 3.3% (Aug-11) 3.1% (Jul-11) Two & half detached houses Industrial Production Index (IPI) 107.5 (Jul-11) 108.0 (June-11) Three storey detached houses Base Lending Rate (BLR) 6.60% (May-11) 6.27% (Apr-11) Major News Exchange rate: RM to US dollar RM3.1910 (30/09) RM2.9700 (01/09) Vue woos prospective buyers with… Source: Department of Statistics Malaysia & Bank Negara Malaysia Canada, Australia next on TA Global… Bukit OUG condominium owners… New HELP campus to be ready by 2013 The Malaysia’s economy recorded a growth of 4.0% during the second quarter of SunREIT to double value of Putra Place 2011. Services sector was the main contributor to the economic growth. The key Laman PKNS to aim for GBI Platinum impetus on the demand side was the Private Final Consumption Expenditure. Kedah Hydrocarbon Hub back on track During the first six months of 2011, the Gross Domestic Products (GDP) expanded by 4.4%. LBS to launch high-end RM3.5bil… Magna Prima in A$210m Aussie… The Consumer Price Index (CPI) accelerated by 3.3% year-on-year in August, on River of Life in full flow higher prices for miscellaneous goods and services, recreation services and PR1MA sites located culture as well as housing, water, electricity, gas and other fuels. -

Managing Facilities on Malaysian Low-Cost Public Residential for Sustainable Adaptation

Available online at www.sciencedirect.com ScienceDirect Procedia - Social and Behavioral Sciences 168 ( 2015 ) 52 – 60 AicE-Bs2014Berlin (formerly AicE-Bs2014Magdeburg) Asia Pacific International Conference on Environment-Behaviour Studies Sirius Business Park Berlin-yard field, Berlin, 24-26 February 2014 “Public Participation: Shaping a sustainable future” Managing Facilities on Malaysian Low-cost Public Residential for Sustainable Adaptation * Ahmad Ezanee Hashim, Siti Aida Samikon , Faridah Ismail, Zulhabri Ismail Faculty of Architecture, Planning and Surveying, Universiti Teknologi MARA, 40450 Shah Alam, Selangor, Malaysia* Abstract Public housing is affordable living houses for low-income group and to overcome the issues of illegal squatters in towns and cities area. Within limited space of land, a multi-storey low-cost building will enable to provide many housing units to be built. This research aims to highlight and analyze issues faced by the management of low-cost public housing toward the sustainable adaptation of existing facilities. Analysis is based from a comparative study of managing multi- storey housing and feedback given by the stakeholders. Finding identified will provides important data to enhance physical facilities requirement and extensive consideration relevant to sustainable adaptation, which the entire problems concurrently in multi-storey public housing can be well treated. © 2015 The Authors. Published by Elsevier Ltd. This is an open access article under the CC BY-NC-ND license (http://creativecommons.org/licenses/by-nc-nd/3.0/© 2014 Published by Elsevier Ltd. Selection). and peer-review under the responsibility of the Centre for Environment- PeerBehaviour-review under Studies responsibility (cE-Bs), ofFaculty Centre forof Architecture,Environment-Behaviour Planning Studies & Surveying, (cE-Bs), Faculty Universiti of Architecture, Teknologi Planning MARA, & Surveying,Malaysia . -

D:\Atsa\Pp\Affordable Housings in Greater Kuala

1 Copyright © 2018 ATSA Architects Published by ATSA Architects Sdn Bhd All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted, in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without written permission from the copyright owner. Disclaimers The information presented in this report has been assembled, derived and developed from various projects and design proposals carried out by ATSA. These are presented in good faith. The author and publisher have made every reasonable effort to ensure that information presented is accurate. It is the responsibility of all users to utilize professional judgment, experience and common sense when applying information presented in this book. This responsibility extends to the verification of local codes, standards and climate data. Every effort has been made to ensure that intellectual property rights are rightfully acknowledged. Omissions or errors, if any, are unintended. Where the publisher or author is notified of an omission or error, these will be corrected in subsequent editions. Publisher ATSA Architects Sdn Bhd 45 Jalan Tun Mohd Fuad 3 Taman Tun Dr Ismail 60000 Kuala Lumpur Malaysia Website: www.atsa.com.my Email: [email protected] Author Ar. Azim A. Aziz Co-Author and Designed by Mohamad Haziq Zulkifli 2 AFFORDABLE HOUSINGS IN GREATER KUALA LUMPUR (KLANG VALLEY) AND URBAN MALAYSIA : PLANNING, ISSUES AND FUTURE CHALLENGES TABLE OF CONTENTS Pages Pages 5.5.1 Numbers of Affordable Housings that Greater -

Dewan Rakyat Parlimen Ketiga Belas Penggal Kedua Mesyuarat Ketiga

Naskhah belum disemak DEWAN RAKYAT PARLIMEN KETIGA BELAS PENGGAL KEDUA MESYUARAT KETIGA Bil. 51 Rabu 19 November 2014 K A N D U N G A N JAWAPAN-JAWAPAN LISAN BAGI PERTANYAAN-PERTANYAAN (Halaman 1) RANG UNDANG-UNDANG: Rang Undang-undang Perbekalan 2015 Jawatankuasa:- Jadual:- Maksud B.47 (Halaman 26) Maksud B.25 (Halaman 87) Maksud B.32 (Halaman 133) Maksud B.21 (Halaman 177) USUL-USUL: Waktu Mesyuarat dan Urusan Dibebaskan Daripada Peraturan Mesyuarat (Halaman 26) Usul Anggaran Pembangunan 2015 Jawatankuasa:- Maksud P.47 (Halaman 26) Maksud P.25 (Halaman 87) Maksud P.32 (Halaman 133) Maksud P.21 (Halaman 177) DR.19.11.2014 1 MALAYSIA DEWAN RAKYAT PARLIMEN KETIGA BELAS PENGGAL KEDUA MESYUARAT KETIGA Rabu, 19 November 2014 Mesyuarat dimulakan pada pukul 10.00 pagi DOA [Tuan Yang di-Pertua mempengerusikan Mesyuarat] JAWAPAN-JAWAPAN LISAN BAGI PERTANYAAN-PERTANYAAN 1. Dato’ Shamsul Anuar bin Haji Nasarah [Lenggong] minta Menteri Dalam Negeri menyatakan: (a) jumlah terkini penjenayah negara asing yang ditahan di negara ini; dan (b) jumlah kerugian, perbelanjaan yang Polis Diraja Malaysia (PDRM) terpaksa belanjakan ekoran pencerobohan Lahad Datu. Timbalan Menteri Dalam Negeri [Dato Sri Dr. Haji Wan Junaidi Tuanku Jaafar]: Terima kasih Tuan Yang di-Pertua. Bismillahi Rahmani Rahim, Assalamualaikum warahmatullahi wabarakatuh. Tuan Yang di-Pertua, pihak polis sentiasa memberi perhatian yang serius dalam membendung kegiatan jenayah melibatkan warga asing sama ada yang datang untuk melancong, untuk belajar atau bekerja di negara ini yang boleh mendatangkan kemudaratan kepada kesejahteraan dan keharmonian rakyat tempatan. Statistik pada tahun 2013 seramai 19,056 orang warga asing telah ditangkap bersamaan dengan 12% daripada keseluruhan 147,062 kes jenayah indeks yang dilaporkan di seluruh negara. -

In the Land Below the Wind

MAKE BETTER DECISIONS FRIDAY FEBRUARY 12, 2016 ISSUE 2102/2016 A PULLOUT EVERY FRIDAY WITH Read this copy online @ TheEdgeProperty.com MAKE BETTER DECISIONS PP 9974/08/2013 (032820) ep2 NEWS ep3 ADVERTORIAL ep7 DEALMAKERS Dynasty Hotel is most A convention Street smarts key to expensive property with a diff erence Nick Lu’s success for auction LUXURY CONDO WAVE in the land below the wind Th e non-landed residential market in Kota Kinabalu, Sabah, is seeing a high-end condominium boom, leading to a fl urry of development activity in the city. See story on pages ep4 & 5. SHAHRIN YAHYA/THE EDGE PROPERTY FRIDAY FEBRUARY 12, 2016 • THEEDGE FINANCIAL DAILY EP2 PROPERTY | NEWS Go to TheEdgeProperty.com for more property news MOST READ ON NEWS ROUNDUP TheEdgeProperty.com “Last year, retail sales have report- value of the land at RM78.4 million. Dynasty Hotel is most edly been very slow, with some retail- expensive property for ers reporting a drop in sales as a result Launch of Qi City in Ipoh auction of a multitude of factors. Th is includes planned for 2Q2016 Dynasty Hotel DESPITE having gone under the the implementation of the Goods tops list of most hammer a few times since 2014, and Services Tax and the weakening expensive property the reserve price of Dynasty Hotel ringgit driving up cost, which reduced for auction at (pictured) in Kuala Lumpur has re- the purchasing power of Malaysian mained at RM210 million. It is the consumers,” Sulaiman noted. RM210 mil most expensive commercial prop- erty on the auction market last year, MKH takes part in redevelop- Australian according to online auction listing ment of Pekeliling fl ats property market platform AuctionGuru.com.my. -

The Construction and Demolition Waste Management in Malaysia: the Life Cycle Assessment Analysis Approach to Sustainability

The Construction and Demolition Waste Management in Malaysia: The Life Cycle Assessment Analysis Approach to Sustainability Mah Chooi Mei September 2017 Graduate School of Environmental and Life Science Division of Environmental Science Solid Waste Management Research Laboratory ABSTRACT Construction and demolition waste (C&DW) continues to increase in parallel with economic growth in emerging and developing countries like Malaysia. The large amount and improper management of C&DW generated during construction often results in considerable environmental impact. Although much of the C&DW material is inert, non- hazardous, and does not produce greenhouse gases (GHG) in landfill, the amount of C&DW quickly depletes the finite land resources. Notwithstanding legislation (Solid Waste and Public Cleansing Management Act 672) governing solid waste management in Malaysia, C&DW attracts significantly less attention than other forms of waste, such as municipal solid waste and hazardous waste. Malaysia's goals are aligned with UN Agenda on “The Sustainable Development Goals: A Universal Push to Transform Our World” through the current five-year development plan, the 11th Malaysia Plan (11th MP). On climate change, Malaysia is committed to reducing the GHG emission intensity as ratio of its GDP by 45% by the year of 2030. Though the 11th MP only briefly addresses waste management, reusing and recycling of C&DW may contribute to GHG reduction goals, including by reducing the need to harvest new raw material. This waste generation study offers a theoretical method in estimating the C&D waste generation rate by utilizing project site waste records, site survey, and information from waste management plans. -

HEALTH and WELLBEING in the CITY WE NEED AF Olioof a Rtand

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/293480452 THRIVE - HEALTH AND WELLBEING IN THE CITY WE NEED A F o l i o o f A r t a n d Te x t Research · February 2016 CITATIONS READS 0 100 3 authors, including: Uta Christine Dietrich Think City Snd Bhd 49 PUBLICATIONS 1,174 CITATIONS SEE PROFILE Some of the authors of this publication are also working on these related projects: People - Planet - Participation: healthy, just and sustainable urban development View project All content following this page was uploaded by Uta Christine Dietrich on 08 February 2016. The user has requested enhancement of the downloaded file. THRIVE Health and Wellbeing in The Kuching Urban Thinkers Campus the City We Need – A Folio of Art is a three day global event bringing THRIVE and Text addresses a broad range together stakeholders from local HEALTH AND WELLBEING IN THE CITY WE NEED of environmental determinants that government, civil society, industry and influence human health and wellbeing academia to build consensus around 2015 in cities across the globe - a sense of issues for health and wellbeing in urban physical and spiritual place, a sense environments as an input to HABITAT of community, air and water quality, III, Quito, Ecuador, October, 2016. fresh food, housing, quality acoustic and visual surroundings, employment, THRIVE, designed to stimulate thought mobility and transportation, access to and ideas through the power of visual health care services, natural heritage art (sourced mainly from SE Asia) and and green space, security and safety, associated text, has been produced and urban regeneration. -

Productivity, the Engine of National

2 HEIGHTS EDITORIAL Productivity, the Engine of National environmental ratings standards and modern practices by the construction In the modern world, there are many practices. Finally, we want to assure a industry, the goal of a highly skilled, factors at play in the marketplace. high living standard for our high-paid workforce can become Financial strength, business diversity, entire population. reality, making the other three a well-trained labour force, visionary strategic thrusts easier to achieve. leadership, global competition, KLCC Property Holdings and environmental concerns and Putrajaya Holdings are to be Nothing is more important, in our sustainability are all components commended for their initiative in view, than a commitment to of economic health, for individual this effort by adopting BREEAM productivity. It is the engine of companies and for nations. standards for all their projects. The national growth, and without it little science-based rating system was first else matters. But productivity has We face many challenges in Malaysia developed in the UK in 1988. Using its many faces. There are numerous in the coming years. We have metrics, independent auditors rate ways in which Malaysia’s construction witnessed progress toward the goals buildings for overall sustainability industries can be transformed, but that were defined by the Construction in numerous categories, including as we move forward together to meet Industry Transformation Programme energy and water use, health and the goals set in 2016, we must also in 2016, and we fully expect to wellbeing, pollution, transport, recognise that this national agenda continue on the path that was materials, waste, ecology and requires ongoing commitment envisioned when the Four Strategic management processes.