Annual Information Form Dated March 25, 2021

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Service Bulletin TECHNICAL

Bulletin No.: 11-08-49-001Z Service Bulletin Date: March, 2019 TECHNICAL Subject: Transport Mode On Message Displayed in DIC and/or Battery Light is Flashing Models: 2011-2019 Buick Regal 2012-2017 Buick Verano 2013-2018 Buick Encore 2014-2019 Buick LaCrosse 2016-2019 Buick Cascada, Envision 2010-2016 Cadillac SRX 2013-2019 Cadillac ATS, XTS 2014-2016 Cadillac ELR 2014-2019 Cadillac CTS Sedan (VIN A) 2015-2019 Cadillac Escalade Models 2016-2019 Cadillac CT6 2017-2019 Cadillac XT5 2020 Cadillac XT6 2010 Chevrolet Camaro 2016-2019 Chevrolet Camaro 2011-2015 Chevrolet Cruze 2016 Chevrolet Cruze (VIN P) 2016-2019 Chevrolet Cruze (VIN B) 2011-2019 Chevrolet Volt 2012-2014 Chevrolet Orlando (Canada) 2012-2019 Chevrolet Sonic 2013-2019 Chevrolet Spark, Trax 2014 Chevrolet Corvette 2014 Chevrolet Silverado 1500 2014-2016 Chevrolet Spark EV 2014-2017 Chevrolet Caprice PPV, Chevrolet SS 2014-2019 Chevrolet Impala 2014-2015 Chevrolet Malibu 2016 Chevrolet Malibu Limited 2016-2019 Chevrolet Malibu (VIN Z) 2015-2018 Chevrolet City Express 2015-2019 Chevrolet Colorado, Silverado, Suburban, Tahoe 2017-2019 Chevrolet Bolt EV 2018-2019 Chevrolet Equinox 2019 Chevrolet Blazer, Silverado (New Model) 2014 GMC Sierra 1500 2015-2019 GMC Canyon, Sierra, Yukon Models, Yukon XL Models 2017-2019 GMC Acadia 2018-2019 GMC Terrain 2019 GMC Sierra (New Model) Attention: This Bulletin applies to any of the above models that may be Exported from North America. Copyright 2019 General Motors LLC. All Rights Reserved. Page 2 March, 2019 Bulletin No.: 11-08-49-001Z This Bulletin has been revised to add the Model Year 2020 Cadillac XT6 and add the 2017-2019 Cadillac XT5 / 2017-2019 GMC Acadia and 2020 Cadillac XT6 to the Procedure Subsection titled: 2016-2019 Buick Envision / 2018-2019 Chevrolet Equinox, GMC Terrain. -

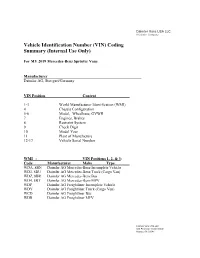

Vehicle Identification Number (VIN) Coding Summary (Internal Use Only)

Daimler Vans USA LLC A Daimler Company Vehicle Identification Number (VIN) Coding Summary (Internal Use Only) For MY 2019 Mercedes-Benz Sprinter Vans Manufacturer Daimler AG, Stuttgart/Germany VIN Position Content 1-3 World Manufacturer Identification (WMI) 4 Chassis Configuration 5-6 Model, Wheelbase, GVWR 7 Engines, Brakes 8 Restraint System 9 Check Digit 10 Model Year 11 Plant of Manufacture 12-17 Vehicle Serial Number WMI - VIN Positions 1, 2, & 3: Code Manufacturer Make Type WDA, 8BN Daimler AG Mercedes-Benz Incomplete Vehicle WD3, 8BU Daimler AG Mercedes-Benz Truck (Cargo Van) WDZ, 8BR Daimler AG Mercedes-Benz Bus WD4, 8BT Daimler AG Mercedes-Benz MPV WDP Daimler AG Freightliner Incomplete Vehicle WDY Daimler AG Freightliner Truck (Cargo Van) WCD Daimler AG Freightliner Bus WDR Daimler AG Freightliner MPV Daimler Vans USA LLC 303 Perimeter Center North Atlanta, GA 30346 Daimler Vans USA LLC A Daimler Company Chassis Configuration - VIN Position 4: Code Chassis Configuration / Intended Market P All 4x2 Vehicle Types / U.S. B All 4x2 Vehicle Types / Canada F All 4x4 Vehicle Types / U.S. C All 4x4 Vehicle Types / Canada Model, Wheelbase, GVWR - VIN Positions 5 & 6: Code Model Wheelbase GVWR E7 C1500/C2500/P1500 3665 mm/ 144 in. 8,000 lbs. to 9,000 lbs. Class G E8 C2500/P2500 4325 mm/ 170 in. 8,000 lbs. to 9,000 lbs. Class G F0 C2500/C3500 3665 mm/ 144 in. 9,000 lbs. to 10,000 lbs. Class H F1 C2500/C3500 4325 mm/ 170 in. 9,000 lbs. to 10,000 lbs. Class H F3 C4500/C3500 3665 mm/ 144 in. -

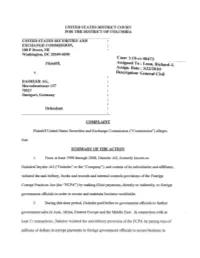

Daimler AG, Formerly Known As

UNITED STATES DISTRICT COURT FOR THE DISTRICT OF COLUMBIA UNITED STATES SECURITIES AND EXCHANGE COMMISSION, 100 F Street,NE Washington, DC 20549-6030 Case: 1:10-cv-00473 Plaintiff, Ass~gned To : Leon, RichardJ-.- ASSIgn. Date: 3/22/2010 v. Description: General Civil DAIMLERAG, .Mercedesstrasse 137 70327 . Stuttgart, Germany Defendant. COMPLAINT PlaintiffUnited States Securities and Exchange Commission ("Commission") alleges that: SUMMARY OF THE ACTION 1. From at least 1998 through 2008, Daimler AG, formerly knoWn as DaimlerChrysler AG ("Daimler" or the "Company"), and certain ofits subsidiaries and affiliates, violated the anti-bribery, books and records and internal controls provisions ofthe Foreign _ Corrupt Practices Act (the "FCPA") by making illicit payments, directly or indirectly, to foreign government officials in order to secure and maintain business worldWide. 2. During this time period, Daimler paid bribes to government officials to further government sales in Asia, Africa, Eastern Europe and the Middle East. In connection With at least 51 transactions, Daimler violated the anti-bribery provision of the FCPA by paying tens of millions of dollars in corrupt payments to foreign government officials to secure business in · Russia,Chilia,Vietnam, Nigeria, Hungary, Latvia, Croatia and Bosnia. These corrupt payments were made through the use ofU.S. mails or the means or instrumentality ofU.S. interstate commerce. 3. Daimler also violated the FCPA's books and records and internal controls provisions in connection with the 51 transactions and at least an additional 154 transactions, in which it made improper payments totaling atleast $56 million to secure business in 22 countries, including, among others, Russia, China, Nigeria, Vietnam, Egypt, Greece, Hungary, North Korea, andIndonesia. -

Innovation and Quality for the International Automotive Industry

Automotive Industry Austria Innovation and Quality for the International Automotive Industry www.investinaustria.at INVEST IN AUSTRIA AUTOMOtive INDustrY 3h All of Europe by Air in Just 3 Hours Helsinki Oslo Stockholm Tallinn 2h Riga Moscow Copenhagen Dublin Vilnius Minsk Amsterdam London Berlin Warsaw Brussels 1h Prague Kiev Paris Luxembourg Bratislava Vienna Berne Kishinev Budapest Ljubljana Zagreb Belgrade Bucharest Madrid Sarajevo Lisbon Pristina Podgorica Sofia Rome Skopje Tirana Ankara Athens Austria’s central location in the heart of Europe makes it the ideal East-West business hub. 2 Invest in Austria Contents 5 The Red-White-Red Automotive Powerhouse 8 The Way Innovations Get into Cars 11 AVL: On the Research-Based Path to Success 12 A Competitive Edge through Knowledge 14 The Cluster: A Success Model with a Future 16 High-Tech Suppliers with Savvy 20 Miba Group: Progress from Passion 22 Non-Stop Production 24 GM Invests in a New Engine Generation 27 The Best Contact Partner for Business Location Issues Editorial: April 2011 Owner&Publisher: Austrian Business Agency, Opernring 3, A-1010 Wien Editor-in Chief: René Siegl Associate Editor: Maria Hirzinger, Karin Schwind-Derdak Design: www.november.at Photos: ACstyria Autocluster GmbH, APA, AVL LIST GmbH, BMW Motoren GmbH, GM Powertrain-Austria, HyCentA Research GmbH, Infineon Technologies Austria AG, KTM-Sportmotorcycle AG, MAN Nutzfahr- zeuge Österreich AG, Miba AG, Schaeffler Austria GmbH, Julius Silver Print: Gugler 3 AUTOMOtive INDustrY Engine production at General Motors Powertrain-Austria. The automobile producer General Motors has put its faith in its Austrian facility since 1982. At that time the first Opel plant opened in Vienna-Aspern. -

FPP8407 X6 F16 January2015.Indd

BMW X6 xDrive35i xDrive40d xDrive50i M50d Sheer www.bmw.co.za/X6 Driving Pleasure BMW X6 PRICE LIST. JANUARY 2015. BMW X6 PRICE LIST. JANUARY 2015. CO2 Tax including 14% VAT X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d 8-speed Sport Automatic Transmission Steptronic 8 002.80 4 411.80 10 773.00 5 540.40 Recommended retail price including 14% VAT but excludes CO2 emissions tax Standard Model X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d 8-speed Sport Automatic Transmission Steptronic 947 500 1 052 500 1 163 000 1 327 000 Exterior Design Pure Extravagance X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d 8-speed Sport Automatic Transmission Steptronic 994 200 1 099 200 1 207 000 – M Sport package X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d 8-speed Sport Automatic Transmission Steptronic 988 000 1 093 000 1 185 400 – Engine Specifi cations and Performance X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d Cylinders/valves 6/4 6/4 8/4 6/4 Capacity (cc) 2 979 2 993 4 395 2 993 Maximum Power (kW/rpm) 225/5 800 - 6 400 230/4 400 330/5 500 - 6 000 280/4 000 - 4 400 Maximum Torque (Nm/rpm) 400/1 200 - 5 000 630/1 500 - 2 500 650/2 000 - 4 500 740/2 000 - 3 000 Acceleration 0 – 100 km/h (s) 6.4 5.8 4.8 5.2 Top speed (km/h) 240 240 250 250 Combined Consumption (l/100 km) 8.5 6.2 9.7 6.6 CO2 (g/km) 198 163 225 174 Code Drivetrain technology X6 xDrive35i X6 xDrive40d X6 xDrive50i X6 M50d SA2TB 8-speed Sport Automatic transmission Steptronic with adaptive transmission control, sporty ■■■■ selector-lever and gearshift paddles on the steering wheel SA217 -

Call for Papers Submit Your International Conference on Gears 2021 Abstract Now!

Source: NORD DRIVESYSTEMS Group Call for Papers Submit your International Conference on Gears 2021 abstract now! Hand in your abstract covering related topics to: l Design, analysis and simulation of gears and transmissions Deadline for abstract l Gear applications submission: November 13th, 2020 l Gear production www.vdi-gears.eu l Possibilities and potential of plastic gears + Accompanying conferences l Materials and lubrication Gear Production 2021 l Testing and monitoring High Performance Plastic Gears 2021 + Exhibition Associated Organisations An event organized by VDI Wissensforum www.vdi-gears.eu September 15–17, 2021, Garching (near Munich), Germany Phone +49 211 6214-201 | Fax +49 211 6214-154 Call for Papers International Conference on Gears 2021 Purpose Call for Submission of Contributions Are you an expert in one of the areas of our topics? Then we call on you to he International Conference on Gears and Trans- make an active contribution to the success of the congress with a missions in Garching/Germany is an established presentation. Tplatform for manufacturers of and researchers on Please submit a brief abstract of max. one A4 size sheet by gears and transmission systems. At the ninth issue of November 13th, 2020 summarizing your presentation. the conference in 2021 you can learn about the latest You can submit your paper at www.vdi-gears.eu. developments and research results from the powertrain industry and academia. Types of Contribution Your contribution can take the form of: State-of-the-art gears transmit power and convert 1. A full presentation: torque and speed with high efficiency and power density If your paper is accepted you will be allowed to speak 20 minutes, with at low noise and therefore determine the performance of additional 5 minutes for discussion and the opportunity to respond to mechanical powertrains. -

Linde Equity Research TSX Performance Review

Linde Equity Research TSX Performance Review 2008 Q2: TSX has strong second quarter thanks to Energy, Materials Canadian market among best performers in the world in Q2 2008 Q2 Sector Returns Energy 24.21% Materials 17 . 16 % S&P/TSX Composite 8.37% Utilities 4.59% Industrials 3.42% Information Technology 2.04% Telecommunications Services 1. 3 1% Consumer Staples 0.17% -5.20% Financials -7.63% Health Care - 11. 4 5 % Consumer Discretionary -15% -10% -5% 0% 5% 10% 15% 20% 25% 30% • TSX 60 (large cap) stocks continued to 2008 Index Returns Q2 YTD outperform the broader market, a trend which S&P/TSX Composite 8.37% 4.58% began in Q2 2007. • The Canadian market again outperformed the US S&P/TSX 60 (Large Cap) 10.18% 6.76% market (S&P 500) in Q2. The S&P/TSX S&P/TSX Mid Cap 2.53% -2.32% Composite returned 8.4% versus -3.2% for the S&P/TSX Small Cap 2.85% -2.22% S&P 500 (-3.9% in Canadian dollar terms). • The dramatic spike in oil prices to around $140 per barrel by quarter-end drove strong Q2 Biggest Contributors Q2 Biggest Detractors performance in energy stocks throughout the Potash Corporation Manulife Financial world. The large weighting of Energy stocks in the Canadian market was the primary reason for Cdn Natural Resources CIBC Canada’s strong relative performance. EnCana Sun Life Financial • Materials stocks were also a strong driver of Suncor Energy Centerra Gold performance. The Canadian Materials sector performed better than comparable sectors in Husky Energy Royal Bank of Canada other countries due its higher exposure to Agrium Magna International fertilizer and gold stocks. -

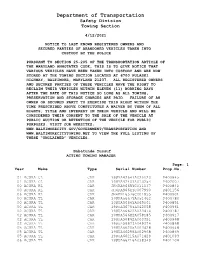

04/12/2021 Unclaimed Vehicle List

Department of Transportation Safety Division Towing Section 4/12/2021 NOTICE TO LAST KNOWN REGISTERED OWNERS AND SECURED PARTIES OF ABANDONED VEHICLES TAKEN INTO CUSTODY BY THE POLICE PURSUANT TO SECTION 25-205 OF THE TRANSPORTATION ARTICLE OF THE MARYLAND ANNOTATED CODE, THIS IS TO GIVE NOTICE THAT VARIOUS VEHICLES HAVE BEEN TAKEN INTO CUSTODY AND ARE NOW STORED AT THE TOWING SECTION LOCATED AT 6700 PULASKI HIGHWAY, BALTIMORE, MARYLAND 21237. ALL REGISTERED OWNERS AND SECURED PARTIES OF THESE VEHICLES HAVE THE RIGHT TO RECLAIM THEIR VEHICLES WITHIN ELEVEN (11) WORKING DAYS AFTER THE DATE OF THIS NOTICE SO LONG AS ALL TOWING, PRESERVATION AND STORAGE CHARGES ARE PAID. FAILURE OF AN OWNER OR SECURED PARTY TO EXERCISE THIS RIGHT WITHIN THE TIME PRESCRIBED ABOVE CONSTITUTES A WAIVER BY THEM OF ALL RIGHTS, TITLE AND INTEREST IN THEIR VEHICLE AND WILL BE CONSIDERED THEIR CONSENT TO THE SALE OF THE VEHICLE AT PUBLIC AUCTION OR RETENTION OF THE VEHICLE FOR PUBLIC PURPOSES. VISIT OUR WEBSITES: WWW.BALTIMORECITY.GOV/GOVERNMENT/TRANSPORTATION AND WWW.BALTIMORECITYTOWING.NET TO VIEW THE FULL LISTING OF THESE “UNCLAIMED” VEHICLES. Babatunde Yussuf ACTING TOWING MANAGER Page: 1 Year Make Type Serial Number Prop.No. 01 ACURA CL CAR 19UYA42641A025120 P400945 01 ACURA CL CAR 19UYA42401A013254 P402007 00 ACURA RL CAR JH4KA9665YC011137 P400840 00 ACURA RL CAR JH4KA966XYC007990 P401156 06 ACURA RL CAR JH4KB16576C001955 P400901 00 ACURA TL CAR 19UUA5667YA051462 P400780 00 ACURA TL CAR 19UUA5664YA065061 P400851 00 ACURA TL CAR 19UUA5679YA042058 P400961 02 ACURA TL CAR 19UUA56622A033474 P400787 02 ACURA TL CAR 19UUA566X2A058185 P400917 02 ACURA TL CAR 19UUA56862A000351 P400968 03 ACURA TL CAR 19UUA56973A049374 P400868 05 ACURA TL CAR 19UUA66205A003428 P400648 05 ACURA TL CAR 19UUA66255A002968 P400869 05 ACURA TL CAR 19UUA66215A071429 P401093 06 ACURA TL CAR 19UUA66216A038349 P401104 Department of Transportation Safety Division Towing Section Newspaper Advertisement Listing Schedule for 4/12/2021 Page: 2 Year Make Type Serial Number Prop.No. -

Provider List Contents

Provider List Contents Provider Rating Only Supports eSignatures AFAS ......................................................................Yes ...................... 1 Allstate ..................................................................Yes ...................... 2 Allstate GAP ..............................................................Yes ...................... 3 Ally (APP Products) .......................................................Yes ...................... 4 Alpha Warranty Services ...................................................Yes ...................... 5 American Auto Guardian ....................................................Yes ...................... 6 American Guardian Warranty Services (AGW ..................................Yes ...................... 7 APPI ................................................................................................ 8 ArmorAll ............................................................................................ 9 ASC Warranty ....................................................................................... 10 ASI Profits ........................................................................................ 11 AssurancePlus ...................................................................................... 12 Audi Financial Services ............................................................................ 13 AUL ................................................................................................ 14 AutoXcel .......................................................................................... -

“Data Security Will Be a Key Challenge” Interview with Jake Hirsch, Magna Powertrain

The AutomotiveCTI TM, HEV & EV DrivesMAG magazine by CTI # May 2017 Expert Forum: Will China Drive Global Powertrain Electrification? ECU Consolidation to Dominate the new E/E Interview with Jake Hirsch, Architectures for President, Magna Powertrain: Powertrain in Hybrid “Data Security will be a and Electric Vehicles Key Challenge” Innovations in motion Experience the powertrain technology of tomorrow. Be inspired by modern designs that bring together dynamics, comfort and highest efficiency to offer superior performance. Learn more about our perfect solutions for powertrain systems and discover a whole world of fascinating ideas for the mobility of the future. Visit us at the CTI Symposium and meet our experts! www.magna.com CTIMAG Contents 6 Expert Forum – Will China Drive Global Powertrain Electrification? CTI 10 P3 Hybridization of Manual Transmissions GETRAG Ford Transmissions GmbH, Magna Powertrain 13 ECU Consolidation to Dominate the new E/E (Electrical/Electronic) Architectures for Powertrain in Hybrid and Electric Vehicles IHS Markit 16 “It’s a Cat-and-Mouse Game” Interview with Bob Gruszczynski, Volkswagen and SAE E/E Diagnostics Committee 19 “Data Security will be a Key Challenge” Interview with Jake Hirsch, Magna Powertrain 22 HOERBIGER Cone Clutch Design yields Fuel Savings for Automatic Transmissions HOERBIGER 25 Today and for a (Vehicle’s) Lifetime W.S. Tyler 26 Modification of Surface Structure and Geometry on Gears Reishauer 30 Engineered Plastics Thrust Bearings for Transmission Applications Freudenberg-NOK Sealing Technologies 33 Polymeric Thrust Bearings Offer Innovative Approach to Light-weight Transmissions & Packaging Flexibility Solvay Specialty Polymers 37 Closed Loop Gear Machining (CLGM) – 5 Axis CNC Gear Process Dontyne / Mazak 40 Improve Precision and Production. -

Magna International Inc. (Exact Name of Registrant As Specified in Its Charter)

United States Securities and Exchange Commission Washington, D.C. 20549 FORM 40-F ☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12 OF THE SECURITIES EXCHANGE ACT OF 1934 OR ☒ ANNUAL REPORT PURSUANT TO SECTION 13(a) or 15(d) of THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2018 Commission File Number 001-11444 Magna International Inc. (Exact name of Registrant as specified in its charter) Not Applicable (Translation of Registrant’s name into English (if applicable) Province of Ontario, Canada (Province of other jurisdiction of incorporation or organization) 3714 (Primary Standard Industrial Classification Code number (if applicable) Not Applicable (I.R.S. Employer Identification Number (if applicable) 337 Magna Drive, Aurora, Ontario, Canada L4G 7K1 (905) 726-2462 (Address and telephone number of Registrant’s principal executive offices) Corporation Service Company, 1180 Avenue of the Americas, Suite 210 New York, New York 10036-8401 Telephone 212-299-5600 (Name, address (including zip code) and telephone number (including area code) of agent for service in the United States) Securities registered or to be registered pursuant to Section 12(b) of the Act. Title of each class Name of each exchange on which registered Common Shares New York Stock Exchange Securities registered or to be registered pursuant to Section 12(g) of the Act. None Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act. None For annual reports, indicate by check mark the information filed with this Form: ☒ Annual Information Form ☒ Audited Annual Financial Statements Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report. -

Michigan Auto Project Progress Report - December 2000 I Inaugural Progress Report Michigan Automotive Pollution Prevention Project

A VOLUNTARY POLLUTION PREVENTION AND RESOURCE CONSERVATION PARTNERSHIP ADMINISTERED BY: Michigan Department of Environmental Quality Environmental Assistance Division DECEMBER, 2000: 1st ISSUE John Engler, Governor • Russell J. Harding, Director www.deq.state.mi.us ACKNOWLEDGMENTS DaimlerChrysler Corporation, Ford Motor Company, General Motors Corporation and the Michigan Department of Environmental Quality (MDEQ) thank the Auto Project Stakeholder Group members for providing advice to the Auto Project partners and facilitating public information exchange. The Auto Companies and MDEQ also acknowledge the guidance and counsel provided by the US EPA Region V. CONTACTS FOR ADDITIONAL INFORMATION For information regarding the Michigan Automotive Pollution Prevention Project Progress Report, contact DaimlerChrysler, Ford, or General Motors at the addresses listed below or the Environmental Assistance Division of the Michigan Department of Environmental Quality at 1-800-662-9278. DaimlerChrysler Ford Doug Orf, CIMS 482-00-51 Sue Rokosz DaimlerChrysler Corporation Ford Motor Company 800 Chrysler Drive One Parklane Blvd., Suite 1400 Auburn Hills, MI 48326-2757 Dearborn, MI 48126 [email protected] [email protected] General Motors MDEQ Sandra Brewer, 482-303-300 Anita Singh Welch General Motors Corporation Environmental Assistance Division 465 W. Milwaukee Ave. Michigan Department of Environmental Quality Detroit, MI 48202 P.O. Box 30457 [email protected] Lansing, MI 48909 [email protected] Michigan Auto Project Progress Report - December 2000 i Inaugural Progress Report Michigan Automotive Pollution Prevention Project TABLE OF CONTENTS Page Foreward iv I. Executive Summary Project Overview 1 Activities and Accomplishments 4 Focus on Michigan 11 Auto Company Profiles II. DaimlerChrysler Corporation Project Status 12 Activities and Accomplishments 14 Focus on Michigan 16 III.