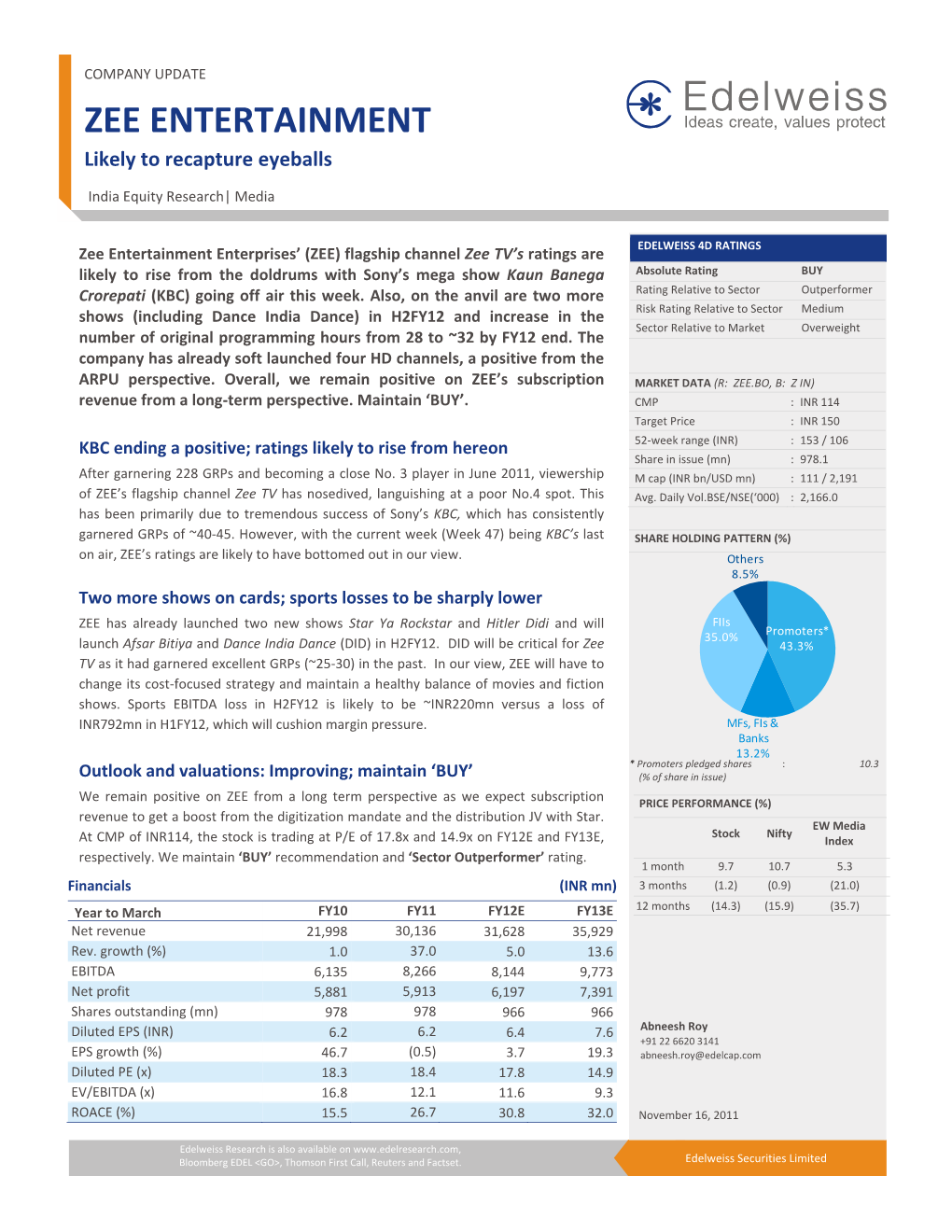

ZEE ENTERTAINMENT Likely to Recapture Eyeballs

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Rate Card Applicable for DTH Operators As Per The

Rate Card applicable for DTH Operators as per the Telecommunication (Broadcasting and Cable) Services (Fourth) (Addressable Systems) Tariff Order, 2010 dated 21st July 2010 (“Tariff Order”) A-La-Carte Rates: Sr. Rate to Operator per No Channels Subscriber per Month (Rs) 1 STAR Plus 7.87 2 STAR Gold 7.42 3 STAR Movies 7.42 4 STAR World 2.05 5 NGC 2.58 6 Fox Traveller 1.98 7 Channel V 0.45 8 Vijay TV 1.80 (Rs. 5.30 for TN) 9 ABP News FTA 10 Zee TV 5.83 11 Zee Cinema 5.83 12 Cartoon Network 5.62 13 Zee Marathi 3.60 14 Zee News 3.37 15 CNN 0.67 16 Zee Café 3.60 17 Zee Studio 3.15 18 Zee Trendz 0.45 19 Zee Punjab Haryana Himachal 0.67 20 Zee Bangla 3.64 21 Fox Crime 6.51 22 Nat Geo Wild 6.72 23 Life OK (Erstwhile STAR ONE) Effective from 18th December, 2011 9.21 24 MGM 2.70 25 HBO 7.01 26 Pogo 5.62 27 Zee Business 2.16 28 WB 2.77 29 FX 6.51 30 Baby TV 5.57 31 Nat Geo People 6.72 32 Nat Geo Music 3.11 33 Zee Salaam 6.30 34 Zee Uttar Pradesh Uttarakhand ( erstwhile FTA Zee News Uttar Pradesh) Effective from 11th June, 2013 35 ETC Punjabi 4.04 36 ETC 1.35 37 Zing 2.25 38 Zee Jagran 0.90 39 ABP Ananda 2.52 40 Star Jalsha 5.04 41 Zee 24 Ghante 2.70 42 Zee Talkies 6.96 43 Zee 24 Taas 3.82 44 NDTV India 3.37 45 NDTV 24*7 3.82 46 NDTV Profit 2.70 47 NDTV Good Times 4.04 48 Star Pravah 5.04 49 ABP Majha (FTA to Pay w.e.f. -

Group Ceiling As on 16Th Dec 2012 .Xlsx

List of empanelled Channel groups & ceilings (w.e.f 26th dec 2012) Ceiling as per revised Sl.NO. Company Name Channel Name guidelines ETV Bangla ETV Marathi ETV Gujarati ETV Oriya ETV Telugu ETV Kannada 1 Ushodaya Enterprised Ltd. 12% ETV Urdu ETV MP ETV UP ETV Bihar ETV - 2 ETV Rajasthan 2 Jaya TV Jaya TV 2% Colors MTV 3 Vaicom 18 Nick 8% VH1 SONIC News Live 4 Pride East Entainments Pvt. Ltd Rang 8% RAMDHENU Cartoon Network 5 Turner International(Affidavit not given) 8% Pogo 6 UTV Entertainment Television Ltd. UTV ACTION TELUGU 2% Discovery Animal Planet TLC 7 Discovery Communication India 8% DISCOVERY TURBO DISCOVERY CHANNEL TAMIL DISCOVERY SCIENCE TV9 Karnataka TV1-Telugu TV 9 Associated Broadcasting Company Pvt TV9(Telugu) 8 8% Ltd TV9(Maharashtra) TV9(Gujarat) NEWS 9 PTC News 9 G-Next Media Pvt Ltd PTC Chak De 8% PTC Punjabi Kairali 10 Malayalam Communications Ltd 8% WE B4U Music 11 B4U Broadband(Affidavit not given) 8% B4U Movies Asianet Plus Suvarna 12 Asianet News Network Pvt. Ltd. Sitara 8% Asianet News Suvarna News Vijay TV Star Pravah Star Jalsha 13 Star India Pvt. Ltd. Star Plus 12% Star Utsav Star Gold Channel V NE Hi FI NE TV Hamar TV 14 Positiv Television Pvt. Ltd. 8% NE Bangla HY TV Focus TV Raj TV Raj Digital Plus Raj Music 15 Raj Television Network Ltd. Vissa 12% RAJ MUSIC KARNATAKA RAJ NEWS 24X7 Raj News Telugu 16 M.H One TV Network Ltd. Shradha MH One 2% NTV Rachna Television Pvt. Ltd.(Only affidavit 17 8% submitted and not acceptance) Bhakti TV Vanitha TV O TV Tarang 18 Odisha Television Ltd. -

Meghbela Digital DAS Packages (Rs

Sheet1 Meghbela Digital DAS Packages (Rs. Per month excluding tax) PLATINUM DIGITAL ₹ 290 p.m. (Taxes Extra) PAY SONY AATH, STAR JALSHA, ZEE BANGLA, ETV BANGLA Bengali R PLUS GOLD, OM BANGLA, RUPASHI BANGLA, DD BANGLA, CTVN AKD PLUS, UTTAR BANGLA, ATN BANGLA, AAMAR BANGLA, Entertainment FTA CHANNEL VISION, BENGAL WATCH, SONAR BANGLA PAY JALSHA MOVIES, ZEE BANGLA CINEMA Bengali Movies FTA PLANET M CINEMA, OPERA BENG PAY ABP ANANDA, 24 GHANTA Bengali News CHANNEL 10, KOLKATA TV, AKASH BANGLA, NEWS TIME, HIGH NEWS, AKHON SOMOY, VOICE 24 TRIPURA, R PLUS, TARA FTA NEWS, MX5, VOX Bengali Music FTA DHOOM MUSIC, TARA MUZIK, SANGEET BANGLA SAB, SONY, CHANNEL V, STAR UTSAV, ZEE SMILE, STAR PLUS, LIFE OK, ZEE TV, STAR VIJAY, 9X, ETC BOLLYWOOD, UTV STAR, PAY Hindi UTV BINDASS, COLORS, SAHARA ONE, ZOOM Entertainment FTA DABANGG, DD INDIA, DD NATIONAL, EXPRESS ENTERTAINMENT English PAY COMEDY CENTRAL, AXN, STAR WORLD, FX, BIG PRIME, WB, BIG LOVE, BIG MAGIC Entertainment FTA TV5, RTR PLANETA, FRANCE 24, GOD TV ASIA, MARINE BIZ TV, ERT WORLD, KUNGFU, EURONEWS, RUSSIA TODAY, DW-TV, SONY MAX, ZEE CINEMA, STAR GOLD, ZEE ACTION, ZEE CLASSIC, ZEE PREMIER, MOVIES OK, UTV ACTION, UTV MOVIES, PAY Hindi Movies FILMY, FIRANGI FTA MOVIE OPERA, OPERA +, CAS TV DIGITAL, CINEMA TV, B4U MOVIES, MANORANJAN TV, ENTER 10 English Movies PAY SONY PIX, HBO, STAR MOVIES, ZEE STUDIO, ZEE CAFÉ, FOX ACTION MOVIES, MGM, UTV WORLD MOVIES, BIG THRILL IBN 7, IBN LOKMAT, ZEE NEWS UP, AAJ TAK, NDTV INDIA, ABP NEWS, ZEE NEWS, TEZ, HEADLINES TODAY, INDIA TV, ZEE 24 PAY TAAS Hindi News -

Packing a Punch Meeting Brands Sunil Lulla

November 1-15, 2013 Volume 2, Issue 12 `100 27 The last couple of years have seen much action in the television broadcasting business in India. An exhaustive report on what is happening. 24 70 38 PLUS MICROMAX Hugh Deal 6 TATA SKY Pocket Entertainment 16 TELEVISION 66 E-COMMERCE INTERVIEW AFAQS! EVENTS It’s all About Timing Packing a Punch Sunil Lulla Meeting Brands PUBLICIS BEEHIVE The box is as important as TTN’s CEO on what ad Chennai-based entrepreneurs what comes out of it. regulation actually means. decode brand values. Scaling Up 69 EDITORIAL This fortnight... Volume 2, Issue 12 oing by all the action in the past year or so you wouldn’t believe that television is a mature business that has been around for a long time. Indian television has EDITOR G Sreekant Khandekar November 1-15, 2013 Volume 2, Issue 12 `100 been going through the pangs of digitisation. It has been in a ferment about television PUBLISHER 27 ratings which have been affected by the inclusion of small-town India. And now it is Prasanna Singh trying to fathom what the coming capping of advertising time will mean to their balance SENIOR LAYOUT ARTIST sheets. The year 2013 has also seen a scrap between broadcasters and agencies (backed Vinay Dominic by advertisers) on the nature of billing (gross vs net) and yet another skirmish on the PRODUCTION EXECUTIVE way television viewership is presented. Andrias Kisku All of this action has also affected programming and what people watch in a big way. ADVERTISING ENQUIRIES Naveen Arora, (0120) 4077803, 4077866 Digitisation has encouraged the launch of many specialised channels – for example, four Noida The last couple of years have seen much action in the new channels have been launched in English alone because viewership in the genre has television broadcasting business in India. -

Siti Digital Cable Tv Package Creator a Truly Flexible Viewing Experience Janta (Bst) 100.00 Pm Popular 205.00 Pm Gr

(index.aspx) Toll Free :1800 1234 001 Find a local cable operator VEnietwer BPiilnl c o(dDeashboardBillingHistory.aspx) SITI DIGITAL CABLE TV PACKAGE CREATOR A TRULY FLEXIBLE VIEWING EXPERIENCE Base Pack Selection Ὃ Base Pack 175.00 KOLKATA Change Step1: Select a base pack. JANTA (BST) POPULAR GRAND PREMIUM 100.00 PM 205.00 PM 265.00 PM 325.00 PM View Channels View Channels View Channels View Channels POPULAR GRAND PREMIUM ECONOMY ECONOMY ECONOMY 175.00 PM 220.00 PM 265.00 PM Close View Channels View Channels Close View Channels View Channels Taxes Extra Popular Economy 172 Channel(s) Bangla Entertainment 14 Channel(s) Channel Vision City Gold CTVN DD Bangla ETV Bangla MX5 Rupashi Bangla Srijan TV Sristi TV U Bangla Uttar Bangla Zee Bangla Aakash Aath Sonar Bangla Bangla Music 5 Channel(s) Music F Sangeet Bangla Tara Music Planet M Music Music Bangla Bangla Movies 7 Channel(s) Metro Orange TV Planet M SITI CINEMA Sony Aath Cinema ZEE Bangla Home TV Cinema Bangla News 12 Channel(s) Channel 10 ETV Bangla Focus Bangla High News Kolkata TV News News Time Onkar News R Plus Sabar Bangla Tara News Bangla 24 Ghanta ABP Ananda Hindi Entertainment 19 Channel(s) Bindass Play Blue Naaptol Colors DD Bharati DD India DD National Home Shop 18 Rishtey SAB TV Siti Romance Sony Star CJ Alive Bindass Zee Anmol Zee Smile Zee TV Zindagi Zoom 9X Hindi Movies 10 Channel(s) B4U Movies Cinema TV MOC Set Max SITI BOLLYWOOD UTV Action UTV Movies Zee Action Zee Cinema & Pictures Hindi News 13 Channel(s) Lok Sabha TV DD News DD Rajya Sabha IBN7 India TV NDTV India -

Zee Telefilms Limited

ZEE TELEFILMS LIMITED Zee Telefilms is India's largest vertically integrated Zee Telefilms Middle East F.Z.L.L.C to handle media and entertainment company. broadcasting operations for the Middle East from the Dubai Media City. Background The promoters currently hold 46.67 per cent stake Zee Telefilms is the pioneer of satellite broadcasting in the company. Foreign institutional investors, in India and is one of the first private-sector overseas corporate bodies and non-resident entrants to the Indian broadcasting industry. It Indians hold 41.60 per cent stake while the mutual launched its flagship television channel Zee TV, in funds, banks and financial institutions hold 6.46 per the year 1992. Since then, it has transformed itself cent stake. Individuals including public holds 4.18 into an integrated media conglomerate with per cent stake while the domestic companies hold operations spanning the entire media spectrum, the remaining stake of 1.09 per cent. including television programming, satellite broadcasting, cable distribution, production and Products and brands distribution of films, music publishing, long distance education and creation of animation software. The operations of the company consist of four main segments viz. Content and Broadcasting, The company currently broadcasts 22 television Access, Education and Film Production and channels in seven languages in India and abroad and Distribution. reaches out to more than 250 million people across 120 countries.The company's channels are The company's Content and Broadcasting segment, beamed either from its fully owned facility in which comprises production and aggregation of TV Singapore or from Hong Kong. -

Platinum Pack

PLATINUM PACK HINDI ENTERTAINTMENT CARE WORLD CARE WORLD COLORS SONY ZEE TV SAHARA ONE SAB TV BIG MAGIC ZOOM BINDASS UTV STARS 9X ENT ZEE SMILE E24 DD BHARTI DD NATIONAL STAR USTAV STAR ALIVE LIFE OK STAR PLUS CHANNEL V HINDI MOVIES SAHARA FILMY SET MAX ZEE CINEMA FIRANGI CINEMA TV UTV MOVIES UTV ACTION BIG RTL THRILL CVO MOVIE OK STAR GOLD ZEE ACTION ZEE PREMIER ZEE CLASSIC CABLE 1 CABLE 2 ENGLISH ENTERTAINTMENT SPARK BIG CBS LOVE BIG CBS COMEDY CENTRAL ZEE CAFÉ ZEE TRENDZ STAR WORLD FOX CRIME FOX FX ENGLISH MOVIES HBO MOVIES NOW SONY PIX WB ZEE STUDIO MGM UTV WORLD MOVIES HBO HITS SD HBO DEFINED SD STAR MOVIES ACTION STAR MOVIES HINDI NEWS IBN7 NDTV INDIA NEWS XPRESS SAHARA SAMAY Sahara Mumbai ZEE NEWS 7 SEA CNBC AWAZ ZEE BUSINESS INDIA TV ABP NEWS AAJ TAK INDIA NEWS TEZ P7 NEWS NEWS 24 DD NEWS DD LOKSABHA DD RAJYASABHA LEMON NEWS CHANNEL ONE NEWS ENGLISH NEWS TIMES NOW NDTV 24/7 CNN IBN News X HEADLINES TODAY CNN BBC WORLD RUSSIA TODAY ALJAZEERA ET NOW NDTV PROFIT CNBC TV - 18 BLOOMBERG TV DW TV TV5 ASIA MUSIC MTV SONY MIX MUSIC EXPRESS M TUNES ZEE MUSIC ETC Mastiii B4U Music 9X JALWA VH1 NG MUSIC CHILDREN POGO DISCOVERY KIDS CARTOON NETWORK ANIMAX NICK DISNEY DISNEY XD HUNGAMA SONIC NICK JR BABY TV BBC CBEEBIES SPORTS SONY SIX ESPN STAR SPORTS STAR CRICKET Star Sports 2 NEO PRIME NEO SPORTS TEN SPORTS TEN ACTION TEN CRICKET DD SPORTS INFOTAINMENT HISTORY TV 18 DISCOVERY DISCOVERY SCIENCE PRIME BIG CBS ANIMAL PLANNET NG AVDVENTURE NG WILD NGC LIFESTYLE NDTV GOOD TIMES TLC DISCOVERY TURBO FOOD FOOD ZEE KHANA KHAZANA FOX TRAVELLER EXPLORE -

D:\Channel Change & Guide\Chann

CHANNEL GUIDE UPDATED AS OF 1ST JULY 2020 FTA = Free To Air SCR = Scrambled Radio Channels in Italics FREQ/POL CHANNEL SR FEC CAS NOTES ARABSAT 5C at 20.0 deg E: Bom Az 256 El 27, Blr Az 262 El 24, Del Az 253 El 20, Chen Az 263 El 21, Bhopal Az 256 El 21, Cal Az 261 El 11 S 3796 LSRTV 1850 3/4 FTA A 3809 RSSBC TV 1600 2/3 FTA T E 3853 L Espace TV 1388 3/5 Mpeg4 FTA L L 3884 R Iqraa Arabic, ERI TV1, Ekhbariya TV, KSA Sports 2, 2M Monde, El Mauritania. Canal Algeria, Al Maghribia 27500 5/6 FTA I T 3934 L ASBU Bouquet: South Sudan TV, Abu Dhabi Europe, Oman TV, KTV 1, Saudi TV, Sharjah TV, Quran TV, Sudan TV, Sunna TV, E Libya Al Watanya; Holy Quran Radio, Emarat FM, Program One, Radio Quran, Qatar Radio, Radio Oman 27500 7/8 FTA & 3964 L Al Masriyah, Al Masriyah USA, Nile Tv International, Nile News, Nile Drama, Nile Life, Nile Sport, ERTU 1 27500 3/4 FTA C A BADR 5 at 26 deg East: Bom Az 253 El 33.02, Blr Az 259.91 El 29.71, Del 248.93 El 25.47, Chennai Az 260.76 El 26.88, Bhopal Az 252 El 27 B L 4087 L Tele Sahel 3330 3/4 FTA Medium Beam E T 4102 L TNT Niger: Télé Sahel, Tal TV, Espérance TV, Liptako TV, Ténéré TV, Dounia TV, Canal 3 Niger, Canal 3 Monde, Saraounia TV, V Bonferey, Tambara TV, Anfani TV, Labari TV, TV Fidelité, Niger 24, Télé Sahel, Tal TV, Voix du Sahel 20000 2/3 FTA MPEG-4 Medium Beam IRIB: IRIB 1, IRIB 2, IRIB 3 (scr), IRIB 4, IRIB 5, IRINN, Amouzesh TV, Quran TV, Doc TV, Namayesh TV, Ofogh TV, Ifilm, Press 11881 H TV, Varzesh, Pooya, Salamat, Nasim, Tamasha HD, IRIB 3 HD (scr), Omid TV, Shoma TV, Tamasha, Alkhatwar TV, Irkala TV, 27500 5/6 FTA MPEG-4 Central Asia beam Sepehr TV HD; Radio Iran, Radio Payam, Radio Jawan, Radio Maaref etc 11900 V IRIB: IRIB 1, IRIB 2, IRIB 3, IRINN, Amouzesh TV, Salamat TV, Sepehr HD; Radio Iran, Radio Payam, Radio Jawan, Radio Maaref etc. -

Top Companies That Hire Mass Communication Graduates Updated On: Feb 22, 2017

Top companies that hire mass communication graduates Updated on: Feb 22, 2017 Chhavi Sharma 3.8K Views Best Media Companies that hire Mass Communication Graduates Mass Communication is a very diverse field and anyone looking to make a career in it should be very clear about the profile he/she wishes to work in. View list of mass communication job profiles. Apart from this, mass communication as a career profile explores different media arenas such as newspapers, magazines, television, radio, event management, advertisements and public relations. Thus, aspirants need to keep this in mind when they head out to join their dream firm because there is a high possibility that the job profile you are seeking isn’t offered at the organisation you wish to work for. Disclaimer: This PDF is auto-generated based on the information available on Shiksha as on 05-Jun-2020. In this article, we will be listing the most popular companies that offer jobs to mass communication graduates. Also, aspirants need to note that the easiest way to secure a job at a media organisation is by interning with them for a short period of time. Hindustan Times Headquarters: New Delhi One of the largest English language daily newspaper, Hindustan Times also hires for its supplements – Brunch, HT City and HT Cafe, HT Education, HT Estates, Shine Jobs, HT Livebhopal. It has sister publications like Hindustan (Hindi Daily), Mint (English business daily), Kadambani (monthly literary magazine) and Nandan (monthly children's magazine). This media group also owns Fever 104 FM, a radio station. Times Group Headquarters: New Delhi/ Noida Owned by Bennett, Coleman and Company Limited, Times Group has under its ambit five dailies, twenty-nine niche magazines and thirty-two Radio Stations. -

Inspired Leadership

Zee Entertainment Enterprises Limited Annual Report 2010-11 Inspired Leadership Zee Entertainment Enterprises Limited Registered & Corporate Office Continental Building 135, Dr. Annie Besant Road, Zee Entertainment Enterprises Limited Enterprises Entertainment Zee Worli, Mumbai 400018 Maharashtra, India. Tel. +91 22 6697 1234 Fax +91 22 2490 0302 www.zeetelevision.com Annual Report 2010-11 Annual Report Inspired Leadership Forward-looking statement In this Annual Report, we have disclosed forward looking information to enable investors to comprehend our prospects and take investment decisions. This report and other statements - written and oral, that we periodically make contain forward looking statements that set out anticipated results based on the management’s plans and assumptions. We have tried, wherever possible, to identify such statements by using words such as ‘anticipate’, ‘estimate’, ‘expects’, ‘projects’, ‘intends’, ‘plans’, ‘believes’, and words of similar substance in connection with any discussion of future performance. We cannot guarantee that these forward looking statements will be realised, although we believe we have been prudent in our assumptions. The achievements of results are subject to risks, uncertainties and even inaccurate assumptions. Should known or unknown risks or uncertainties materialize, or should underlying assumptions prove inaccurate, actual results could vary materially from those anticipated, estimated or projected. Readers should keep this in mind. We undertake no obligation to publicly update -

On Tariff Issues Related to Cable TV Services in Non-CAS Areas

Report on Tariff issues related to Cable TV services in non-CAS areas submitted to the Hon’ble Supreme Court of India in pursuance of its Orders dated 13th May, 2009 passed in Civil Appeal Nos.829-833 of 2009 by Telecom Regulatory Authority of India (TRAI) New Delhi: July 21, 2010 Mahanagar Doorsanchar Bhawan Jawahar Lal Nehru Marg New Delhi- 110 002 1 Table of Contents Page Nos. Glossary of Terms 3 Chapter I: Introduction 5 Chapter II: Industry Scenario 25 Chapter III: Tariff 58 Chapter IV: Carriage and Placement Fee 121 Tariff Order 137 Annexures Annexure I Orders of Hon‟ble Supreme Court 156 Annexure II Tariff regulation in the broadcasting and cable 182 sector Annexure III List of events/steps taken by TRAI since 190 13.05.2009 for completion of the tariff exercise for Non-CAS areas Annexure IV Summary of issues raised in the consultation 198 paper Annexure V List of Pay TV Channels and their prevalent 202 rates Annexure VI Television receipt capacity Vs number of 208 channels received: non-CAS Households 2 GLOSSARY OF TERMS ARPU : Average Revenue Per User BSNL : Bharat Sanchar Nigam Limited B2B : Business To Business transaction CAG : Consumer Advocacy Group CAS : Conditional Access System C&S : Cable and Satellite CBET : Central Bureau of Excise and customs, service Tax CMS : Centre of Media Studies CODA : Cable Operators and Distribution Alliance COFI : Cable Operators Federation of India Cr. : Crore d2h : Direct To Home service of Videocon DTH Operator DD : Door Darshan DTH : Direct To Home EBITDA : Earnings Before Interest, Taxes, Depreciation and Amortization FICCI : Federation of Indian Chambers of Commerce and Industry. -

Management Discussion and Analysis |

| NOTICE | DIRECTORS’ REPORT | CORPORATE GOVERNANCE REPORT | MANAGEMENT DISCUSSION AND ANALYSIS | MANAGEMENT DISCUSSION AND ANALYSIS OVERVIEW Zee Entertainment Enterprises Limited (ZEE) (BSE Code: 505537, NSE Code: ZEEL.EQ) is one of India’s largest vertically integrated media and entertainment company. The Company was formed in 1982. ZEE was the first company to launch a satellite channel in India and from being a single channel for a single geography today operates multiple channels across multiple geographies in different languages and genres. The Company’s programming reaches out to over 670 million viewers across 169 countries. ZEE channel portfolio, across various genres in the Indian market, includes: i. Hindi Entertainment: Zee TV, Zee Smile, 9X ii. Hindi Movies: Zee Cinema, Zee Premier, Zee Action, Zee Classic iii. English Entertainment, Movies and Life style: Zee Studio, Zee Café, Zee Trendz iv. Regional Language Entertainment: Zee Marathi, Zee Bangla, Zee Bangla Cinema, Zee Talkies, Zee Telegu, Zee Kannada, ETC Punjabi, Zee Tamil v. Sports: TEN Cricket, TEN Action, TEN Sports, TEN Golf vi. Religious and Alternate Lifestyle: Zee Jagran, Zee Salaam vii. Music: Zing, ETC viii. Niche and Special Interest: Zee Khana Khazana and Zee Q ix. HD: Zee TV HD, Zee Cinema HD, Zee Studio HD, TEN HD 62 ANNUAL REPORT 2012-13 CORPORATE OVERVIEW OPERATIONAL OVERVIEW BOARD & MANAGEMENT REPORTS FINANCIAL STATEMENTS Apart from the channels listed above which are available in India, the Company also broadcasts 29 dedicated channels in the international markets. ZEE has 5 channels, viz. Zee Cinema, MEDIA AND ENTERTAINMENT INDUSTRY The Indian Media and Entertainment Industry witnessed a slow growth in 2012.