Financial Information

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Hayleys Fibre Plc Annual Report 2019/20

Integral Integration HAYLEYS FIBRE PLC ANNUAL REPORT 2019/20 It has truly been a year of Integration as we took extensive strides in upgrading all aspects of the company through new systems, ventures and centralised resource mobilising. While paying special attention to logistical cohesion, we are taking the next carefully planned steps in expanding our reach. This includes the diversification of our products and its introduction to new markets. Our adoption of the “best” is propelling us to be the best in the business. CONTENTS History of the Business / 3 Financial Highlights / 4 Joint Statement from the Chairman and the Managing Director / 6 Our Product Portfolio / 10 Operational Review and Management Discussion / 14 GOVERNANCE Profiles of Directors /22 Statement of Directors’ Responsibility / 25 Annual Report of the Board of Directors on the Affairs of the Company / 26 Responsibility Statement of Chairman, Managing Director and Chief Financial Officer 30/ Corporate Governance / 31 Risk Management / 38 Related Party Transactions Review Committee Report / 43 Audit Committee Report / 44 FINANCIAL REPORTS Independent Auditor’s Report / 46 Statement of Profit or Loss /50 Statement of Comprehensive Income / 51 Statement of Financial Position / 52 Statement of Changes in Equity / 53 Statement of Cash Flows / 55 Notes to the Financial Statements / 56 SUPPLEMENTARY INFORMATION Share Information / 110 Statement of Value Added / 112 Ten Year Summary - Group / 113 Notice of Meeting / 114 Form of Proxy / 115 Corporate Information (Inner Back Cover) HISTORY OF THE BUSINESS A subsidiary of the blue-chip, Hayleys Group of Sri Lanka, VISION Hayleys Fibre PLC is a manufacturer and exporter of coir To be the leading provider of based, eco friendly products with a growing international innovative, sustainable and market. -

Expolanka Holdings Plc Integrated Annual Report

EXPOLANKA HOLDINGS PLC INTEGRATED ANNUAL REPORT 2020/21 EXPOLANKA HOLDINGS PLC | INTEGRATED REPORT 2020/21 2 fruitionEXPOLANKA HOLDINGS PLC | INTEGRATED ANNUAL REPORT 2020/21 At Expolanka, we remain fully committed to our promise made several years ago, to drive long term sustainable value, by adapting a focused, constant and consistent strategy. Even though the year under review post several challenges, we were able to pursue our said strategies and bring to fruition our plans for progress which was fueled by our innate resilience and strength. The seeds we planted have taken root and we keep our focus upward, expanding in our focused direction in order to adapt to the current environment. We remain fruitful in our optimism, our can-do attitude and endurance, a recipe for success that will carry us through to more opportunity. Overview EXPOLANKA HOLDINGS PLC | INTEGRATED ANNUAL REPORT 2020/21 2 CONTENTS Chairman’s Overview Compliance Reports 12 About Us 3 Corporate Governance 71 Message About this Report 4 Risk Management Report 93 Group Milestones 5 Related Party Transactions Financial Highlights 6 Review Committee Report 101 15 Group CEO’s Highlights of the Year 7 Remuneration Committee Report 103 Review Chairman’s Message 12 Group CEO’s Review 15 Financial Reports Board of Directors 18 Annual Report of the Board of Directors Group Senior Management Team 20 on the Affairs of the Company 108 23 Financial Indicators 22 The Statement of Directors’ Responsibility 112 Performance Group Performance 23 Audit Committee Report 113 Overcoming -

HAYLEYS FABRIC PLC CSE: MGT.N0000 Bloomberg: MGT SL EQUITY | SRI LANKA | CONSUMER DURABLES and APPAREL

HAYLEYS FABRIC PLC CSE: MGT.N0000 Bloomberg: MGT SL EQUITY | SRI LANKA | CONSUMER DURABLES AND APPAREL INITIATING WITH A BUY Riding the TREND!!!! CORPORATE UPDATE | 07 AUG 2019 Fair Value [FY20E]: LKR 20.0 [47%] FIRST CAPITAL RESEARCH Total Return with DPS 47% [AER 82%] Hiruni Perera +94 11 263 9864 [email protected] Disclosure Minimum Return for BUY: Buy Below [AER of 16.83% without DPS]: LKR 18.10 MGT categorized as ‘Grade B’ counter (Refer slide 44 for Recommendation criteria of Grade A, B & C Stocks) Disclosure on Shareholding: First Capital Group does not hold shares in MGT. First Capital Group has not traded in the shares in the three trading days prior to this document and will not trade in the shares for three trading days following the issue of this document. First Capital Research Aug 2019 2 Content Briefing 1.0 Summary and Key Data…………………………………………………………………………………………………………………………………………………… 4 2.0 Investment Thesis…………………………………………………………………………………………………………………………………………………………… 7 2.1 Shifted focus towards synthetic products to drive the topline growth………………………………………………………………… 9 2.2 Stable cotton and polyester prices to further expand margins……………………………………………………………………………. 17 2.3 Capacity expansion in knitting and dying facility to enhance the market share…………………………………………………… 21 2.4 Current Profitability to be set off against the tax losses and ESC…………………………………………………………………………. 24 3.0 Valuation………………………………………………………………………………………………………………………………………………………………………… 26 4.0 Company Profile ……………………………………………………………………………………………………………………………………………………………. -

Annual Report 2012/2013

THE PURSUIT OF EXCELLENCE One hundred years of passion, hard work and perseverance have brought to where we are today: a highly respected, fast growing blue chip conglomerate with interests in several key growth industry sectors: beverages, telecommunications, plantations, hotels, textiles, finance, insurance, power genaration, media and logistics. And yet, we will not rest. Our story is far from over. Indeed, it has only just begun. Look to us for even greater achievements as we step into the next century of our lifetime, to build further upon our current successes. DCSL. 100 years in the passionate pursuit of excellence. Distilleries Company of Sri Lanka PLC | Annual Report 2012/13 1 Financial Highlights 2013 2012 2013 2012 Group Group Company Company Summary of Results Gross Turnover Rs Mn 65,790 63,125 51,549 49,136 Excise Duty Rs Mn 37,024 36,150 34,088 33,860 Net Turnover Rs Mn 28,766 26,975 17,461 15,276 Profit After Tax Rs Mn 5,258 6,052 6,873 4,297 Shareholders Funds Rs Mn 47,978 41,576 39,155 32,597 Working Capital Rs Mn (1,298) (3,234) (6,139) (21,374) Total Assets Rs Mn 78,245 73,355 55,942 62,563 Staff Cost Rs Mn 3,194 3,155 1,039 1,080 No. of Employees 18,674 18,158 1,343 1,389 Per Share Basic Earnings* Rs. 17.13 18.45 10.68 11.85 Net Assets Rs. 159.93 138.59 130.52 108.66 Dividends Rs. 3.00 3.00 3.00 3.00 Market Price - High Rs. -

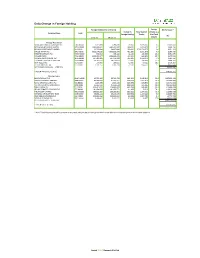

Daily Change in Foreign Holding

Daily Change in Foreign Holding Foreign Holding (No. of Shares) Foreign Net Turnover * Change in Total Volume Volume as a Company Name Code Foreign Holding Traded % of Total Rs. Volume 1-Feb-21 29-Jan-21 Foreign Purchases LANKA ORIX LEASING COMPANY PLC LOLC.N0000 2,313,835 2,286,635 27,200 2,699,110 1.0 13,702,000 EXPOLANKA HOLDINGS LIMITED EXPO.N0000 1,483,800,622 1,483,612,587 188,035 9,893,475 1.9 9,646,196 BROWNS INVESTMENTS LIMITED BIL.N0000 39,790,648 38,857,648 933,000 2,710,774,277 0.0 6,251,100 DIALOG AXIATA PLC DIAL.N0000 7,503,174,020 7,502,692,370 481,650 5,891,576 8.2 6,068,790 SWISSTEK (CEYLON) PLC PARQ.N0000 536,541 495,422 41,119 183,663 22.4 5,951,975 RICHARD PIERIS RICH.N0000 1,535,157,477 1,534,940,476 217,001 643,305 33.7 3,472,016 PIRAMAL GLASS CEYLON PLC GLAS.N0000 567,423,605 567,159,200 264,405 3,624,074 7.3 2,591,169 CHEVRON LUBRICANTS LANKA PLC LLUB.N0000 39,685,643 39,669,043 16,600 108,104 15.4 1,809,400 JOHN KEELLS PLC JKL.N0000 234,960 218,015 16,945 59,322 28.6 1,418,297 CIC HOLDINGS PLC (X) CIC.X0000 3,511,252 3,483,738 27,514 858,562 3.2 1,317,921 NET FOREIGN PURCHASE (TOP TEN) 52,228,863 FOREIGN PURCHASE (TOTAL) 149,626,332 Foreign Sales SAMPATH BANK PLC SAMP.N0000 49,752,499 50,713,780 (961,281) 2,948,613 32.6 (187,690,115) HATTON NATIONAL BANK PLC HNB.N0000 90,479,629 91,019,351 (539,722) 1,012,713 53.3 (81,363,092) ROYAL CERAMICS LANKA PLC RCL.N0000 1,825,896 1,946,188 (120,292) 826,955 14.5 (46,071,836) HATTON NATIONAL BANK PLC (X) HNB.X0000 25,447,044 25,629,644 (182,600) 625,195 29.2 (21,546,800) -

NDB 2020 PWM+Marketupdate Nov

ASSET PRIVATE MY WEALTH MANAGEMENT WEALTH MANAGEMENT MANAGEMENT MARKET UPDATE AND FUND REVIEW 2020 NOVEMBER Click here for download MARKET BRIEF BY NDB WEALTH The 2021 budget focused around post-Covid-19 growth, with strong support to local manufacturing, with the BUDGET 2021 aim of curbing imports whilst supporting the export sector. Consumer taxes remained broadly unchanged in an effort to stimulate growth amidst low economic activity. Further, the government's public investment drive is expected to be the largest in five years. While no material change to the revenue base is a positive factor to support growth, budget 2021 remains ambitious, expecting investment driven growth to bridge the revenue gap in the face of Covid-19 and external debt challenges. Inflation as measured by the CCPI (2013=100), edged up to 4.1% in November on a year-on-year basis from INFLATION PICKS UP the previous months’ 4.00% primarily owing to increases in food prices. During the month, the index was up 0.4% due to food prices increasing by 1.2% and non-food prices rising 0.2%. We believe the Central Bank will be able to manage inflation at mid-single digit levels in the short term. Reversing its rising trend, the Sri Lankan Rupee depreciated against the USD in November by 0.37% to close RUPEE FALLS the month at LKR 184.96 leading to an overall depreciation of 1.80% on a year-to-date basis. The Central Bank was a buyer of foreign exchange in the market in October amounting to USD 47.5 mn, whilst gross official reserves stood at approx. -

Melstacorp Limited Introductory Document

MELSTACORP LIMITED INTRODUCTORY DOCUMENT Listing of 1,165,397,072 Voting Ordinary Shares To be Listed on the Main Board of the Colombo Stock Exchange At a Reference Price of LKR 69.00 Financial Advisors and Managers to the Introduction: CT CLSA Capital (Pvt) Ltd (A CT Holdings Group and CLSA Group Company) # 4-15A, Majestic City, 10, Station Road, Colombo 04. Tel : +94 11 250 3523 : +94 11 258 4843 Fax : +94 11 258 0181 i Registration of the Introductory Document A copy of this Introductory Document has been delivered to the Registrar General of Companies in Sri Lanka for registration. The following documents were also attached to the copy of the Introductory Document delivered to the Registrar General of Companies. 1) The written consent of the Financial Advisors and Managers to the Introduction The Financial Advisors and Managers to the Introduction have given and have not before the delivery of a copy of the Introductory Document for registration withdrawn their written consent for the inclusion of their name as Financial Advisors and Managers to the Introduction and for the inclusion of their statements/declarations in the form in which it is included in the Introductory Document. 2) The written consent of the Auditors and Reporting Accountants to the Company The Auditors and Reporting Accountants to the Company have given and have not before the delivery of a copy of the Introductory Document for registration withdrawn their written consent for the inclusion of their name as Auditors and Reporting Accountants to the Company and for the inclusion of their report/statements in the form and context in which it included in the Introductory Document. -

Guardian Acuity Equity Fund Open Ended Growth Fund June 2021 Tel: +94 112039377 E-Mail: [email protected]

Guardian Acuity Equity Fund Open Ended Growth Fund June 2021 Tel: +94 112039377 E-mail: [email protected] HIGHLIGHT Crishani Perera The fund recorded a 1.29% return for the month and 2.52% return for 3 Months. The Fund Manager Accelerated vaccine rollouts and generally strong economic data in developed YTD return of the fund was 2.19% vs.benchmark ASPI return of 15.70%. economies led to strong gains in equities with S&P 500 leading with an 8.5% RETURNS* gain during 2Q whilst European stocks followed closely with a 7.1% return. The vaccination programs in rest of the Europe is now catching up with the BENCHMARK PERIOD* FUND S&P SL 20 ASTRI ASPI UK & US. The reopening of economies and a fast rebound in activity has fueled 2021 June 1.29% 5.87% -0.35% 5.88% inflation in some of the developed economies which is expected to contribute 3 Months 2.52% 10.06% 4.15% 10.12% to market jitters in the 2H. The emerging equities lagged with a 5.1% gain Year To Date (YTD 2021) 2.19% 15.70% 12.52% 15.84% during 2Q amidst slow vaccination rollout in most economies, policy Since Inception Cum. 85.21% 43.11% 0.43% 58.15% tightening and regulatory concerns in China. 3.91% 0.05% 5.03% Since Inception CAGR 6.82% Note : All Share Price Index (ASPI) ,All Share Total Return Index(ASTRI) & S&P Srilanka 20 Index (S&P SL 20) are based on CSE data as of 30th June 2021 Retail activity continued to dominate the local equities as notable price gains * Performances are based on month end prices as of 30th June 2021. -

Sri Lanka Equities Aspi ^ 4.46% | S&P Sl20 ^ 7.04%

ACUITY STOCKBROKERS RESEARCH | SRI LANKA EQUITIES Weekly Market Review 02 Nov 2018 th nd ASPI Hits 2-Month High Amid Higher Volatility… LKR Indices vs. Turnover (29 Oct – 02 Nov) Falls as Foreign Sell-Off of Assets Increases… 6,300 3,500 ASPI Increases 6,200 S&P SL20 3,400 S&P SL20 S&P ASPI ^ 4.46% | S&P SL20 ^ 7.04% 6,100 3,300 ASPI 6,000 3,200 The Bourse ended the week… Cont. P2 5,900 3,100 5,800 3,000 29-Oct 30-Oct 31-Oct 01-Nov02-Nov Foreign investors closed the week... Cont. P3 5.00 4.00 3.00 Equity market volatility ….… Cont. P4 2.00 LKR Bn) LKR (Turnover 1.00 0.00 Economic Snapshot………… P5 29-Oct 30-Oct 31-Oct 01-Nov 02-Nov KEY STATISTICS Week ending 02-Nov 26-Oct +/- ASPI 6,092.21 5,831.96 4.46% S&P SL20 3,208.43 2,997.33 7.04% Banking & Finance 16,242.78 15,368.05 5.69% Food & Beverage 24,368.96 24,096.79 1.13% Diversified 1,591.90 1,482.33 7.39% Hotel & Travel 2,677.50 2,642.53 1.32% Plantations 749.11 725.44 3.26% Manufacturing 2,963.05 2,742.56 8.04% Turnover (LKR Bn) 9.92 3.15 215.37% Foreign Buying (LKR Mn) 2,656.24 1,959.06 35.59% Foreign Selling (LKR Mn) 6,519.96 2,403.48 171.27% Daily Average Turnover (LKR Bn) 1.98 0.79 152.29% Daily Average Foreign Buying (LKR Mn) 531.25 489.76 8.47% Daily Average Foreign Selling (LKR Mn) 1,303.99 600.87 117.02% TOP 10 GAINERS TOP 10 LOSERS Opening Closing WoW % Opening Closing WoW % Company Code Company Code Price Price Change Price Price Change MTD WALKERS KAPIN 8.0 12.9 61.3% KELSEY KDL N 35.0 29.5 -15.7% BLUE DIAMONDS[NV] BLUEX 0.2 0.3 50.0% UDAPUSSELLAWA UDPL 35.0 29.6 -15.4% AMANA LIFE ATLLN 9.0 12.9 43.3% MERC. -

Annual-Report-2008-2009.Pdf

CONTENTS 03 Financial Highlights 57 Financial Statements 04 Chairman’s Review 58 Statement of Directors’ Responsibility 07 Management Report 59 Auditors’ Report 07 Chief Executive Officer’s Review 60 Income Statement 10 Financial Review 61 Balance Sheet 15 Sector Review 62 Statement of Changes in Equity 24 Risk Management 64 Cash Flow Statement 26 Sustainability Report 65 Notes to the Financial Statements 35 Stewardship 109 Share Information 35 Enterprise Governance 111 Five Year Summary 44 Directors’ Interest in Contracts with the Company 112 Glossary 46 Board of Directors 113 Notice of Meeting 48 Senior Management Enclosed Form of Proxy 50 Annual Report of the Directors on the Affairs of the Company Adding value to and enriching Hemas’ business enterprise lie at the very core of our being. It forms the reason and basis for our unswerving pursuit of new segments of activity that promise more robust growth, at a faster pace in the years ahead. At the same time, ours is an enriching enterprise, where every product, service and process has been imbued with innovation and a defining quality that takes it from the ‘run of the mill’ category to the ‘one of a kind’. In the process, our portfolio uplifts lives across the Nation and lives up to the Company’s new purpose... offering outstanding products and services that enrich the lives of our customers, whilst creating superior value for our shareholders. WEWE AREARE HEMASHEMAS Hemas is one of Sri Lanka’s top diversified conglomerates organised into five key sectors - FMCG, Healthcare, Transportation, Leisure and Power. The Group, which commenced operations in 1948, is listed on the Colombo Stock Exchange. -

DFCC Bank PLC Annual Report 2016.Pdf

Going beyond conventional reporting, we have implemented a About this Report more current format for reporting and have upgraded our corporate website with a focus on investor relations, supplemented by an investor relations app for smart phones and other devices. This is an integrated annual report and is a compact Reporting Period disclosure on how our strategy, governance, performance and prospects have resulted in the The DFCC Bank Annual Report for 2016 covers the 12 month period from 01 January 2016 to 31 December 2016 and is reflective of the creation of sustainable value within our operating change in the financial year-end implemented in 2015. The previous environment. annual report covered the nine month period from 01 April 2015 to 31 December 2015 and is available on the company website Value Creation and Capital Formation (www.dfcc.lk). Some of the Group entities have a 31 March financial year-end and they are consolidated with DFCC Bank’s reporting The ability of an organisation to create sustainable value for itself period with a three month time lag. A summary of the accounting depends on the value it creates for its stakeholders, making value periods covered by the Statement of Profit and Loss and Other creation essentially a two-way process. In fact, the more value an Comprehensive Income in the Bank and the Group columns is given organisation creates, the more value it is able to create for itself. in the Financial Report (page 136). Therefore firms spend substantial resources on creating and maintaining relationships with their stakeholders. Value creation leads to capital formation. -

Acuity Stockbrokers Research | Sri Lanka Equities

ACUITY STOCKBROKERS RESEARCH | SRI LANKA EQUITIES Weekly Market Review 20 Feb 2020 Indices vs. Turnover (17th Feb – 20th Feb) ASPI Closes Flat Amid Market Volatility… Sri Lanka Records a B-o-P Surplus in 2019… 5,900 2,950 ASPI 5,880 S&P SL20 2,910 S&P SL20 S&P ASPI ^ 0.02% | S&P SL20 ^ 0.54% 5,860 2,870 ASPI 5,840 2,830 The Bourse ended the week… Cont. P2 5,820 2,790 5,800 2,750 17-Feb 18-Feb 19-Feb 20-Feb Foreign investors closed the week... Cont. P3 0.75 0.60 0.45 Sri Lankan equities gained ….… Cont. P4 0.30 LKR Bn) LKR (Turnover 0.15 0.00 Economic Snapshot………… P5 17-Feb 18-Feb 19-Feb 20-Feb KEY STATISTICS Week ending 20-Feb 14-Feb +/- ASPI 5,830.51 5,829.21 0.02% S&P SL20 2,788.31 2,773.26 0.54% Banks 664.54 653.93 1.62% Capital Goods 830.26 831.53 -0.15% Food, Beverage & Tobacco 861.41 856.63 0.56% Consumer Durables & Apparel 921.80 969.00 -4.87% Materials 634.67 638.78 -0.64% Diversified Financials 872.01 885.14 -1.48% Turnover (LKR Bn) 1.80 2.21 -18.89% Foreign Buying (LKR Mn) 242.15 499.50 -51.52% Foreign Selling (LKR Mn) 364.62 851.01 -57.15% Daily Average Turnover (LKR Bn) 0.45 0.44 1.39% Daily Average Foreign Buying (LKR Mn) 60.54 99.90 -39.40% Daily Average Foreign Selling (LKR Mn) 91.15 170.20 -46.44% TOP 10 GAINERS TOP 10 LOSERS Opening Closing WoW % Opening Closing WoW % Company Code Company Code Price Price Change Price Price Change TESS AGRO[NON-VOTING] TESSX 0.4 0.5 25.0% S M B LEASING SEMBN 0.5 0.4 -20.0% CITRUS LEISURE REEFN 9.7 11.5 18.6% SINGHE HOSPITALS SERVN 1.7 1.5 -11.8% RADIANT GEMS RGEM 18.0 21.2 17.8% TANGERINE