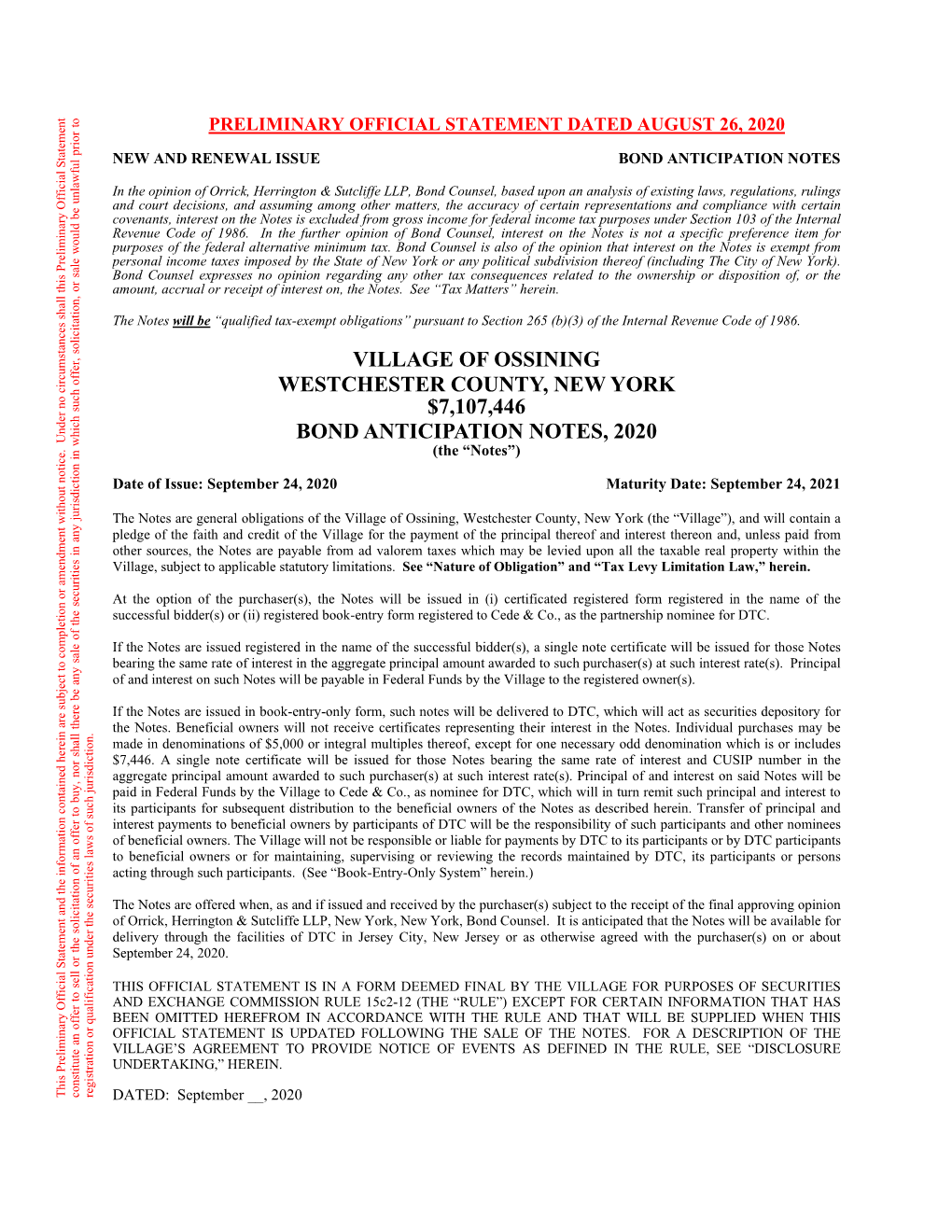

Official Statement Dated August 26, 2020

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Real Estate Record and Builders' Guide

REAL ESTATE RECORD AND BUILDERS' GUIDE. VOL. XXV. NEW TORK, SATURDAY, MAY 1, 1880. No. Qf:: Published Weekly by sation all the various improvements that ought to troversy, maj, however, soon come up, when I will be done in the Park. It seems to have been for look into its various phases. As yet I have not TERMS. gotten that the most attractive features of the P.ark fully done so." ONE YEAR, in advance....SIO.OO. are, the lawns, the foliage, and drives, the flowers " NO 0CC.\.SI0N " FOR MEETINGS. and walks. Of "late years this does not appear_to Cnniraunications should be addressed to " Is it not singular that this question has not have been uppermost in the minds of the Commis been discussed at length at the meetings of your C. MV. SWEET, sioners, and too little attention has been paid to it. Board recently?" No. 137 BROADWAY When I practically ceased to have any control of "My dear sir, we have only two meetings a the Department in 1870 a variety of improve month now. When I say anything about this I am ANDREW H. GREEN AND THE PARKS. ments were proposed for the Park. The conserva told, ' there is no occasion for more meetings,' just IXTRUVIEW WITH THE NEW COMMISSIONEK — THE tory was cut off in 1874, the Belvidere plan has thinkof it, a department having charge of such NEGLECT IN THE CENTRAL PAllK, DECAY OF FOLI.iGE been, disfigured, a ridiculous sheep-fold has been vast interests only meeting twice a month. When .KSV STKUCTaRES—A'ANDALISM BY EX-COMMISSION- EIW—TIME RIPE FOR I3IPROVEMENT3 EVERYWHERE erected better fitted for a regiment of artillary I was Commissioner before, I gave up my entire —TIIE WORLD'S FAIR THE GREAT AGENCY FOR than for sheep, and since my return to the Board business, devoted my entire time to the important milLDING UP THE WEST SIDE—WHAT MUST BE DONE. -

HISTORIC PRESERVATION COMMISSION MINUTES Monday, March 4, 2019 7:30 PM

VILLAGE OF OSSINING Planning Department John Paul Rodrigues Ossining Operations Center 101 Route 9A, Ossining, N.Y. 10562 Tel: (914)762-6232 www.villageofossiningorg HISTORIC PRESERVATION COMMISSION MINUTES Monday, March 4, 2019 7:30 PM Members Present: Also Present: Chairperson Adam Markovics Tracey Corbitt, Director of Planning and Development Commission Member Catherine Wilson Manuel R. Quezada, Trustee Commission Member Dana White Stuart B. Kahan, Corporation Counsel Commission Member J. Phillip Faranda Absent: Commission Member Elizabeth Harlow Commission Member Gauri Gandbhir Commission Member Julia Quinn I. CONTINUING BUSINESS OF THE BOARD A. Local Landmarking Priorities The Commission discussed the possibility of pursuing the Sing Sing Warden's Residence as the next local landmarkingproject. Mr. Markovics mentioned that former HPC member Miguel Hernandez had prepared a lot of the background information for the application. Ms. Corbitt said some research may have to be done to A see if there were any restrictions as part of the sale of the property from New York State to its current owner. Mr. Kahan said that it would be beneficial to get the owner involved in the application process. Mr. Markovics suggested that Ms. Wilson explore the architectural aspects of the applicationto see if there is anything to add and asked Ms. White if she could research any further historical information that would enhance the application. Brandreth Pill Factory Office Building The Commission continued with the ongoing discussion regarding the Brandreth Office Building. The Commission has agreed that the best course of action is to cooperate with the developers of Hidden Cove to salvage as much as possible of the office building. -

Village of Ossining LWRP Described Below Be Incorporated As Routine Program Changes (Rpcs), Pursuant to Coastal Zone Management Act (CZMA) Regulations at 15 C.F.R

Village of Ossining Local Waterfront Revitalization Program Adopted: Village of Ossining Board of Trustees, July 2, 1991 Approved: NYS Secretary of State Gail S. Shaffer, July 11, 1991 Concurred: U.S. Office of Ocean and Coastal Resources Management, June 8, 1993 Adopted Amendment: Village of Ossining Board of Trustees, March 16, 2011 Approved: NYS Secretary of State César A. Perales, October 25, 2011 Concurred: U.S. Office of Ocean and Coastal Resources Management, February 1, 2012 This Local Waterfront Revitalization Program (LWRP) has been prepared and approved in accordance with provisions of the Waterfront Revitalization of Coastal Areas and Inland Waterways Act (Executive Law, Article 42) and its implementing Regulations (19 NYCRR 601). Federal concurrence on the incorporation of this Local Waterfront Revitalization Program into the New York State Coastal Management Program as a routine program change has been obtained in accordance with provisions of the U.S. Coastal Zone Management Act of 1972 (p.L. 92-583), as amended, and its implementing regulations (15 CFR 923). The preparation of this program was financially aided by a federal grant from the U.S. Department of Commerce, National Oceanic and Atmospheric Administration, Office of Ocean and Coastal Resource Management, under the Coastal Zone Management Act of 1972, as amended. [Federal Grant No. NA-82-AA-D-CZ068.] The New York State Coastal Management Program and the preparation of Local Waterfront Revitalization Programs are administered by the New York State Department of State, Office of Coastal, Local Government and Community Sustainability, One Commerce Plaza, 99 Washington Avenue, Suite 1010, Albany, New York 12231-0001. -

Patent Medicine, Quack Cures, and Snake Oil: Why Do We Keep Falling for It?

Patent medicine, quack cures, and snake oil: Why do we keep falling for it? Teaching American History March 2014 Cynthia W. Resor Do we still have a “patent medicine” problem? • Video • http://www.screencast.c om/t/VmN8qbM1cP • Captured parts of on- line videos (with sound) with Snag-it • http://www.techsmith.c om/snagit.html • 15 days free • $30 a year for teachers Why do we keep buying this stuff? • Many have the view the God or Nature has provided the remedies for the ailments of humans and even give clues to humans to find the right thing • Ignorance • Can’t tell the difference in proven medical practices and quackery • placebo effect • People believe it works; sometimes it has a therapeutic effect, causing the patient's condition to improve. • regression fallacy • Certain "self-limiting conditions", such as warts and the common cold, almost always improve • patient may associate the usage of alternative treatments with recovering, when recovery was inevitable 2. Why do we keep buying this stuff? • Distrust of conventional medicine • Many people, for various reasons including the risk of side effects, have a distrust of conventional medicines, the regulating organizations themselves such as the Food and Drug Administration (FDA), or the major drug corporations • Conspiracy theories • Anti-quackery activists ("quackbusters") are accused of being part of a huge "conspiracy" to suppress "unconventional" and/or "natural" therapies, as well as those who promote them • believe the attacks on non-traditional medicine are backed and funded by the pharmaceutical industry and the established medical care system for the purpose of preserving their power and increasing their profits. -

5.5 Appraisal by Hudson Property Advisors

PREPARED FALL 2012 HUDSON PROPERTY ADVISORS APPRAISAL OF REAL PROPERTY SUMMARY APPRAISAL REPORT PROPERTY OF PLATEAU ASSOCIATES “HIDDEN COVE ON THE HUDSON” LOCATED AT 36 WATER STREET VILLAGE OF OSSINING WESTCHESTER COUNTY, NY JONATHAN BERNZ, MAI President SUBMITTED Hudson Property PLATEAU ASSOCIATES Advisors, LLC 427 BEDFORD ROAD PLEASANTVILLE, NY 10549 10 So. Moger Ave. VALUATION DATE Mt. Kisco, NY 10549 USA DECEMBER 6, 2012 File No. 2012.12001 HUDSON PROPERTY 10 South Moger Avenue ADVISORS, LLC Mt. Kisco, NY 10549 Jonathan A. Bernz, MAI Advanced Real Estate Appraisal and Consulting APPRAISAL OF REAL PROPERTY Summary Appraisal Report Property of Plateau Associates, LLC Hidden Cove on the Hudson 36 Water Street Village of Ossining Westchester County, New York (Our file # 2012.12001) Submitted Plateau Associates 427 Bedford Road Pleasantville, NY 10570 Date of Appraisal December 6, 2012 Date of Report December 10, 2012 Telephone (914) 244-3400 Fax (914) 244-3450 HUDSON 10 South Moger Avenue PROPERTY Mt. Kisco, NY 10549 Tel. (914) 244-3400 ADVISORS, LLC Fax (914) 244-3450 Jonathan A. Bernz, MAI Advanced Real Estate Appraisal and Consulting December 10, 2012 Plateau Associates 427 Bedford Road Pleasantville, NY 10570 Attention: Peter Stolatis Re: 36 Water Street (Hidden Cove on the Hudson) Village of Ossining Westchester County, NY (Our File No. 2012.12001) Gentlemen: In accordance with your request, we inspected the captioned property, consisting of a 5.1415 acre parcel improved with a building known as the Brandreth Pill Factory, for the purpose of providing you with our estimate of market value of the fee simple interest under the following hypothetical conditions: 1. -

Ossining Downtown Redevelopment Working Committee Final Report

OSSINING DOWNTOWN REDEVELOPMENT WORKING COMMITTEE FINAL REPORT August 8, 2017 TABLE OF CONTENTS I. Introduction and Executive Summary II. Mission Statement III. Definition of Downtown IV. Summary of Upcoming Development in Downtown V. Strengths, Weaknesses, Opportunities, and Threats: SWOT Analysis VI. Analysis of Comprehensive Plan and Existing Downtown Studies VII. Subject Area 1: Placemaking, Open Space, and The Built Environment VIII. Subject Area 2: Transportation and Parking IX. Subject Area 3 Innovative Ideas X. Subject Area 4: Outside Groups/Consulting XI. Conclusion & Final Recommendations XII. Acknowledgments XIII. Appendices: A. Map of Downtown B. Empty Parcels C. Full SWOT Analysis D. Comprehensive Plan Spreadsheet E. Library of Links F. Additional Outside Groups Spreadsheet INTRODUCTION AND EXECUTIVE SUMMARY In April 2017, the Village of Ossining’s Mayor and Board of Trustees invited an energized group of community members to participate in a newly-formed Downtown Redevelopment Working Committee (DRWC). We are comprised of 20 community members from diverse backgrounds and age groups, including business owners, local not-for-profit leaders, commuters, and government officials. While the DRWC emerged from a vigorous village-wide debate over downtown traffic patterns, it evolved into an exciting process of reimagining, reigniting, and reinvigorating our Downtown. The DRWC was tasked with looking at our Downtown with a new lens. Our members imagined, without limits, what could be possible for our community. Our volunteers collectively spent hundreds of hours meeting as a large group, in subcommittees, and engaging in research individually. During our 90-day tenure, we shared visions for our Downtown, received a presentation from our Village Historian on the current state of development, engaged in an analysis of our Downtown’s strengths, weaknesses, opportunities, and threats (S.W.OT.), received a presentation on zoning from the Village Director of Planning and Development, and participated in a walking tour. -

The Westchester Historian Index, 1990 – 2019

Westchester Historian Index v. 66-95, 1990 – 2019 Authors ARIANO, Terry Beasts and ballyhoo: the menagerie men of Somers. Summer 2008, 84(3):100-111, illus. BANDON, Alexandra If these walls could talk. Spring 2001, 77(2):52-57, illus. BAROLINI, Helen Aaron Copland lived in Ossining, too. Spring 1999, 75(2):47-49, illus. American 19th-century feminists at Sing Sing. Winter, 2002, 78(1):4-14, illus. Garibaldi in Hastings. Fall 2005, 81(4):105-108, 110, 112-113, illus. BASS, Andy Martin Luther King, Jr.: Visits to Westchester, 1956-1967. Spring 2018, 94(2):36-69, illus. BARRETT, Paul M. Estates of the country place era in Tarrytown. Summer 2014, 90(3):72-93, illus. “Morning” shines again: a lost Westchester treasure is found. Winter 2014, 90(1):4-11, illus. BEDINI, Silvio A. Clock on a wheelbarrow: the advent of the county atlas. Fall 2000, 76(4):100-103, illus. BELL, Blake A. The Hindenburg thrilled Westchester County before its fiery crash. Spring 2005, 81(2):50, illus. John McGraw of Pelham Manor: baseball hall of famer. Spring 2010, 86(2):36-47, illus. Pelham and the Toonerville Trolley. Fall 2006, 82(4):96-111, illus. The Pelhamville train wreck of 1885: “One of the most novel in the records of railroad disasters.” Spring 2004, 80(2):36-47, illus. The sea serpent of the sound: Westchester’s own sea monster. Summer 2016, 92(3):82-93. Thomas Pell’s treaty oak. Summer 2002, 78(3):73-81, illus. The War of 1812 reaches Westchester County. -

Attachment H Explanatory Notes to Attachment H

ATTACHMENT H EXPLANATORY NOTES TO ATTACHMENT H 1. This Attachment H consists of: (a) a Department of Environmental Conservation “Full Environmental Assessment Form” (“EAF”) for Verizon’s offering of cable service in Ossining, New York, with Part 1 filled in; (b) an EAF Addendum providing certain additional background information; and (c) exhibits to the Addendum, including maps showing environmentally relevant features of the franchise area and a list of sites included in the SPHINX database of historic sites, as described below. 2. The Attachment is submitted without prejudice to Verizon’s positions that: (a) the activities for which it seeks approval in this proceeding are not “actions” under the State Environmental Quality Review Act (“SEQRA”), and that therefore no EAF is required; and (b) if an EAF is required in this case, a short-form EAF will suffice. 3. The EAF and the EAF Addendum are based on information in Verizon’s possession or available to us through research in readily available sources. Beyond such sources, we have not undertaken any “new studies, research or investigation.”1 4. Historic site information was derived from the SPHINX database of the New York State Historic Preservation Office (see http://www.nysparks.state.ny.us/shpo/resources/ index.htm). Coastal area information was obtained from the New York State Geographic Information Systems Clearinghouse website (see http://www.nysgis.state.ny.us/gisdata/ inventories/details.cfm?DSID=317), as was flood plain data (see http://www.nysgis.state.ny.us/ gisdata/inventories/details.cfm?DSID=246). Information on wetlands locations was obtained from the U.S. -

Healthy Communities; Traffic Calming & Safety Policy Statements And

Land Use Law Center Gaining Ground Information Database Topic: Healthy Communities; Traffic Calming & Safety Resource Type: Policy Statements and Planning Documents State: New York Jurisdiction Type: Municipal Municipality: Ossining Year (adopted, written, etc.): 2009 Community Type – applicable to: Urban; Suburban Title: Traffic Signals and Narrower Lanes to Improve Safety Document Last Updated in Database: March 18, 2019 Abstract Ossining, New York’s Comprehensive Plan includes traffic-calming measures to be implemented throughout the village, though particularly on Route 9. Route 9 is the primary north-south arterial reaching through Ossining and onto major highways in New York. Route 9’s increasingly congested condition has resulted in residential road use throughout the village. These residential roads are narrow, steep, and winding, and often dangerous during inclement weather. Ossining’s goal is to improve pedestrian safety and comfort, and to change the behavior of motorists who would otherwise use residential roads to bypass congestion on the major roads. One traffic-calming measure employed by the New York State Department of Transportation re-striping. Re-striping to a narrower lane slows traffic and increases the safety of the roads. What congestion might be created by this process is mitigated by the town’s restructured traffic signal timing and coordination which is based on traffic data collection. Restructured traffic signals are also meant to increase the safety of pedestrians crossing wide sections of Route 9 by increasing the time allotted. New traffic lights are to be implemented at strategic intersections where congestion and hazards typically occurs. Data collection is to be continued on the sections of the road that underwent re-striping and signal light restructuring in order to assess the effect of the measures. -

J:N":Ou"St:Rial A.:Rch:Eology

J:N":OU"ST:RIAL A.:RCH:EOLOGY Volume 9 Number 2 March 1980 LAST GASP OF LAST CHICAGO STATION? Always the country's premier railroad terminal city, Chicago extolled North Western as one of the most beautiful and efficient rapidly is coming close to losing its last station. Gradually, the city's urban terminals anywhere. Its architecture later lost critical favor onetime six passenger terminals have been demolished (IC's but its efficiency endured. Although the transcontinental and, Central, B&O's Grand Central), defiled (Union), or abandoned indeed, all intercity trains are gone, North Western was always (Dearborn). A fifth, LaSalle St., lives on borrow time, a shadow predominantly a suburban terminal - built to cope with hordes of of its former self. That leaves the Chicago & North Western's North people and multiple train movements in peak periods. Currently it Western Station (1908-11), a Neoclassic hulk located off the Loop serves a thriving commuter traffic of over 90,000 passengers a day, at W. Madison & N. Canal sts., still mostly in original condition. still far short of its designed capacity but more than double its 1915 load. Trains may have disappeared elsewhere, but rush hour at North Western is still a sight to behold. In fact, there is tentative talk of adding some Amtrak Milwaukee runs since Union Station (the city's other major station) is becoming overburdened. Happily, despite some 1965 interior alterations, North Western has survived in reasonably pristine original form, complete with its Bush trainshed and semaphore interlocking system. It is, in short, an almost perfectly preserved 1910-era metropolitan railroad terminal from its columned facade to its rear approach tracks. -

Appendix G Phase 1 Archaeological Assessment

G. Phase 1 Archaeological Assessment PHASE 1 ARCHAEOLOGICAL ASSESSMENT AND FIELD INVESTIGATION HIDDEN COVE DEVELOPMENT BRANDRETH PILL FACTORY VILLAGE OF OSSINING, WESTCHESTER COUNTY, NEW YORK PHASE I ARCHAEOLOGICAL ASSESSMENT and HELD INVESTIGATION HIDDEN COVE DEVELOPMENT BRANDRETH PILL EACTOR Y Village of Ossining, Westchester County, Ne\\-' York Prepared For: Peler StoJali~ 427 Bedford Road Pleasantville. NY 10570 Prepared Uy lli~lorical PerspcLlive~. Inc. P.O. I3(lX 3037 \liestport, CT 06880 Primary Author: Sara Mascia. Ph.D. Field DireclOr: James Cox September 201)6 Managemen! Summary SHPO Project Review Number (if available)c' _ Involved State and Federal Agencie~ (DEC, CORPS,FHWA.elc.): Phase ofSuT\iey:cPCh"",'~'_,~ _ Location lnfonnation Location: Water Street Minor CC;yC,","DC;",C;;C;oCoC'"TCoC.CnCoc,c'OnC"CiOoOinCgc------------------- County Westchesta Survey Area ~Metric & English) Length: _ Width: Depth (when appropriate): Numher ofAcres Survt"ved: <I Number of Square Meters & Feet E"xC'O'Cva=tC,Od"(~P~hc"'C'CIOI-,~P~hc",C,:-;;"~1Co=o~'y=)C,-------- Percentage ofrhe Site Excavated (Phase II. Phase III only): U.5.G.S. 7.5 Minute Quadrangk Map: Ossining _ Archaeological Survey Oven'iew Number & Inter,a] of Shovel Tests: 15 at 15 meter interval or ~ma1Jer Number & Size ofunits,,'CC,,'o5_5cO""'"m'-'-v"S,OC'Cm"- _ Width of Plowed Strips: Surface Sur'iey of Transect rnterval: Results ofAn:haeological Survey Number & name of prehistoric sites identified: N:.0eo"''- _ Number & name of historic ~ites identitied: None Number & name of sites recommendcd for Phase "llc/AC--y-oC;dC,-,-,,----------- Results of Architectur<ll Survey Number ofbuildingsistructures/cemeteries within project area: I Number of buildings/structures/cemet~riesadjacent to project are",c.c3;--------- NillIlher ofprrviously delem1ined NR listed or eligible buildings/structur.:slcemetcries/districis Number of identified eligible bui\dings/stTucrures/ccmeteries/districts: 3 Report Author ($): Sara F. -

Section II Inventory and Analysis R

Section II Inventory and Analysis r General Information The Hudson River, "one of the most beautiful rivers in the world," forms the western boundary of the Village of Ossining. Richly endowed in its setting, Ossining is located 31 miles north of New York City on the rolling hills which characterize the eastern shore of the Hudson Valley. The Village has three miles of riverfront land with some of the most spectacular views in all of the Hudson's 315 mile length: the Palisades lie on the western shore; the Manhattan skyline is to the south; and Croton Point is upriver. However, the waterfront area has been long neglected and most of Ossining's residents have had little opportunity to enjoy the pleasures which the river has to offer. Recently, attempts have been made to provide waterfront park land; however, the riverfront is still underutilized as a people resource. When the railroad came through Ossining, in 1849, it separated the community from the river, both physically and economically. The Hudson was no longer quite as accessible nor would it ever again play as big a role in the transportation of goods and people between Ossining and the communities to its north and south. The railroad was largely constructed on fill placed along the water's edge and only in a few places is there enough land west of the tracks for buildings or for recreational uses. Within the Village of Ossining, there is a 0.6 mile stretch of land west of the railroad tracks which can be reached via two vehicular bridges.