Brentford 2019 Focus On: Brentford

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

INSPECTION REPORT NORWOOD GREEN JUNIOR SCHOOL Southall LEA Area: Hounslow Unique Reference Number: 102495 Headteacher: Mrs R

INSPECTION REPORT NORWOOD GREEN JUNIOR SCHOOL Southall LEA area: Hounslow Unique reference number: 102495 Headteacher: Mrs R Lamb Reporting inspector: Mrs J Richardson 6676 Dates of inspection: 27 - 28 November 2001 Inspection number: 193785 Short inspection carried out under section 10 of the School Inspections Act 1996 © Crown copyright 2002 This report may be reproduced in whole or in part for non-commercial educational purposes, provided that all extracts quoted are reproduced verbatim without adaptation and on condition that the source and date thereof are stated. Further copies of this report are obtainable from the school. Under the School Inspections Act 1996, the school must provide a copy of this report and/or its summary free of charge to certain categories of people. A charge not exceeding the full cost of reproduction may be made for any other copies supplied. INFORMATION ABOUT THE SCHOOL Type of school: Junior School category: Community Age range of pupils: 7 - 11 Gender of pupils: Mixed School address: Thorncliffe Road Southall Middlesex Postcode: UB2 5RN Telephone number: 0208 574 1726 Fax number: 0208 813 9511 Appropriate authority: Governing Body Name of chair of governors: Mrs J Hanspal Date of previous inspection: 6 - 9 May 1997 Norwood Green Junior School - 3 INFORMATION ABOUT THE INSPECTION TEAM Team members 6676 Joy Richardson Registered inspector 13807 Christine Haggerty Lay inspector 21037 Christopher Gray Team inspector 27791 Greg Crawford Team inspector The inspection contractor was: Cambridge Education Associates Ltd Demeter House Station Road Cambridge CB1 2RS Any concerns or complaints about the inspection or the report should be raised with the inspection contractor. -

Download Network

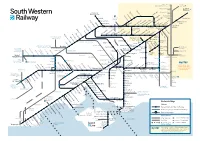

Milton Keynes, London Birmingham and the North Victoria Watford Junction London Brentford Waterloo Syon Lane Windsor & Shepherd’s Bush Eton Riverside Isleworth Hounslow Kew Bridge Kensington (Olympia) Datchet Heathrow Chiswick Vauxhall Airport Virginia Water Sunnymeads Egham Barnes Bridge Queenstown Wraysbury Road Longcross Sunningdale Whitton TwickenhamSt. MargaretsRichmondNorth Sheen BarnesPutneyWandsworthTown Clapham Junction Staines Ashford Feltham Mortlake Wimbledon Martins Heron Strawberry Earlsfield Ascot Hill Croydon Tramlink Raynes Park Bracknell Winnersh Triangle Wokingham SheppertonUpper HallifordSunbury Kempton HamptonPark Fulwell Teddington Hampton KingstonWick Norbiton New Oxford, Birmingham Winnersh and the North Hampton Court Malden Thames Ditton Berrylands Chertsey Surbiton Malden Motspur Reading to Gatwick Airport Chessington Earley Bagshot Esher TolworthManor Park Hersham Crowthorne Addlestone Walton-on- Bath, Bristol, South Wales Reading Thames North and the West Country Camberley Hinchley Worcester Beckenham Oldfield Park Wood Park Junction South Wales, Keynsham Trowbridge Byfleet & Bradford- Westbury Brookwood Birmingham Bath Spaon-Avon Newbury Sandhurst New Haw Weybridge Stoneleigh and the North Reading West Frimley Elmers End Claygate Farnborough Chessington Ewell West Byfleet South New Bristol Mortimer Blackwater West Woking West East Addington Temple Meads Bramley (Main) Oxshott Croydon Croydon Frome Epsom Taunton, Farnborough North Exeter and the Warminster Worplesdon West Country Bristol Airport Bruton Templecombe -

Neighbourhood Governance Note of Norwood Green Ward Forum Meeting ______

Neighbourhood Governance Note of Norwood Green Ward Forum Meeting ______________________________________________________________________________________ Norwood Green Ward Forum meeting – held on Friday 17 October 2008 at 7pm at St Mary’s Church, Norwood Green Road, UB2 Present: Councillors Sharma (Chair), Aslam, Mann Attendees: Over 26 people attended with 24 signing the attendance sheet. Sgt. Andy Storr – Norwood Green Safer Neighbourhood Team Note taker: Kofi Nyamah (KN) - Neighbourhood Co-ordinator (West) Apologies: None No. Note Action Point/Information 1. Welcome and introductions The meeting started at 7pm in the hall of St Mary’s Church, Norwood Green Road. Councillor Sharma (Chair) welcomed those present and introduced Councillors Aslam, Mann and Ealing council officer, Kofi Nyamah. 1 No. Note Action Point/Information 2. The role of ward forums KN outlined the role of ward forums: - Replacing Area Committees - Acting as consultation group on issues of local and borough wide concern - Problem-solving local issues with residents, Councillors and Council officers - £40,000 of funding available to implement local ward improvement projects, such as: local traffic & highways schemes local environmental improvements parks improvements additional clean-up and rubbish removal schemes alley gating schemes - Councillor Sharma explained the process for spending £40,000 for ward improvements. Proposals put forward by ward residents, assessed and recommended by ward councillors. Formal decisions on whether to implement recommendations taken by appropriate council portfolio holder - A number of residents complained that they had not - KN to investigate ‘Neighbourhood Matters’ leaflet received the ‘Neighbourhood Matters’ leaflet and were distribution only aware of the ward forum through friends or via an email sent by KN 2 No. -

Acton and Chiswick Circular Trail (ACCT) – 6.5 Miles

Acton and Chiswick Circular Trail (ACCT) – 6.5 miles Acton Town Station – Gunnersbury Park – Strand on the Green – Gunnersbury Station – Chiswick business park - Gunnersbury Triangle Wildlife Reserve – Chiswick Park Station – Acton Green Common – Chiswick Common – Turnham Green Station – Bedford Park garden suburb - Acton Park – Churchfield Road – Crown Street - Mill Hill Road – Acton Town Station Route: Easy – mostly surfaced paths through parks and commons and quiet roads with short sections of main roads. Local Amenities: cafes, pubs, shops at several places. Toilets available at Gunnersbury Park and in some cafes/pubs and an Acton supermarket on route. Bike racks by Acton Town station and shops. Points of Interest: Gunnersbury Park – historic house, museum and park; the new Brentford Football Stadium; Strand on the Green on the Thames with historic houses; the landscaped Chiswick Business Park; London Wildlife Trust’s reserve at Gunnersbury; the garden suburb of Bedford Park; and Acton Park. Transport: Acton Town Station (Piccadilly and District) and local buses. Join or drop out at Kew Bridge rail station or Gunnersbury, Chiswick Park or Turnham Green tube stations. Starting at Acton Town Station. Turn left out of the station and walk past cafes and shops to cross the busy North Circular Road (A406) at lights. Continue ahead on Popes Lane to turn left into Gunnersbury Park (1), walk down the drive and turn 2nd right by a children’s playground, the café & toilets. Before the boating lake, turn left down a path by the side of the house to the Orangery. At the Orangery turn left to walk round the far side of the Horseshoe Lake. -

A Rare Opportunity to Acquire This Grade II Listed Family House

A rare opportunity to acquire this Grade II Listed family house Fairfax Road, Bedford Park, Chiswick, London, W4 £2,800,000 Freehold ◆ 6 bedrooms ◆ 2 reception rooms ◆ kitchen / dining room ◆ 3 bathrooms ◆ fabulous garden ◆ semi-detached ◆ Grade II Listed ◆ roof terrace ◆ storage ◆ off-street parking ◆ 253.95 sq m (2,734 sq ft) Local Information room / sitting room with doors Fairfax Road is considered to be opening out onto the mature one of the best addresses garden. This floor also in Bedford Park, located in central accommodates a bathroom. Chiswick close to Turnham Green The first floor offers three Terrace. Fairfax Road sits in the bedrooms and a family bathroom. heart of Bedford Park, London’s The bedroom at the back of the first garden suburb and house has the popular Bedford Chiswick's most sought-after Park palisade fencing roof enclave. It is a short distance terrace. The second floor houses from the excellent shops, a further three bedrooms and a boutiques and restaurants of family bathroom. central Chiswick, and close to Overall this is a tremendously Turnham Green Underground versatile house with further station (District Line). Central potential to create a stunning London and Heathrow (A4/M4) family home. are easily accessible, as are several leading independent Tenure schools. Freehold About this property Local Authority Located on a very popular Hounslow Council residential tree lined street in Bedford Park. This Grade II Listed Energy Performance Norman Shaw semi-detached EPC Rating = Listed Building family house offers a secluded westerly facing garden and Viewing superb potential. A Virtual Tour Viewing of the The house is currently arranged house is available on request over three floors retaining a largely original arrangement of All viewings will be accompanied space with many period features, and are strictly by prior whilst several of the rooms are of arrangement through Savills grand proportions with ceiling Chiswick Office. -

Street Name Tree Species/Job Instructions Location Ward ALBURY AVENUE Carpinius Betulus Fastigiata Plant in Grass Verge Outside

Street Name Tree Species/Job Instructions Location Ward Carpinius betulus fastigiata plant Isleworth and ALBURY AVENUE in grass verge Outside 3-5 Brentford Area Carpinus bet.Fastigiata(clear stem) plant in excisting tree pit, Isleworth and ALBURY AVENUE grub out dead sampling. Os 12-14 Brentford Area Plant Sorbus thur. Fastigiata opposite 10 and install new tree ALKERDEN ROAD pit Os 04/06 Chiswick Area Plant Sorbus thur. Fastigiata and ALKERDEN ROAD install new tree pit Os 4-6 Chiswick Area Plant a Sorbus thur. Fastigiata opposite 10 and install new tree ALKERDEN ROAD pit Os 10 Chiswick Area Please plant new Prunus maackii on excisting grass O/S 16 on the O/S 16 on the green plant new Heston and ALMORAH ROAD green Prunus maackii Cranford Area Please plant new Prunus maackii O/S 17 plant new Prunus Heston and ALMORAH ROAD tree on excisting grass O/S 17 maackii tree on excisting grass Cranford Area O/S 21 please plant new O/S 21 Please plant new Prunus Prunus maackii tree on the Heston and ALMORAH ROAD maackii tree on the green grass on the green Cranford Area Please plant new Prunus maackii tree O/S 20-21 on the green on O/S 20-21Please plant new Heston and ALMORAH ROAD excisting grass Prunus maackii tree on grass Cranford Area Please plant new Prunus maackii on excisting grass O/S 16 on the O/S 16 on the green plant new Heston and ALMORAH ROAD green Prunus maackii Cranford Area Transplant Prunus maackii centrally in excisting grass verge O/S 17-21. -

Open a PDF List of This Collection

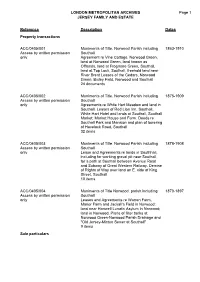

LONDON METROPOLITAN ARCHIVES Page 1 JERSEY FAMILY AND ESTATE ACC/0405 Reference Description Dates Property transactions ACC/0405/001 Muniments of Title. Norwood Parish including 1863-1910 Access by written permission Southall only Agreement re Vine Cottage, Norwood Green, land at Norwood Green, land known as Offlands, land at Frogmore Green, Southall, land at Top Lock, Southall, freehold land near River Brent Leases of the Cedars, Norwood Green, Bixley Field, Norwood and Southall 24 documents ACC/0405/002 Muniments of Title. Norwood Parish including 1875-1909 Access by written permission Southall only Agreements re White Hart Meadow and land in Southall. Leases of Red Lion Inn, Southall, White Hart Hotel and lands at Southall, Southall Market, Market House and Farm. Deeds re Southall Park and Mansion and plan of lowering of Havelock Road, Southall 32 items ACC/0405/003 Muniments of Title. Norwood Parish including 1878-1908 Access by written permission Southall only Lease and Agreements re lands in Southhall, including for working gravel pit near Southall, for a path at Southall between Avenue Road and Subway of Great Western Railway. Demise of Rights of Way over land on E. side of King Street, Southall 10 items ACC/0405/004 Muniments of Title Norwood. parish including 1870-1897 Access by written permission Southall only Leases and Agreements re Warren Farm, Manor Farm and Jackall's Field in Norwood; land near Hanwell Lunatic Asylum in Norwood; land in Norwood. Plans of filter tanks at Norwood Green-Norwood Parish Drainage and "Old Jersey-Minton Sewer at Southall" 9 items Sale particulars LONDON METROPOLITAN ARCHIVES Page 2 JERSEY FAMILY AND ESTATE ACC/0405 Reference Description Dates ACC/0405/005 Muniments of Title Norwood Parish including 1903-1930 Access by written permission Southall only Sales Particulars - including properties in Southall, Norwood Green, Lampton, Osterley and Hanwell. -

THE CHARACTER of the LANDSCAPE 2.39 the Thames

THE CHARACTER OF THE LANDSCAPE 2.39 The Thames enters the Greater London Area at Hampton. From Hampton to Erith, the river fl ows through the metropolis; an urban area even though much of the riverside is verdant open space, particularly in the fi rst stretch between Hampton and Kew. 2.40 The character of the river is wonderfully varied and this chapter concentrates on understanding how that variety works. We have deliberately avoided detailed uniform design guidelines, such as standard building setbacks from the water’s edge. At this level, such guidelines would tend to stifl e rather than encourage the variety in character. Instead we have tried to highlight the main factors which determine the landscape character and propose recommendations to conserve and enhance it. 2.41 Landscape Character Guidance LC 1: New development and new initiatives within the Strategy area should be judged against the paramount aim of conserving and enhancing the unique character of the Thames Landscape as defi ned in the Strategy. The River 2.42 Although, being a physical boundary, the river is often on the periphery of county and local authority jurisdictions, it is essentially the centre of the landscape. The Thames has carved the terraces and banks that line its course, the valley sides drain down to its edges and the water acts as the main visual and physical focus. It is a dynamic force, constantly changing with the tide and refl ecting the wind and the weather on its surface. 2.43 Downstream of the great expanse of water at the confl uence with the Wey, the Thames fl ows from west to east – the Desborough Cut by-passing the large meander near Shepperton. -

Our Feltham Rediscovering the Identity of a Post-Industrial Town

London Borough of Hounslow ৷ Feltham ৷ 2019 Our Feltham Rediscovering the Identity of a Post-Industrial Town An Interactive Qualifying Project Report submitted to the Faculty of the WORCESTER POLYTECHNIC INSTITUTE in partial fulfillment of the requirements for the Degree of Bachelor of Science by: Meredith Forcier ৷ BME ৷ ‘20 Hannah Mikkila ৷ ME ৷ ‘20 Kyle Reese ৷ RBE/CS ৷ ‘20 Jonathan Sanchez ৷ ME/RBE ৷ ‘20 Nicholas Wotton ৷ MA ৷ ‘20 Advisors: Professor Fabio Carrera & Professor Esther Boucher-Yip https://sites.google.com/view/lo19-of/home [email protected] | [email protected] This report represents the work of WPI undergraduate students submitted to the faculty as evidence of completion of a degree requirement. WPI routinely publishes these reports on its website without editorial or peer review. For more information about the projects program at WPI, please see http://www.wpi.edu/academics/ugradstudies/project-learning.html Abstract The London Borough of Hounslow is implementing a fifteen-year revitalization plan for Feltham. Through interviews and community engagement, our project highlighted the elements that make up the identity of the town to be incorporated in the next steps in the redesign of the town center. The team created a website that incorporates project deliverables, a comprehensive list of bibliographical sources, an Encyclopedia of important town assets, a walking tour of key elements of town identity, and a promotional video. ii Acknowledgments There were many people who made the completion of this project possible. It has been a long journey since we began work on the project in January 2019, but a few people have been there all along the way to help us. -

1.0 Site 1.1 Liddle Keen & Co

References – L/676/5/436 & P/2003/3749 Isleworth and Brentford Area Committee 04 March 2004 Case Officer – [email protected] - (020 8583 4943) 1.0 SITE 1.1 LIDDLE KEEN & CO, RAILSHEAD ROAD, ISLEWORTH (London Borough of Richmond, affecting Isleworth Ward) 2.0 PROPOSAL 2.1 Demolition of existing buildings, new development comprising of 18 residential units (9 private dwellings and 9 affordable flats) 2.2 The application has been called into area committee by Councillor Hibbs. The reason given is that this is an environmentally sensitive Thames Riverside area, which should be protected. 3.0 SITE DESCRIPTION: 3.1 The site is located within the London Borough of Richmond upon Thames, and is on the south side of the River Crane at its confluence with the Thames. The Richmond Road traffic bridge passes over the Crane on the western boundary of the site. Land on the northern side of the river is within the London Borough of Hounslow, and comprises the Nazareth House convent and care home complex, and also has the Isleworth Sea Scouts base. This site is within the Isleworth Riverside Conservation Area. A boat shed and dock area is directly opposite the application site. 3.2 The application site is currently used as the headquarters of a building company, and contains offices and storage areas. 4.0 HISTORY: 4.1 L/676/5/429 – Demolition of existing buildings and erection of a new building comprising 18 residential units (9 private dwellings and 9 affordable flats). The Council raised no objection to this application. -

Appointment of Election Agents

Greater London Authority Election of the Assembly Member for the SOUTH WEST Constituency APPOINTMENT OF ELECTION AGENTS NOTICE IS HEREBY GIVEN that the following candidates have appointed or are deemed to have appointed the person named as election agents for the election of the London Assembly Member for the SOUTH WEST Constituency on Thursday, 5 May 2016. NAME AND ADDRESS OF NAME AND ADDRESS OF AGENT ADDRESS OF OFFICE TO WHICH CANDIDATE CLAIMS AND OTHER DOCUMENTS MAY BE SENT IF DIFFERENT FROM ADDRESS OF AGENT Tony Arbour David Richard Jones 372 Upper Richmond Road West, 3 Holmesdale Road, Teddington, 16 Eaton Drive, Kingston Hill, East Sheen, London, SW14 7JU Middlesex, TW11 9LJ Kingston upon Thames, KT2 7QT Adam John Lewis Buick Oliver Rupert Bond 23 Ham Street, Richmond, TW10 Flat 9, 84 London Road, Kingston, 7HR KT2 6PX Alexander Alan Craig Peter Staveley Flat 1, 156 Pentonville Road, 36 Studley Road, London, E7 9LX 247 Davidson Road, Croydon, CR0 London, N1 9JL 6DQ Andree Michelle Frieze Thomas Dunning Beaton 139 Latchmere Lane, Kingston upon 42 Church Street, Isleworth, TW7 Thames, KT2 5NX 6BG Rosina Jane Robson Roisin Miller 21 Berrylands Road, Surbiton, KT5 26 Adelaide Road, Richmond, TW9 6b Arcade Parade, Elm Road, 8QX 1XW Chessington, KT9 1AB Martin James Whelton Alastair Michael Craft Brentford & Isleworth Labour Party, 4 Crossways Road, Mitcham, CR4 1 Arta House, Devonport Street, 367 Chiswick High Road, London, 1DQ London, E1 0EF W4 4AG Dated this Friday, 01 April 2016 Mary Harpley, Constituency Returning Officer London Borough of Hounslow Civic Centre Lampton Road Hounslow TW3 4DN Published and printed by Mary Harpley, Constituency Returning Officer, London Borough of Hounslow, Civic Centre, Lampton Road, Hounslow, TW3 4DN . -

Unit 1 Spruce House, Brentford

WATERSIDE OFFICES WITH CAR PARKING TO LET FLEXIBLE LEASE AVAILABLE – Q2 2021 Unit 1 Spruce House, 1,480 sq. ft. Durham Wharf Drive, Brentford, TW8 8HR (137.5 SQ. M.) Unit 1 Spruce House, Durham Wharf Drive, Brentford, TW8 8HR Location Spruce House is located on Brentford Lock, which is a modern development situated off the west end of High Street (A315) on the edge of Brentford Town Centre. The premises are approximately 8 miles from Central London and 7 miles from Heathrow Airport. There are excellent road communications via the nearby A4, and Brentford Rail Station is approximately 10 minutes’ walk from the property. The nearest underground station is Boston Manor ( Piccadilly Line) which is approximately 5 minutes’ drive. BOSTON MANOR A4 Great West Road 0.7 miles North Circular – Chiswick 1.4 miles KEW BRIDGE M4 – Brentford 1.4 miles BRENTFORD Heathrow Airport 6.8 miles M25 – Junction 14 9.6 miles Spruce House Brentford (British Mainline) 0.7 miles SYON LANE Syon Lane (British Mainline) 0.8 miles Boston Manor (Piccadilly Line) 1.3 miles Northfields (Piccadilly Line) 1.5 miles Gunnersbury (District Line) 2.2 miles www.vokins.co.uk Unit 1 Spruce House, Durham Wharf Drive, Brentford, TW8 8HR The Property Spruce House contains a high-quality waterside development of primarily residential accommodation, with hotel, office and retail elements incorporated. This property comprises a ground-floor self-contained unit with kitchen facility, two storage rooms and separate male and female WCs. The suite is fitted to a good specification to include air-conditioning, under floor trunking, Cat II lighting and new carpeting.