INVESTOR PRESENTATION 29 August 2012

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Belgrade and Istanbul in the Global Competition

UDC 711.4 (497.11) 711.4 (560.118) CHASING THE LIMELIGHT: BELGRADE AND ISTANBUL IN THE GLOBAL COMPETITION Aleksandra Stupar, Cenk Hamamcioglu The purpose of this paper is to analyze and compare main changes of contemporary Belgrade and Istanbul - two urban nodes at the crossroads of different and multileveled flows. Following the same pattern of global activation, inevitable competition and networking, these cities are trying to synchronize their multidimensional background, establish new patterns of global behavior and adjust them to the dynamism of modern life. Consequently, their historical role has been modified, urban tissue has been developed, recreated and regenerated, and the output of this process represents an attractive testimony of their global initiation. Revealing the ambiguous nature of strong economic forces as well as a new fusion of urban cultures, Belgrade and Istanbul are structuring the globalized image with the new key-elements. However, their true potential and the real efficiency of this process should be re-evaluated - the changed physiognomy of the city could improve its position in the global hierarchy and facilitate its integration into the global community, but, sometimes, local limitations are too complex and too strong to be ignored. INTRODUCTION Belgrade and Istanbul, two interesting exam- for the Austrians and the Turks, and both ples interlinked by specific historical circum- conquerors 'molded' the city according to their Although the process of globalization repre- stances, have decided to apply this -

Zuma Istanbul Address: and Servicestyle

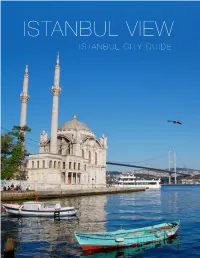

ISTANBUL VIEW ISTANBUL CITY GUIDE ISTANBULVIEW Get the most out of your visit to Istanbul with our essential guides to shopping, dining, and nightlife in Istanbul. ISTANBUL CITY GUIDE ISTANBUL Istanbul - The only metropolis on two continents Istanbul - The only We at Istanbulview give you an creates an atmosphere that overview of Istanbul with feels like you just went through metropolis in the news, highlights, shopping, a time machine. restaurants, nightlife, hotels, A whirl through Istanbul’s luxe world which is and developments. shopping malls, ultra chic situated on two The content on Istanbulview is restaurants, hip hotels, and commented and rated by our exciting nightlife proves that continents and one audience to give you an this ancient city is Europe's of the biggest and interactive experience to find hippest spot. the best place to enjoy. When the night falls, the city most vibrant cities in transforms into a nightlife Mystic mosques, beautiful heaven where glitz and glamor Europe. palaces, small ancient streets, takes over the city. the rich historical past of Istanbul, former Your Istanbulview Team Constantinople of 1001 nights, Welcome to the Istanbul View City Guide where we VIEW celebrate one of the most vibrant and diverse cities in the world. In this guide you will discover many reasons to love Istanbul, the city which was 2010 European Capital of ISTANBUL Culture and named the best place to be in 2010. Table of Contents Istanbul........................................................................................... -

What Do We Recommend?

While travelling, we like feeling the city, wake up early with the sun rise, visit all the cultural and historical places and taste the city’s special flavors. According to that concept, we preapared the “Eat, Love, Pray in Istanbul Guide” which is all about our suggestions with little tips. We hope you could benefit from the hand book. Have a good stay and enjoy the city. Ramada Istanbul Grand Bazaar Family SOPHIA PITA RESTAURANT &TAPAS Offers a fusion of authentic and modern Spanish tapas accompanied by a distinguished selection of Turkish wines and selected international wines and liqours, also open for breakfast and dinner with a relaxing atmosphere at the Aya Sofya’s backyard. Adress;Boutique St. Sophia Alemdar Cad. No.2 34122 Sultanahmet / Istanbul Phone;009 0212 528 09 73-74 PS:How to get there;The nearest tram station is Sultanahmet or Gulhane tram station. BALIKÇI SABAHATTİN “Balıkçı Sabahattin” ( Fisherman Sabahattin) was at first running a traditional restaurant left by his father some streets behind which not everyone knew but those who knew could not give up, before he moved to this 1927 made building restored by Armada... Sabahattin, got two times the cover subject of The New York Times in the first three months in the year 2000… Sabahattin, originally from Trilye (Mudanya, Zeytinbag), of a family which knows the sea, fish and the respect of fish very well, know continues to host his guest in summer as in winter in this wooden house...His sons are helping him... In summer some of the tables overflow the street. -

Public Istanbul

Frank Eckardt, Kathrin Wildner (eds.) Public Istanbul Frank Eckardt, Kathrin Wildner (eds.) Public Istanbul Spaces and Spheres of the Urban Bibliographic information published by the Deutsche Nationalbib- liothek The Deutsche Nationalbibliothek lists this publication in the Deut- sche Nationalbibliografie; detailed bibliographic data are available in the Internet at http://dnb.d-nb.de © 2008 transcript Verlag, Bielefeld This work is licensed under a Creative Commons Attribution-NonCommercial-NoDerivatives 3.0 License. Cover layout: Kordula Röckenhaus, Bielefeld Cover illustration: Kathrin Wildner, Istanbul, 2005 Proofred by: Esther Blodau-Konick, Kathryn Davis, Kerstin Kempf Typeset by: Gonzalo Oroz Printed by: Majuskel Medienproduktion GmbH, Wetzlar ISBN 978-3-89942-865-0 CONTENT Preface 7 PART 1 CONTESTED SPACES Introduction: Public Space as a Critical Concept. Adequate for Understanding Istanbul Today? 13 FRANK ECKARDT Mapping Social Istanbul. Extracts of the Istanbul Metropolitan Area Atlas 21 MURAT GÜVENÇ Contested Public Spaces vs. Conquered Public Spaces. Gentrification and its Reflections on Urban Public Space in Istanbul 29 EDA ÜNLÜ YÜCESOY Globalization, Locality and the Struggle over a Living Space. The Case of Karanfilköy 49 SEVIL ALKAN Fortress Istanbul. Gated Communities and the Socio-Urban Transformation 83 ORHAN ESEN/TIM RIENIETS Peripheral Public Space. Types in Progress 113 ELA ALANYALI ARAL Old City Walls as Public Spaces in Istanbul 141 FUNDA BA BÜTÜNER Regenerating »Public Istanbul«. Two Projects on the Golden Horn 163 SENEM ZEYBEKOLU Public Transformation of the Bosporus. Facts and Opportunities 187 EBRU ERDÖNMEZ/SELIM ÖKEM PART 2 EXPERIENCING ISTANBUL Introduction: Spaces of Everyday Life 209 KATHRIN WILDNER Istanbul's Worldliness 215 ASU AKSOY Public People. -

Yigit Yazici Born in 1969 in Turkey. Graduated from Mimar Sinan University Istanbul, Fine Arts Faculty Painting Department in 1

Yigit Yazici Born in 1969 in Turkey. Graduated from Mimar Sinan University Istanbul, Fine Arts Faculty Painting Department in 1982. Lives and works in Istanbul. Solo Exhibitions 2015 “Fountain“ Pébéo Contemporary Gallery, Gémenos Marseille, France ‘La Felicita’, Zorlu Center, Beyaz Art, Istanbul, Turkey 2014 ‘Consciousness’, Mart Collection Art Gallery, Ankara, Turkey 2013 ‘Peace Unlimited’, Gallery AP87, Den Haag, The Netherlands ‘E-Cosi’ Linart, Istanbul, Turkey ‘Layers of a Tale’ Art on 56th, Beirut, Lebanon 2012 ‘Nobody’s Business But the Turk’s’ , Tally Beck Contemporary, New York, USA 2010 ‘Look into Yourself’, Bali Art Gallery, Istanbul, Turkey ‘Oxygen’, La Table de Tee Tally Beck Contemporary, Bangkok, Thailand ‘Yigit Yazıcı Painting Exhibition’, Armoni Art Gallery, Ankara, Turkey 2008 ‘Color of the Cities’, Cırağan Palace Kempinski, Istanbul, Turkey 2007 ‘19’ Gallery G–Art, Istanbul, Turkey 2006 ‘My Family’, Article Art Gallery, Istanbul, Turkey 2005 ‘RTU100005’ Creamart Gallery, Istanbul, Turkey 2004 Gallery Artist Çukurcuma, Istanbul, Turkey ‘The Place I was Born’, Zafer Plaza, Bursa, Turkey 2003 ‘Sketch Books’, Panini, Mayadrom, Istanbul, Turkey ‘Meeting’, Turuncu Art Gallery, Bodrum, Turkey 2002 Milli Piyango Art Gallery, Ankara, Turkey 2001 ‘Functional Art’, Dem–Art Gallery, Istanbul, Turkey Isbank Art Gallery, Izmir, Turkey Seattle Town Hall, USA 1998 ‘Functional Art’, Akmerkez, Istanbul, Turkey 1997 ‘Yesterday–Today’, Ataturk Center of Culture, Istanbul, Turkey 1996 ‘Second Step’, GYIAD, Istanbul, Turkey 1995 ‘Pages’, Maya -

2017 Finalists

ICSC Solal Marketing Awards 2017 Finalists The ICSC Solal Marketing Awards bring together the very best of retail marketing across Europe and South Africa to reward those with the most effective campaigns. By recognising best practices and outstanding marketing performances, the ICSC Solal Marketing Awards are seen as a benchmark of quality throughout the industry. AWARD CATEGORIES BRAND AWARENESS & (RE)POSITIONING EMERGING TECHNOLOGY This category aims to reward entrants who have This category focuses on campaigns that are driven successfully and creatively changed or consolidated primarily via new technologies such as hardware, the customer perception of their centre. It may address software, big data, digital tools and digital channels. a shift in the behaviour of shoppers or a change in Programmes can include any of the following elements their profile, a new competitor or a significant change as part of a clear marketing strategy: innovative and in the centre. It should demonstrate innovation in the effective use of websites, mobile technology, augmented techniques used to bring about tangible, measurable reality, location-based technologies, big data or any new results and could involve advertising, PR, social media, integrated digital innovations. mobile technology and communication, research or events. FOOTFALL ACTIVATION This category is geared towards campaigns and activities BUSINESS-TO-BUSINESS designed primarily to generate footfall traffic within the This category acknowledges success in targeting a mall. The footfall could be for a one-off activity or for business audience rather than consumers and rewards more long-lasting initiatives. It could relate to the type creative originality and cost-effective results. It is geared of shopper in terms of profile and quality and not merely toward campaigns as it relates to tenants, mall operators, to the volume of shoppers. -

Istanbul City Guide

ISTANBUL CITY GUIDE Index Istanbul p 4 History p 5 Neighbourhood Districts p 6 The Big Sights p 9 Eating/Drinking p 11 Bars/Clubs p 13 Arts/Entertainment p 15 Shopping/Fashion p 17 Sport/Leisure p 20 Media p 21 Practical Stuff p 22 Useful Words and Phrases p 27 3 Istanbul City Guide Old Istanbul is the crowded streets of the Grand Bazaar, magnificent mosques, hamams (bathouses), and grand palaces of the Ottoman Empire. Headscarved women walk down the cobbled lanes and men smoke apple tobacco from a nargileh (water pipe) to a soundtrack of the Muezzin’s call to prayer. New Istanbul was voted 2007 design capital by Wallpaper* magazine. It’s boutiques selling one-offs by globally recognised Turkish designers and the Cihangir districts’ clubs, bars and restaurants rival Soho. The “Istanbul Modern” – showcases Turkey’s contemporary art. In Istanbul both these worlds co-exist. It’s a vital, ever changing city, charged with energy, creativity and commerce. Other cities claim to be at the crossroads of Europe and Asia – but only Istanbul can legitimately claim to straddle both continents. Split by the Bosphorus the western bank of the city is in Europe whilst the eastern side is in Asia. Istanbul is surrounded on 3 sides by water – as well as the Bosphorus there is the Sea of Marmara to the south of the city, and a narrow inlet known as the Golden Horn splits the European side. Istanbul is one of the biggest cities in Europe – home to a population of ap- proximately 12 million. -

Finalist Brand Awareness & (Re) Positioning

2017 ICSC Solal Marketing Awards Finalist Brand Awareness & (Re) Positioning Shopping Centres Akasya Kültür Sanat (AKS ) Akasya Shopping Centre Istanbul, Turkey Owner: AKIS REIT Management Company: AKYASAM Alameda Market - The New Pop-Up Concept Alameda Shop & Spot Porto, Portugal Owner: EPFPorto Antas, Sociedade Anónima Management Company: CBRE First Store by Alexa Alexa Berlin, Germany Owner: Union Investment Management Company: Sierra Germany GmbH Almada Forum Everything to Be Happy Almada Forum Almada, Portugal Owner: Multi Management Company: Multi Portugal Armazéns do Chiado "Lisbon Music Point" Armazén do Chiado Lisbon, Portugal Owner: CRI Management Company: Multi Portugal All in The Name of Fashion Baneasa Shopping City Bucuresti, Romania Owner: Baneasa Developments Management Company: Baneasa Developments Neighbouring Village Beylikdüzü Migros Shopping Center İstanbul, Turkey Owner: Migros Ticaret A.Ş. Management Company: Ece Turkey Cresta Magic Cresta Shopping Centre Johannesburg, South Africa Owner: Pareto Ltd Management Company: Mowana Properties Today We Are Sixteen ! Europark Maribor Maribor, Slovenia Owner: SES Spar European Shopping Centers Gmbh Management Company: Europark d.o.o. “Queima Connosco" Festival by Forum Coimbra Forum Coimbra Coimbra, Portugal Owner: Greenbay Management Company: Multi Portugal Forum Sintra - Shaping Christmas out of Play-Doh Forum Sintra Rio de Mouro, Portugal Owner: Multi Asset Management Management Company: Multi Portugal Remains of Love İstinyePark İSTANBUL, Turkey Owner: Orjin Group - -

Istanbul Fact Sheet Ingilizce Revize

İstanbul Levent LOCATION Wyndham Grand İstanbul Levent is located at Büyükdere Street, Levent where the city's most modern business and shopping centers are founded. This advantageous location oers many alternatives to guests travelling for business & leisure purposes in order to meet their superior expectations. Wyndham Grand Levent with its 32 floors will contribute to the dynamics of the city outstandingly together with River Plaza Business Center and ÖzdilekPark İstanbul Shopping Center within the scope of the Özdilek Center project. Büyükdere Caddesi No. 181 34394 Levent, Şişli İstanbul / Turkey Tel: +90 (212) 386 10 00 Fax: +90 (212) 386 10 10 [email protected] | [email protected] wyndhamgrandlevent.com | wyndham.com İstanbul Levent HOTEL FACILITIES Foyer • 389 guest room • 19 meeting & banquet venues between 1270 m² – 54 m² area with modern infrastructure • Poolside venue with 1250 pax capacity for organizations in summer • Heliport • Indoor parking • Direct metro access • 3200 m² SPA Center • Indoor and outdoor swimming pool • Executive Lounge • Restaurants and bars • Concierge • Valet Parking • Business Center • High speed wired & wireless internet access • Laundry & dry cleaning service • Handicapped rooms • Private reception for groups and stand area Lobby Executive Lounge İstanbul Levent GUEST ROOM FACILITIES & CATEGORIES Wyndham Grand İstanbul Levent is overlooking the city skyline and oering 360 degrees of beauty, provides guest rooms with combination of comfort and luxury besides the beautiful city views; -

Torun Center Catalogue

A NEW PERSPECTIVE TO ISTANBUL Inspired by this connecting feature of Istanbul, where the continents of Asia and Europe, the west and the east, the old and the new, the modern and the traditional, the universal and the local are together in a great harmony, Torun Center provides new definitions for the business world and modern life. Based on its great experience and knowledge, Torun Center brings a new breath and a new perspective to Istanbul, the world’s most colorful and cosmopolitan city. Welcome to the brilliant world of Torun Center rising up with our philosophy “WORTH TO INVEST, WORTH TO LIVE” in Mecidiyeköy located in the center of Istanbul, by the side of the Bosporus Bridge and at the heart of the business world. Already one of the most charming cities of the world with its modern face, business power and unique scene of Bosphorus, Istanbul is preparing to gain a new value. Inspired by the connecting characteristic of the great city which joins two continents together, Torun Center brings in Istanbul a new life and a fresh breath by reuniting life, business and sociality within the same project. WHERE ISTANBUL’S HEART BEATS Torun Center is located just beside Bosphorus Bridge in Mecidiyeköy, the new axis of business world. It is collated with life, prestige and luxury in the real center of ‹stanbul where millions meet every day. YAVUZ ISTANBUL SULTAN SELİM AIRPORT BRIDGE 34 KM İSTİNYEPARK MALL MASLAK SARIYER FSM BRIDGE KANYON MALL MALL OF İSTANBUL AKMERKEZ MALL ZORLU MALL LEVENT MECIDIYEKOY GAYRETTEPE BOSPHORUS CEVAHIR MALL AMERICAN HOSPITAL BESIKTAS NISANTASI BOSPHORUS BRIDGE CIRAGAN TAKSIM PALACE BAHCESEHIR UNIVERSITY DOLMABAHCE PALACE GOLDEN HORN USKUDAR BOSPHORUS ATATURK AIRPORT TOPKAPI 20 KM PALACE SULTANAHMET SQUARE KADIKOY METRO LINE LIVE IN THE CENTER OF IT ALL Mecidiyeköy becomes the real center of Istanbul with Torun Center. -

An Assessment on Shopping Centers As Consumption Places

KUJES 7(1):65-73, 2021 An Assessment on Shopping Centers as Consumption Places Sevgi Ozturka, Oznur Isinkaralarb, Feyza Kesimoglu*, c a Department of Landscape Architecture, Faculty of Engineering and Architecture, Kastamonu University, Kastamonu, Turkey e-mail: [email protected] ORCID ID: 0000-0002-3383-7822 bDepartment of Landscape Architecture, Faculty of Engineering and Architecture, Kastamonu University, Kastamonu, Turkey e-mail: [email protected] ORCID ID: 0000-0001-9774-5137 cDepartment of Landscape Architecture, Faculty of Engineering and Architecture, Kastamonu University, Kastamonu, Turkey ORCID ID: 0000-0003-2955-9054 e-mail: [email protected] ARTICLE INFO ABSTRACT RESEARCH ARTICLE Consumption was a phenomenon that occurred to meet basic needs in ancient times. It is no Received: May: 17. 2021 longer basic essential for individuals with changing times and technology. Urban Reviewed: June: 07. 2021 consumption places also included commercial products accessible within walking distance Accepted: June: 09. 2021 in the city in the past. Today, it has turned into shopping malls that have multiple functions Keywords: individually and gain an image of the city as well as consumption. Within the scope of the Consumption, study, the historical development process of the shopping centers, which are common in Urban consumption places, Shopping centers. today's cities, has been examined. Markets, agoras, forums, passages, bazaars, multi-storey Corresponding Author: stores, and today's shopping centers and the missions of these places in the city are dealt *E-mail:[email protected] with temporally. In the research, the change of the concept of consumption in the historical process has been evaluated. -

Industry Real Estate Overview Turkish Gross Domestic Product (GDP) at Current Prices Rose by 12.7% on the Year in 2008 to TRY 950.144 Bln

Industry Real Estate Overview Turkish gross domestic product (GDP) at current prices rose by 12.7% on the year in 2008 to TRY 950.144 bln. For the first quarter of 2008 the Turkish GDP at current prices grew by 17.5% year-on- year to TRY 221.704 bln. In 2007 Turkey's GDP at current prices marked a 12.9% annual increase and reached TRY 856.387 bln. In July 2008 the consumer price index (CPI) rose by 12.06% year-on-year. Housing market marked a highest increase on the annual basis by 21.84%. In 2007, the real estate sector had a 4.0% share of the gross national product (GNP), compared to 3.7% in 2006. At current prices, the real estate sector grew by 23.7% year- on-year in 2007. Share of Construction in GDP Period 2008 Q4 2008 Q3 2008 Q2 2008 Q1 2008 Construction 12.03 8.26 9.36 11.11 (bln TRY) 40,76 Share in 5.2% 3.1% 3.9% 5.2% GDP 4,3% Growth Rate 15.3% 20.3% 20.6% 16.5% 17,8% Share of Real Estate, Renting and Business Activities in GDP Real Estate, Renting and Business Activities at Share of Period Growth Rate Current Prices GNP (bln TRY) 2007 34.412 4.0% 23.7% 2006 27.823 3.7% 23.0% 2005 22.614 3.5% 19.7% Source: Turkish Statistical Institute Ratings (Long Term TRY) Agency Rating Date Standard&Poors BB (Negative) Apr 3, 2008 JC R BB- (Stable) Dec 28, 2007 Fitch BB- (Stable) May 10, 2007 Moody's Ba3 (Stable) Dec 14, 2005 Source: www.turkisheconomy.org.uk History & Geography The largest cities in Turkey are Istanbul, Ankara, Izmir, Bursa, Adana and Gaziantep.