Estimating the NAIRU in Australia

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Total and Short-Term Unemployment and the Recent Behavior of Prices and Wages

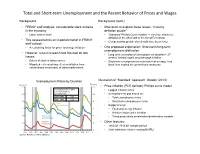

Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Background Background (cont.) • FRBNY staff analysis: considerable slack remains • Motivation to explore these issues: “missing in the economy deflation puzzle” • Labor market flows • “Standard” Phillips Curve models → very low inflation or deflation in the aftermath of the Great Recession • This assessment is an important factor in FRBNY • Compensation growth also should have been lower staff outlook • A restraining factor for price- and wage-inflation • One proposed explanation: Short-term/long-term unemployment distinction • However, recent research has focused on two • Long-term unemployed (unemployment duration > 27 issues: weeks): limited impact on price/wage inflation • Extent of slack in labor market • Short-term unemployment near historical average: less • Magnitude of restraining effect on inflation from slack than implied by conventional measures conventional measure(s) of labor market slack Unemployment Rates by Duration Illustration of “Standard” Approach: Gordon (2013) Percent Percent 12 12 • Price-inflation (PCE deflator) Phillips curve model: Correlation Between Short- • Lagged inflation terms term and Long-term 10 Unemployment 10 • Unemployment gap based on: 1976—2007 0.63 • Total unemployment rate 1976—2013 0.28 8 8 • Short-term unemployment rate Total Unemployment • Supply shocks: 6 6 • Food and energy inflation • Relative import price inflation 4 Short-term 4 • Trend productivity acceleration/deceleration variable Unemployment Long-term • Other features: 2 Unemployment 2 • 1960:Q1-2013:Q1 sample period 0 0 • Joint estimation of time-varying NAIRU 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 4 Source: Bureau of Labor Statistics Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Evaluation of Short-term vs. -

New Keynesian Macroeconomics: Empirically Tested in the Case of Republic of Macedonia

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Josheski, Dushko; Lazarov, Darko Preprint New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia Suggested Citation: Josheski, Dushko; Lazarov, Darko (2012) : New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia, ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften, Leibniz-Informationszentrum Wirtschaft, Kiel und Hamburg This Version is available at: http://hdl.handle.net/10419/64403 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu NEW KEYNESIAN MACROECONOMICS: EMPIRICALLY TESTED IN THE CASE OF REPUBLIC OF MACEDONIA Dushko Josheski 1 Darko Lazarov2 Abstract In this paper we test New Keynesian propositions about inflation and unemployment trade off with the New Keynesian Phillips curve and the proposition of non-neutrality of money. -

Revised Proof

Housing Policy in Australia “Australia has avoided a recession in its economic system for nigh on 30 years. Good management our political leaders claim. But Australia’s housing system has failed throughout this time: homelessness has risen; insecure and unaffordable rental are common-place; the over-valuing of homeownership has escalated; and a massive shortage of social and affordable housing has been allowed to develop. How is such neglect or mismanagement of Australians’ housing dreams possible? This book explains why and what to do about it. Pawson, Milligan and Yates carefully document compelling evidence on these issues to provide a contemporary and robust analysis of the when, where, how and why of housing problems in Australia. Moreover, the authors provide the policy solutions and actions to be taken by Federal, State and local governments, as well as the development, fnance and property management industries. Pawson, Milligan and Yates are Australia’s foremostPROOF housing analysts. This book is essential reading for anyone with an interest or a care in reforming Australia’s housing system to be once again ft for all Australians.” —Ian Winter, Housing consultant, and Director, Australian Housing and Urban Research Institute 2000–17 “Housing policy and housing systems are rapidly changing and profoundly reshaping access to affordable and high quality housing across all Australia’s cities and regions. Housing Policy in Australia superbly harnesses international evidence and more than two decades of experience to not only analyse but also provide potential solutions to the current housing policy impasse. The book’s comprehen- sive canvassing of housing system diversity—tenures, social differentiation, histor- ical trends—will become necessary reading for housing practitioners and students. -

Fostering Employment for People with Intellectual Disability: the Evidence to Date

Fostering employment for people with intellectual disability: the evidence to date Erin Wilson and Robert Campain August 2020 This document has been prepared by the Centre for Social Impact Swinburne for Inclusion Australia as part of the ‘Employment First’ project, funded by the National Disability Insurance Agency. ‘ About this report This report presents a set of ‘evidence pieces’ commissioned by Inclusion Australia to inform the creation of a website developed by Inclusion Australia as part of the ‘Employment First’ (E1) project. Suggested citation Wilson, E. & Campain, R. (2020). Fostering employment for people with intellectual disability: the evidence to date, Hawthorn, Centre for Social Impact, Swinburne University of Technology. Research team The research project was undertaken by the Centre for Social Impact, Swinburne University of Technology, under the leadership of Professor Erin Wilson together with Dr Robert Campain. The research team would like to acknowledge the contributions of Ms Jenny Crosbie, Dr Joanne Qian, Ms Aurora Elmes, Dr Andrew Joyce and Mr James Kelly (of the Centre for Social Impact) and Dr Kevin Murfitt (Deakin University) who have collaborated in the sharing of information and analysis regarding a range of research related to the employment of people with a disability. Page 2 ‘ Contents Background 5 About the research design 6 Structure of this report 7 Synthesis: How can employment of people with intellectual disability be fostered? 8 Evidence piece 1: Factors positively influencing the employment of people -

Invasive Meningococcal Disease (IMD) an Update on Prevention in Australia Prof Robert Booy, NCIRS

Invasive Meningococcal Disease (IMD) An update on prevention in Australia Prof Robert Booy, NCIRS Declaration of interests: RB consults to vaccine companies but does not accept personal payment Invasive Meningococcal Disease Caused by the bacterium Neisseria meningitidis1 • Meningococci are classified into serogroups that are determined by the components of the polysaccharide capsule1 • Globally, 6 serogroups most commonly cause disease2 A B C W X Y • In Australia, three serogroups cause the majority of IMD3 B W Y Cross-section of N. meningitidis bacterial cell wall (adapted from Rosenstein et al)4 1. Australian Technical Advisory Group on Immunisation (ATAGI). The Australian Immunisation Handbook 10th Edition (2018 update) . Canberra: Australian Government Department of Health, 2018 [Accessed September 2018] 2. Meningococcal meningitis factsheet No 141. World Health Organization website. http://www.who.int/mediacentre/factsheets/fs141/en/ [Accessed February 2017] 3. Lahra and Enriquez. Commun Dis Intell 2016; 40 (4):E503-E511 4. Rosenstein NE, et al. N Engl J Med. 2001; 344:1378-1388 Invasive meningococcal disease (IMD) in Australia • Overall, the national incidence of invasive meningococcal disease (IMD) in Australia is low • From 2003 to 2013, there was a large decrease in the number AUS notifications: 99% drop in Men C! - after the introduction of 2003 meningococcal C (Men C) dose at 12 months to National Immunisation Program (NIP) – catch-up vacc’n 2-19 year olds (herd immunity <1 & >20yrs) • & reduced smoking +improved SES: 55% drop in Men B! Without a vaccine program • However, in recent years the rate of IMD has increased: 2017 had the highest rate in 10 years • Men W and Y now important in older adults Notifications of invasive meningococcal disease, Australia, 1992- 2017, by year, all serogroups 2013-2017: 4 yrs 3rd Age peak 60-64 yrs W and Y 2017:2018: 383281 cases Highest2019: number? fewer of cases since 2006 Nat’l Men C program from 2003 Adapted from National Notifiable Diseases Surveillance System1 1. -

The Nairu Concept, Its Phillips Curve Origins and Its Evolution in Terms of the Economic Policy Debate

7+(1$,58&21&(37±0($685(0(17 81&(57$,17,(6+<67(5(6,6$1'(&2120,& 32/,&<52/( 30&$'$0$1'.0&02552: 7$%/(2)&217(176 ,QWURGXFWRU\5HPDUNV &KDSWHUUncertainties concerning model selection : A number of plausible modelling approaches exist for Measuring the NAIRU 1.1 Univariate Methods / Models 1.2 Variants of the Expectations Augmented Phillips Curve Approach &KDSWHUProduction of NAIRU estimates for the US, Japan and EU- 15 using a Conventional Bargaining model approach &KDSWHU Empirical Inadequacies : Uncertainties surrounding the NAIRU Point Estimates 3.1 Confidence Intervals 3.2 Results from US and Canadian NAIRU studies &KDSWHU Theoretical Weaknesses : The Notion of Hysteresis Complicates the Interpretation of Changes in the NAIRU &KDSWHU The Nairu Concept, its Phillips Curve Origins and its Evolution in terms of the Economic Policy Debate &RQFOXGLQJ5HPDUNV 2 7+(1$,58&21&(37±0($685(0(17 81&(57$,17,(6+<67(5(6,6$1' (&2120,&32/,&<52/( ,1752'8&725<5(0$5.6 In 1968 Friedman put forward the notion of a “natural” rate of unemployment to encapsulate the idea that a “normal” level of unemployment, roughly equivalent to the amount of frictional and structural unemployment, persists even when the labour market is in equilibrium. Since there are no direct measures of the natural rate, as it is essentially a theoretical construct, one must be satisfied with proxy estimates derived using various methods including that which draws on Tobin’s concept of the non- accelerating inflation rate of unemployment(i.e. the NAIRU). This latter concept has been used extensively since the 1970s to show that policy makers are not in a position to buy permanent reductions in unemployment by tolerating a higher rate of inflation. -

The Labor Market and the Phillips Curve

4 The Labor Market and the Phillips Curve A New Method for Estimating Time Variation in the NAIRU William T. Dickens The non-accelerating inflation rate of unemployment (NAIRU) is fre- quently employed in fiscal and monetary policy deliberations. The U.S. Congressional Budget Office uses estimates of the NAIRU to compute potential GDP, that in turn is used to make budget projections that affect decisions about federal spending and taxation. Central banks consider estimates of the NAIRU to determine the likely course of inflation and what actions they should take to preserve price stability. A problem with the use of the NAIRU in policy formation is that it is thought to change over time (Ball and Mankiw 2002; Cohen, Dickens, and Posen 2001; Stock 2001; Gordon 1997, 1998). But estimates of the NAIRU and its time variation are remarkably imprecise and are far from robust (Staiger, Stock, and Watson 1997, 2001; Stock 2001). NAIRU estimates are obtained from estimates of the Phillips curve— the relationship between the inflation rate, on the one hand, and the unemployment rate, measures of inflationary expectations, and variables representing supply shocks on the other. Typically, inflationary expecta- tions are proxied with several lags of inflation and the unemployment rate is entered with lags as well. The NAIRU is recovered as the constant in the regression divided by the coefficient on unemployment (or the sum of the coefficient on unemployment and its lags). The notion that the NAIRU might vary over time goes back at least to Perry (1970), who suggested that changes in the demographic com- position of the labor force would change the NAIRU. -

Urgent Factsheet

Background This factsheet provides an overview of the influence of climate change on extreme rainfall and flooding. As the heavy downpours and thunderstorms begin to hit Victoria and Australia’s southeast, some of Victoria’s most intense rainfall in decades is expected to fall over the next two to three days. Across the northern and central regions of the state, 100- 200 mm is expected over three days, while rain totals may reach 250mm+ in the northeast ranges. Some parts are expected to receive more than 50 mm of rain in one hour. As a result, dangerous and widespread flash flooding is expected across Victoria. Key points 1. Climate change is influencing all extreme rainfall events. The warmer atmosphere holds more moisture, about 7% more than previously. This increases the risk of heavier downpours. 2. Globally, there are more areas with significant increases in heavy rainfall events than with decreases. 3. Extreme rainfall events like the Victoria rains are expected to further increase in intensity across most of Australia. 4. While there isn't a significant trend in observed extreme rainfall in Victoria yet, maximum one-day rainfall is projected to increase by 2-23% in Victoria by the end of the century if greenhouse gas emissions continue to rise. 5. It is critical that communities and emergency services have access to information about rainfall in a changing climate to ensure they can prepare for the future. The influence of climate change on extreme rainfall The heavy downpours across southeast Australia are yet another reminder of how extreme weather events place lives, property and critical infrastructure at risk. -

Cranking up the Intensity: Climate Change and Extreme Weather Events

CRANKING UP THE INTENSITY: CLIMATE CHANGE AND EXTREME WEATHER EVENTS CLIMATECOUNCIL.ORG.AU Thank you for supporting the Climate Council. The Climate Council is an independent, crowd-funded organisation providing quality information on climate change to the Australian public. Published by the Climate Council of Australia Limited ISBN: 978-1-925573-14-5 (print) 978-1-925573-15-2 (web) © Climate Council of Australia Ltd 2017 This work is copyright the Climate Council of Australia Ltd. All material Professor Will Steffen contained in this work is copyright the Climate Council of Australia Ltd Climate Councillor except where a third party source is indicated. Climate Council of Australia Ltd copyright material is licensed under the Creative Commons Attribution 3.0 Australia License. To view a copy of this license visit http://creativecommons.org.au. You are free to copy, communicate and adapt the Climate Council of Australia Ltd copyright material so long as you attribute the Climate Council of Australia Ltd and the authors in the following manner: Cranking up the Intensity: Climate Change and Extreme Weather Events by Prof. Lesley Hughes Professor Will Steffen, Professor Lesley Hughes, Dr David Alexander and Dr Climate Councillor Martin Rice. The authors would like to acknowledge Prof. David Bowman (University of Tasmania), Dr. Kathleen McInnes (CSIRO) and Dr. Sarah Perkins-Kirkpatrick (University of New South Wales) for kindly reviewing sections of this report. We would also like to thank Sally MacDonald, Kylie Malone and Dylan Pursche for their assistance in preparing the report. Dr David Alexander Researcher, — Climate Council Image credit: Cover Photo “All of this sand belongs on the beach to the right” by Flickr user Rob and Stephanie Levy licensed under CC BY 2.0. -

Two Approaches for Measuring the NAIRU Considered

TI 2007-017/1 Tinbergen Institute Discussion Paper Derived Measurement in Macroeconomics: Two Approaches for Measuring the NAIRU Considered Peter Rodenburg University of Amsterdam. Tinbergen Institute The Tinbergen Institute is the institute for economic research of the Erasmus Universiteit Rotterdam, Universiteit van Amsterdam, and Vrije Universiteit Amsterdam. Tinbergen Institute Amsterdam Roetersstraat 31 1018 WB Amsterdam The Netherlands Tel.: +31(0)20 551 3500 Fax: +31(0)20 551 3555 Tinbergen Institute Rotterdam Burg. Oudlaan 50 3062 PA Rotterdam The Netherlands Tel.: +31(0)10 408 8900 Fax: +31(0)10 408 9031 Most TI discussion papers can be downloaded at http://www.tinbergen.nl. Derived Measurement in Macroeconomics: Two Approaches for Measuring the NAIRU considered ∗ Peter Rodenburg Faculty of Economics and Econometrics and Faculty of European Studies University of Amsterdam Spuistraat 134 1012 VB Amsterdam The Netherlands Tel: 0031 20-525 4660 E-mail: [email protected] http://home.medewerker.uva.nl/p.rodenburg/ Abstract: This paper investigates two different procedures for the measurement of the NAIRU; one based on structural modeling while the other is a statistical approach using Vector Auto Regression (VAR)-models. Both measurement procedures are assessed by confronting them with the dominant theory of measurement, the Representation Theory of Measurement, which states that for sound measurement a strict isomorphism (strict one-to- one mapping) is needed between variations in the phenomenon (the NAIRU) and numbers. The paper argues that shifts of the Phillips-curve are not a problem for the structural approach to measurement of the NAIRU, as the NAIRU itself is a time-varying concept. -

Vehicle-Related Flood Fatalities in Australia, 2001–2017

University of Wollongong Research Online Faculty of Science, Medicine and Health - Papers: Part B Faculty of Science, Medicine and Health 1-1-2020 Vehicle-related flood fatalities in ustrA alia, 2001–2017 Mozumdar Ahmed Katharine A. Haynes University of Wollongong, [email protected] Mel Taylor Follow this and additional works at: https://ro.uow.edu.au/smhpapers1 Publication Details Citation Ahmed, M., Haynes, K. A., & Taylor, M. (2020). Vehicle-related flood fatalities in ustrA alia, 2001–2017. Faculty of Science, Medicine and Health - Papers: Part B. Retrieved from https://ro.uow.edu.au/ smhpapers1/1326 Research Online is the open access institutional repository for the University of Wollongong. For further information contact the UOW Library: [email protected] Vehicle-related flood fatalities in ustrA alia, 2001–2017 Abstract © 2020 The Authors. Journal of Flood Risk Management published by Chartered Institution of Water and Environmental Management and John Wiley & Sons Ltd. This study analyses the circumstances of vehicle-related flood fatalities between 2001 and 2017, in Australia. The research identified 96 deaths from 74 incidents during this period. The aim of this analysis is to understand the demographic, spatial and temporal patterns, and the situational conditions in which those (n = 96) deaths have occurred. This is important for informing efficient and strategic risk reduction strategies to reduce vehicle related deaths and injuries in floodwater. Data were accessed from the Australian National Coronial Information System (NCIS), which includes witness and police statements, forensic documents, and detailed coronial findings. Analysis was conducted in two phases. In phase one, data were coded and categorised according to a range of factors previously identified as significant inehicle-r v elated flood fatalities internationally. -

The NAIRU, Unemployment and Monetary Policy

Journal of EconomicPerspectives-Volume 11, Number1-Winter 1997-Pages 33-49 The NAIRU, Unemployment and Monetary Policy Douglas Staiger, James H. Stock, and Mark W. Watson S ince Milton Friedman's(1968) presidentialaddress to the AmericanEco- nomic Association, one of the most enduring ideas in macroeconomics has LJ been that inflation will increase when unemployment persists below its nat- ural rate, the so-called NAIRU, or nonaccelerating inflation rate of unemployment. But what is the NAIRU? Is it 5.8 percent as estimated by the CBO (1996)? Is it 5.7 percent as used by the Council of Economic Advisors (1996) or 5.6 percent as estimated by Gordon (this issue)? Or can unemployment safely go much lower, as recently argued by Eisner (1995a,b)? For all of 1995 and the first two quarters of 1996, unemployment hovered around 5.6 percent, while inflation remained in check. This has led to a debate among academics and policymakers over whether there has been a decline in the NAIRU and, more generally, whether economists should continue to rely on unemployment and the NAIRU as indicators of an over- heated economy (Weiner, 1993, 1994; Tootell, 1994; Fuhrer, 1995; Council of Eco- nomic Advisors, 1996, pp. 51-57; Congressional Budget Office, 1996, pp. 5, 27). At the heart of this debate lie several empirical questions. Has the NAIRU declined in recent years? What is the current value of the NAIRU? How confident should economists be in these estimates? How useful is knowledge of NAIRU in *Douglas Staigeris AssistantProfessor of PoliticalEconomy, Kennedy School of Government, Harvard University,Cambridge, Massachusetts.