Keynes After Sraffa and Kaldor: Effective Demand, Accumulation and Productivity Growth Alcino F. Camara-Neto and Matías Verne

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Total and Short-Term Unemployment and the Recent Behavior of Prices and Wages

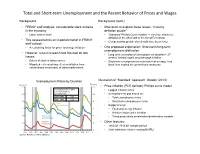

Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Background Background (cont.) • FRBNY staff analysis: considerable slack remains • Motivation to explore these issues: “missing in the economy deflation puzzle” • Labor market flows • “Standard” Phillips Curve models → very low inflation or deflation in the aftermath of the Great Recession • This assessment is an important factor in FRBNY • Compensation growth also should have been lower staff outlook • A restraining factor for price- and wage-inflation • One proposed explanation: Short-term/long-term unemployment distinction • However, recent research has focused on two • Long-term unemployed (unemployment duration > 27 issues: weeks): limited impact on price/wage inflation • Extent of slack in labor market • Short-term unemployment near historical average: less • Magnitude of restraining effect on inflation from slack than implied by conventional measures conventional measure(s) of labor market slack Unemployment Rates by Duration Illustration of “Standard” Approach: Gordon (2013) Percent Percent 12 12 • Price-inflation (PCE deflator) Phillips curve model: Correlation Between Short- • Lagged inflation terms term and Long-term 10 Unemployment 10 • Unemployment gap based on: 1976—2007 0.63 • Total unemployment rate 1976—2013 0.28 8 8 • Short-term unemployment rate Total Unemployment • Supply shocks: 6 6 • Food and energy inflation • Relative import price inflation 4 Short-term 4 • Trend productivity acceleration/deceleration variable Unemployment Long-term • Other features: 2 Unemployment 2 • 1960:Q1-2013:Q1 sample period 0 0 • Joint estimation of time-varying NAIRU 1976 1979 1982 1985 1988 1991 1994 1997 2000 2003 2006 2009 2012 4 Source: Bureau of Labor Statistics Total and Short-term Unemployment and the Recent Behavior of Prices and Wages Evaluation of Short-term vs. -

The Principle of Effective Demand and the State of Post Keynesian Monetary Economics

The University of Adelaide School of Economics Research Paper No. 2008-04 The Principle of Effective Demand and the State of Post Keynesian Monetary Economics Colin Rogers The principle of effective demand and the state of post Keynesian monetary economics Colin Rogers (Revised 20/08/08) School of Economics University of Adelaide Introduction Keynesians of all shades have generally misunderstood the theoretical structure of the General Theory. What is missing is an appreciation of the principle of effective demand. As Laidler (1999) has documented, Old Keynesians largely fabricated the theoretical basis of the Keynesian Revolution and retained the `classical' analysis of long-period equilibrium. Old Keynesians generally took Frank Knight's (1937) advice to ignore the claim to revolution in economic theory and interpreted the General Theory as another contribution to the theory of business cycles. This is most obvious from the Old Keynesian reliance on wage rigidity to generate involuntary unemployment. But for Keynes (1936, chapter 19), wage and price stickiness is the `classical' explanation for unemployment to be contrasted with his explanation, in terms of the principle of effective demand, where the flexibility of wages and prices cannot automatically shift long-period equilibrium to full employment. New Keynesians have continued the `classical' vision by providing the microeconomic foundations for the `ad hoc' rigidities employed by Old 1 Keynesians. Generally, New Keynesians do not question the underlying `classical' vision. Post Keynesians have always questioned the `classical' vision but have not succeeded as yet in agreeing on what the principle of effective demand is1. There should, however, be no grounds for misunderstanding of the principle of effective demand given Keynes's exposition in the General Theory and Dillard's (1948) synopsis. -

KALDOR's WAR J.E. King*

DEPARTMENT OF ECONOMICS ISSN 1441-5429 DISCUSSION PAPER 25/07 KALDOR’S WAR * J.E. King * Department of Economics and Finance, La Trobe University, Victoria 3086, Australia Email: [email protected] © 2007 J.E. King All rights reserved. No part of this paper may be reproduced in any form, or stored in a retrieval system, without the prior written permission of the author. Introduction In the 1930s the young Nicholas Kaldor (1908-1986) established himself as one of the world’s leading economic theorists (King 2007). As with so many lives, Kaldor’s was turned around by the Second World War. This was not the result of enemy action. Although his family in Hungary suffered grievously at the hands of the Nazis, Nicky himself was not called to arms. While he had become a British citizen in 1934, and made enquiries about joining the Civil Service as an economic advisor, he was told that his Hungarian origins would disqualify him from anything other than menial duties in Whitehall. He therefore decided to stay in academia, and relocated to Cambridge with his remaining LSE colleagues in September 1939, when the Ministry of Works took over the School’s Aldwych site in central London .1 Now based at Peterhouse, Kaldor was able to deepen old friendships and develop new ones. A ‘war circus’ of economists began to operate, named by analogy with the ‘Cambridge circus’ of young theorists who had interrogated Keynes in 1930- 1 after the publication of the Treatise on Money and helped to focus his mind on the revolutionary breakthrough of the General Theory (Moggridge 1995, pp. -

Kaldor After Sraffa

BULLETIN OF POLITICAL ECONOMY 13:1 (2019): 1-19 Kaldor after Sraffa ÓSCAR DEJUÁN Abstract: Kaldor led the postKeynesian school in an attempt to project Keynes’ principle of effective demand into the long run, the realm of growth theories. This paper examines Kaldor’s major contributions to growth, technical change, distribution and money, in order to integrate them into the surplus approach. An approach that combines the classical- Sraffian theory of value and distribution with the Keynesian- postKeynesian theory of output and money. An approach that considers capitalism as a demand- constrained system, both in the short run and in the long run, without neglecting the limits derived from the supply side. Keywords: Surplus approach; principle of effective demand; growth and distribution; supermultiplier; Sraffa; Kaldor JEL Codes: B24, E11, E12 INTRODUCTION The lives and intellectual activity of Nicholas Kaldor (1908-1986) and Piero Sraffa (1898-1983) present many similarities and, surprisingly, mutual ignorance. Both worked at the University of Cambridge for more than 30 years. Both were the bastions of the resistance against the marginalist revolution in microeconomics and the Grand Neoclassical Synthesis in macroeconomics. Yet, the communication between them was minimal1. The different personal tempers and different styles of research may explain the lack of communication between them. The mind of Nicholas Kaldor was a boiler in continuous ebullition. His works fill eight volumes, apart from several books in a variety of subjects (N. Kaldor, 1960-80). Regarding Sraffa, we can apply Aquinas’ dictum “Beware of the person of one book”, a sentence that involves an appreciation of the minds with few but coherent and powerful ideas. -

Measuring the Natural Rate of Interest: International Trends and Determinants

FEDERAL RESERVE BANK OF SAN FRANCISCO WORKING PAPER SERIES Measuring the Natural Rate of Interest: International Trends and Determinants Kathryn Holston and Thomas Laubach Board of Governors of the Federal Reserve System John C. Williams Federal Reserve Bank of San Francisco December 2016 Working Paper 2016-11 http://www.frbsf.org/economic-research/publications/working-papers/wp2016-11.pdf Suggested citation: Holston, Kathryn, Thomas Laubach, John C. Williams. 2016. “Measuring the Natural Rate of Interest: International Trends and Determinants.” Federal Reserve Bank of San Francisco Working Paper 2016-11. http://www.frbsf.org/economic-research/publications/working- papers/wp2016-11.pdf The views in this paper are solely the responsibility of the authors and should not be interpreted as reflecting the views of the Federal Reserve Bank of San Francisco or the Board of Governors of the Federal Reserve System. Measuring the Natural Rate of Interest: International Trends and Determinants∗ Kathryn Holston Thomas Laubach John C. Williams December 15, 2016 Abstract U.S. estimates of the natural rate of interest { the real short-term interest rate that would prevail absent transitory disturbances { have declined dramatically since the start of the global financial crisis. For example, estimates using the Laubach-Williams (2003) model indicate the natural rate in the United States fell to close to zero during the crisis and has remained there into 2016. Explanations for this decline include shifts in demographics, a slowdown in trend productivity growth, and global factors affecting real interest rates. This paper applies the Laubach-Williams methodology to the United States and three other advanced economies { Canada, the Euro Area, and the United Kingdom. -

Redalyc.Recovering Effectiveness of Monetary Policy Under A

Investigación Económica ISSN: 0185-1667 [email protected] Facultad de Economía México Ferreira de Mendonça, Helder; Caldas Montes, Gabriel Recovering Effectiveness of Monetary Policy under a Deflationary Environment Investigación Económica, vol. LXVII, núm. 265, julio-septiembre, 2008, pp. 121-144 Facultad de Economía Distrito Federal, México Available in: http://www.redalyc.org/articulo.oa?id=60126504 How to cite Complete issue Scientific Information System More information about this article Network of Scientific Journals from Latin America, the Caribbean, Spain and Portugal Journal's homepage in redalyc.org Non-profit academic project, developed under the open access initiative investigación económica, vol. LXVII, 265, julio-septiembre de 2008, pp. 121-144 Recovering Effectiveness of Monetary Policy under a Deflationary Environment H����� F������� �� M������� G������ C����� M�����* I����������� In the last decade several countries have adopted a strategy for the conduction of a monetary policy based on central bank independence and inflation targeting. Generally speaking, the results suggest success in controlling inflation in several emerging and industrialized economies. Nonetheless, under this new environment, a new problem emerges: the risk of deflation. The main problem, as shown by the Japanese experience, is that falling prices may lock countries into a spiral of economic decline. The core of the idea is: once consumers expect falling prices, they decide to postpone purchases, implying a decrease in demand and a consequent fall in prices by producers, threatening the start of a spiral of fall in output and demand. Furthermore, based on the results presented by a profit maximizing behavior, both prices and output are influenced by expected future prices. -

New Keynesian Macroeconomics: Empirically Tested in the Case of Republic of Macedonia

A Service of Leibniz-Informationszentrum econstor Wirtschaft Leibniz Information Centre Make Your Publications Visible. zbw for Economics Josheski, Dushko; Lazarov, Darko Preprint New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia Suggested Citation: Josheski, Dushko; Lazarov, Darko (2012) : New Keynesian Macroeconomics: Empirically tested in the case of Republic of Macedonia, ZBW - Deutsche Zentralbibliothek für Wirtschaftswissenschaften, Leibniz-Informationszentrum Wirtschaft, Kiel und Hamburg This Version is available at: http://hdl.handle.net/10419/64403 Standard-Nutzungsbedingungen: Terms of use: Die Dokumente auf EconStor dürfen zu eigenen wissenschaftlichen Documents in EconStor may be saved and copied for your Zwecken und zum Privatgebrauch gespeichert und kopiert werden. personal and scholarly purposes. Sie dürfen die Dokumente nicht für öffentliche oder kommerzielle You are not to copy documents for public or commercial Zwecke vervielfältigen, öffentlich ausstellen, öffentlich zugänglich purposes, to exhibit the documents publicly, to make them machen, vertreiben oder anderweitig nutzen. publicly available on the internet, or to distribute or otherwise use the documents in public. Sofern die Verfasser die Dokumente unter Open-Content-Lizenzen (insbesondere CC-Lizenzen) zur Verfügung gestellt haben sollten, If the documents have been made available under an Open gelten abweichend von diesen Nutzungsbedingungen die in der dort Content Licence (especially Creative Commons Licences), you genannten Lizenz gewährten Nutzungsrechte. may exercise further usage rights as specified in the indicated licence. www.econstor.eu NEW KEYNESIAN MACROECONOMICS: EMPIRICALLY TESTED IN THE CASE OF REPUBLIC OF MACEDONIA Dushko Josheski 1 Darko Lazarov2 Abstract In this paper we test New Keynesian propositions about inflation and unemployment trade off with the New Keynesian Phillips curve and the proposition of non-neutrality of money. -

Chapter 19 the Theory of Effective Demand

Chapter 19 The theory of effective demand In essence, the “Keynesian revolution” was a shift of emphasis from one type of short-run equilibrium to another type as providing the appropriate theory for actual unemployment situations. Edmund Malinvaud (1977), p. 29. In this and the following chapters the focus is shifted from long-run macro- economics to short-run macroeconomics. The long-run models concentrated on factors of importance for the economic evolution over a time horizon of at least 10-15 years. With such a horizon the supply side (think of capital accumulation, population growth, and technological progress) is the primary determinant of cumulative changes in output and consumption the trend. Mainstream macro- economists see the demand side and monetary factors as of key importance for the fluctuations of output and employment about the trend. In a long-run perspective these fluctuations are of only secondary quantitative importance. The preceding chapters have chieflyignored them. But within shorter horizons, fluctuations are the focal point and this brings the demand-side, monetary factors, market imper- fections, nominal rigidities, and expectation errors to the fore. The present and subsequent chapters deal with the role of these short- and medium-run factors for the failure of the laissez-faire market economy to ensure full employment and for the possibilities of active macro policies as a means to improve outcomes. This chapter introduces building blocks of Keynesian theory of the short run. By “Keynesian theory”we mean a macroeconomic framework that (a) aims at un- derstanding “what determines the actual employment of the available resources”,1 including understanding why mass unemployment arises from time to time, and (b) in this endeavor ascribes a primary role to aggregate demand. -

Journal of Economic Methodology Sen, Sraffa and the Revival Of

This article was downloaded by: [b-on: Biblioteca do conhecimento online UAC] On: 22 June 2012, At: 07:04 Publisher: Routledge Informa Ltd Registered in England and Wales Registered Number: 1072954 Registered office: Mortimer House, 37-41 Mortimer Street, London W1T 3JH, UK Journal of Economic Methodology Publication details, including instructions for authors and subscription information: http://www.tandfonline.com/loi/rjec20 Sen, Sraffa and the revival of classical political economy Nuno Ornelas Martins a a University of the Azores, Azores, PortugalCentro de Estudos em Gestão e Economia Available online: 22 Jun 2012 To cite this article: Nuno Ornelas Martins (2012): Sen, Sraffa and the revival of classical political economy, Journal of Economic Methodology, 19:2, 143-157 To link to this article: http://dx.doi.org/10.1080/1350178X.2012.683598 PLEASE SCROLL DOWN FOR ARTICLE Full terms and conditions of use: http://www.tandfonline.com/page/terms-and-conditions This article may be used for research, teaching, and private study purposes. Any substantial or systematic reproduction, redistribution, reselling, loan, sub-licensing, systematic supply, or distribution in any form to anyone is expressly forbidden. The publisher does not give any warranty express or implied or make any representation that the contents will be complete or accurate or up to date. The accuracy of any instructions, formulae, and drug doses should be independently verified with primary sources. The publisher shall not be liable for any loss, actions, claims, proceedings, demand, or costs or damages whatsoever or howsoever caused arising directly or indirectly in connection with or arising out of the use of this material. -

Nicholas Kaldor

PROFILES OF WORLD ECONOMISTS 26 NICHOLAS KALDOR NICHOLAS KALDOR – ONE OF THE FIRST CRITICS OF MONETARISM doc. Ing. Ján Iša, DrSc. Known in economic circles as one of the thought in several fields, but it was his work founders of Post-Keynesianism, Nicholas on the theory of distribution and economic Kaldor (1908–1986) ranks among the worl- growth that stirred the greatest reaction. d's foremost economists of the second half Less well-known, however, is Kaldor's con- of the 20th century. Kaldor contributed to tribution to monetary theory, which has long the development of modern economic been standing quietly in the background. Nicholas Kaldor was born in Budapest on 12 May 1908. rous Third World countries, as well as an advisor to central His father was a lawyer and his mother came from wealthy banks and to the United Nations Economic Commission for business family. Although his father had wanted him to Latin America. Most significant, however, was his role as an study law, Kaldor opted for economics. He began his studi- advisor to Labour finance ministers from 1964 to 1968 and es at the University of Berlin in 1925 and then after two 1974 to 1976. After completing his two-year mission in years moved to the London School of Economics (LSE), Geneva in 1949, Kaldor began to work at Cambridge Uni- from which he graduated in 1930. He remained at the LSE versity and became, as John Maynard Keynes had been, a as lecturer until 1947, during which time his colleagues inc- fellow of King's College, Cambridge. -

Old, New and Post Keynesian Perspectives on the Is-Lm Framework: a Contrast and Evaluation

1 OLD, NEW AND POST KEYNESIAN PERSPECTIVES ON THE IS-LM FRAMEWORK: A CONTRAST AND EVALUATION Huw Dixon and Bill Gerrard 1.1 INTRODUCTION The IS-LM framework has been the standard model used for understanding and teaching Keynesian macroeconomics since 1960. Indeed, even a monetarist such as Friedman could subscribe to a modified version of the IS-LM model (1970); Sargent and Wallace (1975) formulated the first New Classical neutrality proposition with an IS-LM model of aggregate demand. The main decisive break from this tradition was Barro's textbook, Macroeconomics, whose first edition was 1984. This relegated the IS-LM analysis to an afterthought at the end of the book; the bulk of the textbook was devoted to the market clearing intertemporal equilibrium approach to macroeco nomics, which had its origins in the work of Lucas and Rapping (1969). In this paper we trace a brief history of the IS-LM framework, and how it has been reinterpreted over the last few decades by economists of an essentially "Keynesian" viewpoint. The IS-LM model was developed as a way of understanding Keynes's General Theory. What defines the IS-LM approach? There are two crucial factors: I. Output is an endogenous variable which is demand-determined. 2. The rate of interest is an endogenous variable, and affects both the demand for goods (investment and possibly consumption) and the demand for money. The IS-LM model can be viewed either as merely a model of aggregate demand (as in the AD-AS model), in which case (1) becomes the demand for output. -

Demand Composition and the Strength of Recoveries†

Demand Composition and the Strength of Recoveriesy Martin Beraja Christian K. Wolf MIT & NBER MIT & NBER September 17, 2021 Abstract: We argue that recoveries from demand-driven recessions with ex- penditure cuts concentrated in services or non-durables will tend to be weaker than recoveries from recessions more biased towards durables. Intuitively, the smaller the bias towards more durable goods, the less the recovery is buffeted by pent-up demand. We show that, in a standard multi-sector business-cycle model, this prediction holds if and only if, following an aggregate demand shock to all categories of spending (e.g., a monetary shock), expenditure on more durable goods reverts back faster. This testable condition receives ample support in U.S. data. We then use (i) a semi-structural shift-share and (ii) a structural model to quantify this effect of varying demand composition on recovery dynamics, and find it to be large. We also discuss implications for optimal stabilization policy. Keywords: durables, services, demand recessions, pent-up demand, shift-share design, recov- ery dynamics, COVID-19. JEL codes: E32, E52 yEmail: [email protected] and [email protected]. We received helpful comments from George-Marios Angeletos, Gadi Barlevy, Florin Bilbiie, Ricardo Caballero, Lawrence Christiano, Martin Eichenbaum, Fran¸coisGourio, Basile Grassi, Erik Hurst, Greg Kaplan, Andrea Lanteri, Jennifer La'O, Alisdair McKay, Simon Mongey, Ernesto Pasten, Matt Rognlie, Alp Simsek, Ludwig Straub, Silvana Tenreyro, Nicholas Tra- chter, Gianluca Violante, Iv´anWerning, Johannes Wieland (our discussant), Tom Winberry, Nathan Zorzi and seminar participants at various venues, and we thank Isabel Di Tella for outstanding research assistance.