Innovating Antibodies, Improving Lives

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

Genmab Announces Data to Be Presented at 2017 ASCO Annual Meeting

Genmab Announces Data to be Presented at 2017 ASCO Annual Meeting Media Release 8 abstracts on Genmab programs scheduled for presentation at ASCO Two daratumumab oral presentations and five daratumumab poster presentations Copenhagen, Denmark; April 20, 2017 – Genmab A/S (Nasdaq Copenhagen: GEN) announced today that seven daratumumab abstracts have been accepted for presentation at the 2017 American Society of Clinical Oncology (ASCO) Annual Meeting in Chicago, June 2 – 6. These abstracts, submitted by our collaboration partner, Janssen Biotech, Inc., include updates for the POLLUX and CASTOR trials, and the first data for a Phase I study evaluating daratumumab with carfilzomib, lenalidomide and dexamethasone in front line multiple myeloma patients, which will be presented in an oral presentation. In addition, descriptions of the Phase Ib/II study of daratumumab plus atezolizumab in non-small cell lung cancer and of our Phase I/II study with HuMax-AXL-ADC are scheduled for poster presentations at the meeting. The titles of the abstracts are currently available on the ASCO website with the full abstracts scheduled to be published on May 17, 2017. “We are very pleased that, once again, a number of abstracts based on exciting work with Genmab’s innovative therapeutic antibody products have been accepted for presentation at the prestigious ASCO conference,” said Jan van de Winkel, Ph.D., Chief Executive Officer of Genmab. List of abstracts: Daratumumab: Efficacy Of Daratumumab In Combination with Lenalidomide Plus Dexamethasone (DRd) or -

Genmab's 2020 Capital Markets

WELCOME Genmab’s 2020 Capital Markets Day November 13, 2020 Webcast Live from Utrecht and Princeton Forward Looking Statement This presentation contains forward looking statements. The words “believe”, “expect”, “anticipate”, “intend” and “plan” and similar expressions identify forward looking statements. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding our financial position, business strategy, plans and objectives of management for future operations (including development plans and objectives relating to our products), are forward looking statements. Such forward looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward looking statements. Such forward looking statements are based on numerous assumptions regarding our present and future business strategies and the environment in which we will operate in the future. The important factors that could cause our actual results, performance or achievements to differ materially from those in the forward looking statements include, among others, risks associated with product discovery and development, uncertainties related to the outcome of clinical trials, slower than expected rates of patient recruitment, unforeseen safety issues resulting from the administration of our products in patients, uncertainties related to product manufacturing, the lack of market acceptance of our products, our inability to manage growth, the competitive environment in relation to our business area and markets, our inability to attract and retain suitably qualified personnel, the unenforceability or lack of protection of our patents and proprietary rights, our relationships with affiliated entities, changes and developments in technology which may render our products obsolete, and other factors. -

Second Pre-Clinical Milestone Met in Lundbeck Collaboration - €1 Million Milestone Payment to Genmab

GENMAB REACHES SECOND MILESTONE IN LUNDBECK COLLABORATION - Second pre-clinical milestone met in Lundbeck collaboration - €1 million milestone payment to Genmab Copenhagen, Denmark; February 10, 2012 – Genmab A/S (OMX: GEN) announced today it had reached the second pre-clinical milestone in the collaboration with H. Lundbeck A/S, triggering a €1 million payment. Genmab has reached the second milestone in the collaboration with H. Lundbeck A/S to create and develop human antibody therapeutics for disorders of the central nervous system (CNS). The milestone triggers a payment of €1 million to Genmab. Under the collaboration with Lundbeck Genmab creates novel human antibodies to three targets identified by Lundbeck and Lundbeck has access to Genmab’s antibody creation and development capabilities, including its state of the art, fully automated pre-clinical antibody screening and characterization capabilities and its proprietary stabilized IgG4 and UniBody therapeutic antibody platforms. Under the terms of the agreement, Genmab received an upfront payment of €7.5 million in October 2010 (approximately DKK 56 million). Lundbeck fully funds the development of the antibodies. If all milestones in the agreement are achieved, the total value of the agreement to Genmab would be approximately €38 million (approximately DKK 283 million), plus single-digit royalties. “We are very pleased to have met the in vitro proof of concept milestone for another target in the Lundbeck collaboration. This partnership is progressing well, with this second milestone coming shortly after we achieved the first preclinical milestone in December last year,” said Jan van de Winkel, Ph.D., Chief Executive Officer of Genmab. -

Classification Decisions Taken by the Harmonized System Committee from the 47Th to 60Th Sessions (2011

CLASSIFICATION DECISIONS TAKEN BY THE HARMONIZED SYSTEM COMMITTEE FROM THE 47TH TO 60TH SESSIONS (2011 - 2018) WORLD CUSTOMS ORGANIZATION Rue du Marché 30 B-1210 Brussels Belgium November 2011 Copyright © 2011 World Customs Organization. All rights reserved. Requests and inquiries concerning translation, reproduction and adaptation rights should be addressed to [email protected]. D/2011/0448/25 The following list contains the classification decisions (other than those subject to a reservation) taken by the Harmonized System Committee ( 47th Session – March 2011) on specific products, together with their related Harmonized System code numbers and, in certain cases, the classification rationale. Advice Parties seeking to import or export merchandise covered by a decision are advised to verify the implementation of the decision by the importing or exporting country, as the case may be. HS codes Classification No Product description Classification considered rationale 1. Preparation, in the form of a powder, consisting of 92 % sugar, 6 % 2106.90 GRIs 1 and 6 black currant powder, anticaking agent, citric acid and black currant flavouring, put up for retail sale in 32-gram sachets, intended to be consumed as a beverage after mixing with hot water. 2. Vanutide cridificar (INN List 100). 3002.20 3. Certain INN products. Chapters 28, 29 (See “INN List 101” at the end of this publication.) and 30 4. Certain INN products. Chapters 13, 29 (See “INN List 102” at the end of this publication.) and 30 5. Certain INN products. Chapters 28, 29, (See “INN List 103” at the end of this publication.) 30, 35 and 39 6. Re-classification of INN products. -

Interim Report for the First Quarter of 2020

Genmab Announces Financial Results for the First Quarter of 2020 May 6, 2020; Copenhagen, Denmark; Interim Report for the First Quarter Ended March 31, 2020 Highlights DARZALEX® (daratumumab) net sales increased approximately 49% compared to the first quarter of 2019 to USD 937 million, resulting in royalty income of DKK 775 million DARZALEX approved in Europe in combination with bortezomib, thalidomide and dexamethasone for the treatment of adult patients with newly diagnosed multiple myeloma who are eligible for autologous stem cell transplant U.S. FDA approved TEPEZZA™ (teprotumumab-trbw), developed and commercialized by Horizon Therapeutics, for thyroid eye disease U.S. FDA accepted, with priority review, Novartis’ supplemental Biologics License Application for subcutaneous ofatumumab in relapsing multiple sclerosis Anthony Pagano appointed Chief Financial Officer Anthony Mancini appointed Chief Operating Officer “Despite the unprecedented challenges posed by the coronavirus (COVID-19) pandemic, we will continue to invest in our innovative proprietary products, technologies and capabilities and use our world-class expertise in antibody drug development to create truly differentiated products with the potential to help cancer patients. While Genmab is closely monitoring the developments in the rapidly evolving landscape, we are extremely fortunate to have a solid financial foundation and a fabulous and committed team to carry us through these uncertain times,” said Jan van de Winkel, Ph.D., Chief Executive Officer of Genmab. Financial Performance First Quarter of 2020 Revenue was DKK 892 million in the first quarter of 2020 compared to DKK 591 million in the first quarter of 2019. The increase of DKK 301 million, or 51%, was mainly driven by higher DARZALEX royalties. -

Portfolio of Investments

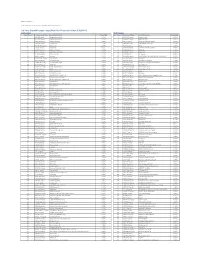

PORTFOLIO OF INVESTMENTS CTIVP® – Lazard International Equity Advantage Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.6% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 6.9% Finland 1.0% AGL Energy Ltd. 437,255 4,269,500 Metso OYJ 153,708 2,078,669 ASX Ltd. 80,181 4,687,834 UPM-Kymmene OYJ 36,364 1,106,808 BHP Group Ltd. 349,229 9,021,842 Valmet OYJ 469,080 11,570,861 Breville Group Ltd. 153,867 2,792,438 Total 14,756,338 Charter Hall Group 424,482 3,808,865 France 9.5% CSL Ltd. 21,611 4,464,114 Air Liquide SA 47,014 7,452,175 Data#3 Ltd. 392,648 1,866,463 Capgemini SE 88,945 11,411,232 Fortescue Metals Group Ltd. 2,622,808 30,812,817 Cie de Saint-Gobain(a) 595,105 24,927,266 IGO Ltd. 596,008 1,796,212 Cie Generale des Etablissements Michelin CSA 24,191 2,596,845 Ingenia Communities Group 665,283 2,191,435 Electricite de France SA 417,761 4,413,001 Kogan.com Ltd. 138,444 2,021,176 Elis SA(a) 76,713 968,415 Netwealth Group Ltd. 477,201 5,254,788 Legrand SA 22,398 1,783,985 Omni Bridgeway Ltd. 435,744 1,234,193 L’Oreal SA 119,452 38,873,153 REA Group Ltd. 23,810 1,895,961 Orange SA 298,281 3,106,763 Regis Resources Ltd. -

Targeting Costimulatory Molecules in Autoimmune Disease

Targeting costimulatory molecules in autoimmune disease Natalie M. Edner1, Gianluca Carlesso2, James S. Rush3 and Lucy S.K. Walker1 1Institute of Immunity & Transplantation, Division of Infection & Immunity, University College London, Royal Free Campus, London, UK NW3 2PF 2Early Oncology Discovery, Early Oncology R&D, AstraZeneca, Gaithersburg, MD, USA 3Autoimmunity, Transplantation and Inflammation Disease Area, Novartis Institutes for Biomedical Research, Basel, Switzerland *Correspondence: Professor Lucy S.K. Walker. Institute of Immunity & Transplantation, Division of Infection & Immunity, University College London, Royal Free Campus, London, UK NW3 2PF. Tel: +44 (0)20 7794 0500 ext 22468. Email: [email protected]. 1 Abstract Therapeutic targeting of immune checkpoints has garnered significant attention in the area of cancer immunotherapy, and efforts have focused in particular on the CD28 family members CTLA-4 and PD-1. In autoimmunity, these same pathways can be targeted to opposite effect, to curb the over- exuberant immune response. The CTLA-4 checkpoint serves as an exemplar, whereby CTLA-4 activity is blocked by antibodies in cancer immunotherapy and augmented by the provision of soluble CTLA-4 in autoimmunity. Here we review the targeting of costimulatory molecules in autoimmune disease, focusing in particular on the CD28 family and TNFR family members. We present the state-of-the-art in costimulatory blockade approaches, including rational combinations of immune inhibitory agents, and discuss the future opportunities and challenges in this field. 2 The risk of autoimmune disease is an inescapable consequence of the manner in which the adaptive immune system operates. To ensure effective immunity against a diverse array of unknown pathogens, antigen recognition systems based on random gene rearrangement and mutagenesis have evolved to anticipate the antigenic universe. -

Portfolio of Investments

PORTFOLIO OF INVESTMENTS Variable Portfolio – Partners International Value Fund, September 30, 2020 (Unaudited) (Percentages represent value of investments compared to net assets) Investments in securities Common Stocks 97.9% Common Stocks (continued) Issuer Shares Value ($) Issuer Shares Value ($) Australia 4.2% UCB SA 3,232 367,070 AMP Ltd. 247,119 232,705 Total 13,350,657 Aurizon Holdings Ltd. 64,744 199,177 China 0.6% Australia & New Zealand Banking Group Ltd. 340,950 4,253,691 Baidu, Inc., ADR(a) 15,000 1,898,850 Bendigo & Adelaide Bank Ltd. 30,812 134,198 China Mobile Ltd. 658,000 4,223,890 BlueScope Steel Ltd. 132,090 1,217,053 Total 6,122,740 Boral Ltd. 177,752 587,387 Denmark 1.9% Challenger Ltd. 802,400 2,232,907 AP Moller - Maersk A/S, Class A 160 234,206 Cleanaway Waste Management Ltd. 273,032 412,273 AP Moller - Maersk A/S, Class B 3,945 6,236,577 Crown Resorts Ltd. 31,489 200,032 Carlsberg A/S, Class B 12,199 1,643,476 Fortescue Metals Group Ltd. 194,057 2,279,787 Danske Bank A/S(a) 35,892 485,479 Harvey Norman Holdings Ltd. 144,797 471,278 Demant A/S(a) 8,210 257,475 Incitec Pivot Ltd. 377,247 552,746 Drilling Co. of 1972 A/S (The)(a) 40,700 879,052 LendLease Group 485,961 3,882,083 DSV PANALPINA A/S 15,851 2,571,083 Macquarie Group Ltd. 65,800 5,703,825 Genmab A/S(a) 1,071 388,672 National Australia Bank Ltd. -

Quarterly Commentary—Artisan Non-U.S. Small-Mid Growth Strategy

QUARTERLY Artisan Non-U.S. Small-Mid Growth Strategy FactCommentary Sheet As of 30 June 2019 Investment Process We seek long-term investments in high-quality businesses exposed to structural growth themes that can be acquired at sensible valuations in a contrarian fashion and are led by excellent management teams. Investing with Tailwinds We identify structural themes at the intersection of growth and change with the objective of investing in companies having meaningful exposure to these trends. Themes can be identified from both bottom-up and top-down perspectives. High-Quality Businesses We seek future leaders with attractive growth characteristics that we can own for the long term. Our fundamental analysis focuses on those companies exhibiting unique and defensible business models, high barriers to entry, proven management teams, favorable positions within their industry value chains and high or improving returns on capital. In short, we look to invest in small companies that have potential to become large. A Contrarian Approach to Valuation We seek to invest in high-quality businesses in a contrarian fashion. Mismatches between stock price and long-term business value are created by market dislocations, temporary slowdowns in individual businesses or misperceptions in the investment community. We also examine business transformation brought about by management change or restructuring. Manage Unique Risks of International Small- and Mid-Cap Equities International small- and mid-cap equities are exposed to unique investment risks that require managing. We define risk as permanent loss of capital, not share price volatility. We manage this risk by having a long-term ownership focus, understanding the direct and indirect security risks for each business, constructing the portfolio on a well-diversified basis and sizing positions according to individual risk characteristics. -

Immunfarmakológia Immunfarmakológia

Gergely: Immunfarmakológia Immunfarmakológia Prof Gergely Péter Az immunpatológiai betegségek döntő többsége gyulladásos, és ennek következtében általában szövetpusztulással járó betegség, melyben – jelenleg – a terápia alapvetően a gyulladás csökkentésére és/vagy megszűntetésére irányul. Vannak kizárólag gyulladásgátló gyógyszereink és vannak olyanok, amelyek az immunreakció(k) bénításával (=immunszuppresszió révén) vagy emellett vezetnek a gyulladás mérsékléséhez. Mind szerkezetileg, mind hatástanilag igen sokféle csoportba oszthatók, az alábbi felosztás elsősorban didaktikus célokat szolgál. 1. Nem-szteroid gyulladásgátlók (‘nonsteroidal antiinflammatory drugs’ NSAID) 2. Kortikoszteroidok 3. Allergia-elleni szerek (antiallergikumok) 4. Sejtoszlás-gátlók (citosztatikumok) 5. Nem citosztatikus hatású immunszuppresszív szerek 6. Egyéb gyulladásgátlók és immunmoduláns szerek 7. Biológiai terápia 1. Nem-szteroid gyulladásgátlók (NSAID) Ezeket a vegyületeket, melyek őse a szalicilsav (jelenleg, mint acetilszalicilsav ‘aszpirin’ használatos), igen kiterjedten alkalmazzák a reumatológiában, az onkológiában és az orvostudomány szinte minden ágában, ahol fájdalom- és lázcsillapításra van szükség. Egyes felmérések szerint a betegek egy ötöde szed valamilyen NSAID készítményt. Szerkezetük alapján a készítményeket több csoportba sorolhatjuk: szalicilátok (pl. acetilszalicilsav) pyrazolidinek (pl. fenilbutazon) ecetsav származékok (pl. indometacin) fenoxiecetsav származékok (pl. diclofenac, aceclofenac)) oxicamok (pl. piroxicam, meloxicam) propionsav -

The Two Tontti Tudiul Lui Hi Ha Unit

THETWO TONTTI USTUDIUL 20170267753A1 LUI HI HA UNIT ( 19) United States (12 ) Patent Application Publication (10 ) Pub. No. : US 2017 /0267753 A1 Ehrenpreis (43 ) Pub . Date : Sep . 21 , 2017 ( 54 ) COMBINATION THERAPY FOR (52 ) U .S . CI. CO - ADMINISTRATION OF MONOCLONAL CPC .. .. CO7K 16 / 241 ( 2013 .01 ) ; A61K 39 / 3955 ANTIBODIES ( 2013 .01 ) ; A61K 31 /4706 ( 2013 .01 ) ; A61K 31 / 165 ( 2013 .01 ) ; CO7K 2317 /21 (2013 . 01 ) ; (71 ) Applicant: Eli D Ehrenpreis , Skokie , IL (US ) CO7K 2317/ 24 ( 2013. 01 ) ; A61K 2039/ 505 ( 2013 .01 ) (72 ) Inventor : Eli D Ehrenpreis, Skokie , IL (US ) (57 ) ABSTRACT Disclosed are methods for enhancing the efficacy of mono (21 ) Appl. No. : 15 /605 ,212 clonal antibody therapy , which entails co - administering a therapeutic monoclonal antibody , or a functional fragment (22 ) Filed : May 25 , 2017 thereof, and an effective amount of colchicine or hydroxy chloroquine , or a combination thereof, to a patient in need Related U . S . Application Data thereof . Also disclosed are methods of prolonging or increasing the time a monoclonal antibody remains in the (63 ) Continuation - in - part of application No . 14 / 947 , 193 , circulation of a patient, which entails co - administering a filed on Nov. 20 , 2015 . therapeutic monoclonal antibody , or a functional fragment ( 60 ) Provisional application No . 62/ 082, 682 , filed on Nov . of the monoclonal antibody , and an effective amount of 21 , 2014 . colchicine or hydroxychloroquine , or a combination thereof, to a patient in need thereof, wherein the time themonoclonal antibody remains in the circulation ( e . g . , blood serum ) of the Publication Classification patient is increased relative to the same regimen of admin (51 ) Int . -

Citi Pure Growth Europe Long-Short Net TR Series II Index (CIISGRE2)

Date: 23-May-21 Index Weights as of monthly rebalance date 12-May-21 Citi Pure Growth Europe Long-Short Net TR Series II Index (CIISGRE2) Long Exposure Short Exposure Constituent Bloomberg Ticker Constituent Name Weight(%) Constituent Bloomberg Ticker Constituent Name Weight(%) 1 AAL LN Equity Anglo American Plc 1.62% 1 1COV GY Equity Covestro AG -0.89% 2 ACA FP Equity Credit Agricole SA 1.37% 2 ABBN SE Equity ABB LTD-REG -0.31% 3 ADM LN Equity Admiral Group 0.09% 3 ABF LN Equity Associated British Foods -0.62% 4 ADS GY Equity Adidas AG 1.01% 4 ABN NA Equity ABN AMRO Group NV -1.24% 5 ADYEN NA Equity Adyen NV 2.43% 5 AC FP Equity Accor -1.54% 6 AD NA Equity Ahold NV 0.61% 6 ADEN SE Equity ADECCO GROUP AG-REG -0.49% 7 AHT LN Equity Ashtead Group 0.24% 7 AENA SQ Equity AENA SA -1.05% 8 ALC SE Equity ALCON AG CHF0.04 0.70% 8 AGN NA Equity Aegon NV -0.71% 9 ALFA SS Equity Alfa Laval AB 0.11% 9 AI FP Equity Air Liquide -0.69% 10 ALO FP Equity Alstom 0.45% 10 AKZA NA Equity AKZO NOBEL NV EUR0.50(POST REV SPLIT) -0.37% 11 AMBUB DC Equity Ambu A/S 1.41% 11 ALV GY Equity Allianz SE -0.79% 12 AMP IM Equity Amplifon SpA 0.45% 12 AMS SQ Equity Amadeus IT Hldg SA -1.78% 13 ANTO LN Equity Antofagasta Hldgs 1.62% 13 VNA GY Equity Deutsche Annington Immobilien -0.27% 14 ASM NA Equity ASM Intl 0.65% 14 ASSAB SS Equity Assa Abloy B -1.11% 15 ASML NA Equity ASML Holding NV 0.82% 15 ATCOA SS Equity Atlas Copco AB A -0.68% 16 ATO FP Equity AtoS 0.51% 16 ATCOB SS Equity Atlas Copco AB B -0.66% 17 AZN LN Equity AstraZeneca Plc 0.38% 17 AV/ LN Equity Aviva -0.07%