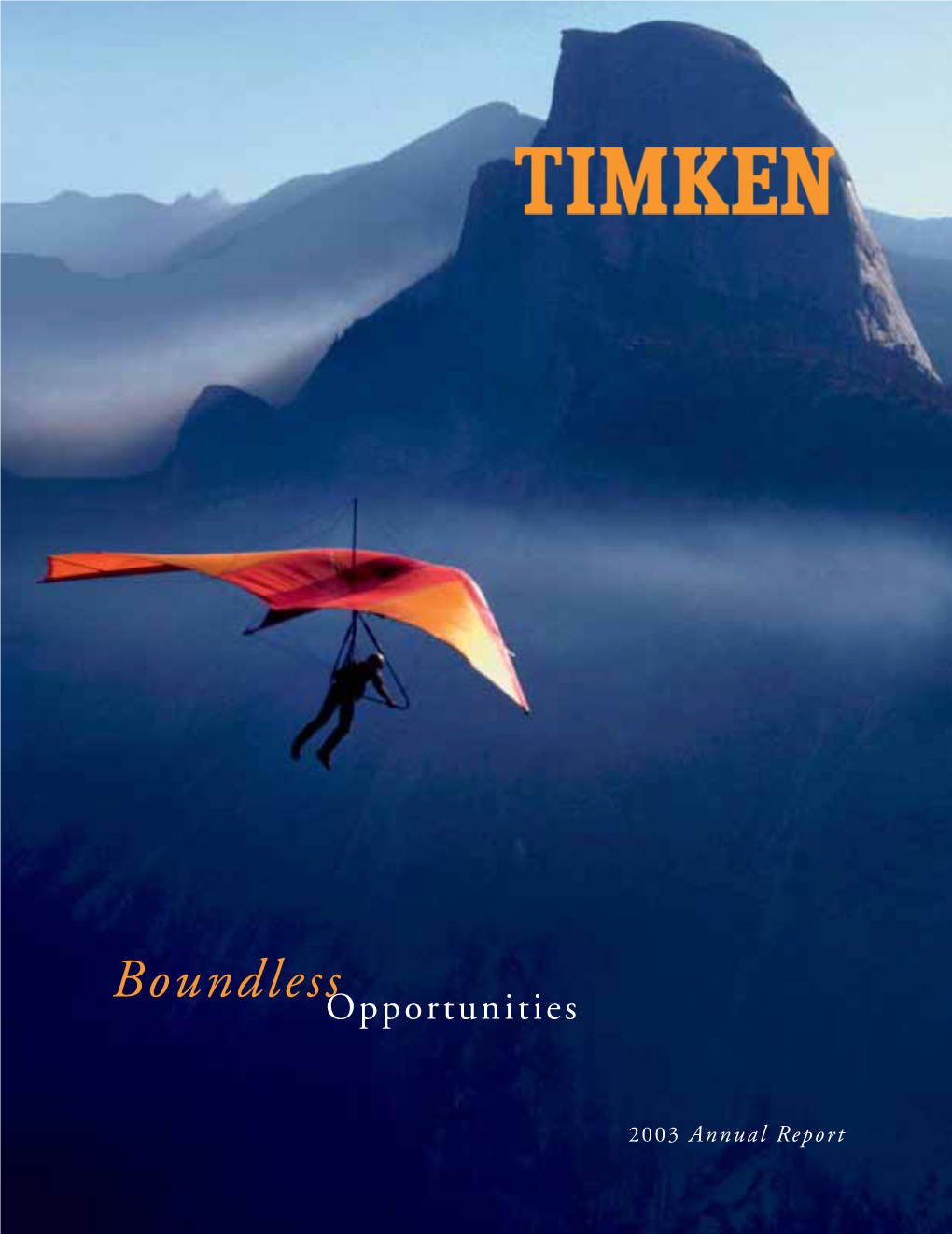

View Annual Report

Total Page:16

File Type:pdf, Size:1020Kb

Load more

Recommended publications

-

GLASTONBURY Remedial Investigation Remediation Monitoring Remediation Name Address Site Definition Started Started Started Completed ELUR ELUR Type

List of Contaminated or Potentially Contaminated Sites “Hazardous Waste Facilities” as defined by Section 22a-134f of the Connecticut General Statutes Post TOWN OF: GLASTONBURY Remedial Investigation Remediation Monitoring Remediation Name Address Site Definition Started Started Started Completed ELUR ELUR Type 19 Kenneth Street Llc 19 Kenneth Street Leaking Underground Storage Tanks – Completed 2749 Main St (former Shell 2749 Main Street Leaking Underground Storage Service Station #136313) Tanks – Completed 45 School St., Llc (formerly 45 School Street Leaking Underground Storage Carl's Garage) Tanks – Completed 7-eleven #32960 3041 Main Street Leaking Underground Storage Tanks – Completed 81 Commerce Road 81 Commerce Road Leaking Underground Storage Tanks – Completed A C Fonda Enterprises (former 381 Hebron Avenue Leaking Underground Storage Dufford Drilling) Tanks – Completed Aaabon Pest Control 2 Mill Street Leaking Underground Storage Tanks – Pending Anthony Dignoti 70 Oakwood Drive Leaking Underground Storage Tanks – Completed Arbor Acres Farm, Inc. 429 Marlborough Rd. Leaking Underground Storage Tanks – Rem. Started Arbor Acres Farm, Inc. 429 Marlborough Road Property Transfer – Form III 4/1/2009 Investigation started Arbor Acres Farm, Inc. 429 Marlborough Road Property Transfer - Form III Post 10/8/2008 NO Remedial Monitoring Started Arbor Acres 439 Marlboro Rd. Leaking Underground Storage Residence Tanks – Investigation Astro Enterprises Inc. 44 Commerce Street Property Transfer – Form III 1/25/2005 Investigation started Battistons -

Notice of 2013 Annual Meeting of Shareholders and Proxy Statement

Notice of 2013 Annual Meeting of Shareholders and Proxy Statement THE TIMKEN COMPANY Canton, Ohio U.S.A. 1300100_1_64sc.pdf 2 3/14/13 5:01 PM TABLE OF CONTENTS PAGE Chairman’s Letter ……………………………………………………………………………….… 2 Notice of Annual Meeting ………………………………………………………………………... 3 Proxy Statement ………………………………………………………………………………….. 5 Election of Directors ………………………………………………………………………… 5 Election of Directors (Item No. 1) ………………………………………..……………. 5 Nominees ………………………………………………………………………………… 6 Director Compensation ………………………………….………………………………….. 11 2012 Director Compensation Table………………………………………………………… 12 Board Leadership Structure ………………………………………………………………... 13 Risk Oversight ……………………………………………………………………………….. 13 Audit Committee ……………………………………………………………………………... 14 Audit Committee Report ………………………………………………………………..…… 14 Compensation Committee ………………………………………………………………….. 14 Compensation Committee Report ……………………………………………………….… 15 Nominating and Corporate Governance Committee ………………………………….…. 16 Beneficial Ownership of Common Stock ………………………………………………….. 17 Compensation Discussion and Analysis ……………………………………….……….… 20 Executive Compensation …………………………………………………………….…..…. 32 Ratification of Appointment of Independent Auditors (Item No. 2) ……………………... 44 Auditors ……………………………………………………………………………………….. 45 Shareholder Advisory Vote on Named Executive Officer Compensation (Item No. 3).. 45 Amendments to the Company’s Amended Articles of Incorporation to Reduce Certain Shareholder Voting Requirements (Item No. 4)……………………………….… 46 Amendments to the Company’s Amended -

United States Securities and Exchange Commission Washington, D.C

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 FORM 10-K (Mark One) [ X ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [FEE REQUIRED] For the fiscal year ended: May 31, 1997 or [ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [NO FEE REQUIRED] For the transition period from ______________ to _______________ Commission File Number: 0-23996 SCHMITT INDUSTRIES, INC. (Exact name of registrant as specified in its charter) Oregon 91-1151989 (State or other jurisdiction of (IRS Employer Identification Number) incorporation or organization) 2765 N.W. Nicolai Street Portland, Oregon 97210 (Address of principal executive offices) (Zip Code) (503) 227-7908 (Registrant's telephone number, including area code) Securities registered pursuant to Section 12(b) of the Act: Title of each class Name of each exchange on which registered - ---------------------------- --------------------------------------------- None None Securities registered pursuant to Section 12(g) of the Act: Common Stock - no par value (Title of each class) Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes X No --- --- Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. -

Certain Bearings from China, 731-Ta-344, 391A, 392A

CERTAIN BEARINGS FROM CHINA, 731-TA-344, 391A, 392A (SECOND REVIEW) FRANCE, GERMANY, ITALY, JAPAN, 731-TA-392C, 393A, 394A (SECOND REVIEW) SINGAPORE, AND THE UNITED KINGDOM 731-TA-396 and 399A (SECOND REVIEW) AMENDED PUBLIC SERVICE LIST I, Marilyn R. Abbott, hereby certify that the parties listed have entered an appearance in the above captioned investigation, and a copy of the PUBLIC CERTIFICATE OF SERVICE was served upon the following parties via first class mail and air mail where necessary. ONLY PUBLIC INFORMATION IS TO BE SERVED ON THE PARTIES LISTED BELOW. Served April 20, 2006. *NOTE: Changes to personnel. /s/ ___________________________ Marilyn R. Abbott, Secretary U.S. International Trade Commission 500 E Street, SW Suite 112A Washington, DC 20436 Behalf of NSK, Ltd.; NSK Europe Ltd; NSK Corporation and Japan Bearing Behalf of New Hampshire Ball Bearings; Industrial Association: NMB Singapore, Ltd.; Pelmec Industries (Pte), Ltd. and NMB Technologies Corp.: Matthew P. Jaffe, Esq. CROWELL MORING Christopher F. Corr, Esq. 1001 Pennsylvania Avenue, NW WHITE AND CASE Washington, DC 20004-2595 701 Thirteenth Street, N.W. Washington, D.C. 20005 Behalf of Pacamor Kubar Bearings, RBC Bearings and The Timken Company: Behalf of SKF, USA, Inc.; SKF GmbH, SKF France, S.A.; Sarma; SKF Industrie, Erick P. Salonen, Esq. S.p.A.; and SKF Aeroengine Bearings STEWART AND STEWART UK: 2100 M Street, NW Washington, DC 20037 Herbert C. Shelley, Esq. STEPTOE AND JOHNSON Behalf of NTN Corporation; NTN Bearing 1330 Connecticut Avenue, NW Corporation of America; American NTN Washington, DC 20036-1795 Bearing Manufacturing Corporation; NTN-BCA Corporation and NTN Behalf of Peer Bearing Company: Driveshaft, Inc.: John M. -

Companies That Have Matching Gift Programs and Will Match to Christian-Based Charities (This List Is Not Comprehensive)

Companies that Have Matching Gift Programs and will Match to Christian-Based Charities (this list is not comprehensive) Key: * Match U.S. employees only A - Donor must be an alumna/us P - Permanent part-time employees are eligible D - Directors are also eligible R - Retirees are also eligible S - Spouses are also eligible W - Widows and widowers are also eligible M - Greater than 1 to 1 match -A Allstate Foundation of Canada D,R Allstate Giving Campaign and Matching Program ABB Altria Group Inc Asea Brown Boveri Inc. D,R Aluminium Company of America D,R,M Abbott Laboratories and Fund *D,R,S AMD Matching Gift Program Abbott Northwestern Center for Outpatient Surgery Amdahl Canada Limited ABN AMRO Bank American Express Co. D,R,M ACE INA Foundation American Express Foundation & Matching Gift ACE Limited Program Acromental Companies Inc American General Corporation D,S,M Acxiom Corporation American Home Products D,R ADC Telecommunications American International Group (AIG) R,S Addison-Wesley Publishers Ltd. American Mutual Insurance Companies Addison-Wesley Publishing Company, Inc. A,P,D,S American National Bank Adeptec Inc American Standard, Inc. D Adobe Systems Inc America's Charities ADP Foundation Ameriprise Philanthropic Program Adria Laboratories R Ameritech Corporation and Foundation D,R,M AES Corporation Amgen Foundation / Amgen PAC-Match Gift Program Aetna Canada P,D,R Amoco Canada Petroleum D,R,M Aetna Foundation, Inc./Partners In Community Giving Amoco Corporation D,R,M Aetna Life & Casualty P,D,R,S,W AMSCO International, Inc. A AGIA Inc Anadarko Petroleum Corporation D,R,S,W Agribank FCB Analog Devices D Agriliance Analysts International Corp, Minneapolis AIG Matching Grants Program Analytical Group Inc. -

Givingleaders in LEVELS of GIVING Bronze

LEADERS IN Giving2017 United Way of Greater Stark County 1 “Greater Stark County is fortunate to have leaders like you! You are our community’s most exciting and influential force, giving local kids, families and individuals hope for a better tomorrow.” GivingLEADERS IN LEVELS OF GIVING Bronze............................$1,000 - $1,499 Pewter............................$1,500 - $2,499 Silver...............................$2,500 - $4,999 Gold................................$5,000 - $7,499 Platinum.........................$7,500 - $9,999 Alexis de Tocqueville.............$10,000+ Maria Heege President & CEO United Way of Greater Stark County CONTENTS Officers & Board of Directors .. ..............................4 Leaders in Giving, Pewter ............................20 - 21 New Branding .. .....................................................5 Leaders in Giving, Bronze ........................... 22 - 25 Work in the Community ...................................6 - 7 Corporate & Foundation Gifts..............................26 Alexis de Tocqueville Society........................8 - 15 Corporate & Foundation Gifts by Firm..........27 - 28 Alexis de Tocqueville Society Mentors...............16 Women United Members..............................29 - 30 New Alexis de Tocqueville Society Members......16 Campaign Message............................................31 Leaders in Giving Platinum.................................17 Campaign Awards...............................................32 Leaders in Giving, Gold.......................................17 -

Corporate Match Companies Only

Corporate Matching Companies A A D P Foundation A D Phelps, Jr. Charitable Foundation, Inc. A H Williams & Co Aid Association for Lutherans (AAL) Abbott Laboratories ABN-AMRO ADC Telecommunications Addison-Wesley Advanta Foundation Aeroquip-Vickers AES Corporation Aetna, Inc. Air & Water Technologies Cor Air Liquide America Corporation Air Products and Chemicals Akzo America Albany International Albertson's Alcan Alco Standard Corp Alcoa Alexander & Baldwin Alco Standard Corporation Allegro Micro Systems W G Inc Allendale Insurance Company AllFirst Alliance Capital Mgm Corp Alliant Techsystems Allied Signal Alliant Energy Foundation Alliant Techsystems Incl Allied Signal Foundation, Inc Allmerica Financial Allstate Foundation Amerada Hess Corp American Cyanamid Company American Express American General Corp. American Home Products American International Group American Medical Security American Home Products Corporation American Honda Motor Co Inc. American Express Co. American Express Financial Advisors Inc. American International Group American National Bank American Ref-Fuel American Re-Insurance Company American Standard, Inc American Stock Exchange Ameritech Amoco AMSTED Industries Ameritech Amica Mutual Insurance Co Amoco, Inc. AMP Incorporated AMSCO International, Inc. American Brands Amsted Industries Foundation Anadarko Petroleum Corporatio Analog Devices inc. Anchor Capitol Advisors Inc. Anderson Consulting Foundation AON Foundation Aramark Archer Daniels Midland Foundation ARCO Chemical Co. Arkwright Foundation, Inc. Arthur Andersen LLP Armstrong World Industries, Inc. Asarco Foundation Asea Brown Boveri Inc AT&T Auto Alliance International Inc. Automatic Data Processing Avery Dennison Corp. Avon Products Astoria Federal Savings AstraZeneca LP AT & T Atlantic Electric Aurther Andersen Consulting Anheuser-Busch Aon Corp. Apple Computers Inc. Appleton Papers Aramark Archer Daniel Midland ARCO Arkwright Mutual Insurance Co. -

Only Class 3110 Aerospace Roller Bearings Granted a Waiver from The

LIST CURRENT AS OF 17 SEPTEMBER 2013 List of Class 3110, Aerospace Roller Bearings that have been granted a Waiver from the Non-Manufacturing Rule (NMR) Legend: All of the below bearing Federal Stock Numbers begin with a class-designation of 3110 and are then followed by 9 digits (ex. 000045095), which identifies the specific bearing Below each bold Federal Stock Number are the CAGE codes and names of approved manufacturers of that bearing o The CAGE code is listed first and the name of the manufacturer is below each CAGE code (ex. NTN BEARING CORPORATION OF AMERICA with their CAGE code [0LTL1] listed above ) 000045095 0LTL1 NTN BEARING CORPORATION OF AMERICA 60038 THE TIMKEN CORPORATION Z0992 AUSTRALIAN TIMKEN PTY LTD 000389332 52676 SKF USA INC. 77107 PARAGON POWER INC SUB OF GREAT LAKES 000519119 13499 1 | P a g e LIST CURRENT AS OF 17 SEPTEMBER 2013 ROCKWELL COLLINS INC. DIV GOVERNMENT 40920 MPB CORPORATION DBA TIMKEN SUPER PRE 50294 NEW HAMPSHIRE BALL BEARINGS, INC. DB 000616154 40920 MPB CORPORATION DBA TIMKEN SUPER PRE 83086 NEW HAMPSHIRE BALL BEARINGS INC. DIV 000866964 0LTL1 NTN BEARING CORPORATION OF AMERICA 52676 SKF USA INC. 001000268 0LTL1 NTN BEARING CORPORATION OF AMERICA 3D6E9 AXLETECH INTERNATIONAL LLC 60038 THE TIMKEN CORPORATION 78500 MERITOR HEAVY VEHICLE SYSTEMS LLC DI F0272 2 | P a g e LIST CURRENT AS OF 17 SEPTEMBER 2013 SKF FRANCE F0704 THE TIMKEN COMPANY H2229 RDM TECHNOLOGY B.V. 001000271 06085 BAE SYSTEMS LAND & ARMAMENTS L.P. BA 0LTL1 NTN BEARING CORPORATION OF AMERICA 45152 OSHKOSH CORPORATION 60038 THE TIMKEN CORPORATION 001000282 04627 NACCO MATERIALS HANDLING GROUP INC 0LTL1 NTN BEARING CORPORATION OF AMERICA 60038 THE TIMKEN CORPORATION F0272 SKF FRANCE F0704 THE TIMKEN COMPANY 3 | P a g e LIST CURRENT AS OF 17 SEPTEMBER 2013 001000285 0LTL1 NTN BEARING CORPORATION OF AMERICA 11083 CATERPILLAR INC. -

Final STATEMENT of BRIAN J. RUEL VICE PRESIDENT, THE

Final CERTAIN TAPERED ROLLER BEARINGS FROM THE REPUBLIC OF KOREA INV. No. 731-TA-1380 (FINAL) HEARING BEFORE THE UNITED STATES INTERNATIONAL TRADE COMMISSION JUNE 5, 2018 STATEMENT OF BRIAN J. RUEL VICE PRESIDENT, THE AMERICAS THE TIMKEN COMPANY Good morning, Chairman Schmidtlein, Commissioners and Commission staff My name is Brian Ruel. I am the Vice President for the Americas at The Timken Company. In my current role, I oversee all aspects of customer contacts in the Americas such as sales, application engineering and service engineering. I have responsibility for sales to both OEM customers and our distributors regardless of particular market such as automotive, heavy truck, various industrial, rail and so on. This is my 34th year in the bearing industry, and with Timken. I have been in my current role since the beginning of 2016. As Chris Coughlin just testified, tapered roller bearings come in a wide range of sizes, but in the market there are meaningful distinctions between small diameter TRBs (those that are 8" or smaller) and large diameter TRBs (those larger than 8"). The tapered roller bearing was invented to address a problem that vehicles were having handling cornering loads. Not surprisingly, the largest use of TRBs in the market continues to be automotive and heavy truck customers. Nearly 100% of these customers need and use 0-8" TRBs. There is a distinct automotive aftermarket which consists of distributors and dealers/service operations catering to automobiles and trucks. Replacement parts, like those used by OEM customers, are nearly all 0- 1 Final 8" in OD. -

Corporate Matching Funds

Increase the size of your gift with a Matching Gift! 1. What is a Matching Gift Program? 2. How does a Matching Gift Program Work? 3. Does it work? 4. List of companies that have Matching Gift Programs? 1. What is a Matching Gift Program? Many companies allow their employees to direct their charitable giving programs through matching gifts. When an employee notifies the company that he/she has made a charitable donation, the company will make a gift of the same amount, and in some cases double the amount, to the same charitable organization. Matching Gift Programs are a wonderful way for employees to make their charitable dollars stretch farther at no cost to themselves. Simply ask your company's human resources office for a matching gift form and we will do the rest! Below is a partial list of companies with matching gift programs. Even if you do not find your employer on this list, be sure to check with your human resources office, personnel department, or community relations office. 2. How does a Matching Gift Program Work? It is extremely easy to process. Gift matching procedures can vary from company to company. The following example is typical. 1. An employee/retiree gets a matching gift form from the employer, usually from the human resource department or company website. 2. After completing the form, the employee/retiree sends it along with the donation to the educational institution or nonprofit charity. 3. The nonprofit certifies on the form that it has received the gift and meets the company’s guidelines for receiving a matching gift. -

2014-2015 Internship Survey Report

Case Western Reserve University Career Center Internship Report 2014-2015 Internship Survey 2014‐15 Introduction The 2014‐15 Internship Survey was administered using Qualtrics, a web‐based assessment vendor, over approximately four weeks during August – September 2015 to 3,931 returning undergraduate students. Students were asked to report on their internship experiences over the time period Fall 2014 – Summer 2015. There were 1,511 individuals who responded to the survey for a response rate of 38%. Appendix A includes a copy of the survey. Internship Participation Students were asked whether or not they had participated in an internship, defined as a work‐based learning experience, typically related to one’s major field of study and/or intended career, which could be full‐time or part‐time, paid or unpaid, with no course enrollment. Six hundred forty students reported that they participated in one internship within this timeframe; 29 students reported participating in two internships; for a total of 669 internships reported. Timing Of the 669 internships reported, 633 (95%) had information about which semester(s) the internship took place. Ninety‐three percent (n=587) took place during one semester, six percent (n=36) took place over two semesters, and two percent (n=10) nine took place over three semesters. Summer was the most popular time of year for students to complete internships with 550 (87%) taking place exclusively during the summer, and 37 more taking place over summer plus one or more semesters. Timing n % Fall 2014 20 3% Spring 2015 17 3% Summer 2015 550 87% Fall 2014, Spring 2015 9 1% Fall 2014, Summer 2015 3 0% Spring 2015, Summer 2015 24 4% Fall 2014, Spring 2015, Summer 2015 10 2% Qualifications Six hundred (90%) responses were recorded regarding the relationship between student’s major and internship. -

Ball Bearings and Parts Thereof from Japan and United Kingdom

UNITED STATES DEPARTMENT OF COMMERCE International Tr·ade Adminis tration Washington, D.C. 20230 A-588-804 A-421-801 Admin. Rev. 5/1/09-4/30/10 Public Document AD/CVD I: AFBs Team June 13, 2014 MEMORANDUM TO: Lynn Fischer Fox Deputy Assistant Secretary for Policy and Negotiations FROM: Christian Marsh ~ Deputy Assistant Secretary for Antidumping and Countervailing Duty Operations SUBJECT: Issues and Decision Memorandum for the Antidumping Duty Administrative Reviews ofBall Bearings and Parts Thereof from Japan and the United Kingdom; 2009-2010 Summary We analyzed the case and rebuttal briefs of interested parties in the administrative reviews of the antidumping duty orders on ball bearings and parts thereof (ball bearings) from Japan and the United Kingdom for the period May 1, 2009, through April30, 2010. As a result of our analysis, we have made changes, including corrections of certain inadvertent programming and other errors, in the margin calculations. We recommend that you approve the positions we developed in the Discussion ofthe Issues section of this memorandum. Background On April21, 2011, the Department of Commerce (Department) published the preliminary results of the administrative reviews of the antidumping duty orders on ball bearings and parts thereof from Japan and the United Kingdom. 1 The period of reviews is May 1, 2009, through April30, 2010. We invited interested parties to comment on the Preliminary Results. We received case and rebuttal briefs from various parties to these reviews? On July 15, 2011 , the Department discontinued these reviews.3 1 See Ball Bearings and Parts ThereofF rom France, Germany, Italy, Japan, and the United Kingdom: Preliminary Results ofAntidumping Administrative and Changed-Circumstances Reviews, 76 FR 22372 (April21, 2011) (Preliminary Results).